Veeco launches Lumina+ MOCVD system, receives Rocket Lab order

Introduction & Market Context

Hovnanian Enterprises Inc (NYSE:HOV) presented its third-quarter fiscal 2025 results on August 21, showing revenue growth but continued margin pressure in a challenging housing market. Despite meeting or exceeding guidance across key metrics, the stock fell 11.24% during the trading session, reflecting investor concerns about future profitability amid high mortgage rates and economic uncertainty.

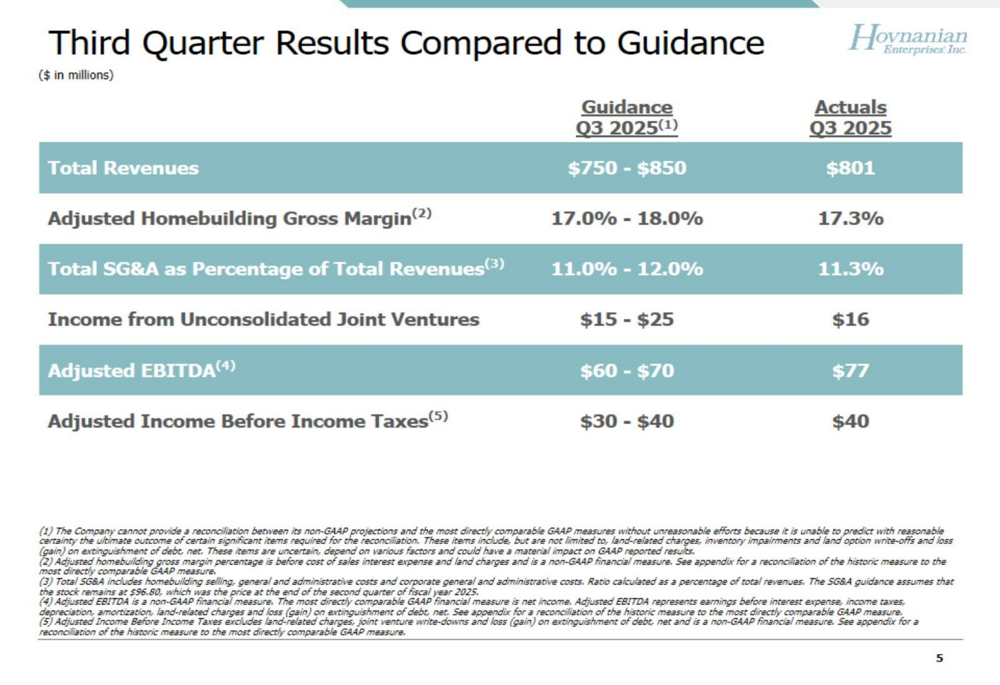

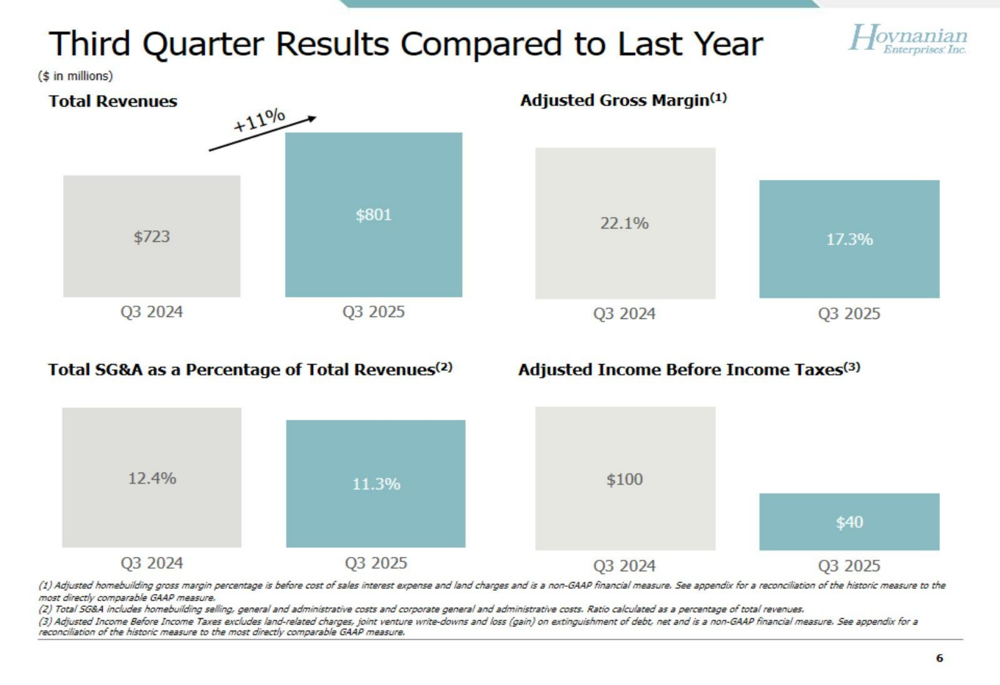

The homebuilder reported total revenues of $801 million, representing an 11% increase year-over-year, while adjusted income before income taxes reached $40 million, at the high end of the company’s guidance range but significantly below the $100 million reported in the same quarter last year.

Quarterly Performance Highlights

Hovnanian’s third-quarter performance largely aligned with or exceeded the company’s previously issued guidance across all key metrics. Total (EPA:TTEF) revenues of $801 million fell within the guided range of $750-850 million, while adjusted EBITDA of $77 million surpassed the upper end of guidance ($60-70 million).

As shown in the following comparison of actual results versus guidance:

Year-over-year comparisons reveal mixed results. While revenue grew by 11% compared to Q3 2024, adjusted gross margin declined significantly from 22.1% to 17.3%, and adjusted income before income taxes fell by 60% from $100 million to $40 million. This margin compression reflects ongoing challenges in the housing market, including elevated costs and pricing pressures.

The following chart illustrates these year-over-year changes:

Contract activity showed modest improvement, with total contracts including joint ventures increasing 1% year-over-year to 1,416 units. Monthly contract trends improved throughout the quarter, from a 4% decline in May to a 7% increase in July, suggesting potentially improving market conditions heading into the fourth quarter.

Strategic Initiatives

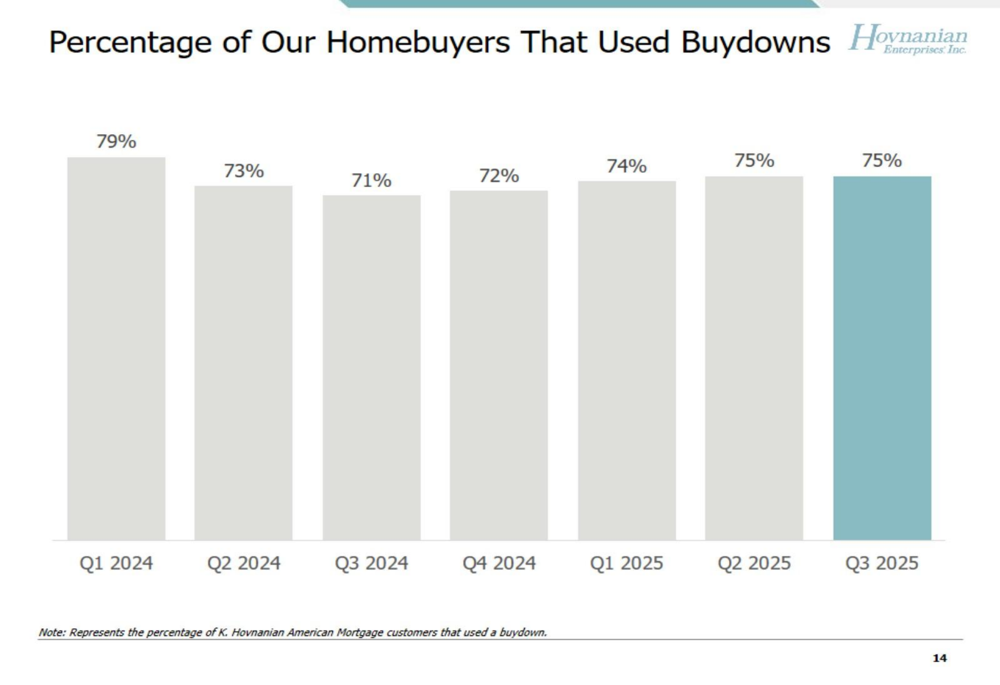

Hovnanian continues to rely heavily on mortgage rate buydowns as a key sales strategy, with 75% of homebuyers utilizing this option in Q3 2025, consistent with the previous quarter. This high percentage underscores the ongoing impact of elevated mortgage rates on buyer affordability.

The following chart shows the consistent reliance on buydowns over recent quarters:

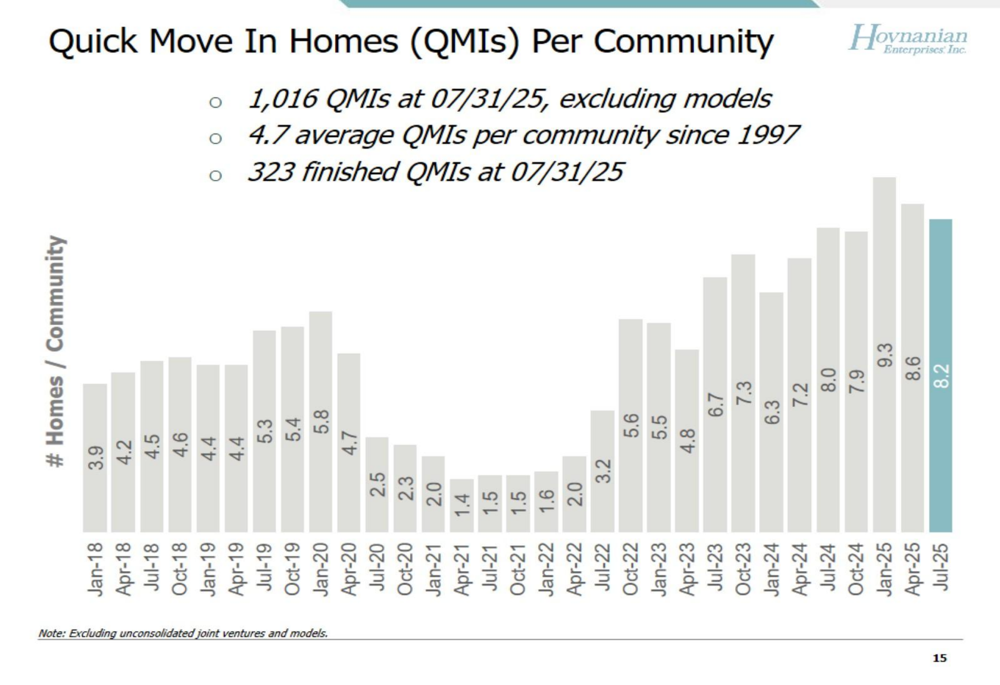

The company has been gradually reducing its inventory of Quick Move-In (QMI) homes, with 1,016 units as of July 31, 2025, representing an 8.2 QMI per community ratio. This marks a 13% reduction from January 2025 levels, suggesting a more disciplined approach to inventory management.

As illustrated in this trend of QMIs per community:

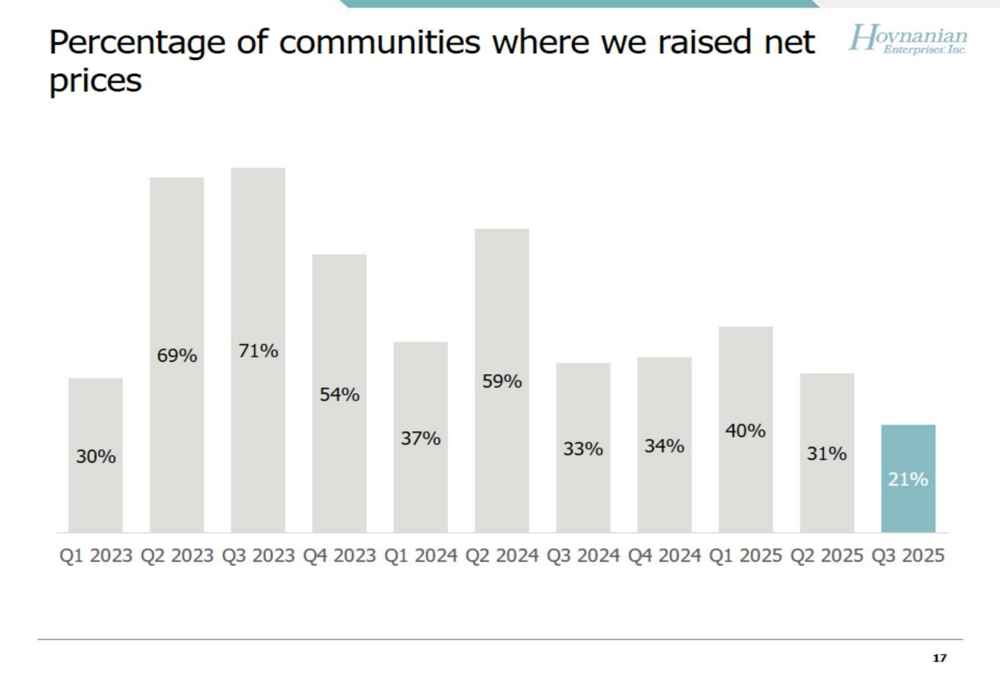

Pricing power continues to weaken across Hovnanian’s communities, with only 21% of communities implementing net price increases in Q3 2025, down from 33% in Q3 2024 and significantly below the peak of 71% in Q3 2023. This trend reflects the competitive market environment and affordability challenges.

The following chart shows this declining trend in pricing power:

Competitive Industry Position

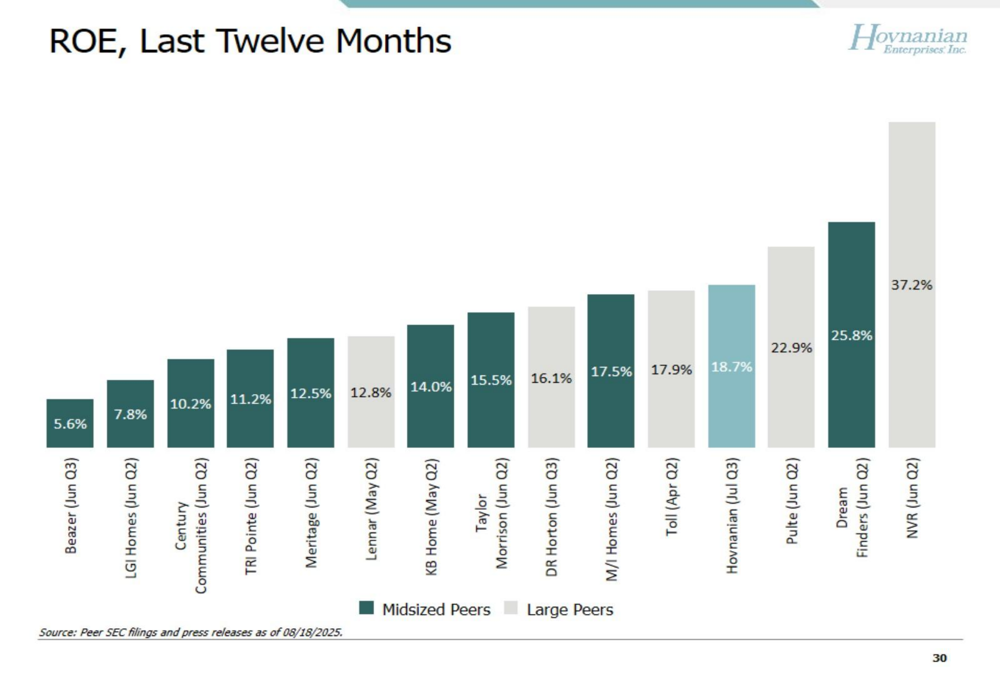

Despite market challenges, Hovnanian maintains strong performance metrics relative to peers. The company ranks third among homebuilders in Return on Equity (ROE) at 18.7%, behind only NVR (NYSE:NVR), Pulte, and Dream Finders.

The following chart compares ROE across the homebuilding sector:

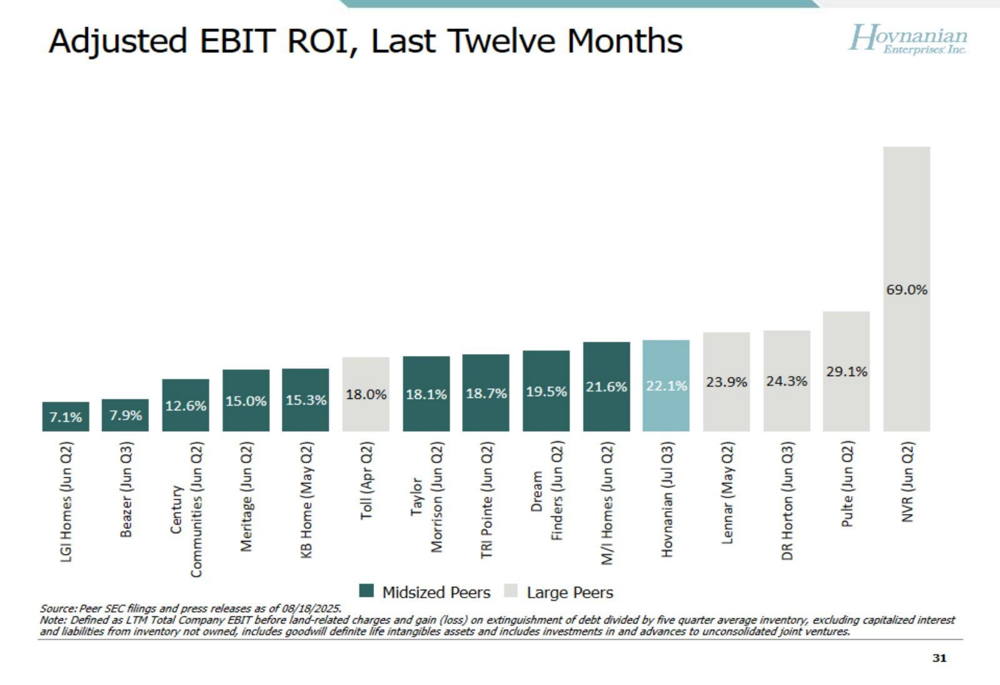

Similarly, Hovnanian ranks fifth in Adjusted EBIT Return on Investment (ROI) at 22.1%, demonstrating efficient capital utilization despite margin pressures.

As shown in this industry comparison:

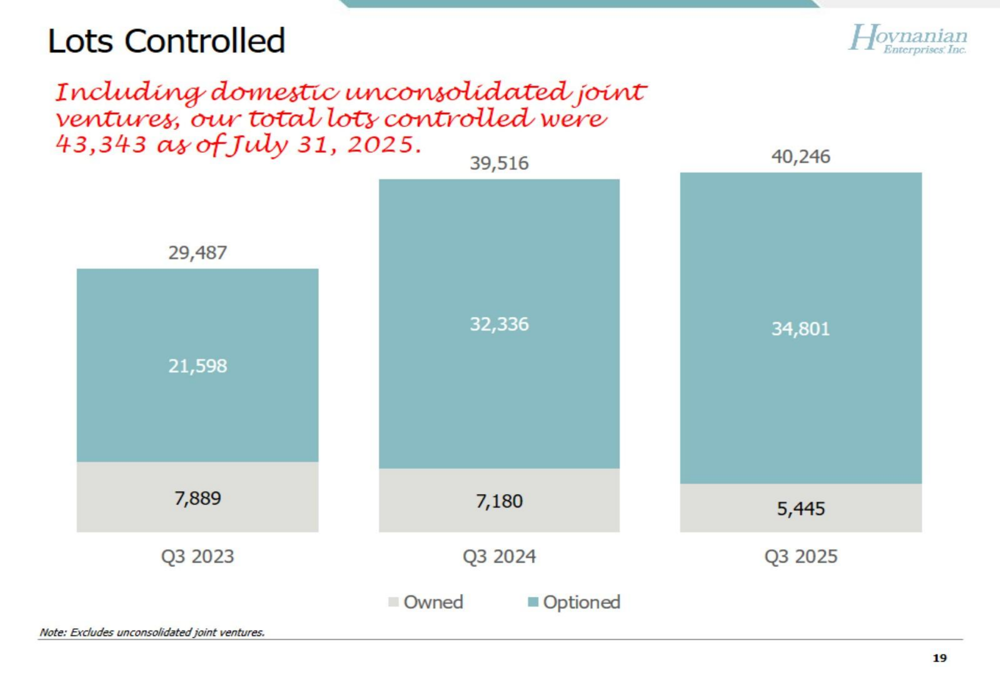

The company’s land strategy remains focused on optioned lots, which represent 86% of total lots controlled as of Q3 2025, the highest percentage among peers. This approach reduces capital requirements and mitigates risk in an uncertain market environment.

The following chart shows Hovnanian’s lots controlled, with the increasing proportion of optioned lots:

Forward-Looking Statements

Looking ahead to the fourth quarter of fiscal 2025, Hovnanian provided guidance that suggests continued revenue stability but further margin compression. The company expects total revenues between $750-850 million, unchanged from Q3 guidance, but projects adjusted homebuilding gross margin to decline to 15.0-16.5%, down from the 17.3% achieved in Q3.

Despite margin pressure, Hovnanian forecasts adjusted income before income taxes to increase to $45-55 million in Q4, up from $40 million in Q3, likely driven by expected improvements in joint venture income and operational efficiencies.

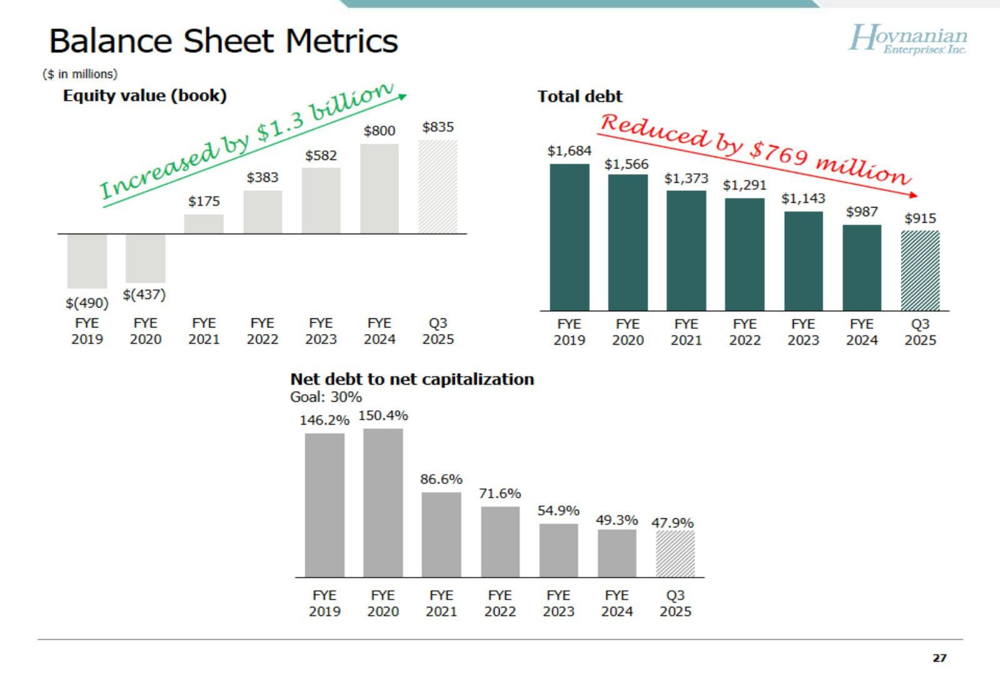

The company’s balance sheet metrics show significant improvement over recent years, with equity value increasing by $1.3 billion and total debt reduced by $769 million. Net debt to capitalization stands at 47.9% as of Q3 2025.

As illustrated in these key balance sheet metrics:

Market Reaction and Valuation

Despite meeting or exceeding Q3 guidance and maintaining strong relative performance metrics, Hovnanian’s stock dropped 11.24% following the presentation. This reaction likely reflects concerns about declining margins and the challenging outlook for the housing market amid persistent high mortgage rates.

The company continues to trade at a significant discount to peers, with a price-to-earnings ratio of 7.24, the lowest among public homebuilders. This valuation disconnect persists despite Hovnanian’s superior ROE and competitive EBIT ROI metrics, suggesting investor skepticism about the sustainability of performance in the current housing environment.

The stock’s performance follows a challenging second quarter, when Hovnanian missed analyst expectations with an EPS of $2.43 against projections of $7.52. While the third quarter showed improved execution relative to guidance, the outlook for further margin compression in Q4 appears to have overshadowed these improvements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.