Bitcoin price today: steady near $92k after sharp losses; Fed caution weighs

Introduction & Market Context

inTest Corporation (NYSE:INTT) presented its second quarter 2025 financial results on August 6, 2025, showing sequential improvement from a challenging first quarter while continuing to navigate customer hesitation around capital spending. The company reported Q2 revenue of $28.1 million, up 6% sequentially but down from $34.0 million in the same quarter last year.

The results come after a disappointing Q1 2025 where inTest missed earnings expectations with an adjusted loss of $0.11 per share. The stock has been under pressure, trading near $6.93, closer to its 52-week low of $5.24 than its high of $9.77.

Quarterly Performance Highlights

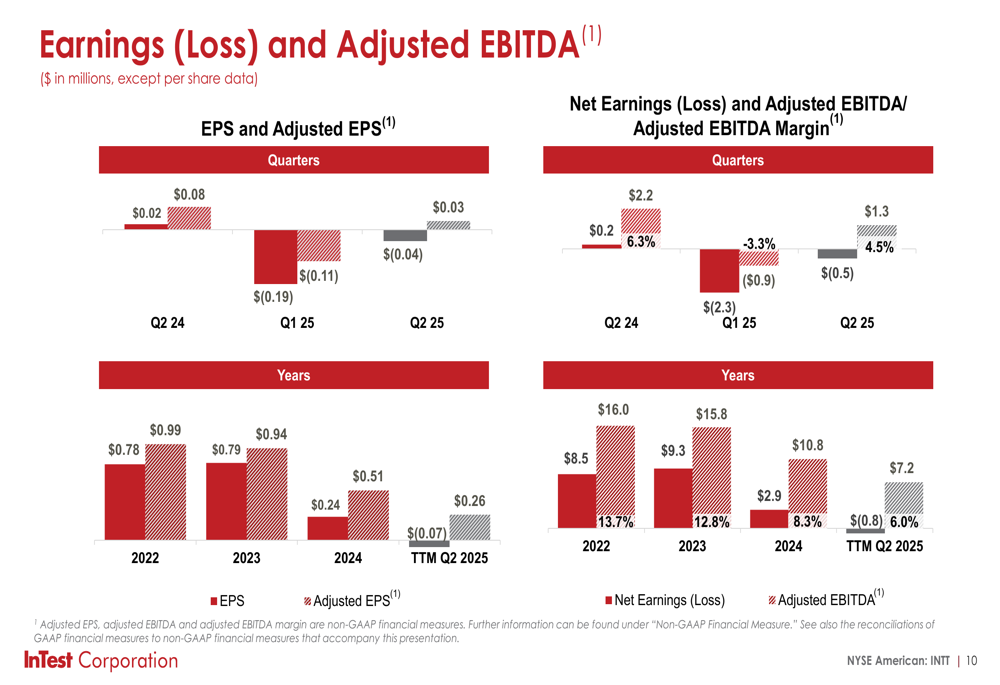

inTest reported Q2 2025 earnings per share of $0.03, a significant improvement from the $(0.19) loss in Q1 2025 and slightly better than the $0.02 reported in Q2 2024. However, adjusted EPS remained negative at $(0.04), though improved from $(0.11) in the previous quarter.

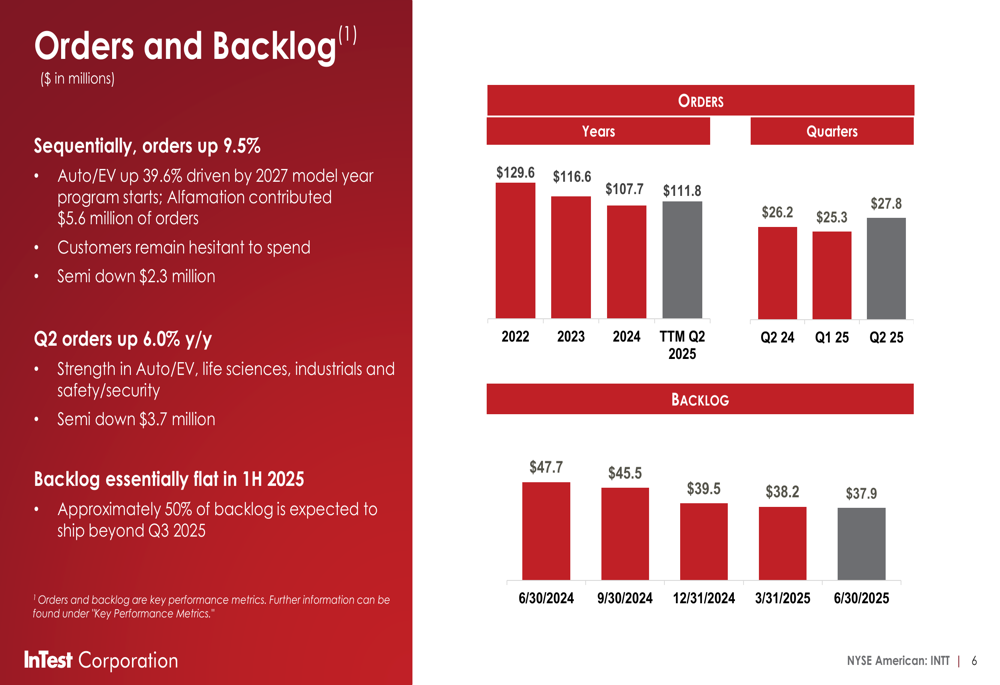

Orders showed positive momentum, increasing 6% year-over-year and 10% sequentially to $27.8 million, with particular strength in the automotive/EV sector where orders jumped 39.6% sequentially.

As shown in the following chart of orders and backlog trends, while quarterly orders have improved, the backlog has remained relatively flat in the first half of 2025:

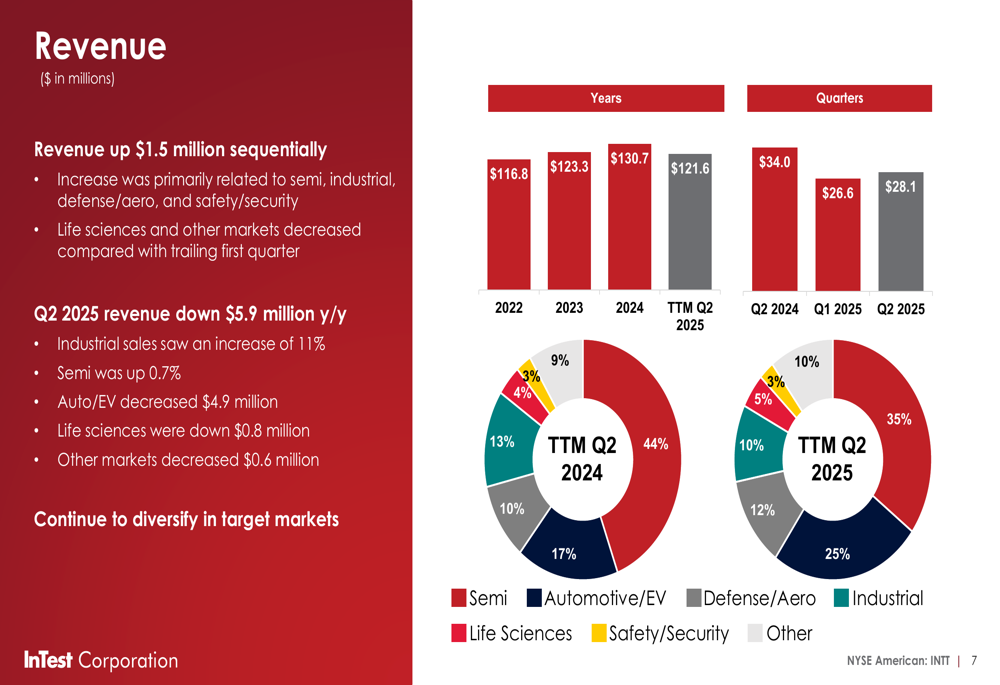

Revenue grew 6% sequentially to $28.1 million but remained down $5.9 million year-over-year. The company has made significant progress in market diversification, with the industrial sector now representing 35% of trailing twelve-month revenue, up from 10% in the prior year period, as illustrated in this revenue breakdown:

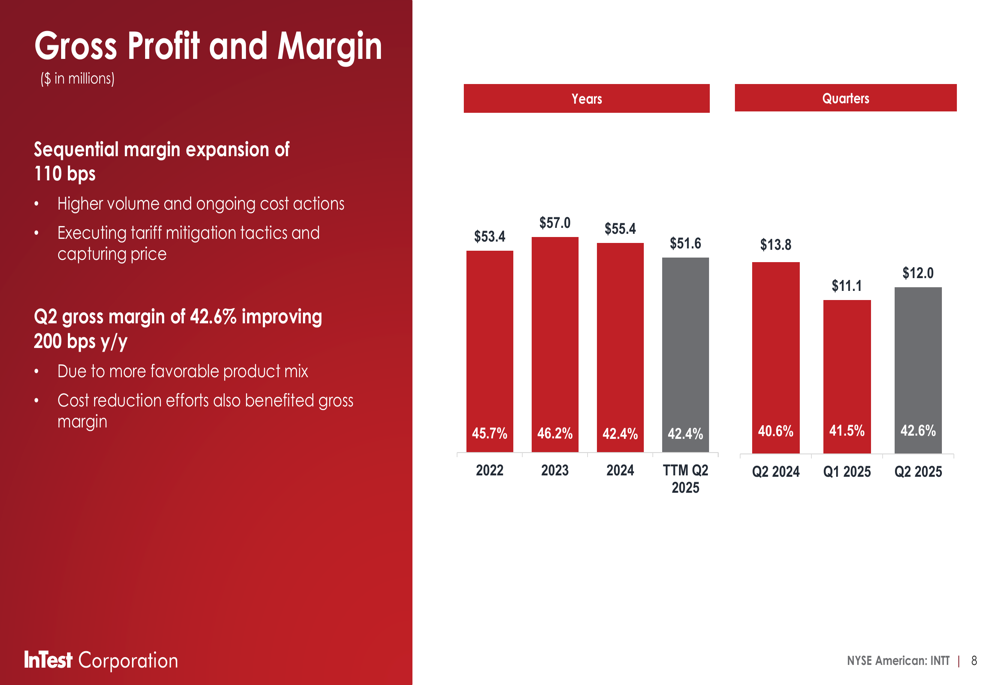

Gross margin showed notable improvement, reaching 42.6% in Q2 2025, up 200 basis points year-over-year and 110 basis points sequentially. Management attributed this to a more favorable product mix and ongoing cost reduction efforts:

Strategic Initiatives

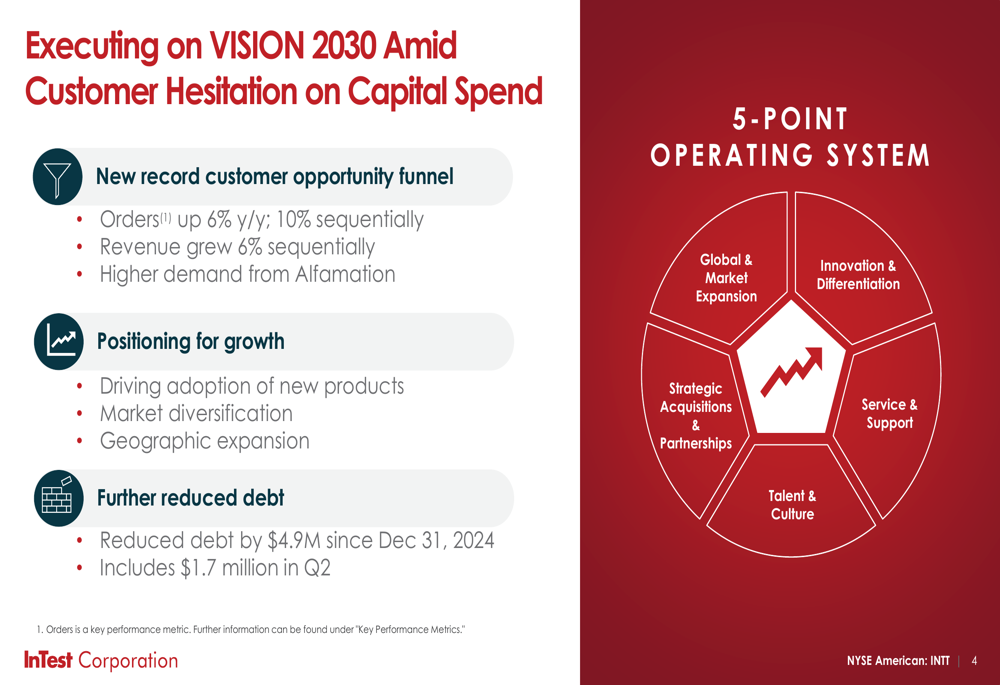

Despite market challenges, inTest continues to execute on its VISION 2030 growth strategy, focusing on five key areas: global and market expansion, innovation and differentiation, strategic acquisitions and partnerships, service and support, and talent and culture.

The company highlighted its progress on geographic expansion with a new facility in Penang, Malaysia, supporting its "In the Region, for the Region" strategy:

President and CEO Nick Grant emphasized the company’s strategic positioning: "Our opportunity funnel is at a historic peak, which provides optimism on what’s on the other side," a statement consistent with his comments from the previous quarter’s earnings call.

The following slide summarizes the company’s progress on its VISION 2030 strategy amid customer hesitation on capital spending:

Detailed Financial Analysis

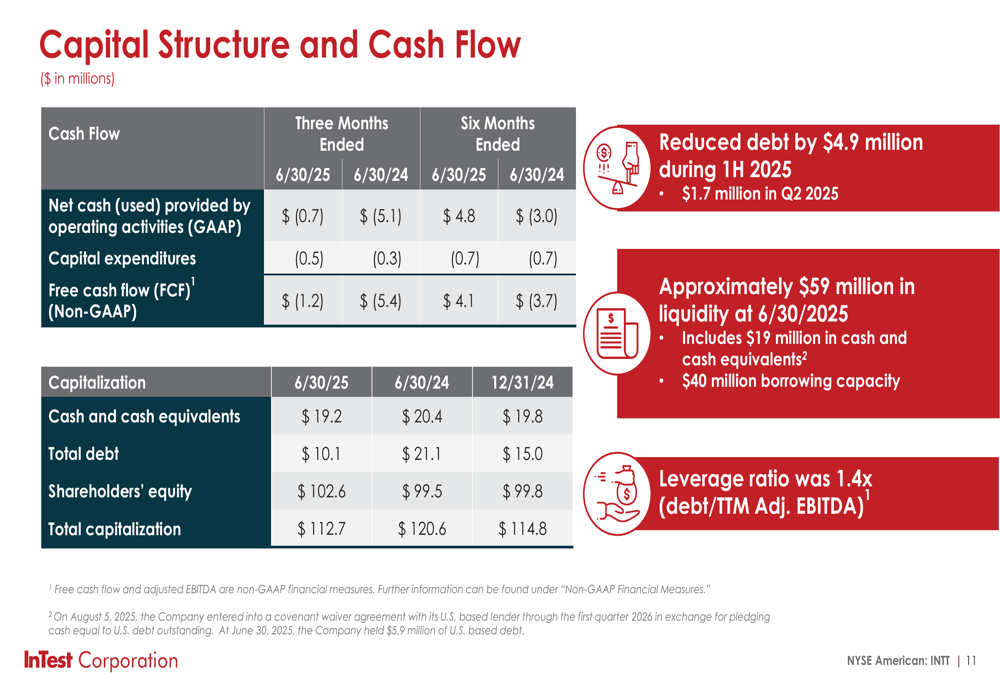

inTest continued to strengthen its balance sheet in Q2 2025, reducing debt by $1.7 million during the quarter and $4.9 million since December 31, 2024. The company reported $19.2 million in cash and cash equivalents as of June 30, 2025, with approximately $59 million in total liquidity including available borrowing capacity.

The company’s leverage ratio (debt/TTM Adjusted EBITDA) stood at 1.4x, as shown in this capital structure overview:

Earnings and adjusted EBITDA metrics showed mixed results, with Q2 2025 net earnings of $1.3 million compared to a loss of $(2.3) million in Q1 2025. However, adjusted EBITDA remained negative at $(0.5) million, though improved from $(0.9) million in the previous quarter:

Operating expenses decreased by $1.0 million sequentially and $0.6 million year-over-year, reflecting the company’s focus on cost management and austerity measures, including consolidating Videology facilities for an estimated $0.5 million in annualized savings beginning in 2026.

Forward-Looking Statements

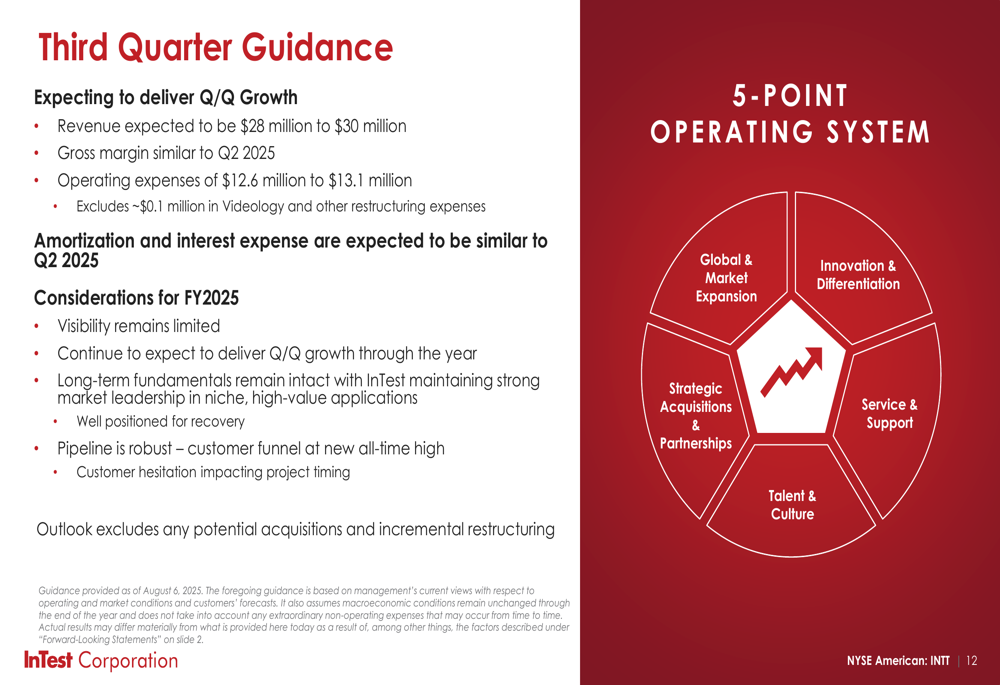

For the third quarter of 2025, inTest provided guidance for revenue between $28 million and $30 million, suggesting continued sequential growth. The company expects gross margin to remain similar to Q2 2025 levels, with operating expenses projected at $12.6 million to $13.1 million, excluding approximately $0.1 million in restructuring expenses.

Management noted that while visibility remains limited, they continue to expect quarter-over-quarter growth through the year, emphasizing that long-term fundamentals remain intact with inTest maintaining strong market leadership in niche, high-value applications:

The company remains confident in its strategic direction, highlighting its healthy balance sheet, record customer opportunity funnel, and progress on market diversification:

While inTest faces continued market challenges, its sequential improvement in Q2 2025 and focus on strategic initiatives suggest the company is taking appropriate steps to position itself for recovery when market conditions improve. Investors will be watching closely to see if the projected sequential growth materializes in Q3 and whether customer hesitation on capital spending begins to ease.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.