CVS Group profit drops 7.4% as revenue rises on Australia expansion, asset sale

Introduction & Market Context

Huntsman Corporation (NYSE:HUN) released its second quarter 2025 earnings presentation on July 31, 2025, revealing significant financial challenges across all business segments. The chemical manufacturer reported results that fell short of analyst expectations, triggering a 6.08% stock price decline to $9.70 following the August 1 earnings call. The stock is now trading near its 52-week low of $9.06, having lost 44% of its value year-to-date.

The presentation highlighted deteriorating market conditions, particularly in construction markets, alongside competitive pressures in Europe. Despite these challenges, management emphasized improvements in cash flow generation and progress on cost-cutting initiatives as bright spots in an otherwise difficult quarter.

Quarterly Performance Highlights

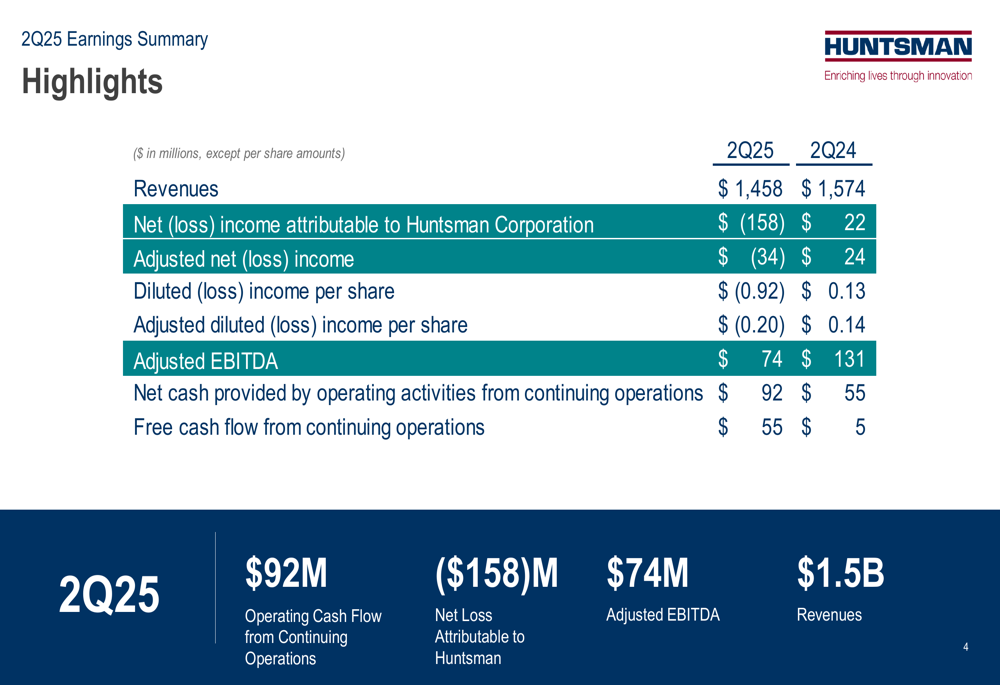

Huntsman reported a net loss of $158 million for Q2 2025, a stark contrast to the $22 million net income recorded in the same period last year. Adjusted net loss was $34 million compared to an adjusted net income of $24 million in Q2 2024. Revenue declined to $1.458 billion from $1.574 billion in the prior-year quarter.

The company’s adjusted diluted loss per share came in at $(0.20), missing analyst expectations of $(0.12) and representing a significant decline from the $0.14 adjusted diluted income per share reported in Q2 2024. Adjusted EBITDA fell to $74 million from $131 million in the prior-year period.

As shown in the following financial highlights:

Despite the earnings decline, Huntsman demonstrated improved cash flow metrics, with operating cash flow from continuing operations increasing to $92 million compared to $55 million in Q2 2024. Free cash flow from continuing operations rose significantly to $55 million from just $5 million in the prior-year quarter, reflecting management’s focus on working capital efficiency and cash preservation.

Segment Analysis

All three of Huntsman’s business segments experienced year-over-year declines in both revenue and adjusted EBITDA during the quarter.

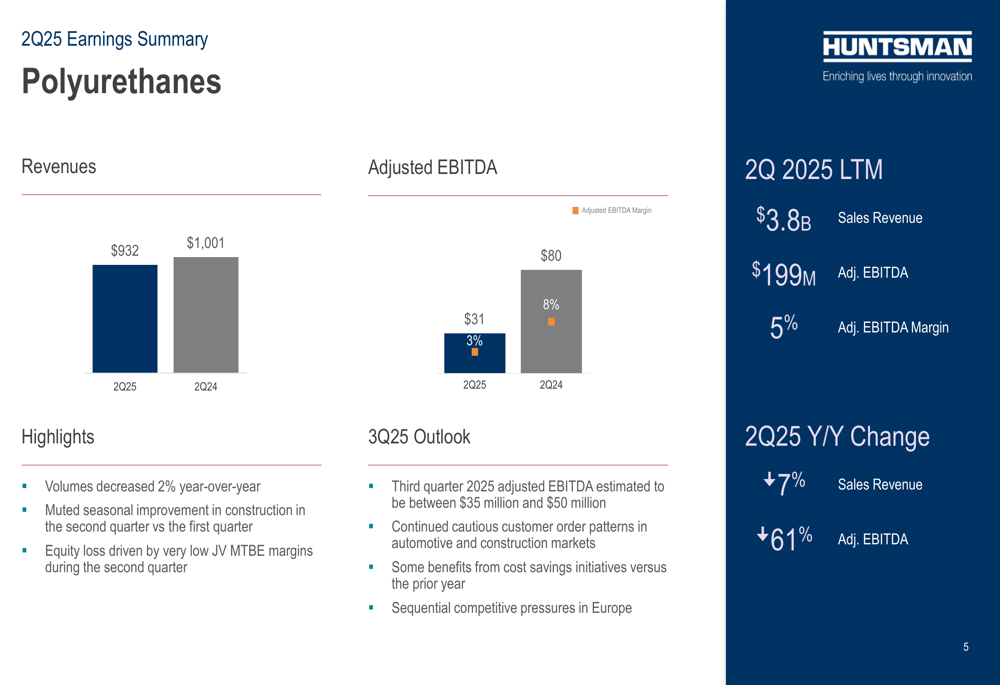

The Polyurethanes segment, Huntsman’s largest business unit, reported revenue of $932 million, down 7% from $1,001 million in Q2 2024. Adjusted EBITDA plummeted 61% to $31 million, with margins contracting to 3% from 8% in the prior-year period. Management cited a 2% year-over-year volume decrease, muted seasonal improvement in construction, and low joint venture MTBE margins as key factors impacting performance.

The segment’s performance is illustrated in the following chart:

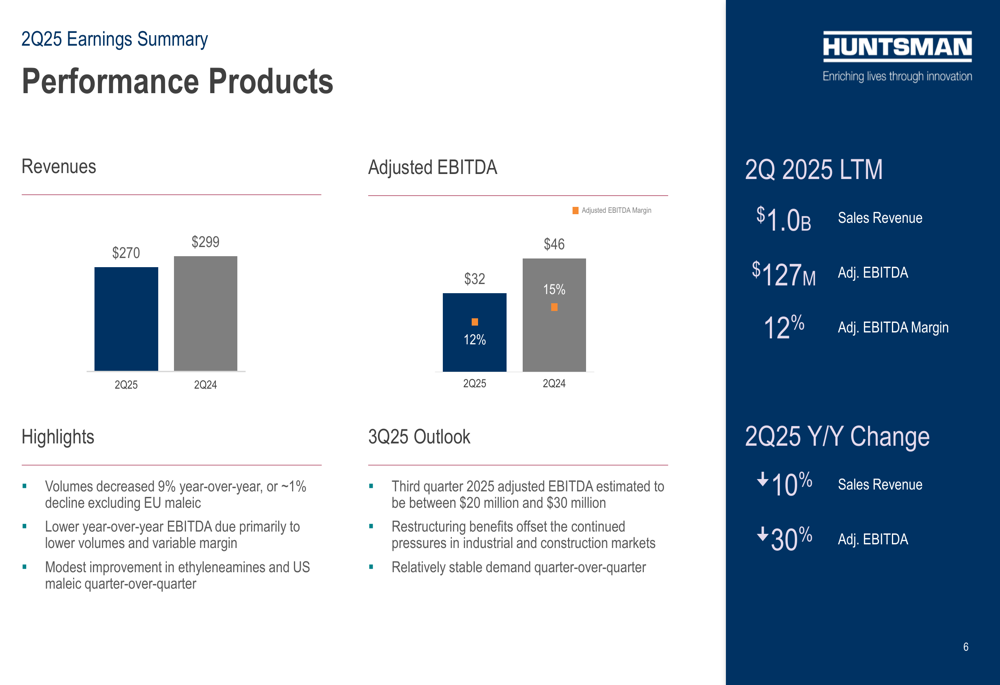

The Performance Products segment generated revenue of $270 million, down 10% from $299 million in Q2 2024, with a 9% volume decrease. Adjusted EBITDA fell 30% to $32 million, while margins contracted to 12% from 15%. Management noted modest improvement in ethyleneamines and US maleic business lines.

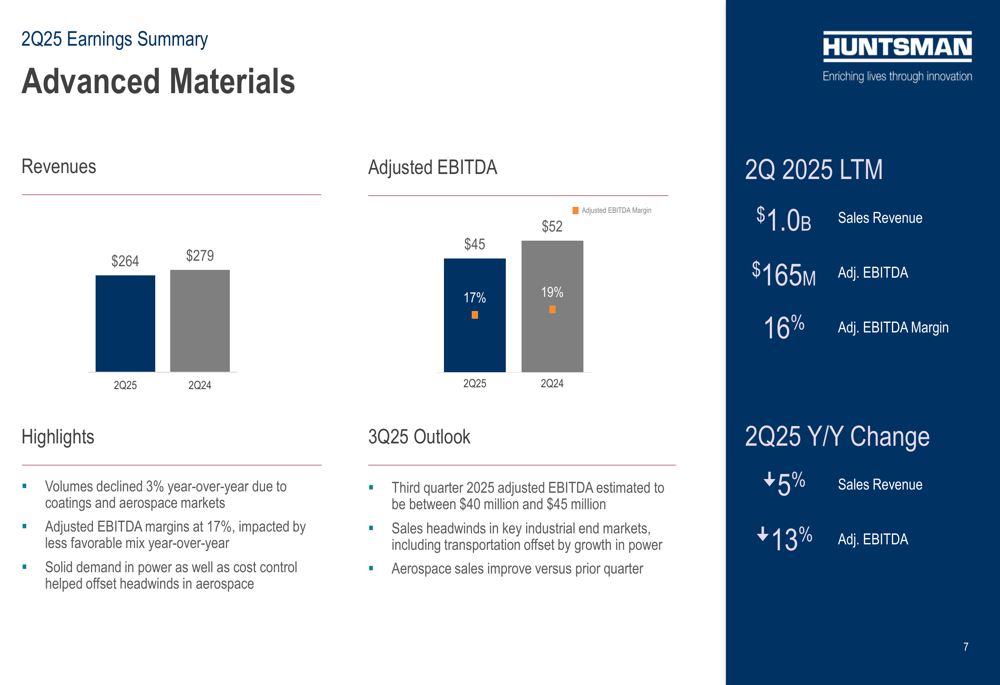

The Advanced Materials segment showed the most resilience, with revenue of $264 million, down 5% from $279 million in Q2 2024. Adjusted EBITDA decreased 13% to $45 million, with margins contracting to 17% from 19%. The segment benefited from solid demand in power applications, which helped offset headwinds in other markets.

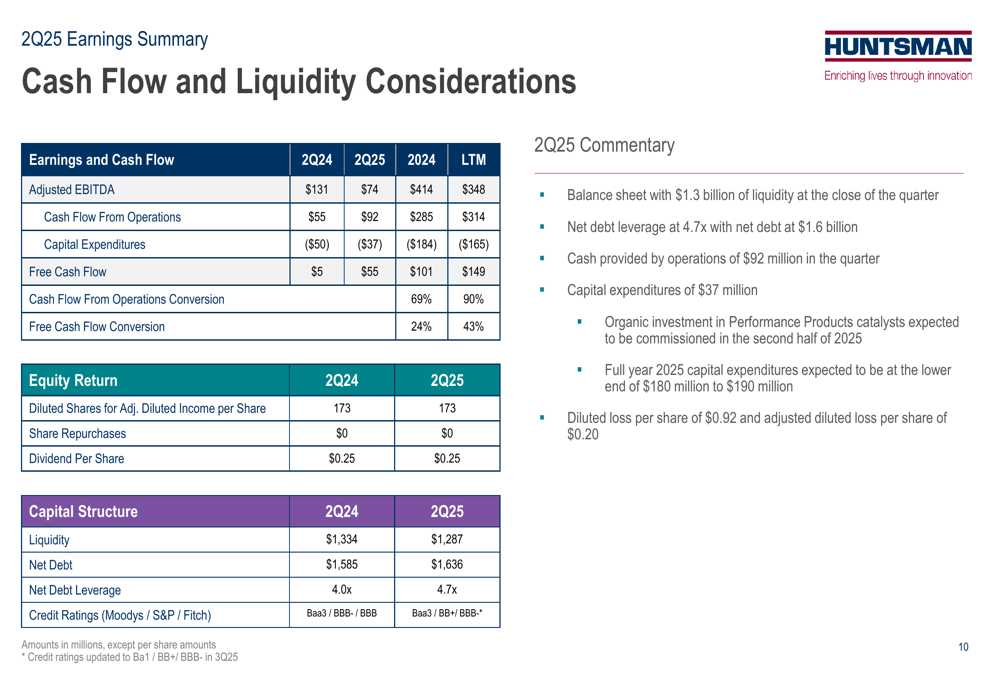

Cash Flow and Liquidity Position

Despite the challenging earnings environment, Huntsman’s cash flow metrics showed notable improvement. Cash flow from operations conversion increased to 90% in Q2 2025 from 69% in Q2 2024, while free cash flow conversion rose to 43% from 24%.

The company maintained a liquidity position of $1.287 billion at the end of Q2 2025, slightly down from $1.334 billion a year earlier. However, net debt increased to $1.636 billion from $1.585 billion, and the net debt leverage ratio deteriorated to 4.7x from 4.0x, reflecting the impact of lower EBITDA on the company’s balance sheet metrics.

The following chart details Huntsman’s cash flow and liquidity considerations:

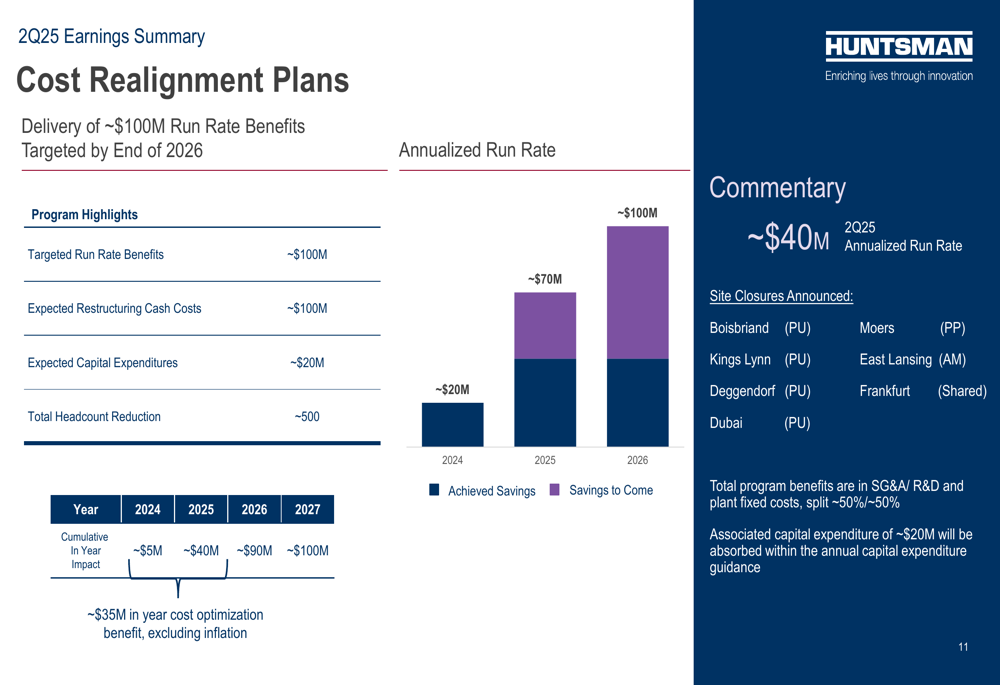

Cost Realignment Progress

A central theme of Huntsman’s presentation was its aggressive cost-cutting initiatives aimed at offsetting market headwinds. The company is targeting approximately $100 million in run-rate benefits by the end of 2026, with expected restructuring cash costs of around $100 million and capital expenditures of approximately $20 million.

The restructuring plan involves a headcount reduction of approximately 500 employees and multiple site closures, including facilities in Kings Lynn, Boisbriand, Deggendorf, East Lansing, Dubai, Moers, and Frankfurt. As of Q2 2025, the company has achieved an annualized run rate of approximately $40 million in cost savings.

The progress of the cost realignment plan is illustrated in the following chart:

During the earnings call, CEO Peter Huntsman emphasized the company’s strategic focus on "value over volume," particularly in high-cost regions like Europe. CFO Phil Lister acknowledged the company’s sub-investment grade credit rating status, indicating that financial management would operate within those constraints.

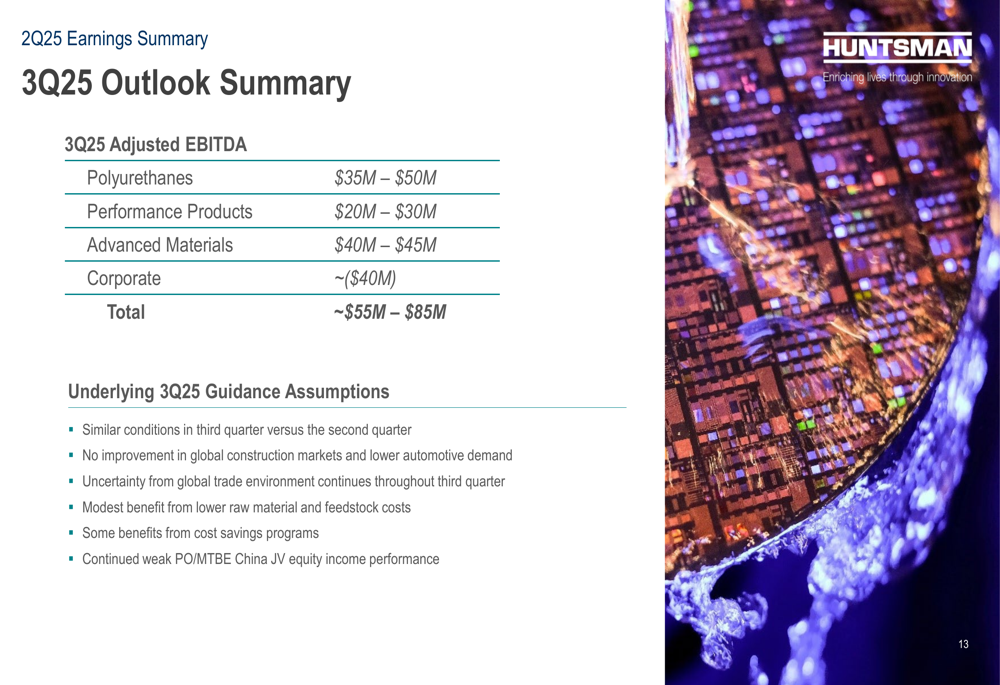

Outlook and Guidance

Looking ahead to Q3 2025, Huntsman provided adjusted EBITDA guidance of $55-85 million, with segment-specific projections of $35-50 million for Polyurethanes, $20-30 million for Performance Products, and $40-45 million for Advanced Materials. Corporate costs are expected to be approximately $40 million.

The guidance is based on several assumptions, including similar market conditions, no improvement in construction markets, uncertainty from global trade, benefits from raw materials and cost savings initiatives, and continued weak performance from the PO/MTBE China joint venture.

The Q3 2025 outlook is summarized in the following chart:

For the full year 2025, Huntsman expects corporate and other expenses of approximately $150 million, with cost savings program benefits of around $65 million. Capital expenditures are projected to be at the lower end of the $180-190 million range, reflecting the company’s cautious approach to capital allocation in the current environment.

The company remains cautious about the near-term outlook, with no plans for new MDI capacity and potential supply rationalization in Europe. Management anticipates a potential recovery in North America and China, contingent on economic improvements such as interest rate cuts and consumer confidence restoration, though the timing remains uncertain.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.