S&P 500 rises as health care, tech gain to overshadow Fed independence concerns

Introduction & Market Context

Hubbell Inc (NYSE:HUBB) reported its first quarter 2025 results on May 1, revealing a modest decline in financial performance while maintaining its full-year outlook. The electrical and power company’s stock fell 4.5% to $346.83 following the earnings release, as investors reacted to results that fell short of analyst expectations.

The company’s presentation highlighted a challenging quarter marked by tariff pressures and raw material cost increases, but emphasized accelerating order momentum in its Grid Infrastructure business and strong performance in its Electrical Solutions segment, particularly in datacenter markets.

Quarterly Performance Highlights

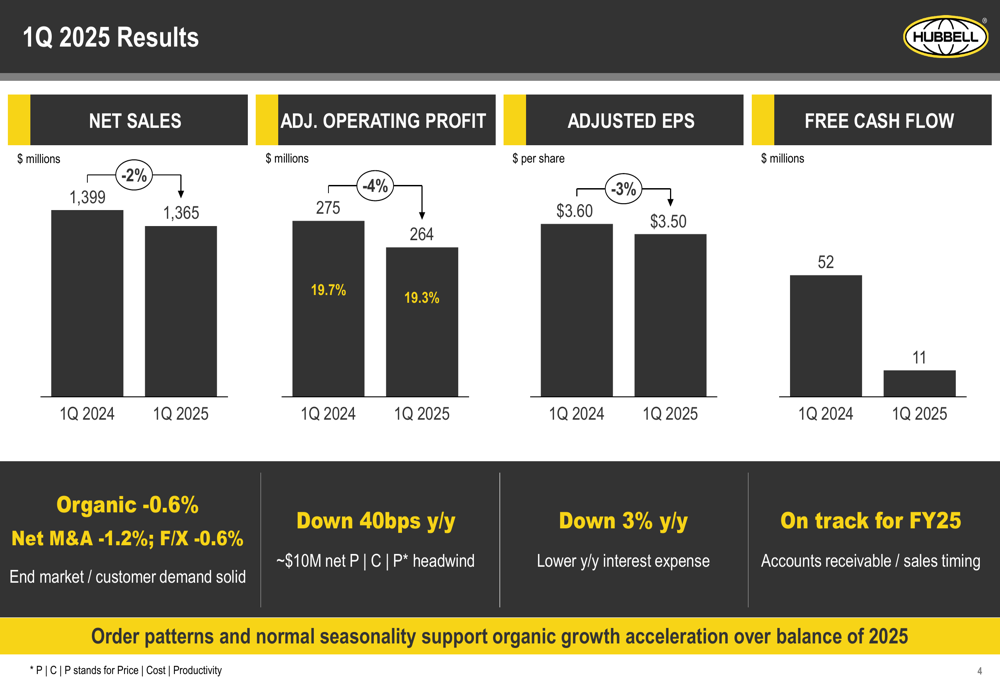

Hubbell reported first quarter net sales of $1.365 billion, representing a 2% decrease compared to the same period in 2024. Adjusted operating profit declined 4% year-over-year to $264 million, with operating margins contracting slightly to 19.3% from 19.7% in the prior year. Adjusted earnings per share came in at $3.50, down 3% from $3.60 in Q1 2024, missing analyst expectations of $3.72.

As shown in the following financial results summary:

The company’s performance was impacted by approximately $10 million in net price/cost/productivity headwinds during the quarter. Free cash flow declined significantly to $11 million from $52 million in the prior-year period, though management indicated this was in line with expectations for the full year.

Segment Performance

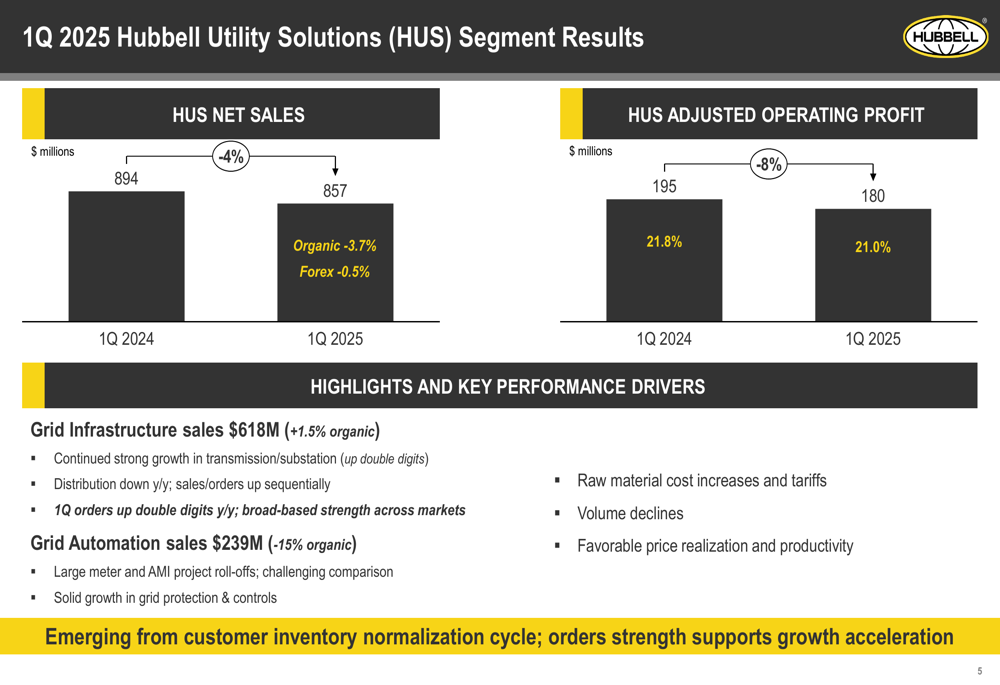

Hubbell’s two business segments delivered divergent results in the first quarter. The Hubbell Utility Solutions (HUS) segment, which represents approximately 63% of total sales, experienced a 4% decline in revenue to $857 million, with organic sales declining 3.7%. The segment’s adjusted operating profit decreased 8% to $180 million, with margins contracting to 21.0% from 21.8%.

The HUS segment performance breakdown shows mixed results within its product categories:

Despite current sales challenges, management highlighted that Grid Infrastructure orders increased by double digits year-over-year, suggesting potential revenue acceleration in coming quarters as the company emerges from a customer inventory normalization cycle.

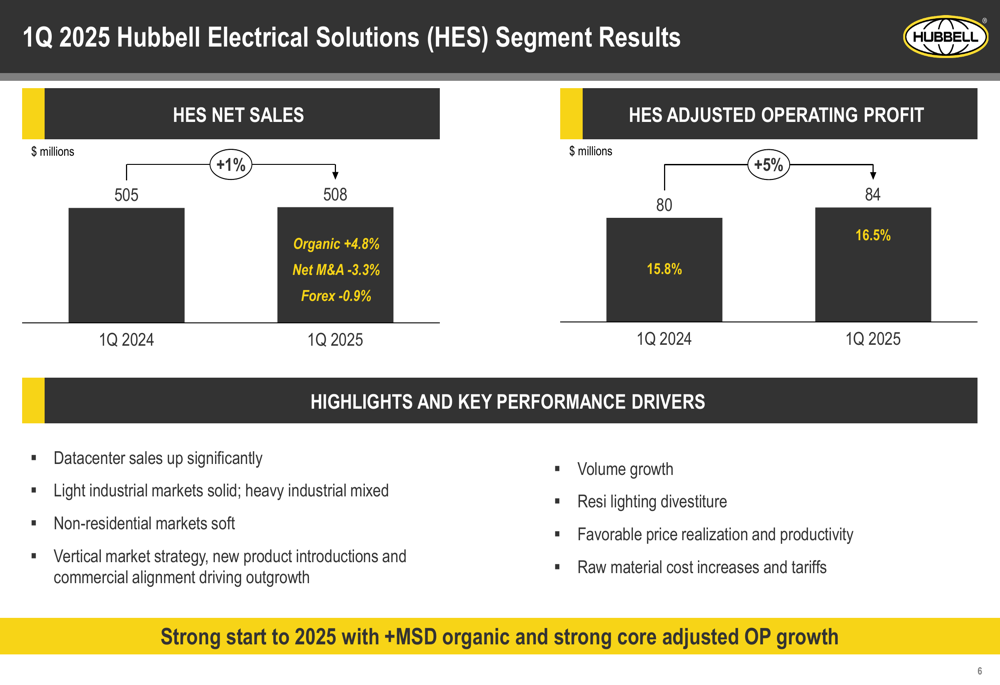

In contrast, the Hubbell Electrical Solutions (HES) segment delivered positive results, with sales increasing 1% to $508 million, driven by 4.8% organic growth partially offset by the impact of divestitures. Adjusted operating profit for the segment grew 5% to $84 million, with margins expanding to 16.5% from 15.8% in the prior year.

The following chart illustrates the HES segment’s performance:

Management attributed the segment’s strength to significant growth in datacenter sales and solid performance in light industrial markets, while noting softness in non-residential markets.

Tariff and Raw Material Challenges

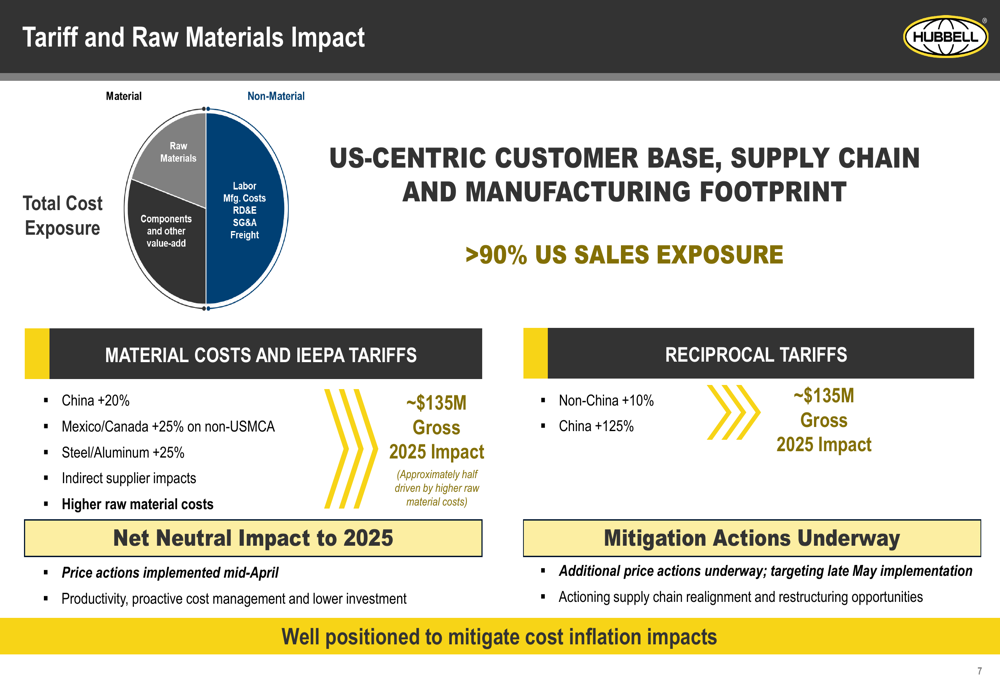

A significant focus of Hubbell’s presentation was the impact of tariffs and rising raw material costs, which are estimated to create approximately $135 million in gross impact for 2025. The company emphasized its U.S.-centric business model, with over 90% of sales in the United States, as both a challenge and opportunity in the current trade environment.

As illustrated in the following slide, Hubbell is implementing several mitigation strategies:

Management outlined plans to offset these headwinds through additional pricing actions targeted for late May implementation, along with supply chain realignment and restructuring opportunities. The company expressed confidence in achieving a net neutral impact to its 2025 results through these initiatives.

Forward-Looking Statements

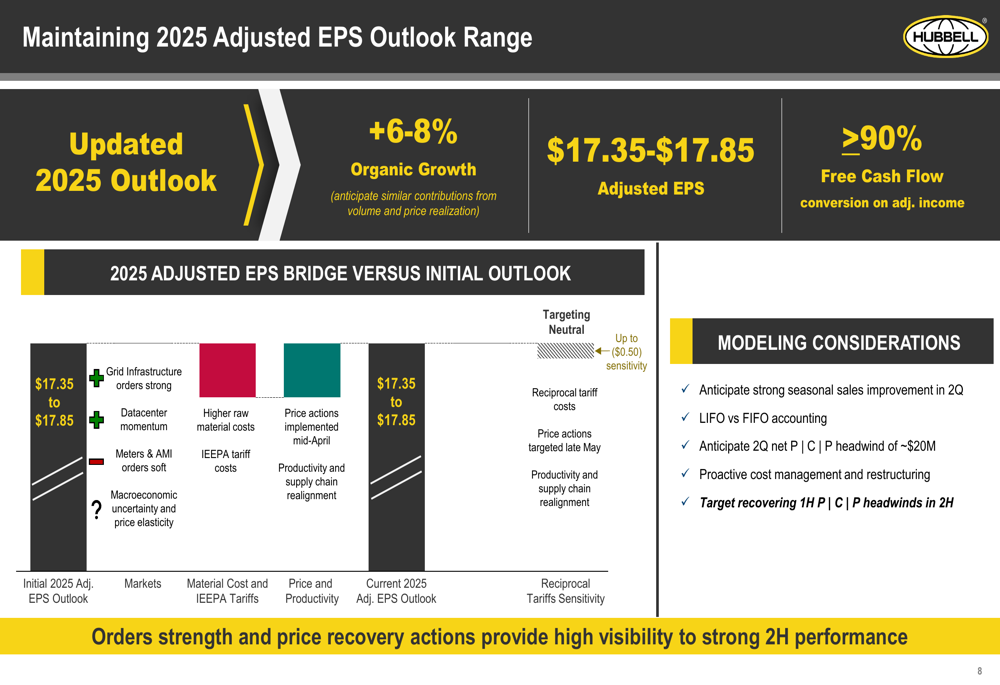

Despite the first quarter challenges, Hubbell maintained its full-year 2025 adjusted EPS outlook range of $17.35 to $17.85, supported by expected organic growth of 6-8%. The company anticipates stronger seasonal sales improvement in the second quarter, though it warned of continued price/cost/productivity headwinds of approximately $20 million in Q2.

The following outlook bridge illustrates the factors influencing Hubbell’s 2025 guidance:

Management expects to recover first-half headwinds in the second half of the year, citing strong order momentum in Grid Infrastructure and the impact of pricing actions as key drivers. The company anticipates that proactive cost management and restructuring initiatives will support margin improvement as the year progresses.

Strategic Initiatives

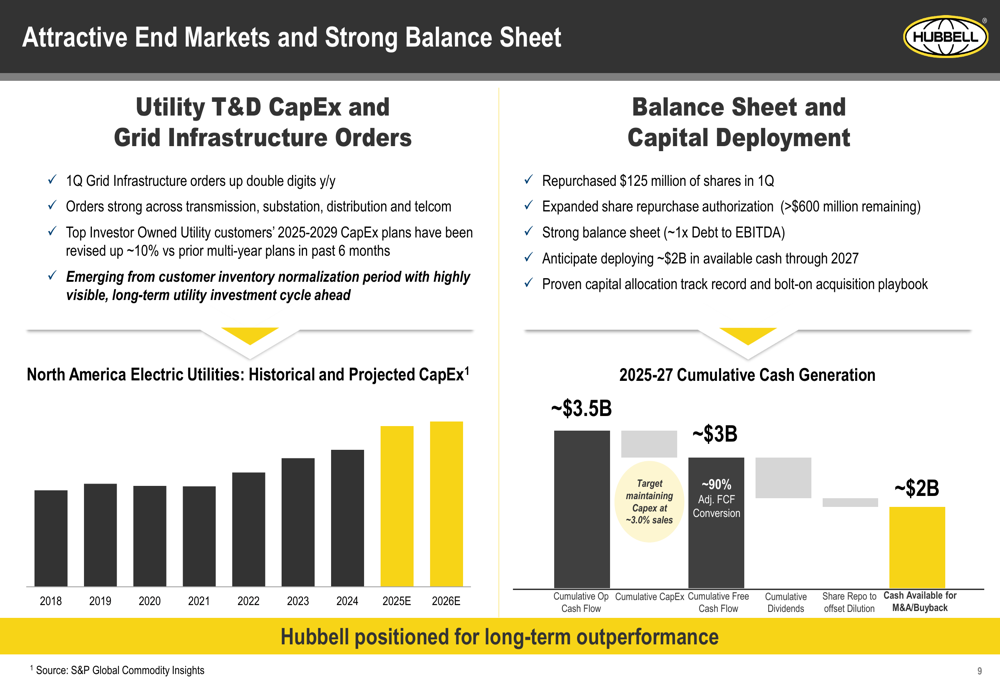

Hubbell highlighted its strong market position in utility transmission and distribution markets, noting that its top investor-owned utility customers have recently increased their 2025-2029 capital expenditure plans by approximately 10% compared to previous multi-year forecasts.

The company’s long-term market outlook remains positive, as illustrated in this projection of North American electric utility capital expenditures:

On the capital allocation front, Hubbell repurchased $125 million of shares in the first quarter and expanded its share repurchase authorization, with over $600 million remaining. The company maintains a strong balance sheet with a debt-to-EBITDA ratio of approximately 1.0x and anticipates deploying around $2 billion in available cash through 2027 through a combination of dividends, share repurchases, and strategic acquisitions.

While Hubbell’s first quarter results fell short of expectations, management’s maintained outlook and emphasis on accelerating order momentum suggest confidence in the company’s ability to navigate near-term challenges while capitalizing on long-term growth opportunities in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.