EU and US could reach trade deal this weekend - Reuters

Introduction & Market Context

IDEXX Laboratories Inc (NASDAQ:IDXX) released its Q1 2025 earnings presentation on May 1, 2025, revealing solid performance despite headwinds in clinical visit trends. The veterinary diagnostics leader reported earnings per share of $2.96, exceeding analyst expectations of $2.86, while revenue came in at $998 million, slightly below the anticipated $1 billion. Following the earnings release, IDEXX shares surged 9.1% to $432.65, reflecting strong investor confidence in the company’s growth trajectory.

The company’s performance comes amid a challenging environment for the veterinary industry, with U.S. clinical visits declining 2.5% year-over-year in Q1 2025. Despite this headwind, IDEXX demonstrated resilience through strong diagnostic utilization and continued expansion of its instrument installed base.

Quarterly Performance Highlights

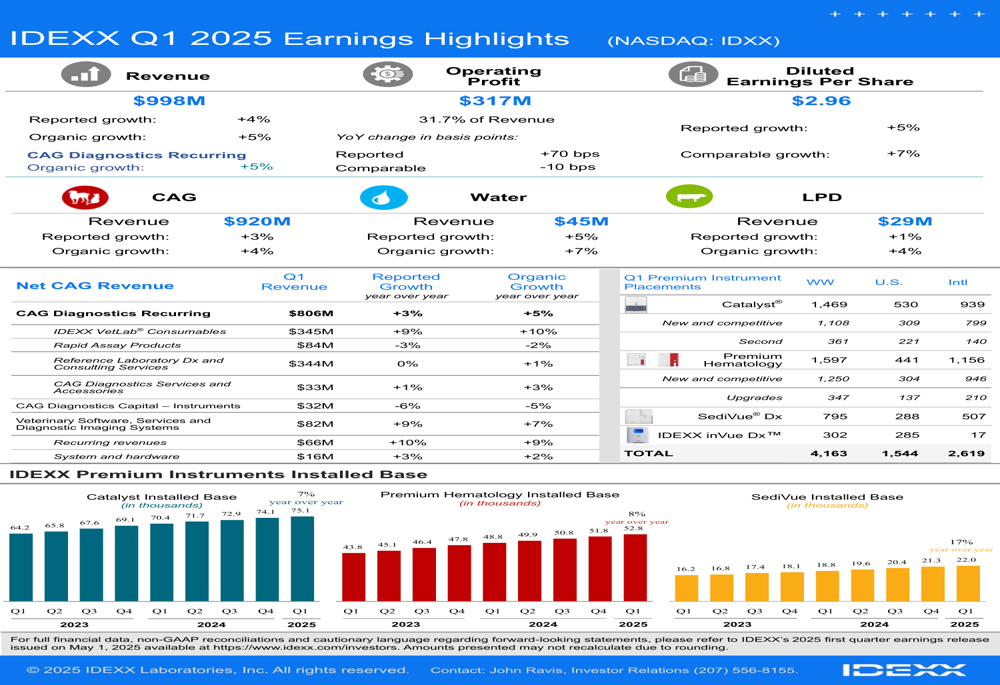

IDEXX reported Q1 2025 revenue of $998 million, representing 4% reported growth and 5% organic growth compared to the same period last year. Operating profit reached $317 million, accounting for 31.7% of revenue, while diluted earnings per share grew 5% on a reported basis and 7% on a comparable basis to $2.96.

As shown in the following comprehensive earnings summary:

The Companion Animal Group (CAG) segment, which represents the bulk of IDEXX’s business, generated $920 million in revenue, reflecting 3% reported growth and 4% organic growth. Within CAG, diagnostic recurring revenue reached $806 million with 5% organic growth, primarily driven by IDEXX VetLab consumables, which grew 10% organically to $345 million. The Water and Livestock, Poultry and Dairy (LPD) segments also showed positive performance, with organic growth of 7% and 4% respectively.

Growth Drivers and Challenges

A key strength in IDEXX’s Q1 performance was the continued expansion of its instrument installed base. The Catalyst installed base grew 7% year-over-year to 74,100 units, while the Premium Hematology and SediVue installed bases increased by 8% and 17% respectively. The company placed 4,163 premium instruments worldwide during the quarter, including 1,469 Catalyst analyzers and 302 of the new IDEXX inVue Dx cellular analyzers.

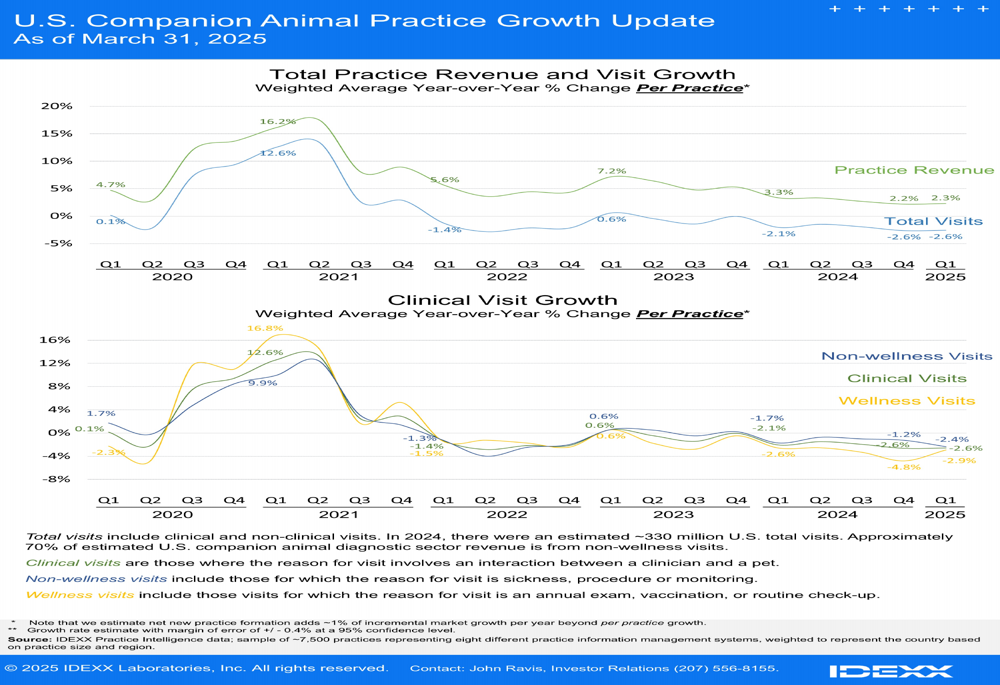

The company’s performance is particularly notable given the challenging trends in veterinary clinic visits. As illustrated in the following chart tracking U.S. companion animal practice growth:

Clinical visits in U.S. veterinary practices declined by 2.5% year-over-year in Q1 2025, continuing a downward trend observed in recent quarters. This represents a significant shift from the Q1 average of +3.0% growth seen during 2020-2023.

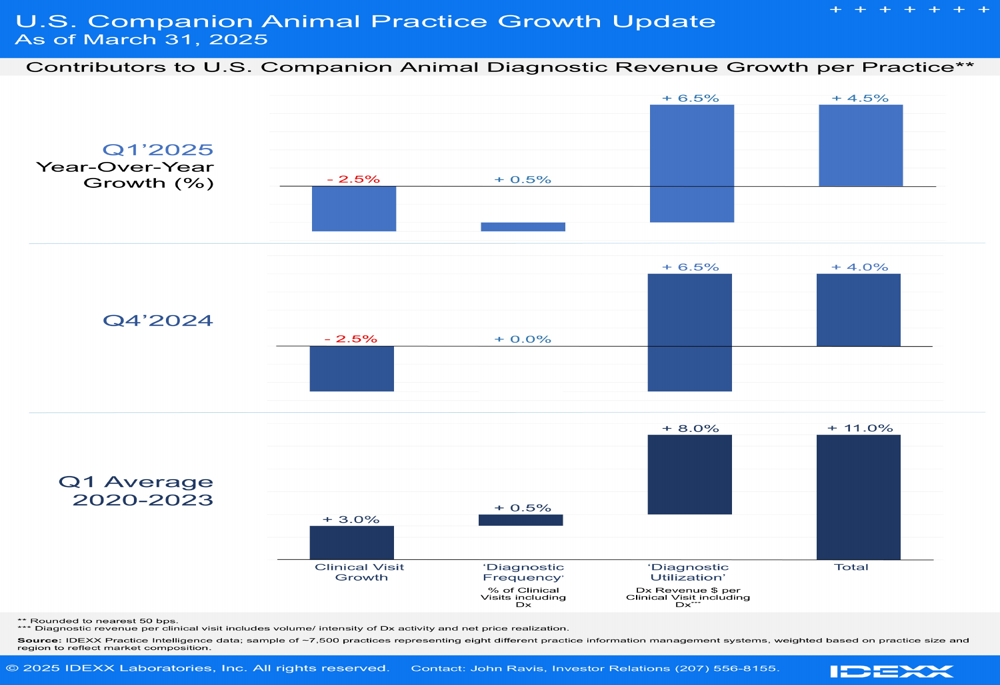

Despite this headwind, IDEXX has successfully maintained growth through increased diagnostic utilization. The following breakdown illustrates how diagnostic revenue growth per practice has been achieved:

Diagnostic utilization contributed +6.5% to revenue growth, more than offsetting the -2.5% impact from declining clinical visits. This demonstrates the effectiveness of IDEXX’s strategy to drive deeper penetration of diagnostics within existing veterinary practices.

"Cancer is personal to many pet owners. The earlier we can detect cancer and determine the type of cancer, the better the chance for targeted treatments and improved outcomes," CEO Jay Mazelski emphasized during the earnings call, highlighting the company’s focus on innovative diagnostic solutions like the IDEXX CancerDx for canine lymphoma detection.

Forward-Looking Statements

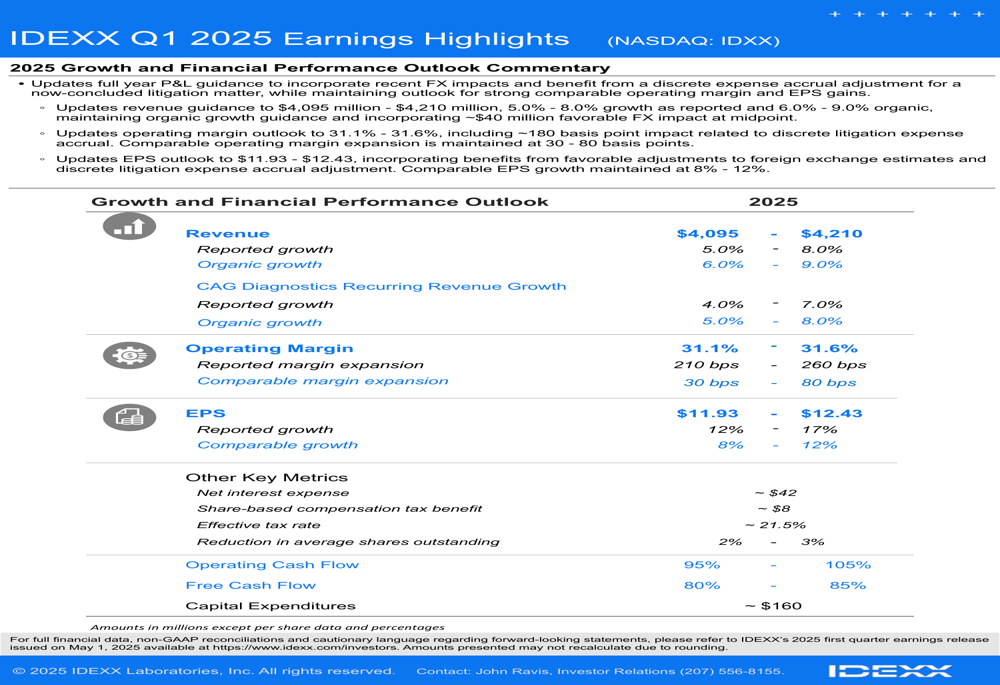

IDEXX updated its full-year 2025 guidance, maintaining a positive outlook while incorporating recent foreign exchange impacts and a discrete expense accrual adjustment. The company now expects:

Revenue is projected to reach $4,095 million to $4,210 million, representing 5.0% to 8.0% reported growth and 6.0% to 9.0% organic growth. This includes approximately $40 million in favorable foreign exchange impact. The CAG Diagnostics recurring revenue is expected to grow 4.0% to 7.0% on a reported basis and 5.0% to 8.0% organically.

Operating margin is forecasted between 31.1% and 31.6%, with comparable margin expansion of 30 to 80 basis points. The updated EPS guidance range of $11.93 to $12.43 reflects 12% to 17% reported growth and 8% to 12% comparable growth.

CFO Andrew Emerson (NYSE:EMR) commented on the guidance during the earnings call, stating, "Our guidance is a range. We certainly have a range of outcomes here that we’re expecting."

Market Reaction and Analyst Perspectives

The market responded positively to IDEXX’s Q1 results and updated guidance, with the stock surging 9.1% following the announcement. This reaction suggests investors are focusing on the company’s ability to deliver earnings growth despite macroeconomic challenges and declining clinical visits.

With a market capitalization of $38.8 billion and a P/E ratio of 40.08, IDEXX continues to trade at a premium valuation, reflecting market confidence in its long-term growth prospects. Analyst targets for the stock range from $385 to $566, with a consensus recommendation of moderate buy.

The company’s robust gross profit margin of 61.04% and strong return on equity of 58% underscore its operational efficiency and market leadership position. However, challenges remain, including supply chain issues, tariff uncertainties, and the ongoing pressure on veterinary clinic visits.

IDEXX’s strategic focus on innovation, particularly in cancer detection and point-of-care testing, positions it well to navigate these challenges. The company plans to expand its IDEXX InVue DX placements to over 4,500 units in 2025, supporting its revenue growth projections and reinforcing its commitment to advancing veterinary diagnostics despite the challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.