Trump announces trade deal with EU following months of negotiations

Introduction & Market Context

Insperity, Inc. (NYSE:NSP) released its first quarter 2025 earnings presentation on April 29, revealing a challenging start to the year with significant earnings declines despite modest growth in worksite employees. The company’s shares plunged 12.62% in premarket trading to $68.70, reflecting investor concerns about the reduced profitability and lowered full-year guidance.

The professional employer organization (PEO) faced headwinds from what it described as "macroeconomic turbulence and healthcare cost volatility," while continuing to invest in strategic initiatives aimed at future growth. These factors combined to create pressure on the company’s bottom line despite operational stability.

Quarterly Performance Highlights

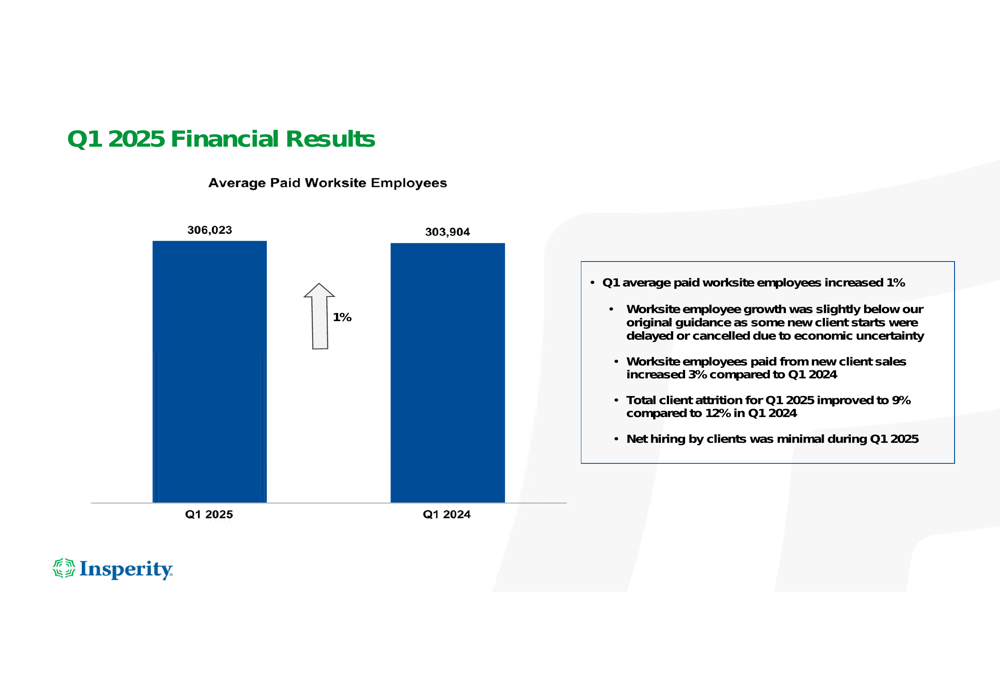

Insperity reported a 1% increase in average paid worksite employees, reaching 306,023 in Q1 2025 compared to 303,904 in Q1 2024. However, this growth fell slightly below the company’s original guidance, which management attributed to delayed or cancelled new client starts.

As shown in the following chart of worksite employee growth:

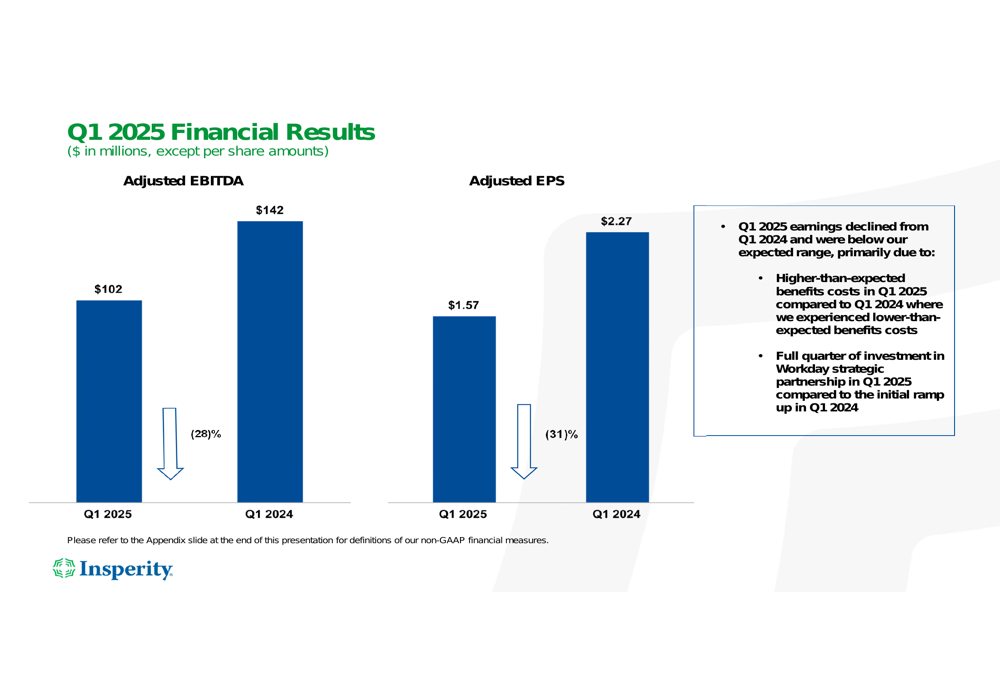

Despite the modest growth in worksite employees, the company’s financial performance deteriorated significantly. Adjusted EBITDA declined by 28% to $102 million from $142 million in the prior-year quarter, while adjusted earnings per share fell 31% to $1.57 from $2.27.

The following chart illustrates the substantial year-over-year declines in these key financial metrics:

The company cited two primary factors for the earnings decline: higher-than-expected benefits costs in Q1 2025 (compared to lower costs in Q1 2024) and a full quarter of investment in the Workday (NASDAQ:WDAY) strategic partnership. On a positive note, total client attrition improved to 9% from 12% in Q1 2024, indicating stronger client retention despite the challenging environment.

Detailed Financial Analysis

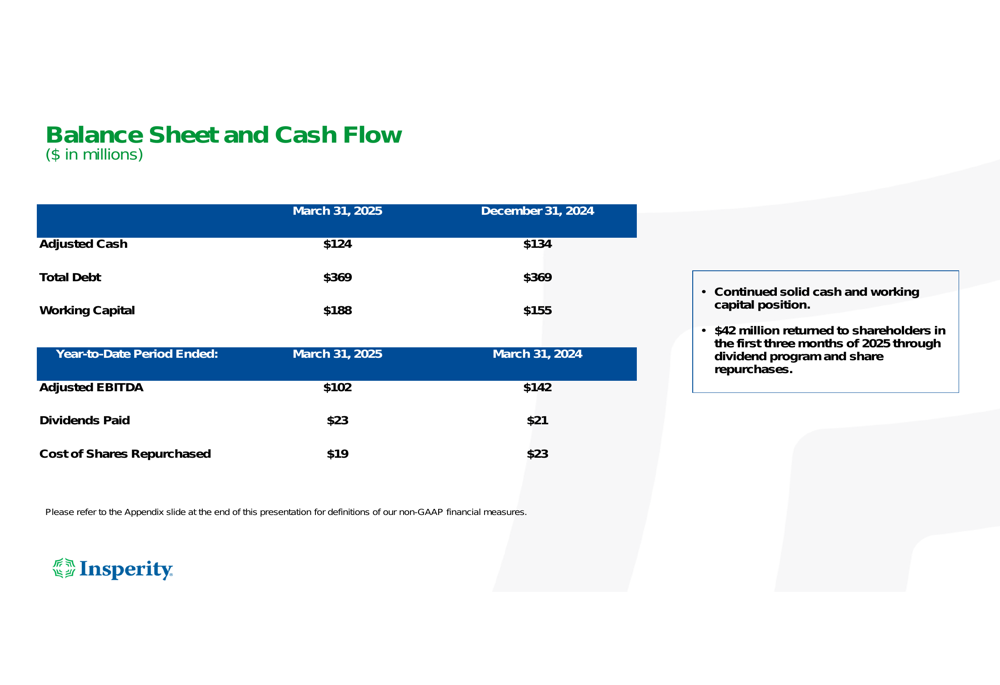

Insperity maintained a solid balance sheet position despite the earnings pressure. As of March 31, 2025, the company reported adjusted cash of $124 million, down slightly from $134 million at the end of 2024. Total (EPA:TTEF) debt remained unchanged at $369 million, while working capital improved to $188 million from $155 million at year-end 2024.

The company continued to return capital to shareholders, distributing $42 million through dividends ($23 million) and share repurchases ($19 million) during the quarter. This commitment to shareholder returns aligns with Insperity’s historical pattern, as noted in the previous earnings report which highlighted the company’s 20-year track record of consecutive dividend payments.

The following slide details the company’s balance sheet and cash flow metrics:

Forward-Looking Statements

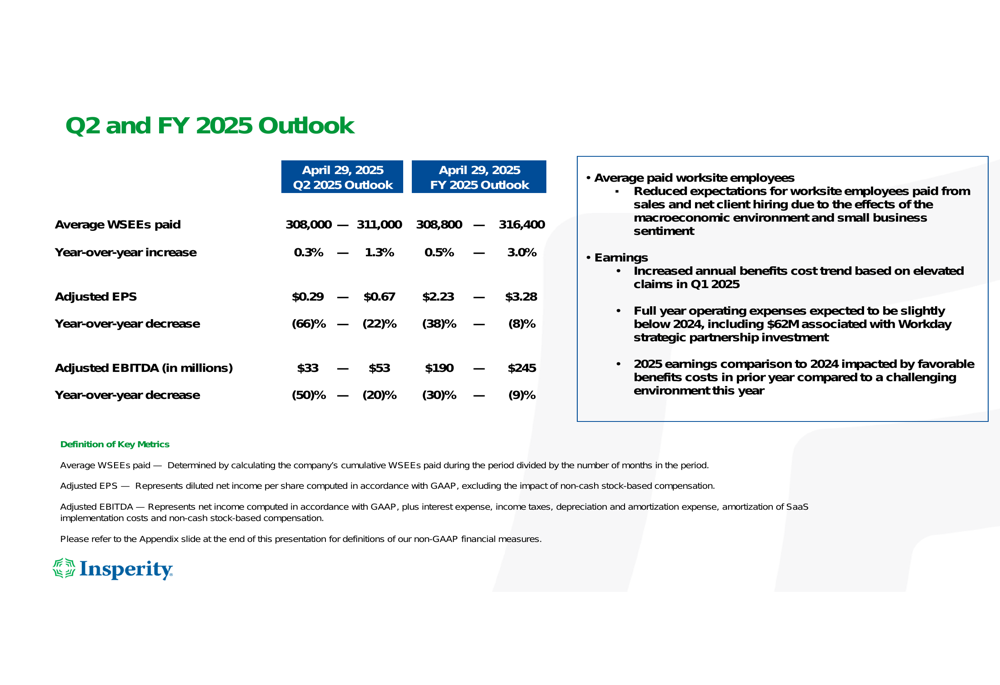

Insperity’s outlook for the remainder of 2025 reflects continued challenges, with the company projecting full-year adjusted EPS of $2.23 to $3.28, representing a year-over-year decrease of 8% to 38%. Similarly, adjusted EBITDA is expected to decline by 9% to 30%, reaching $190 to $245 million for the full year.

For the second quarter of 2025, the company forecasts average worksite employees of 308,000 to 311,000, a modest 0.3% to 1.3% increase year-over-year. However, Q2 adjusted EPS is projected to decline significantly by 22% to 66%, landing between $0.29 and $0.67.

The company’s detailed guidance is presented in the following table:

Management cited several key considerations affecting the outlook, including reduced expectations for worksite employees from sales and net client hiring due to macroeconomic factors, increased annual benefits cost trends, and continued investment in the Workday strategic partnership, which is expected to total $62 million for the full year.

Strategic Initiatives

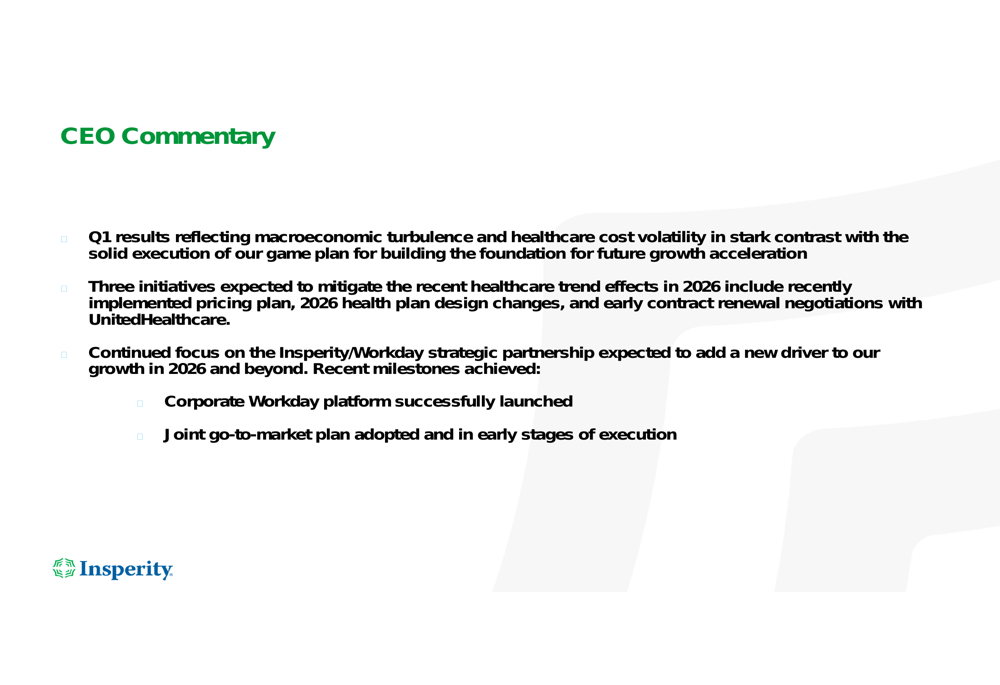

In his commentary, Insperity’s CEO outlined three key initiatives to mitigate healthcare trend effects in 2026: implementing a new pricing plan, making health plan design changes, and pursuing early contract renewal negotiations with UnitedHealthcare. These measures aim to address the healthcare cost volatility that has significantly impacted the company’s profitability.

The CEO’s commentary highlights these strategic priorities:

The company also emphasized its continued focus on the strategic partnership with Workday, which it expects to drive growth in 2026 and beyond. Recent milestones include the successful launch of the Corporate Workday platform and the adoption of a joint go-to-market plan. This aligns with information from the previous earnings call, which mentioned plans to deploy the Workday partnership in the first half of 2025 and noted the narrowing of an initial beta program to approximately 30 mid-market clients.

While these strategic initiatives position Insperity for potential future growth, the current financial impact is significant, with the Workday partnership investment contributing to the earnings decline in Q1 2025. The company appears to be in a transitional phase, balancing near-term profitability challenges against investments intended to strengthen its competitive position in the PEO market over the longer term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.