ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Inwido AB (STO:INWI), Europe’s leading window group, released its Q2 2025 interim report on July 14, 2025, showing stable performance despite challenging market conditions. The company’s stock closed at SEK 207.20 on July 11, down 1.99% ahead of the announcement, reflecting investor caution about the company’s growth trajectory.

Inwido, which holds the top position in the Nordic window market and ranks second in the UK, reported that the expected market recovery has been further delayed. Despite this, the company has strengthened its market positions and gained market share across key regions.

As shown in the following overview of Inwido’s market position and strategic goals:

Quarterly Performance Highlights

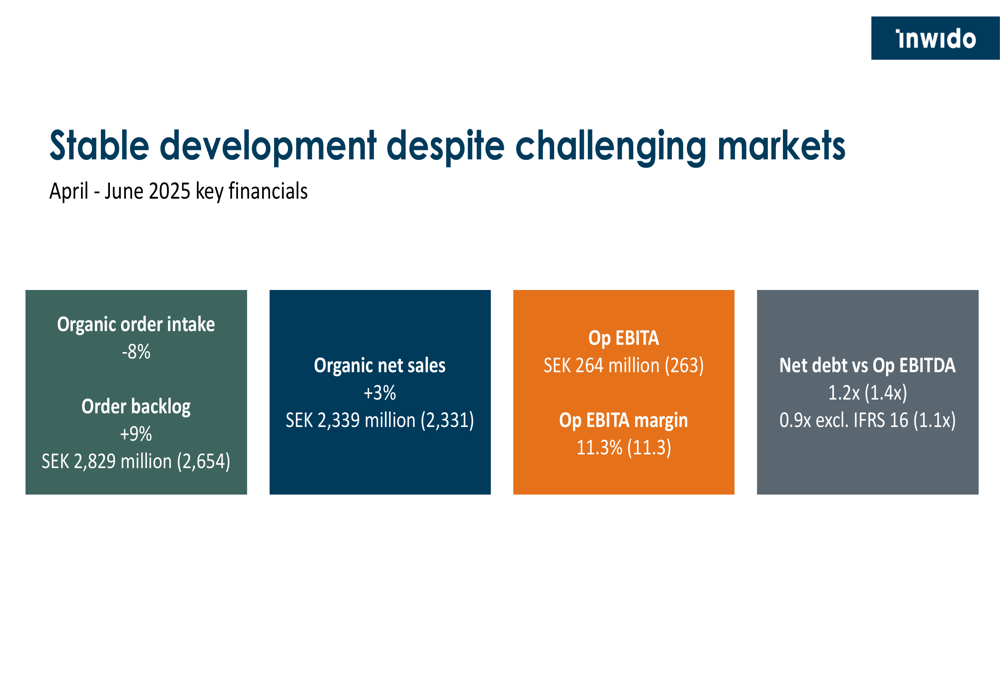

Inwido achieved organic sales growth of 3% in Q2 2025, reaching SEK 2,339 million compared to SEK 2,331 million in the same period last year. The company maintained its operating EBITA margin at 11.3%, despite facing price pressure, negative mix effects, and adverse foreign exchange impacts.

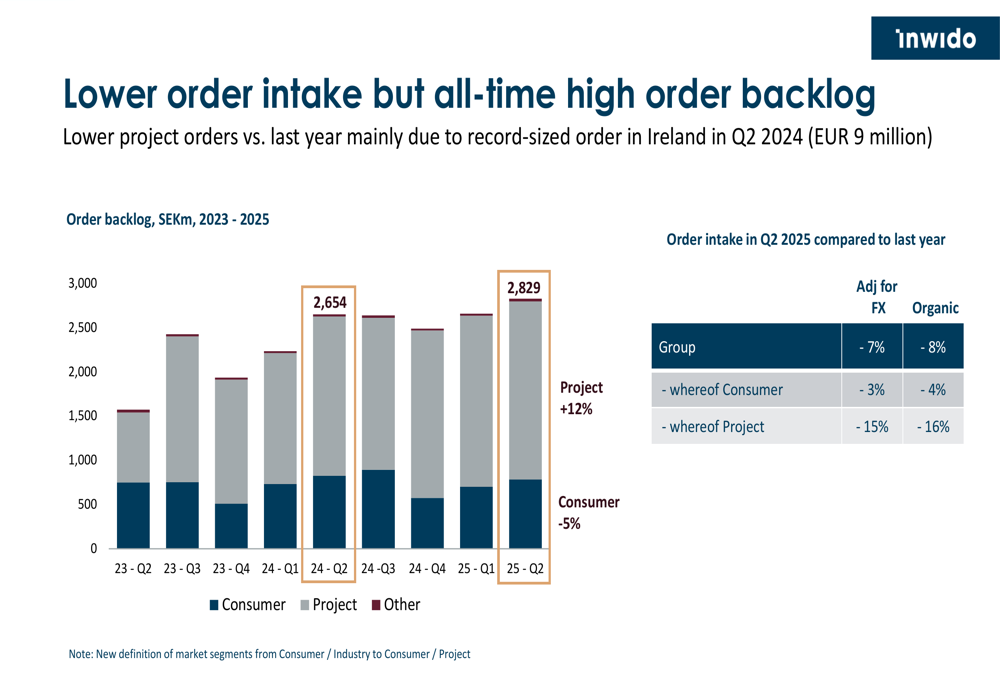

Order intake decreased by 8% organically, primarily due to lower project orders compared to last year, which included a record-sized order in Ireland worth EUR 9 million in Q2 2024. Despite the decline in new orders, Inwido reported an all-time high order backlog, up 9% organically to SEK 2,829 million.

The following slide highlights Inwido’s key financial metrics for Q2 2025:

Earnings per share improved to SEK 2.69 in Q2 2025, up from SEK 2.52 in the same period last year, representing a 6.7% increase. This performance marks a significant slowdown from Q1 2025, when the company reported a 78% increase in EPS according to previous earnings reports.

Detailed Financial Analysis

Inwido maintained its gross margin at 25.6% in Q2 2025, identical to the previous year, while slightly improving its operating EBITDA margin to 14.9% from 14.8%. The company’s financial position strengthened with reduced gearing and strong cash flow generation.

The comprehensive financial breakdown shows consistent performance across key metrics:

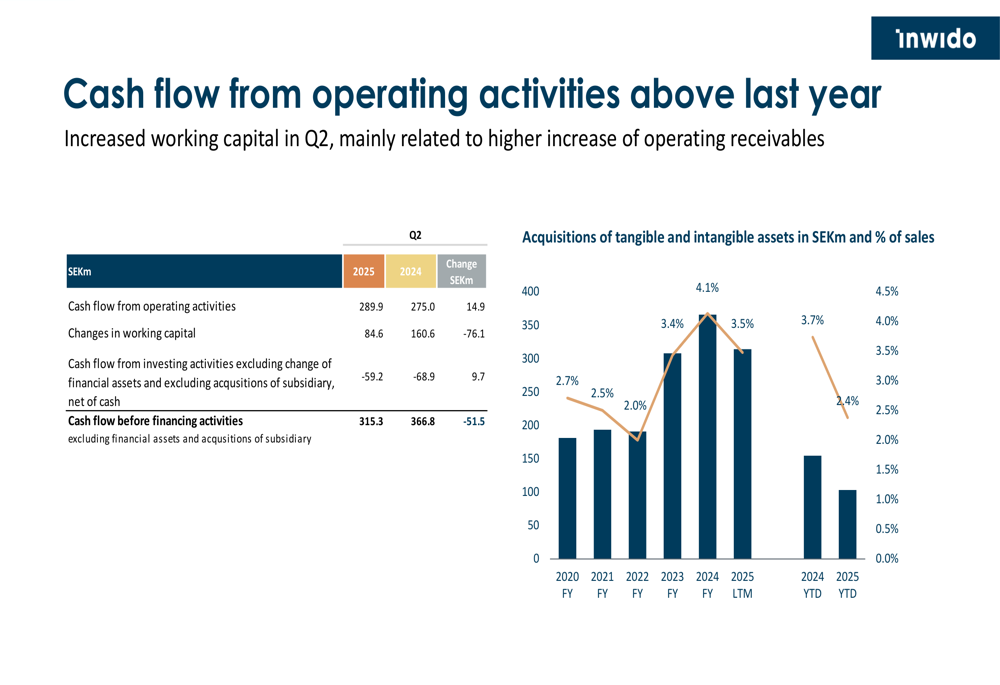

Cash flow from operating activities improved to SEK 289.9 million in Q2 2025, up from SEK 275.0 million in Q2 2024. This increase came despite lower working capital contributions, which decreased to SEK 84.6 million from SEK 160.6 million in the previous year, primarily due to higher operating receivables.

The company’s financial position continues to strengthen, with net debt to operating EBITDA ratio improving to 1.2x (including IFRS 16) from 1.4x last year, and 0.9x (excluding IFRS 16) from 1.1x. This improvement occurred despite a dividend payment of SEK 319 million during the quarter.

The following chart illustrates Inwido’s cash flow and investment activities:

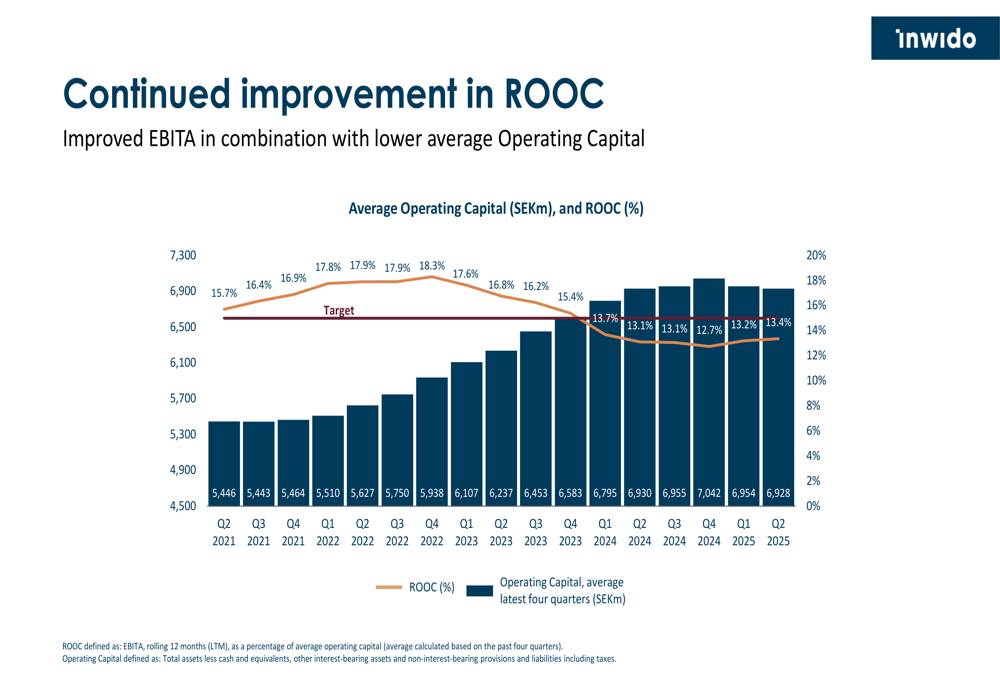

Return on operating capital (ROOC) improved to 13.4% from 13.1% last year, reflecting enhanced capital efficiency:

Business Area Performance

Inwido’s performance varied significantly across its four business areas, with Scandinavia and Eastern Europe showing growth while e-Commerce and Western Europe faced challenges.

Scandinavia delivered 5% sales growth to SEK 1,168 million, driven by the project market in Sweden. Operating EBITA increased to SEK 169 million, though gross margins declined due to changes in market mix, offset by effective cost control.

Eastern Europe achieved 1% sales growth to SEK 443 million, with Operating EBITA increasing to SEK 29 million and margin improving to 6.6%. The region benefited from increased project sales.

In contrast, e-Commerce sales declined by 7% to SEK 289 million in a challenging consumer market, with Operating EBITA decreasing to SEK 26 million and margin falling to 9.1%. However, order intake increased by 7%, suggesting potential improvement in coming quarters.

Western Europe experienced an 8% sales decline to SEK 433 million, with order intake down 34%, reflecting difficult market conditions particularly in the UK. Operating EBITA decreased to SEK 48 million with margin falling to 11.1%.

The order intake and backlog situation provides insight into future business prospects:

Strategic Initiatives & Outlook

Inwido continues to make progress on its 2030 roadmap, which targets SEK 20 billion in sales by 2030. The company is pursuing acquisitions to expand its geographic footprint, though market uncertainty has lengthened acquisition processes.

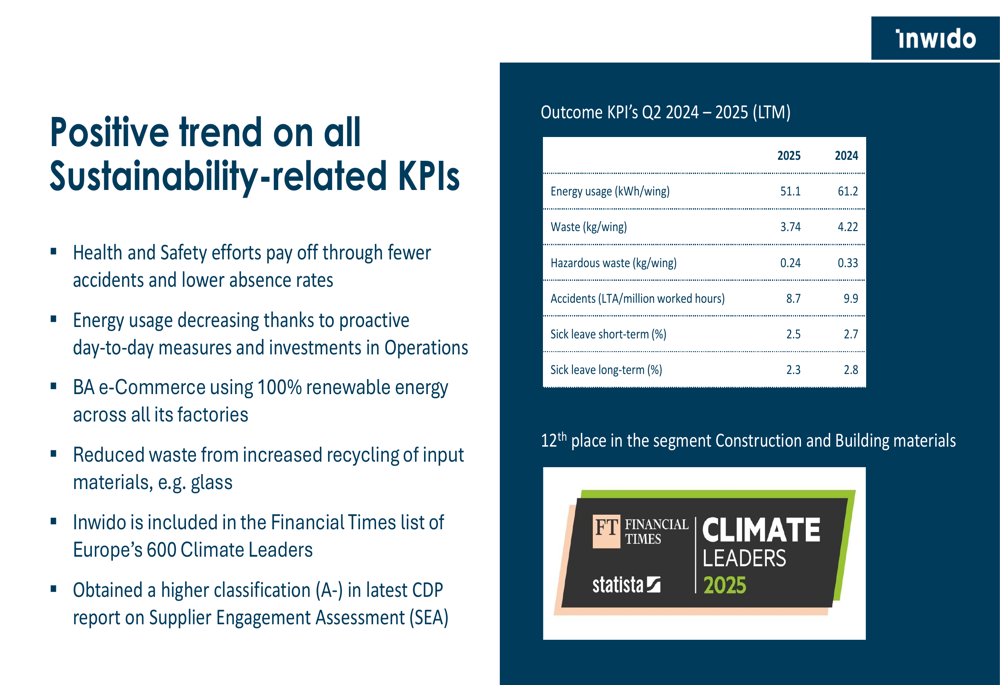

Sustainability remains a key focus, with the company reporting positive trends across environmental metrics. Energy usage decreased thanks to proactive measures and investments, with the e-Commerce business unit now using 100% renewable energy across all factories. Inwido was included in the Financial Times list of Europe’s 600 Climate Leaders and obtained a higher classification (A-) in the latest CDP report on Supplier Engagement Assessment.

The company’s sustainability performance shows notable improvements:

Looking ahead, Inwido’s management indicated that while market rebound is delayed, the company has strong fundamentals, including an all-time high order backlog and strengthened market positions. The company continues to make progress on strategic priorities and maintains high M&A activity despite challenging market conditions.

CEO Fredrik Meuller emphasized that Inwido is gaining market share despite volume challenges, positioning the company well for when market conditions improve. The company remains committed to its long-term strategy while navigating the current market environment with disciplined cost management and strategic investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.