Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Introduction & Market Context

Hovnanian Enterprises Inc (NYSE:HOV) released its second quarter fiscal 2025 results on May 20, revealing year-over-year declines in key financial metrics that fell short of analyst expectations. The homebuilder’s stock dropped 8.82% following the announcement, closing at $100.16, as investors reacted to the earnings miss despite the company meeting most of its own guidance targets.

The results come amid ongoing challenges in the housing market, with high mortgage rates continuing to impact buyer affordability and demand. Hovnanian’s presentation highlighted both the company’s operational strategies to navigate these headwinds and its strong competitive positioning on key metrics relative to industry peers.

Quarterly Performance Highlights

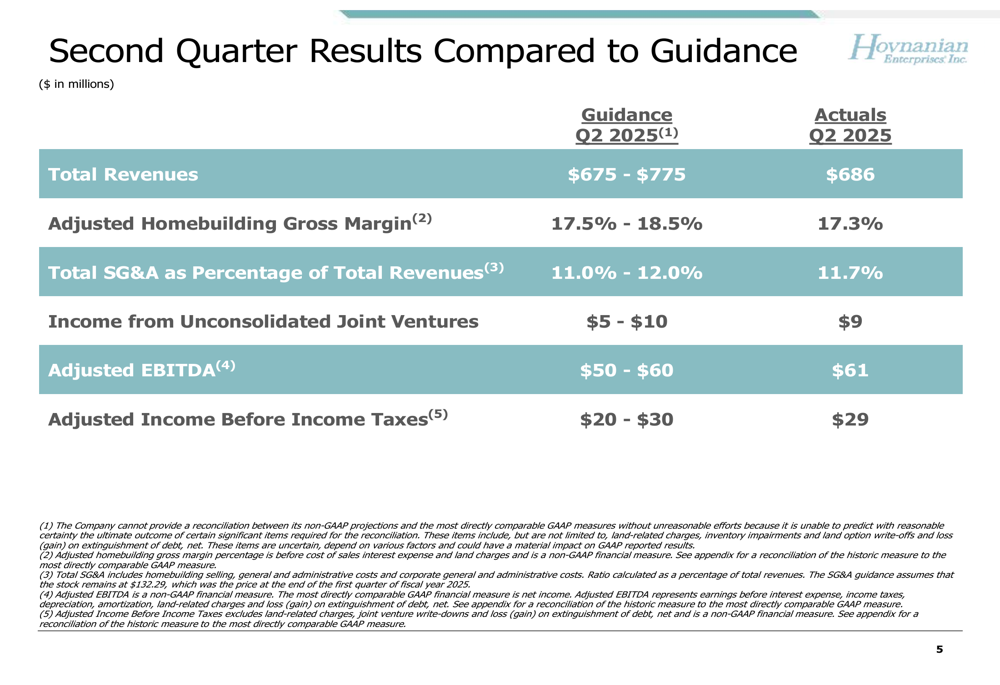

Hovnanian reported total revenues of $686 million for Q2 2025, near the low end of its guidance range of $675-775 million but significantly below analyst expectations of $821.8 million. The company’s adjusted homebuilding gross margin came in at 17.3%, slightly below its guidance of 17.5-18.5%, while adjusted income before income taxes reached $29 million, within the guided range of $20-30 million.

As shown in the following comparison of Q2 2025 results against guidance:

Year-over-year comparisons revealed more concerning trends, with total revenues declining from $708 million in Q2 2024 to $686 million in Q2 2025. The adjusted gross margin saw a substantial drop from 22.6% to 17.3%, while total SG&A as a percentage of total revenues increased from 11.2% to 11.7%. Most notably, adjusted income before income taxes fell by more than half, from $70 million to $29 million.

The company also reported a 7% year-over-year decrease in contracts, with 1,629 contracts in Q2 2025 compared to 1,761 in Q2 2024. Monthly contract data showed mixed results, with February declining 17%, March increasing 3%, and April declining 9% compared to the same months in 2024.

Strategic Initiatives

Hovnanian continues to employ several key strategies to navigate the challenging housing market environment. The company has maintained its focus on mortgage rate buydowns, with 75% of homebuyers utilizing this incentive in Q2 2025, consistent with recent quarters. This approach helps address affordability concerns amid elevated mortgage rates.

The company has also continued to expand its community count, growing from 132 communities in Q2 2024 to 148 communities in Q2 2025, a 12% increase. This growth is expected to continue through fiscal 2025, providing a foundation for potential volume increases.

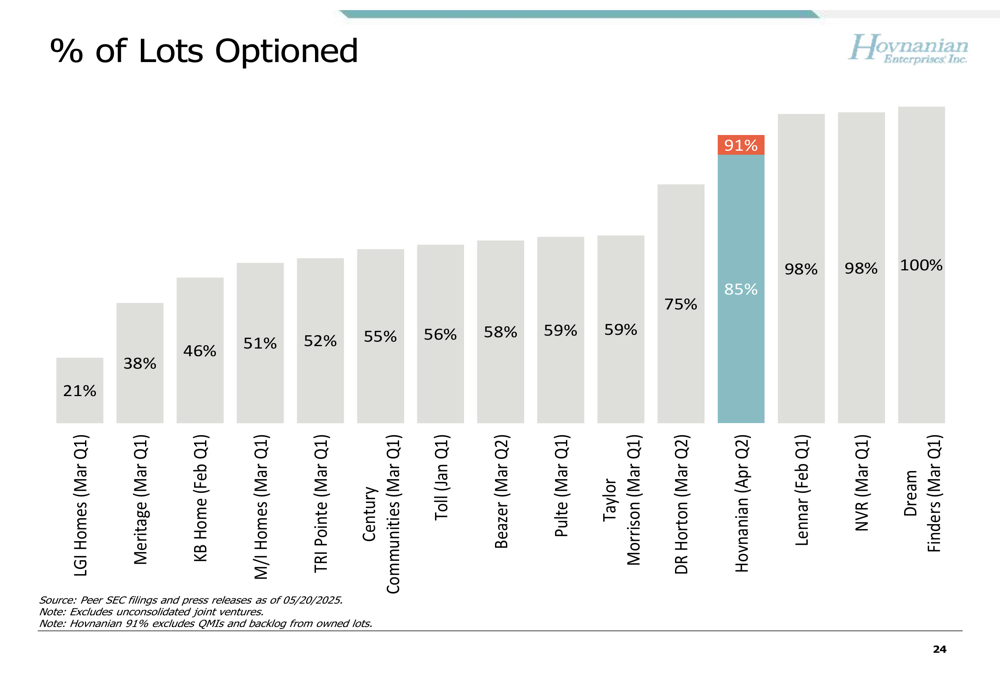

One of Hovnanian’s most distinctive strategies is its emphasis on optioning land rather than owning it outright. The company has increased its percentage of optioned lots to 85% in Q2 2025, up from 80% in Q2 2024. This approach provides flexibility while reducing capital requirements and risk.

As shown in the following peer comparison, Hovnanian’s 85% optioned lots (91% when excluding quick move-ins and backlog from owned lots) places it among the industry leaders in this metric:

The company has also benefited from a 7% reduction in base construction costs per square foot, which helps partially offset margin pressures from incentives and price adjustments.

Competitive Industry Position

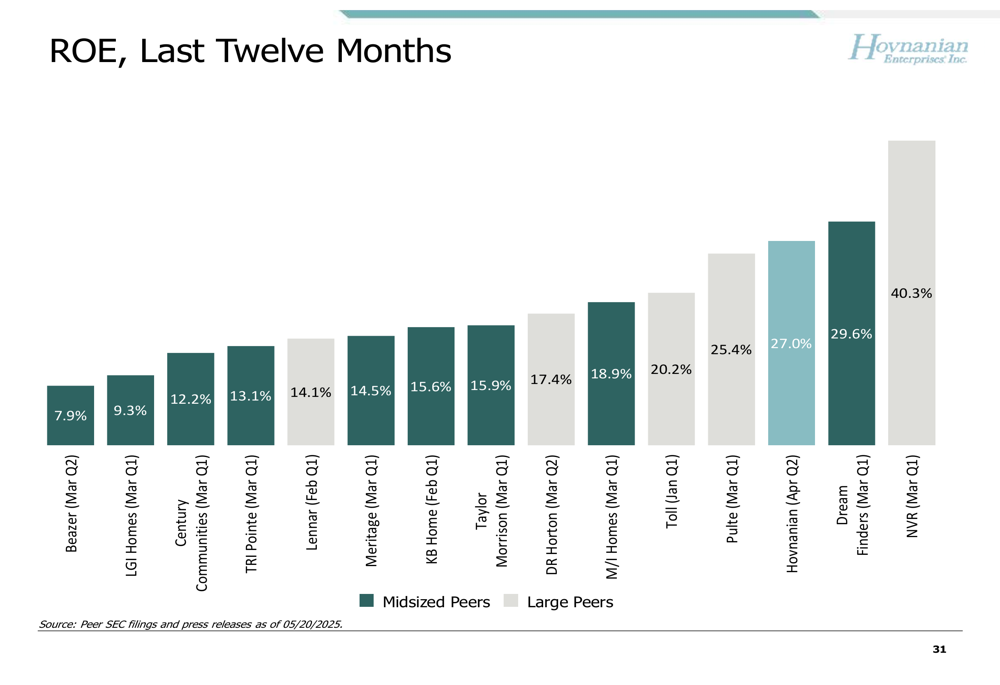

Despite the earnings miss and year-over-year declines, Hovnanian maintains strong competitive positioning on several key metrics compared to industry peers. The company’s return on equity (ROE) for the last twelve months stands at 27.0%, ranking third among homebuilders behind only Dream Finders and NVR (NYSE:NVR):

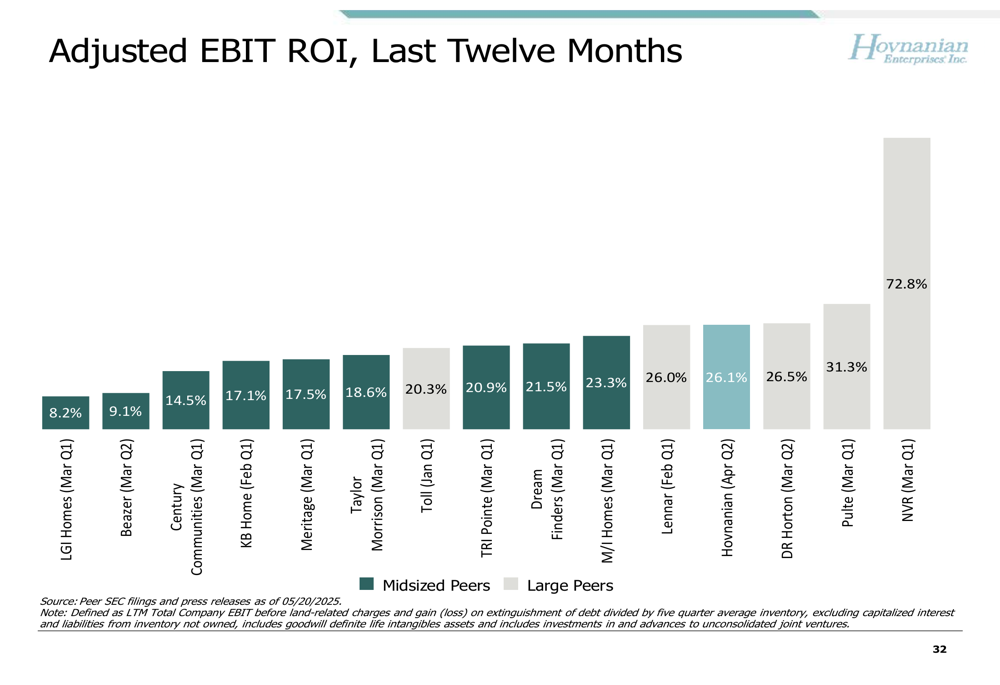

Similarly, Hovnanian’s adjusted EBIT return on investment (ROI) of 26.1% places it in the top tier of the industry:

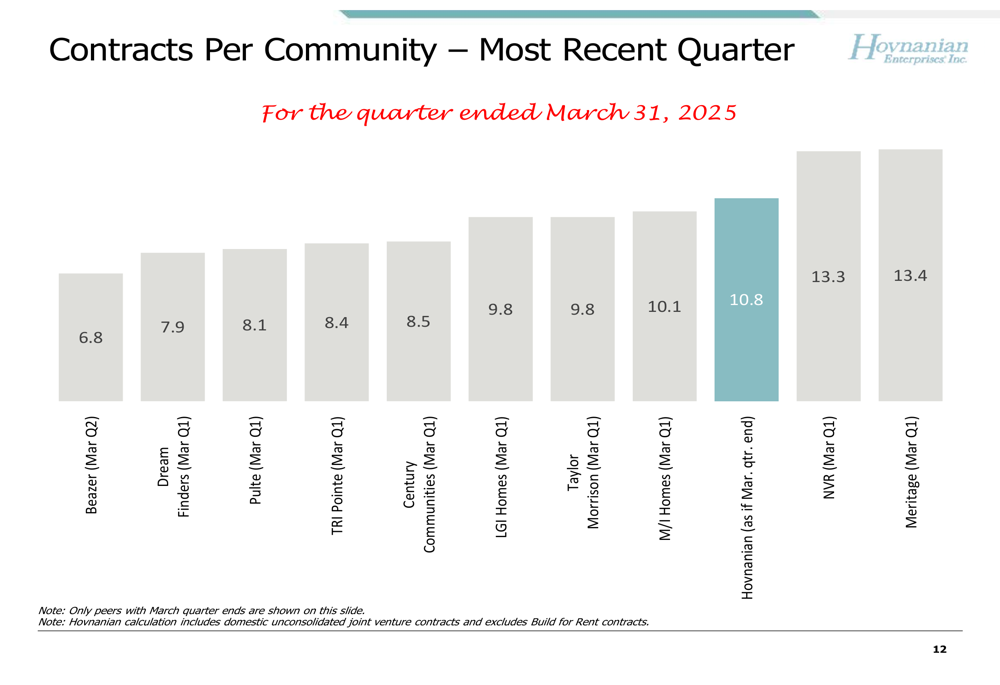

The company’s contracts per community metric of 10.8 for the quarter ended March 31, 2025, also compares favorably to most peers, ranking fourth in the industry:

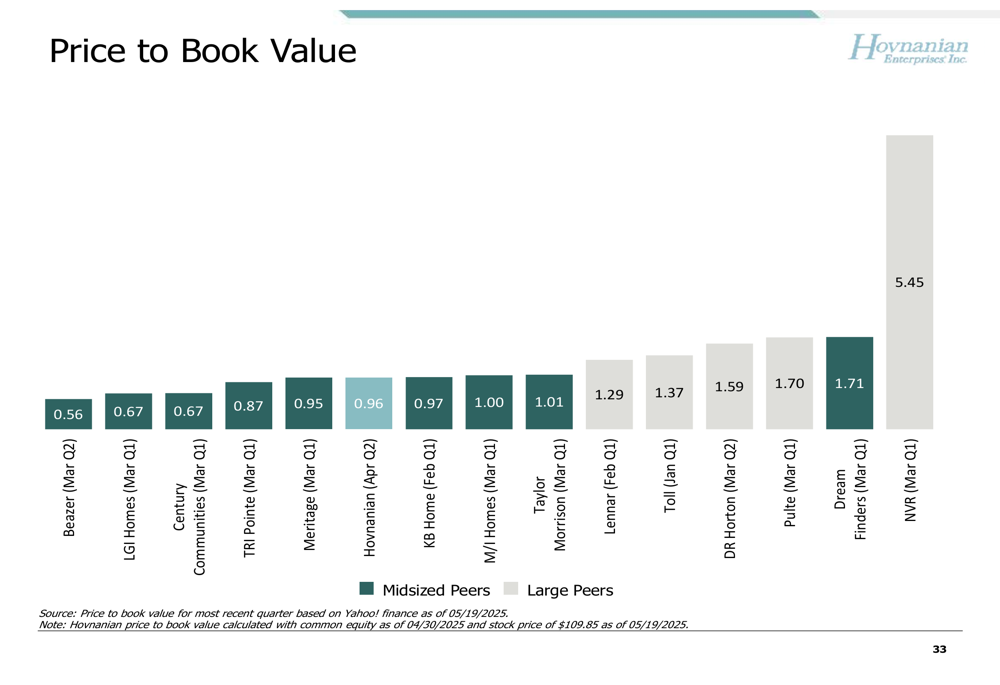

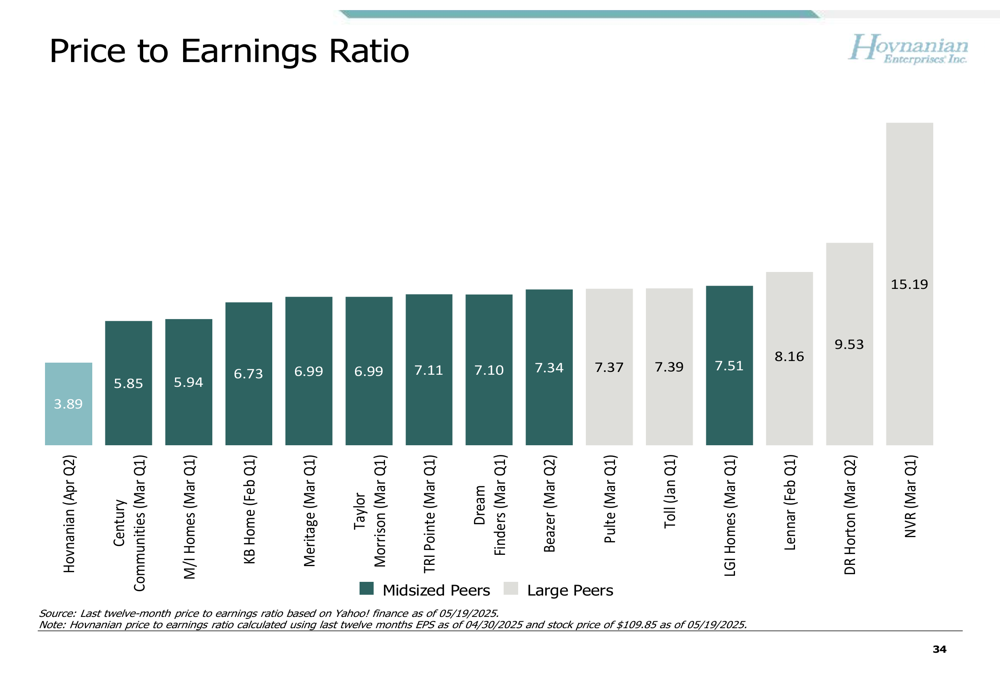

Perhaps most notably, Hovnanian trades at significant valuation discounts compared to peers, with a price-to-book value of 0.96 (below the theoretical fair value of 1.0) and a price-to-earnings ratio of just 3.89, the lowest among all public homebuilders:

These valuation metrics suggest potential undervaluation if the company can stabilize its financial performance and demonstrate sustainable growth.

Balance Sheet Improvements & Liquidity

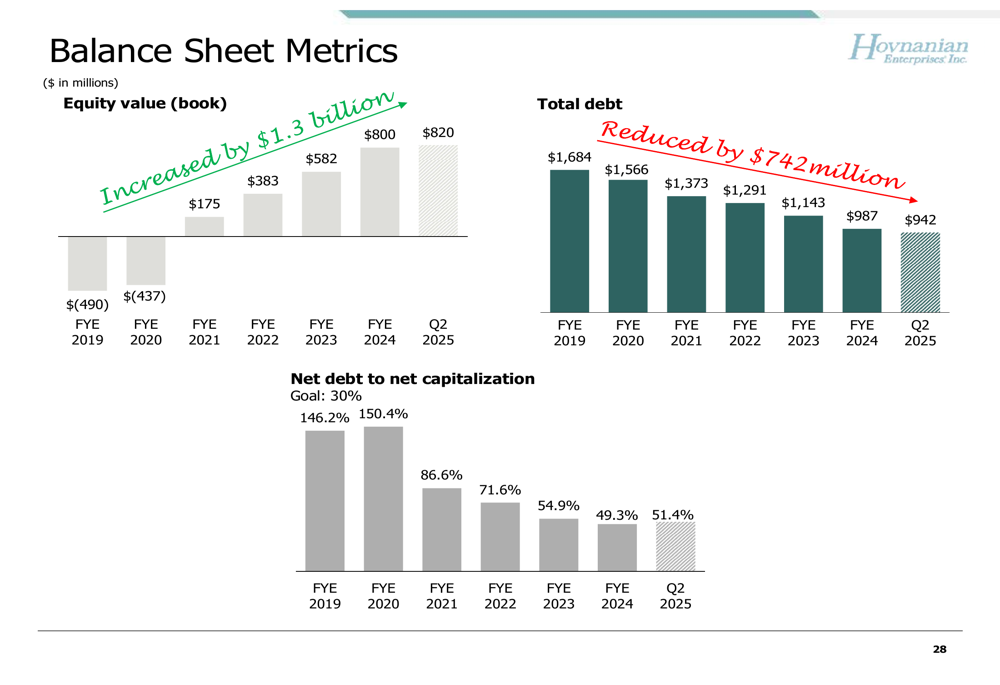

Hovnanian has made substantial progress in strengthening its balance sheet over recent years. The company’s equity value has increased from negative $(490) million in fiscal year 2019 to $820 million in Q2 2025, while total debt has been reduced from $1,684 million to $942 million over the same period:

In Q2 2025, the company redeemed $27 million of 13.5% senior notes due February 2026, continuing its debt reduction efforts. The company’s liquidity position as of April 30, 2025, stood at $202 million, consisting of $77 million in homebuilding cash and $125 million in revolver availability.

Forward-Looking Statements

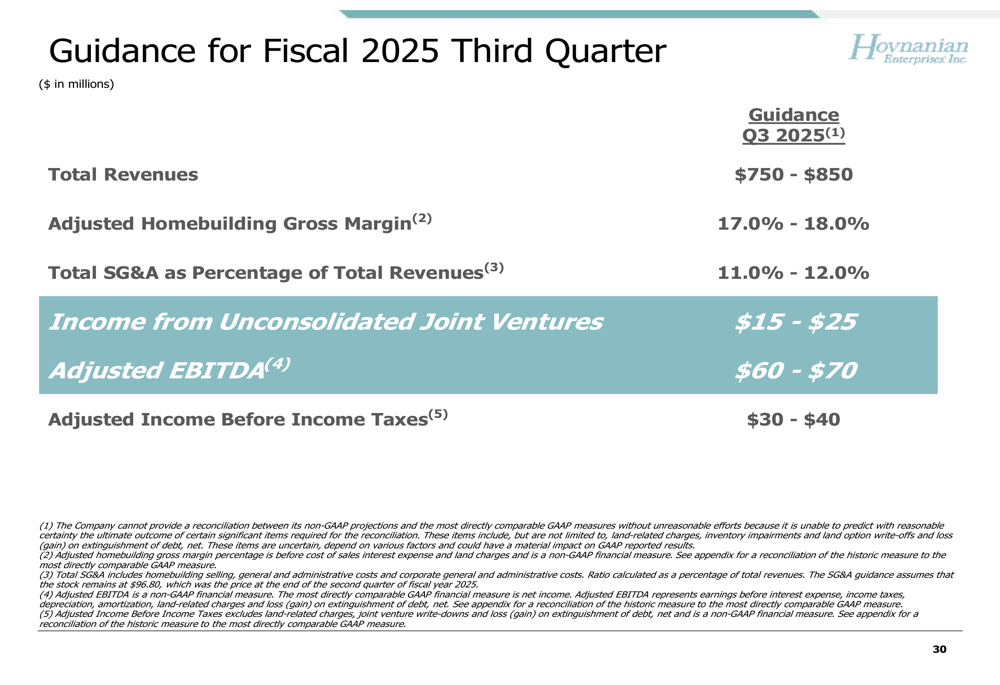

Looking ahead to the third quarter of fiscal 2025, Hovnanian provided guidance that suggests modest sequential improvement:

The company expects total revenues between $750-850 million, adjusted homebuilding gross margin between 17.0-18.0%, and adjusted income before income taxes between $30-40 million. This guidance reflects a cautious outlook amid ongoing market challenges.

During the earnings call, CEO Ara Hovnanian expressed satisfaction with the quarter "given the difficult environment," while CFO Brad O’Connor emphasized the company’s valuation, stating, "We believe our stock continues to be the most undervalued in the entire universe of public homebuilders."

The company’s focus on community count growth, lot optioning, and mortgage rate buydowns remains central to its strategy as it navigates the challenging housing market environment. However, investors appear focused on the near-term earnings miss and year-over-year declines, as reflected in the stock’s negative price reaction following the results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.