S&P 500 could hit 8,000 in 2026 on more easing from Fed: JPMorgan

Introduction & Market Context

International Business Machines (NYSE:IBM) released its first quarter 2025 earnings presentation on April 23, highlighting solid financial performance led by its software segment and growing artificial intelligence business. Despite reporting better-than-expected results, IBM ’s stock retreated 4.71% in after-hours trading to $233.92, suggesting investor skepticism about the company’s growth trajectory.

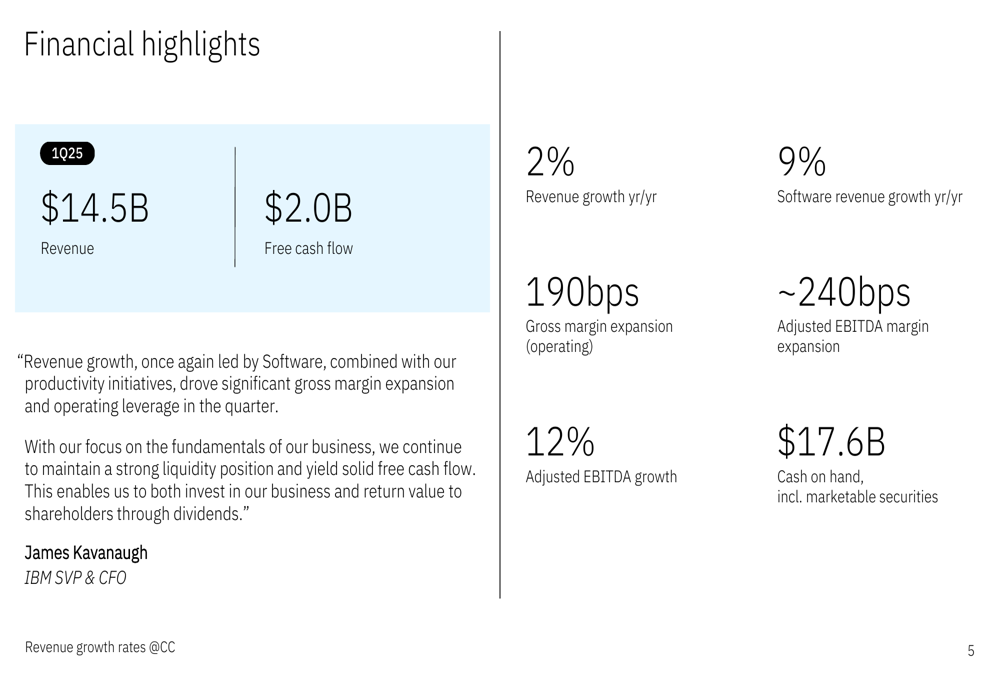

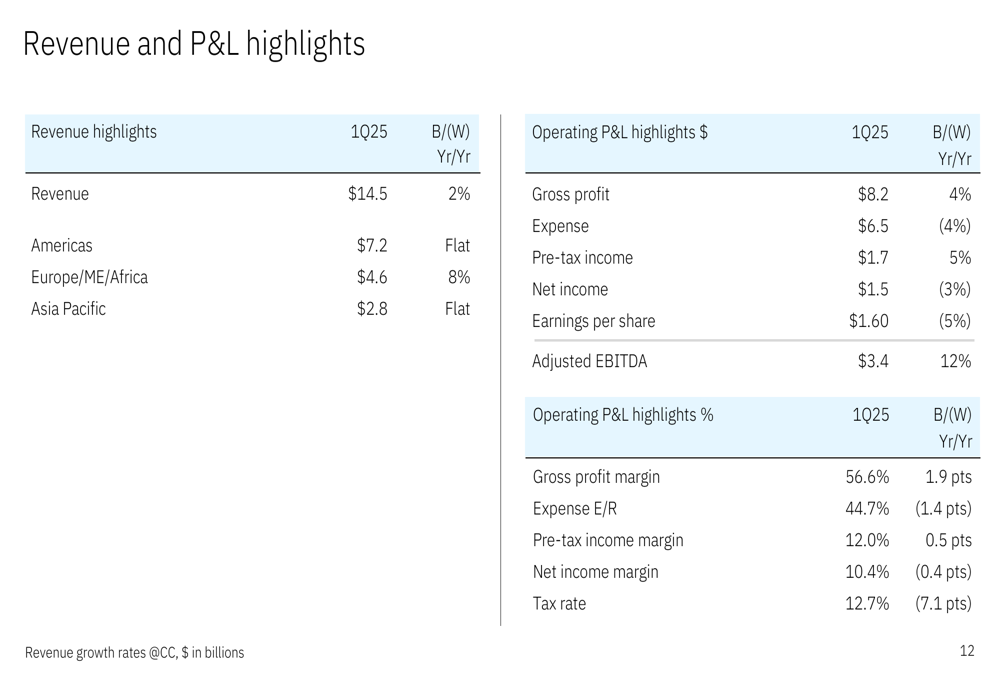

The tech giant reported revenue of $14.5 billion, representing 2% year-over-year growth, while generating $2.0 billion in free cash flow – its highest first-quarter free cash flow "in many years," according to company executives. The results come as IBM continues its transformation into a hybrid cloud and AI-focused enterprise technology provider.

Quarterly Performance Highlights

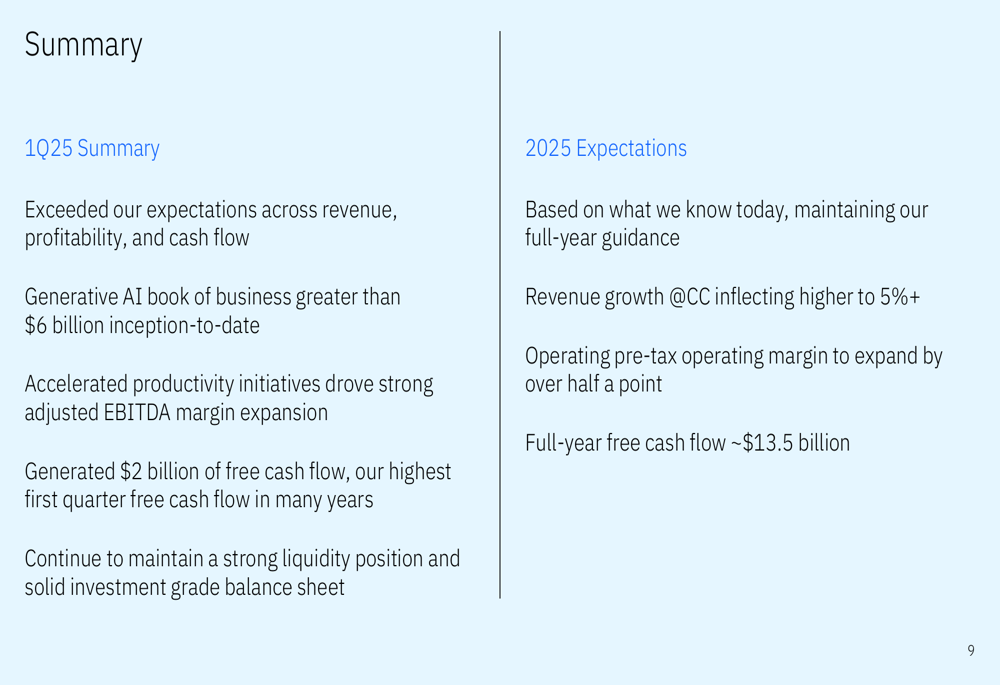

IBM exceeded its internal expectations across revenue, profitability, and cash flow metrics. The company’s adjusted EBITDA grew 12% year-over-year to $3.4 billion, with margin expansion of approximately 240 basis points.

As shown in the following financial highlights slide, IBM delivered significant gross margin expansion of 190 basis points while maintaining a strong cash position of $17.6 billion:

"We exceeded our expectations across revenue, profitability, and cash flow," stated Arvind (NSE:ARVN) Krishna, IBM’s Chairman, President, and CEO. Krishna highlighted the company’s generative AI momentum, noting that IBM’s "book of business exceeds $6 billion inception-to-date, up more than $1 billion in the quarter."

James Kavanaugh, IBM’s SVP & CFO, emphasized "revenue growth led by Software (ETR:SOWGn), significant gross margin expansion, strong liquidity, solid free cash flow, and value return to shareholders" as key achievements for the quarter.

Segment Analysis

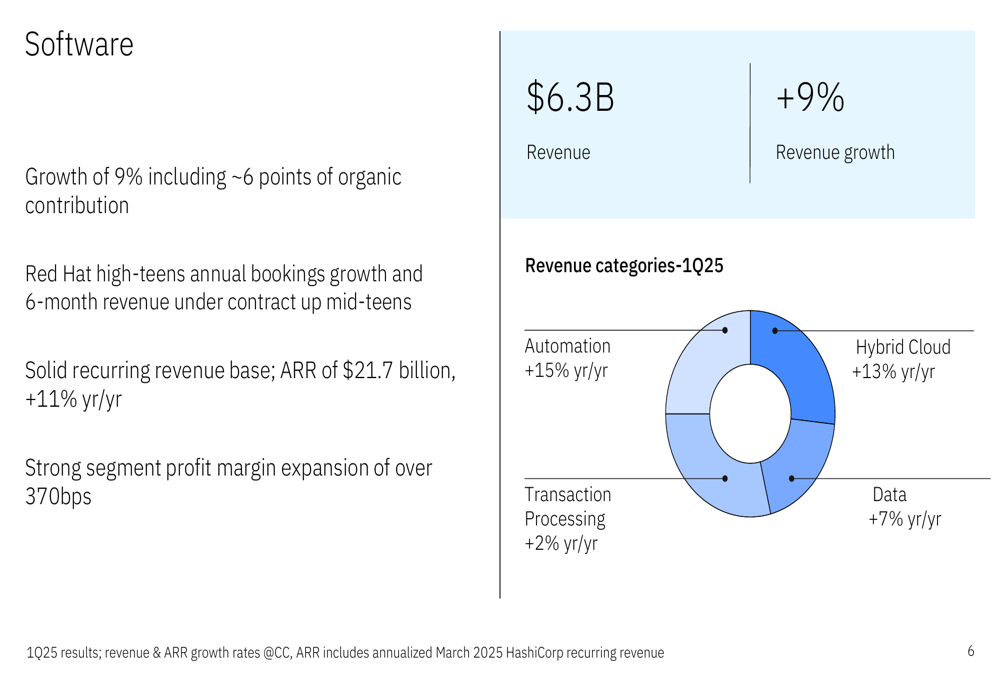

IBM’s software segment emerged as the clear standout performer, with 9% year-over-year revenue growth to $6.3 billion. The segment delivered impressive profit margin expansion of over 370 basis points, with particularly strong performance in automation (15% growth) and hybrid cloud (13% growth).

The following breakdown illustrates the software segment’s performance across key categories:

Red Hat continued to show strong momentum with high-teens annual bookings growth, while IBM’s annual recurring revenue reached $21.7 billion, representing an 11% increase year-over-year – a critical metric for the company’s subscription-based business model.

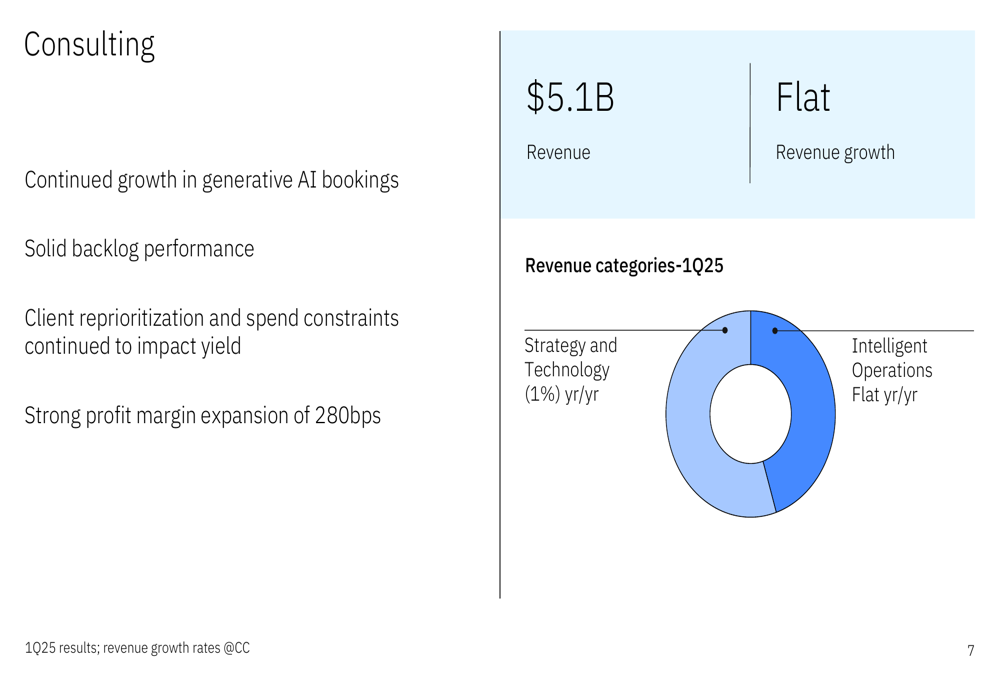

By contrast, IBM’s consulting segment reported flat revenue of $5.1 billion, though it achieved strong profit margin expansion of 280 basis points. The company noted that "client reprioritization and spend constraints continued to impact yield," suggesting ongoing challenges in the enterprise consulting market.

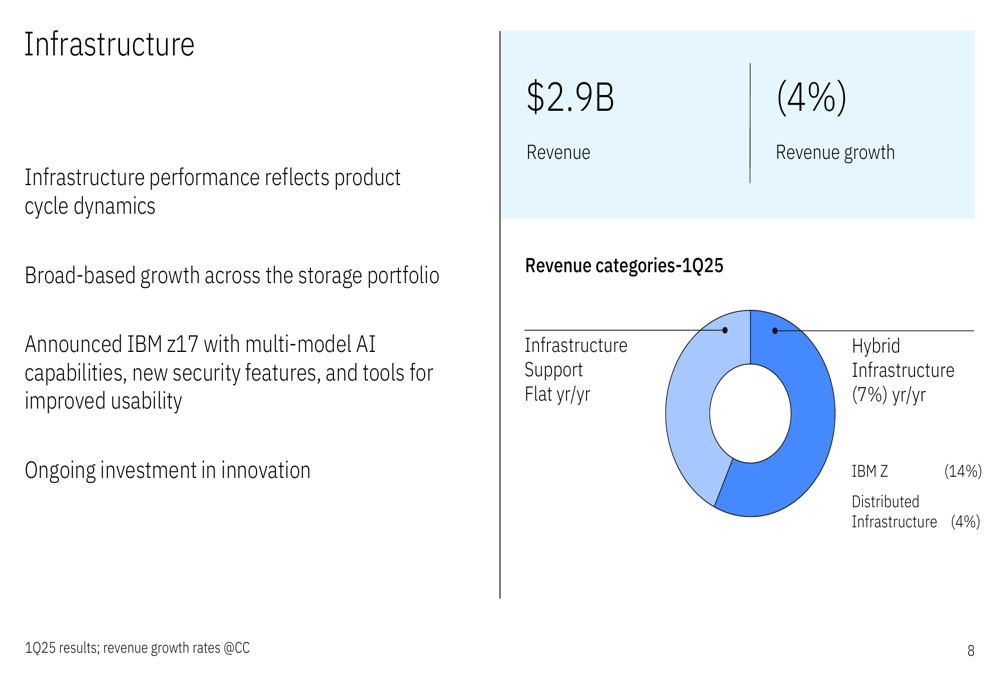

The infrastructure segment saw a 4% revenue decline to $2.9 billion, which IBM attributed to "product cycle dynamics." The company announced its new IBM z17 mainframe system with multi-model AI capabilities, which could drive future growth in this segment as customers upgrade their systems.

AI and Strategic Initiatives

Generative AI remains a central focus of IBM’s strategy, with the company reporting that its AI book of business now exceeds $6 billion inception-to-date, growing by more than $1 billion in the first quarter alone. This acceleration suggests IBM is gaining traction in the competitive enterprise AI market.

The company’s recently announced IBM z17 mainframe incorporates multi-model AI capabilities, new security features, and improved usability tools, demonstrating IBM’s strategy to integrate AI across its product portfolio.

IBM’s software-led approach appears to be yielding results, with the segment now representing approximately 43% of total revenue and growing at a pace well above the company average. The emphasis on recurring revenue models is also evident in the 11% growth in annual recurring revenue.

Financial Position and Outlook

IBM’s detailed revenue and profit & loss highlights reveal strength across geographic regions, with particularly strong performance in Europe/Middle East/Africa, which grew 8% year-over-year:

The company maintained a strong balance sheet with $17.6 billion in cash and marketable securities, though total debt increased to $63.3 billion, partly due to $7.1 billion in acquisitions during the quarter.

Looking ahead, IBM maintained its full-year 2025 guidance, projecting revenue growth at constant currency to inflect higher to over 5%, operating pre-tax margin expansion of more than half a point, and full-year free cash flow of approximately $13.5 billion.

Market Reaction

Despite the positive results and maintained guidance, IBM’s stock fell 4.71% in after-hours trading following the earnings release. This decline contrasts with the company’s recent strong performance – the stock had gained 1.82% during regular trading hours on the day of the announcement, closing at $245.29.

The negative after-hours reaction may reflect investor concerns about the flat consulting performance, infrastructure segment decline, or questions about the sustainability of IBM’s AI growth. It’s worth noting that IBM’s stock had been trading near its 52-week high of $266.45 prior to the earnings release, suggesting high expectations were already priced in.

IBM’s Q1 2025 presentation paints a picture of a company successfully executing its software-led strategy with particular strength in AI initiatives. However, the market’s immediate reaction indicates investors may be looking for even stronger growth signals or may have concerns about specific segments before pushing the stock to new heights.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.