5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

International Business Machines (NYSE:IBM) released its third-quarter 2025 earnings presentation on October 22, showcasing accelerated performance across all business segments. The technology giant reported its highest revenue growth in several years, with a 7% year-over-year increase, exceeding analyst expectations. Following the announcement, IBM’s stock rose 2.16% in after-hours trading to $288.15, reflecting investor confidence in the company’s strategic direction and improved financial outlook.

The presentation highlighted IBM’s continued transformation toward higher-growth areas like artificial intelligence and hybrid cloud, while maintaining strong cash generation capabilities. The company has now raised its full-year expectations for revenue growth, operating pre-tax margin, adjusted EBITDA, and free cash flow.

As shown in the following CEO perspective from the earnings presentation:

Quarterly Performance Highlights

IBM reported strong financial results for Q3 2025, with revenue reaching $16.3 billion, representing a 7% year-over-year increase. The company’s earnings per share grew 15% to $2.65, surpassing the forecast of $2.44. Free cash flow for the quarter was $2.4 billion, contributing to a year-to-date total of $7.2 billion, which IBM noted is the highest year-to-date free cash flow margin in its reported history.

The company demonstrated significant improvement in profitability metrics, with adjusted EBITDA growing 22% and pre-tax margin expanding by approximately 200 basis points. These results reflect IBM’s strategic focus on higher-margin businesses and operational efficiency.

The key financial highlights from the quarter are illustrated in this slide:

From a geographical perspective, IBM saw strong performance in the Americas and Europe/Middle East/Africa regions, both growing at 9% year-over-year, while Asia Pacific remained flat. The company’s gross profit margin expanded to 58.7%, an increase of 1.2 percentage points compared to the same period last year.

Segment Analysis

IBM’s performance was strong across all three of its primary business segments: Software, Infrastructure, and Consulting.

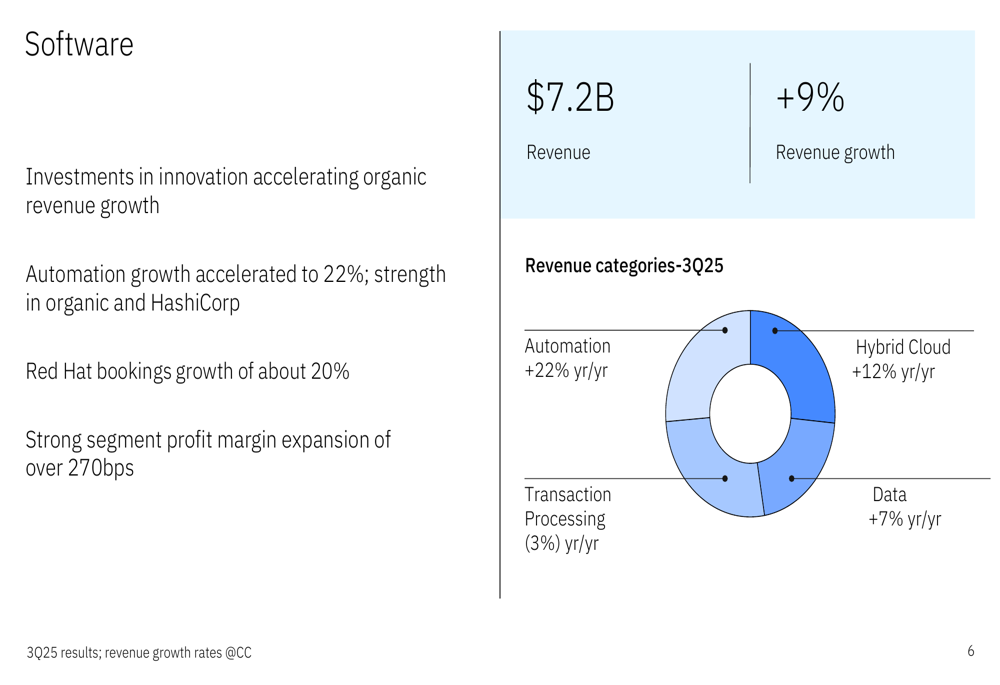

The Software segment, which represents the largest portion of IBM’s business, generated $7.2 billion in revenue, a 9% increase year-over-year. This growth was driven primarily by Automation solutions, which grew 22%, benefiting from both organic growth and the integration of HashiCorp. Red Hat continued its strong performance with bookings growth of approximately 20%. The segment’s profit margin expanded by over 270 basis points, reflecting the high-value nature of IBM’s software portfolio.

The following slide breaks down the Software segment’s performance:

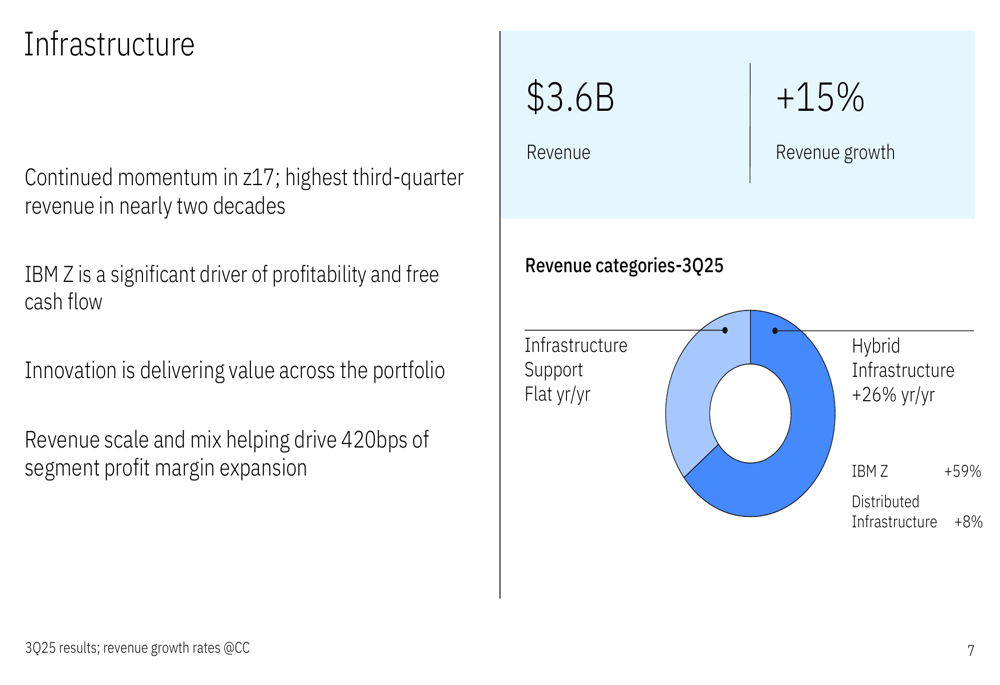

The Infrastructure segment delivered exceptional results, with revenue of $3.6 billion representing a 15% year-over-year increase. This performance was largely driven by continued momentum in the z17 mainframe cycle, which helped IBM Z revenue grow by 59%. The company noted that this was the highest third-quarter revenue for this segment in nearly two decades. The segment’s profit margin expanded significantly by 420 basis points.

As shown in the Infrastructure segment performance slide:

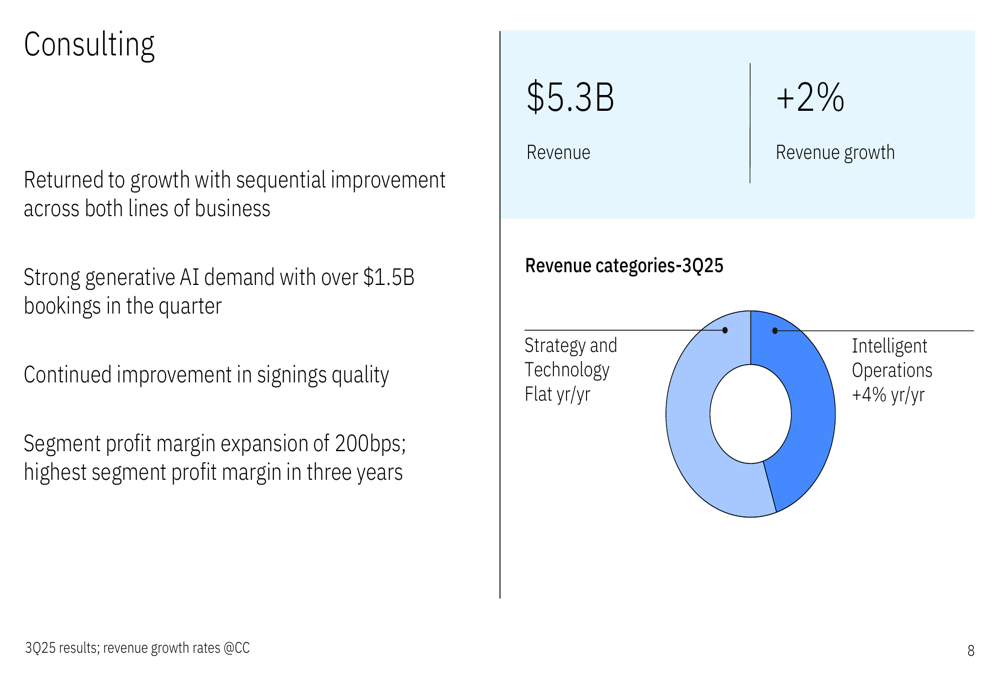

The Consulting segment returned to growth with revenue of $5.3 billion, a 2% increase year-over-year. IBM highlighted sequential improvement across both lines of business within Consulting. Notably, generative AI demand remained strong, with over $1.5 billion in bookings during the quarter. The segment achieved its highest profit margin in three years, expanding by 200 basis points.

The Consulting segment’s performance is illustrated in this slide:

Strategic Focus on AI

A key highlight of IBM’s presentation was the growing momentum in its artificial intelligence business. The company reported that its generative AI book of business has now exceeded $9.5 billion inception-to-date, underscoring the increasing adoption of AI solutions across its client base.

In the Consulting segment, IBM secured over $1.5 billion in generative AI bookings during the quarter alone, indicating strong client demand for AI implementation services. The company’s Software segment is also benefiting from AI integration, particularly in its Automation solutions, which grew 22% year-over-year.

During the earnings call, CEO Arvind Krishna emphasized the importance of technology as a driver of growth and competitive advantage, with a particular focus on hybrid cloud and artificial intelligence as the core of IBM’s strategy.

Forward Outlook

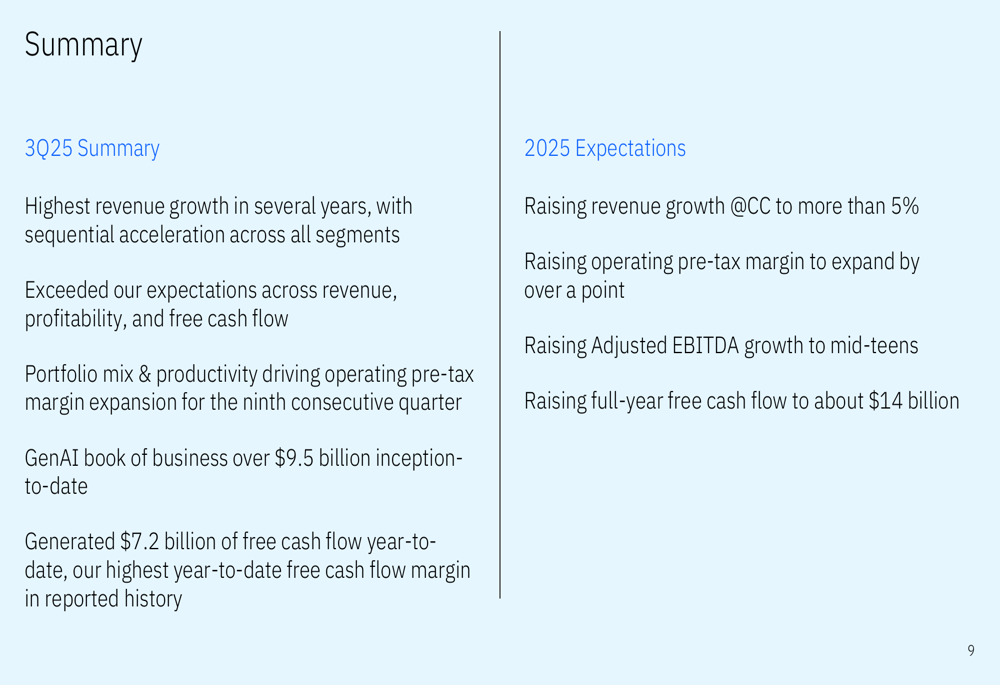

Based on its strong performance in the third quarter, IBM has raised its full-year 2025 expectations across several key metrics. The company now anticipates revenue growth of more than 5% at constant currency, up from its previous guidance. IBM also raised its operating pre-tax margin expansion target to over one percentage point and expects adjusted EBITDA growth in the mid-teens.

Perhaps most significantly, IBM increased its full-year free cash flow projection to approximately $14 billion, reflecting confidence in its ability to generate strong cash flows through the remainder of the year.

The summary of Q3 results and raised expectations for 2025 is presented in this comprehensive slide:

In the software business specifically, IBM projects revenue growth approaching double digits, with Red Hat expected to return to mid-teens growth. These projections reflect the company’s strategic focus on higher-growth, higher-margin business areas.

IBM’s strong quarterly performance and raised outlook demonstrate the company’s successful execution of its hybrid cloud and AI strategy. With consistent margin expansion for nine consecutive quarters and accelerating revenue growth, IBM appears well-positioned to continue its positive momentum through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.