Bubble or no bubble, this is the best stock for AI exposure: analyst

Introduction & Market Context

Ingram Micro Holding Ltd (NASDAQ:INGM) released its third-quarter 2025 earnings presentation on October 30, highlighting 7.2% year-over-year revenue growth while falling short of analyst EPS expectations. The technology distributor reported quarterly revenue of $12.6 billion and non-GAAP earnings per share of $0.72, which missed analyst forecasts of $0.79, representing an 8.86% negative surprise.

Despite the earnings miss, Ingram Micro's stock showed resilience, rising 0.36% in aftermarket trading to close at $21.98. The company continues to position itself at the center of the global technology ecosystem, with particular emphasis on artificial intelligence initiatives and its Xvantage digital platform.

Quarterly Performance Highlights

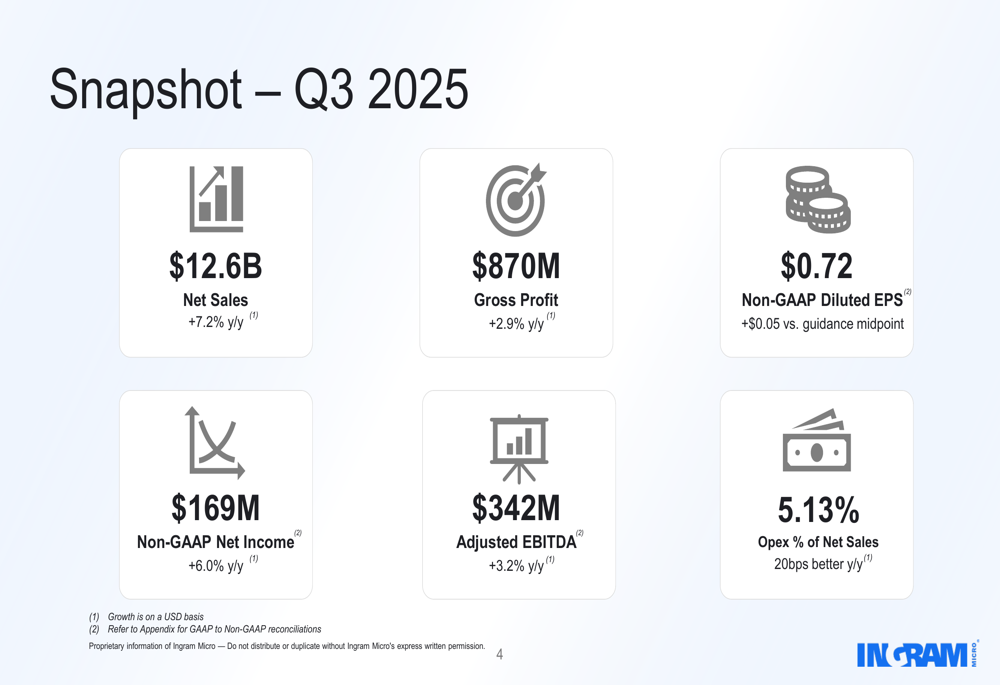

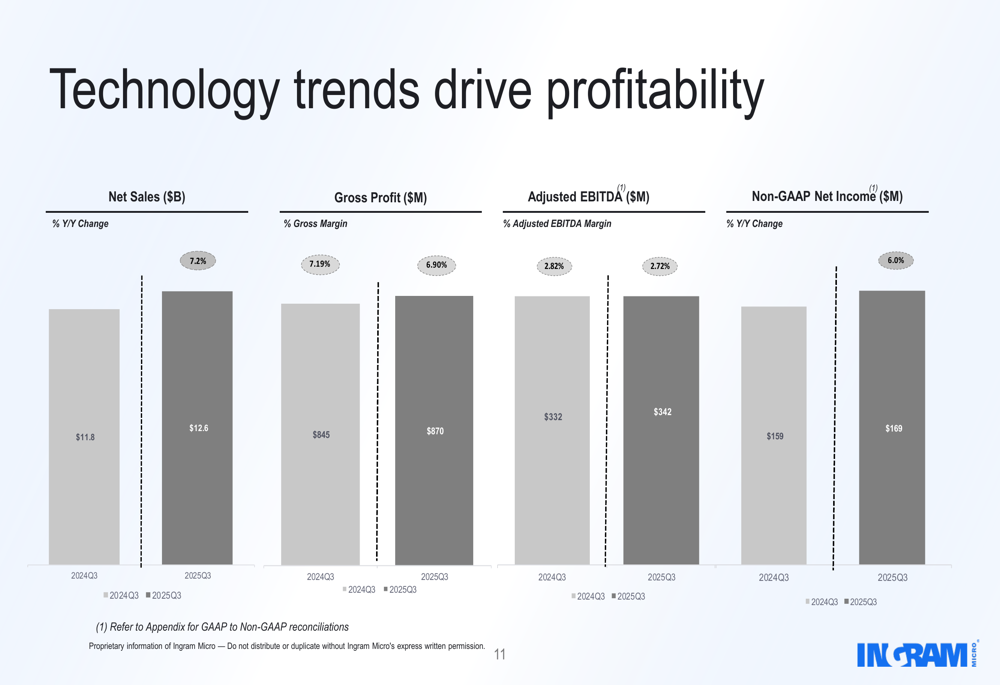

Ingram Micro reported solid top-line growth for Q3 2025, with net sales reaching $12.6 billion, a 7.2% increase year-over-year. The company achieved non-GAAP net income of $169 million, up 6.0% from the prior year, while adjusted EBITDA rose 3.2% to $342 million.

As shown in the following comprehensive performance snapshot:

The company highlighted operational efficiency improvements, with operating expenses as a percentage of net sales decreasing by 20 basis points year-over-year to 5.13%. However, gross margin compression was evident, declining from 7.19% in Q3 2024 to 6.90% in Q3 2025, suggesting pricing pressures or shifts in product mix.

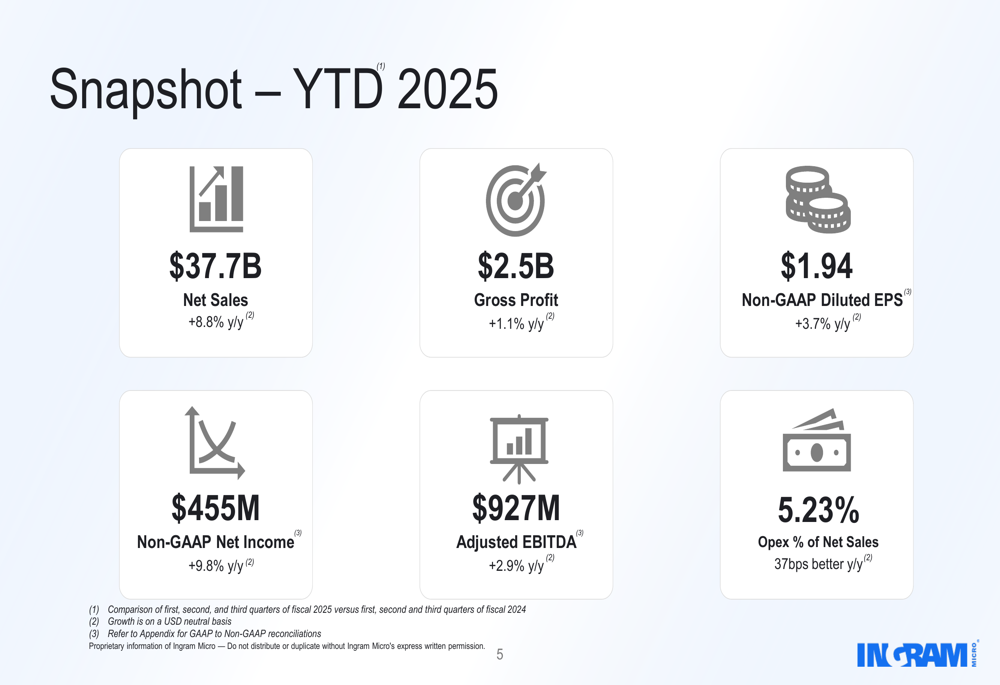

Year-to-date performance showed even stronger revenue growth at 8.8%, with non-GAAP net income up 9.8% compared to the same period in 2024:

Geographic Diversification

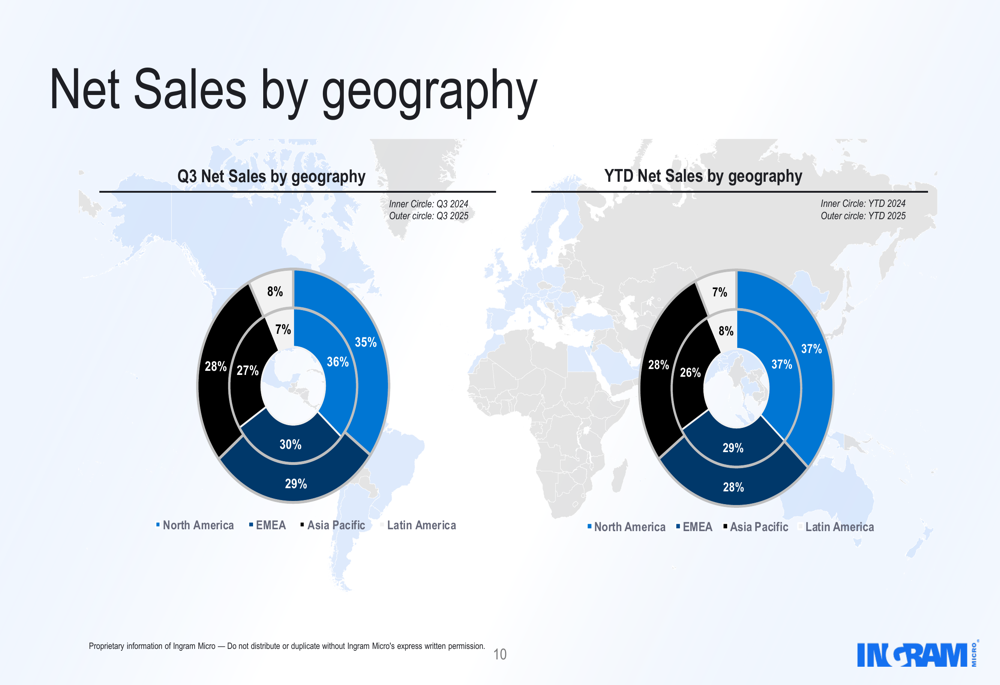

Ingram Micro's global footprint continues to evolve, with notable shifts in revenue contribution by region. Latin America and North America showed increased contribution to overall sales, while Asia Pacific's share slightly decreased in Q3 2025 compared to the prior year.

The following geographical breakdown illustrates the company's diverse revenue streams:

Asia Pacific remains the largest contributor at 35% of Q3 sales, followed by Latin America at 30%, North America at 28%, and EMEA at 8%. This geographic diversification provides some insulation against regional economic fluctuations, though the company faced a ransomware incident during the quarter that was not explicitly mentioned in the presentation materials.

Strategic Initiatives: AI Ecosystem

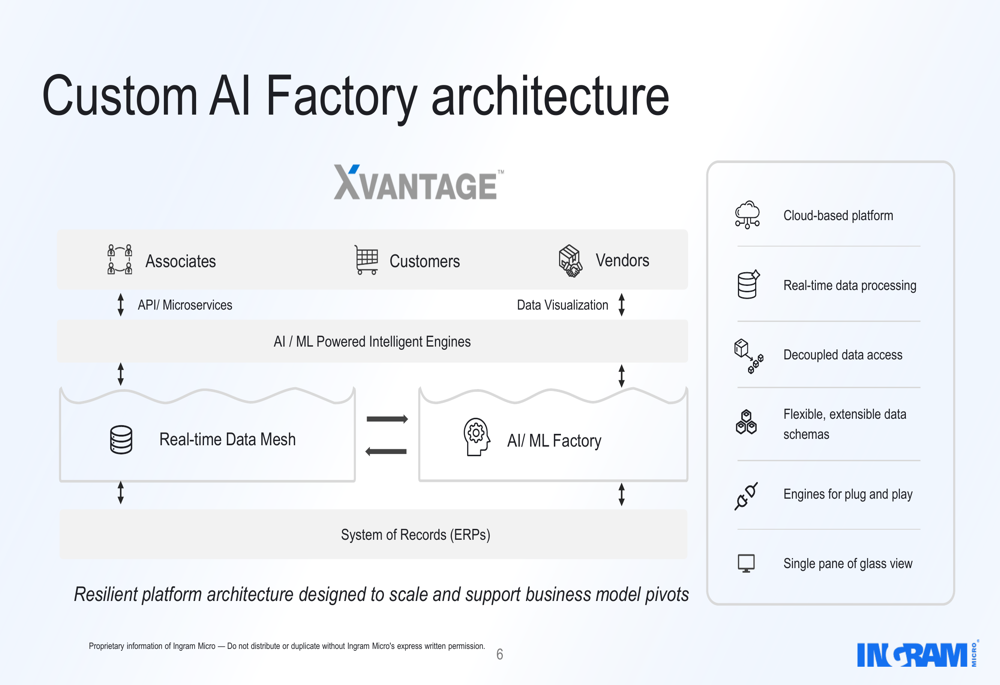

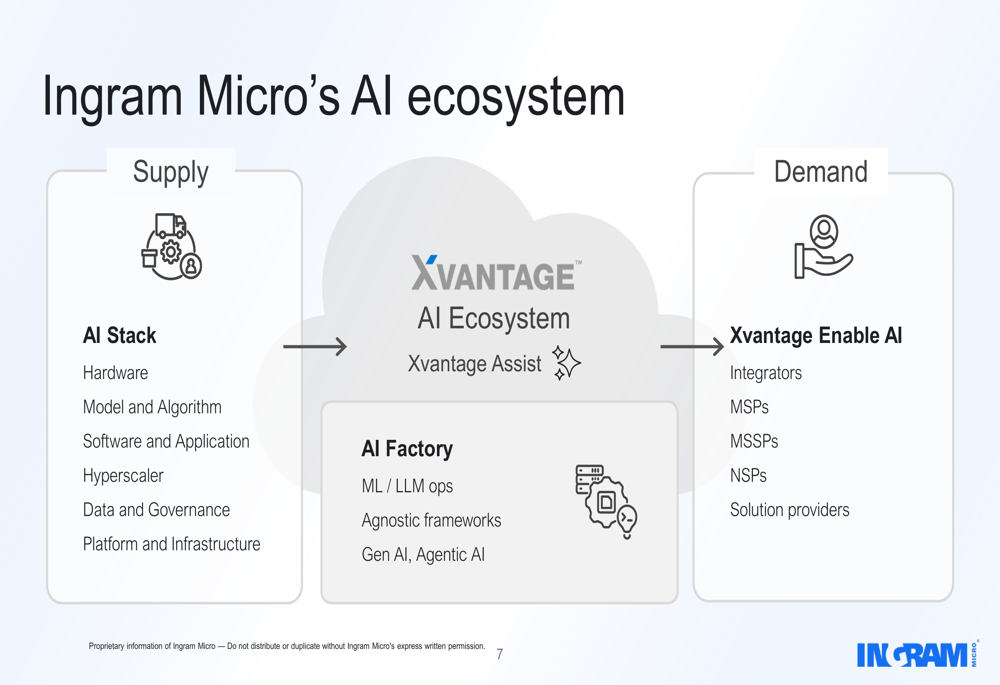

A significant portion of Ingram Micro's presentation focused on its artificial intelligence strategy, positioning the company to capitalize on emerging AI trends through its Xvantage platform. The company outlined its custom AI factory architecture and ecosystem approach:

This AI factory architecture represents Ingram Micro's effort to create a resilient, cloud-based platform with real-time data processing capabilities. The company is developing a comprehensive AI ecosystem that connects supply-side components with demand-side solution providers:

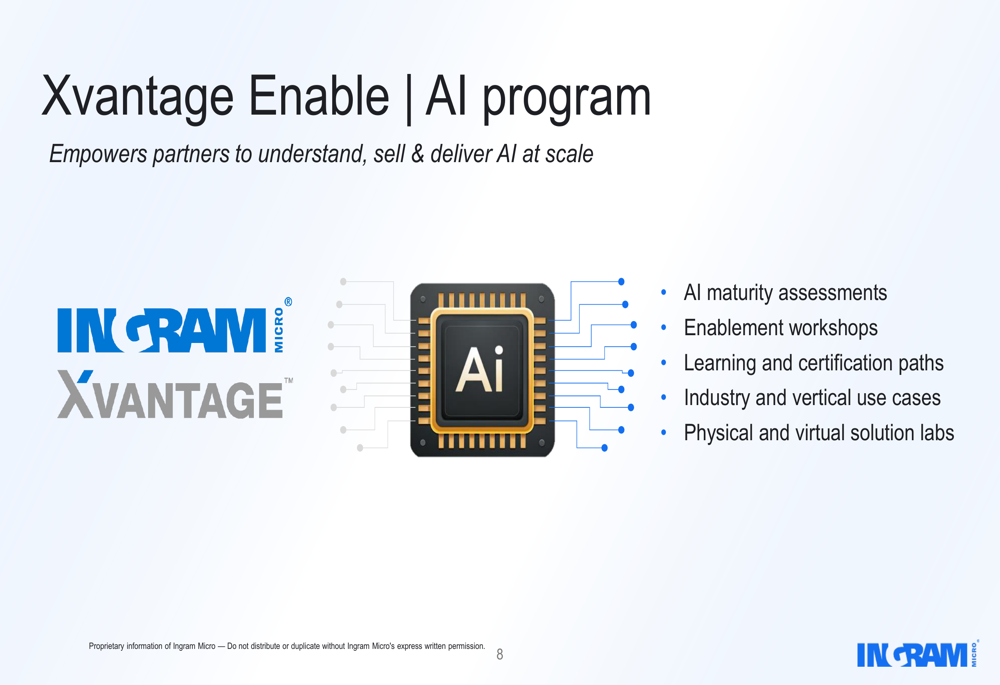

To support this ecosystem, Ingram Micro has launched the Xvantage Enable | AI program, designed to help partners understand, sell, and deliver AI solutions at scale:

The company reported continued momentum for its Xvantage platform, claiming "hundreds of millions in incremental revenue" and doubled quote-to-order conversion rates, though specific metrics were limited.

Detailed Financial Analysis

A closer examination of Ingram Micro's financial performance reveals mixed results. While revenue growth was robust, profitability metrics showed more modest improvements, as illustrated in the following comparison:

The company maintains a relatively strong balance sheet with $3.1 billion in available liquidity under its revolving credit facility. However, leverage ratios indicate substantial debt, with total debt to trailing twelve-month adjusted EBITDA at 2.8x and net debt to TTM adjusted EBITDA at 2.2x.

A concerning trend appears in the company's cash flow metrics, with negative adjusted free cash flow of $109.9 million for Q3 2025, improving from negative $254.6 million in Q3 2024 but still indicating challenges in cash generation. Year-to-date adjusted free cash flow stands at negative $531.9 million, compared to positive $106.1 million in the same period last year.

Forward-Looking Statements

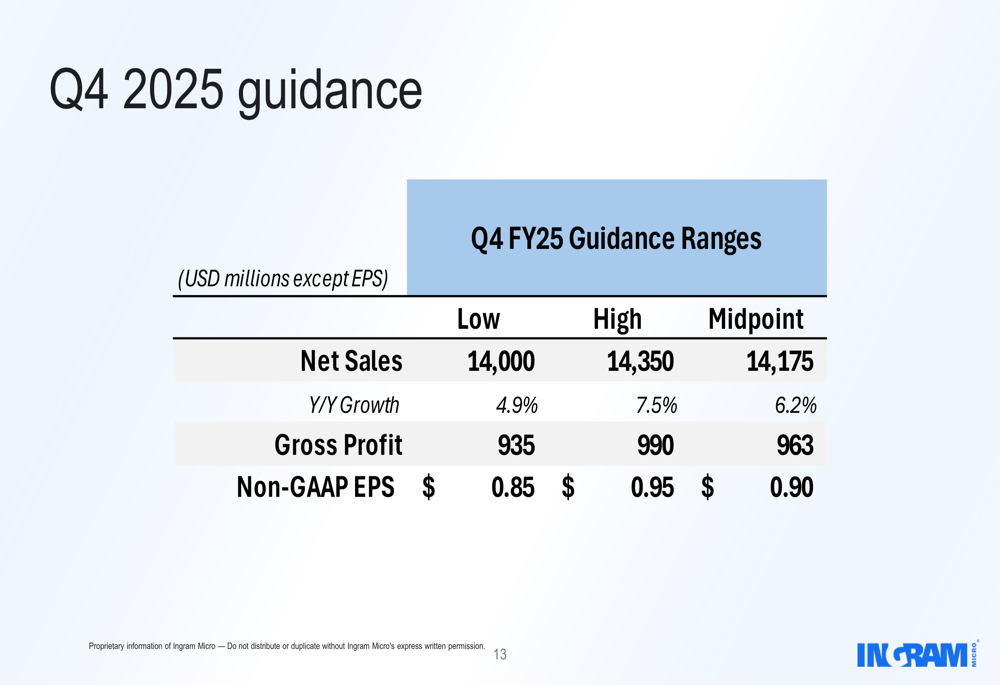

Looking ahead to Q4 2025, Ingram Micro provided guidance that suggests continued growth:

The company expects Q4 net sales between $14.0-14.35 billion, representing 6.2% year-over-year growth at the midpoint. Gross profit is projected at $935-990 million, with non-GAAP EPS guidance of $0.85-0.95.

During the earnings call, management addressed questions about the PC refresh cycle and potential extension through AI PCs, expressing optimism about the SMB segment recovery. The company did not report significant concerns regarding component cost inflation, which could support margin stability in coming quarters.

Conclusion

Ingram Micro's Q3 2025 presentation portrays a company experiencing solid revenue growth while navigating profitability challenges. The strategic focus on artificial intelligence and the Xvantage platform represents efforts to position for future growth opportunities, though current financial results show mixed performance.

While the EPS miss raises questions about the company's ability to translate revenue growth into proportional earnings growth, Ingram Micro's geographic diversification and strategic initiatives provide potential pathways for future value creation. Investors will likely watch closely for improvements in free cash flow and evidence that AI investments are generating tangible returns in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.