Can anything shut down the Gold rally?

Introduction & Market Context

Interpublic Group of Companies Inc (NYSE:IPG) released its second quarter 2025 financial results on July 22, showing continued revenue pressure but improved profitability metrics. The advertising and marketing services company reported a 3.5% organic decline in net revenue while achieving margin expansion through restructuring efforts. IPG shares responded positively in premarket trading, rising 2.58% to $24.64, building on momentum from its Q1 results when the stock jumped 4.42%.

The results come as IPG continues to make progress toward its planned acquisition by Omnicom, expected to close in the second half of 2025. The company is operating in a challenging macroeconomic environment, with significant regional variations in performance.

Quarterly Performance Highlights

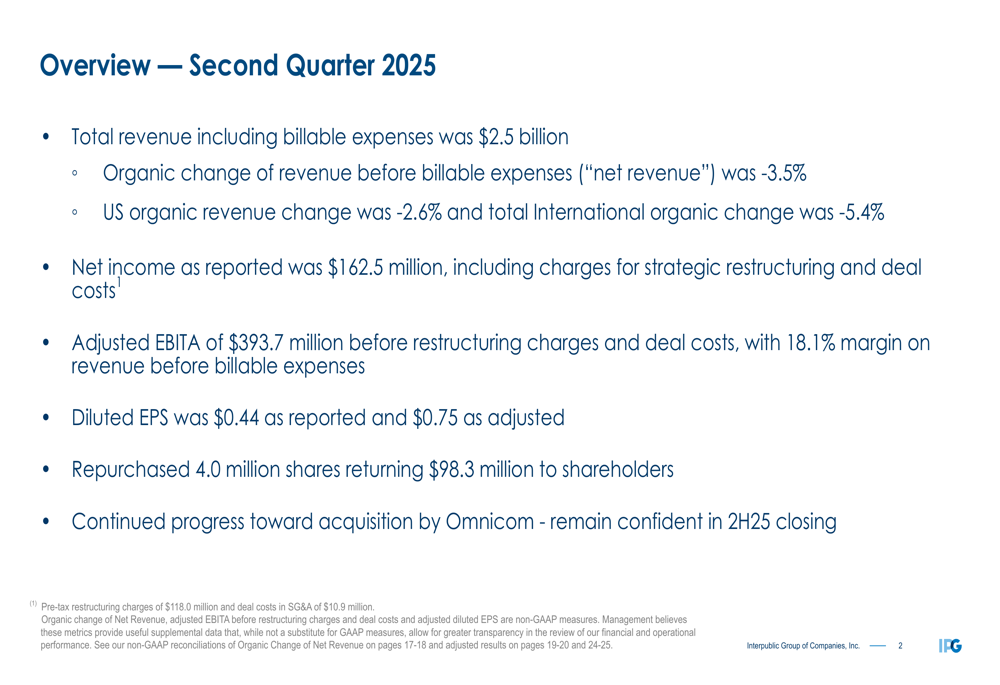

IPG reported total revenue of $2.5 billion for Q2 2025, with net revenue (revenue before billable expenses) of $2.17 billion, representing an organic decline of 3.5% compared to the same period last year. Net income was $162.5 million, resulting in reported earnings per share of $0.44, or $0.75 on an adjusted basis.

As shown in the following overview of second quarter results:

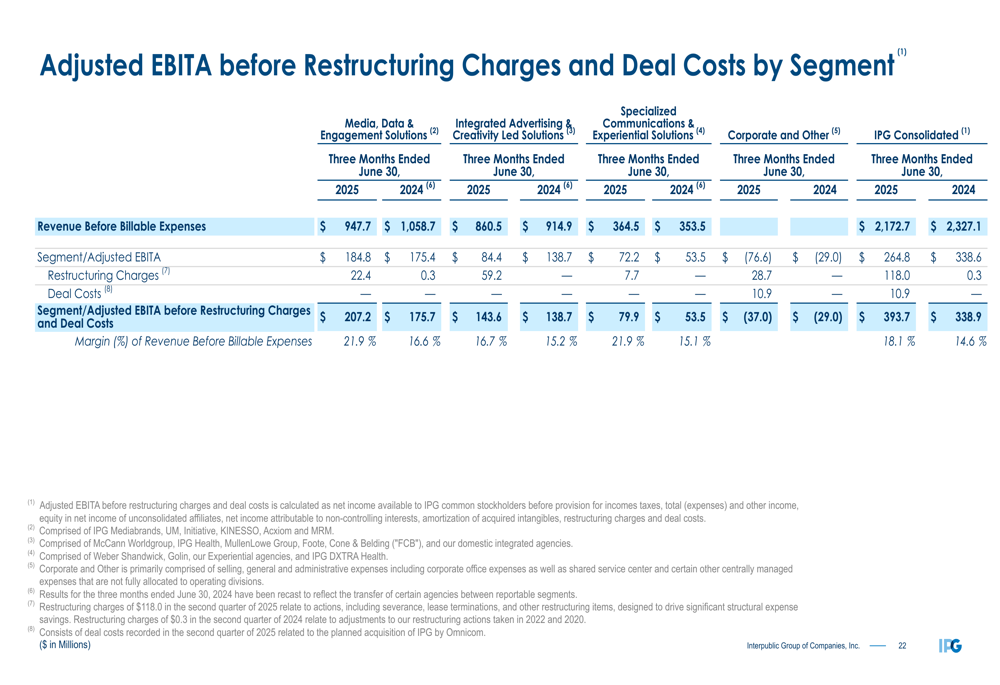

The company’s adjusted EBITA before restructuring charges and deal costs reached $393.7 million, representing an 18.1% margin on net revenue. This margin improvement came despite the revenue contraction, highlighting the effectiveness of IPG’s cost management initiatives. During the quarter, IPG also returned $98.3 million to shareholders through the repurchase of 4.0 million shares.

Detailed Financial Analysis

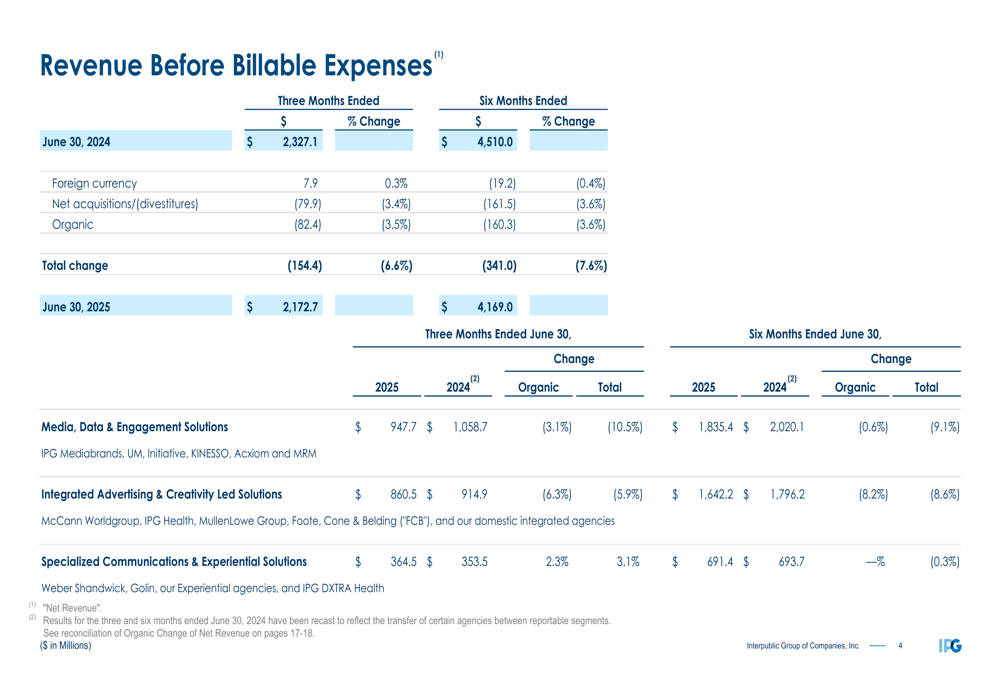

IPG’s performance varied significantly across business segments and geographic regions. The company’s Media, Data & Engagement Solutions segment saw a 3.1% organic decline, while Integrated Advertising & Creativity Led Solutions experienced a steeper 6.3% drop. The Specialized Communications & Experiential Solutions segment was the only bright spot, posting 2.3% organic growth.

The following breakdown illustrates the segment performance for Q2 2025:

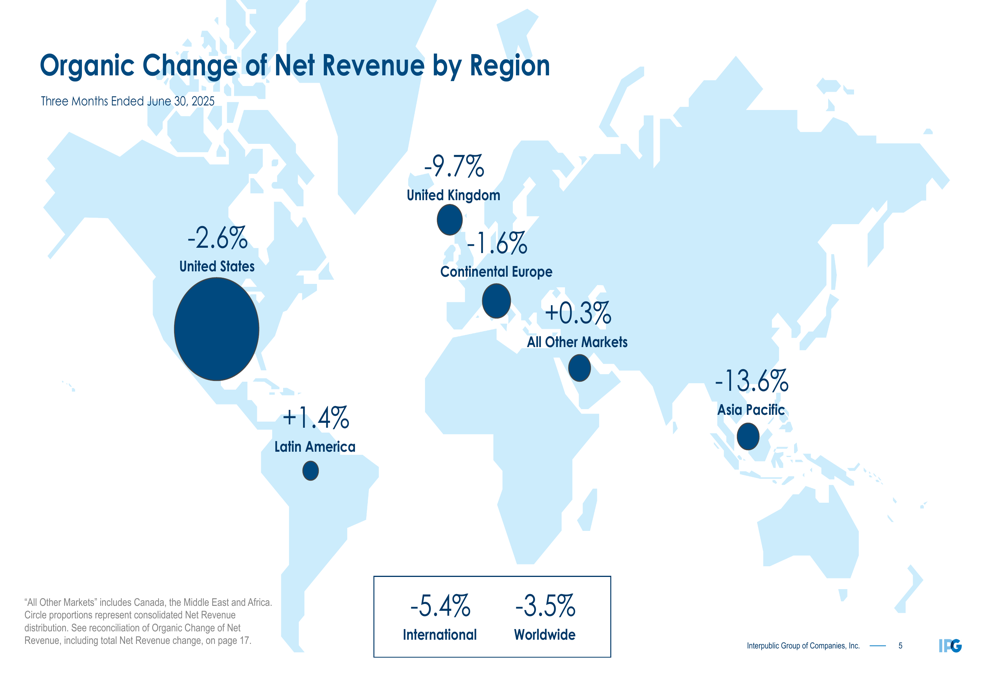

From a geographic perspective, IPG faced challenges across most regions, with Asia Pacific (-13.6%) and the United Kingdom (TADAWUL:4280) (-9.7%) showing the steepest declines. The United States, which represents the company’s largest market, saw a 2.6% organic decline. Latin America was one of the few regions showing growth, with a 1.4% organic increase.

The regional performance is visualized in this world map showing organic change of net revenue:

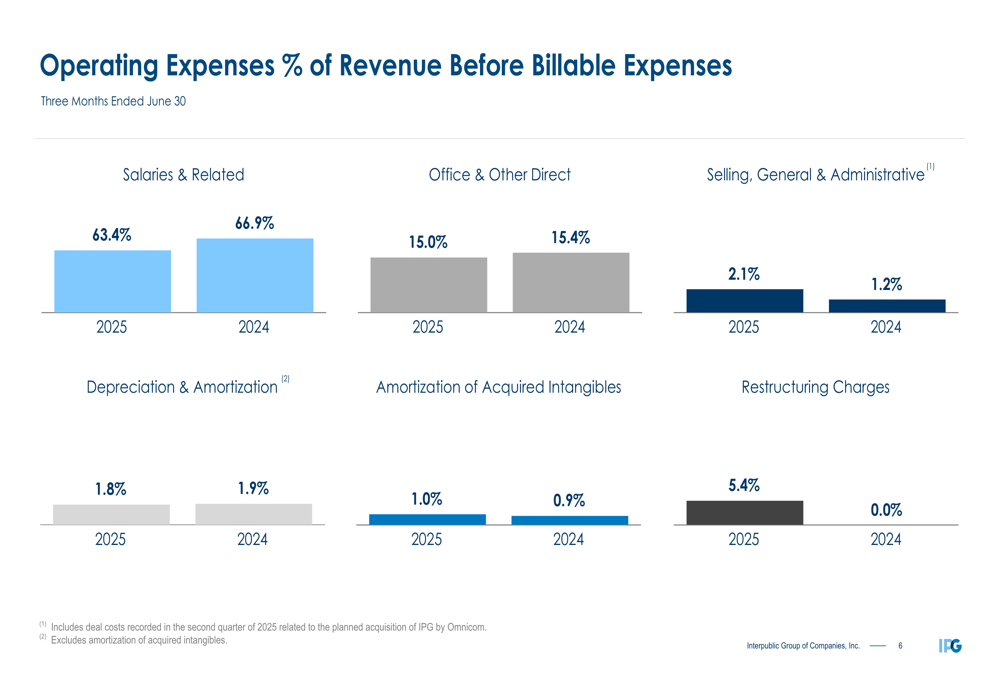

Operating expenses as a percentage of net revenue showed significant shifts compared to the previous year. Salaries and related expenses decreased to 63.4% from 66.9%, reflecting the company’s restructuring efforts. However, restructuring charges represented 5.4% of net revenue in Q2 2025 compared to nearly zero in the prior year.

The following chart details the operating expense ratios:

Strategic Initiatives

IPG’s financial results reflect its ongoing strategic transformation, with significant restructuring charges of $118.0 million in Q2 2025. These efforts appear to be yielding results, as evidenced by the improved adjusted EBITA margin of 18.1%, up from 14.6% in Q2 2024.

The company’s segment profitability shows improvements across all operating units despite revenue challenges:

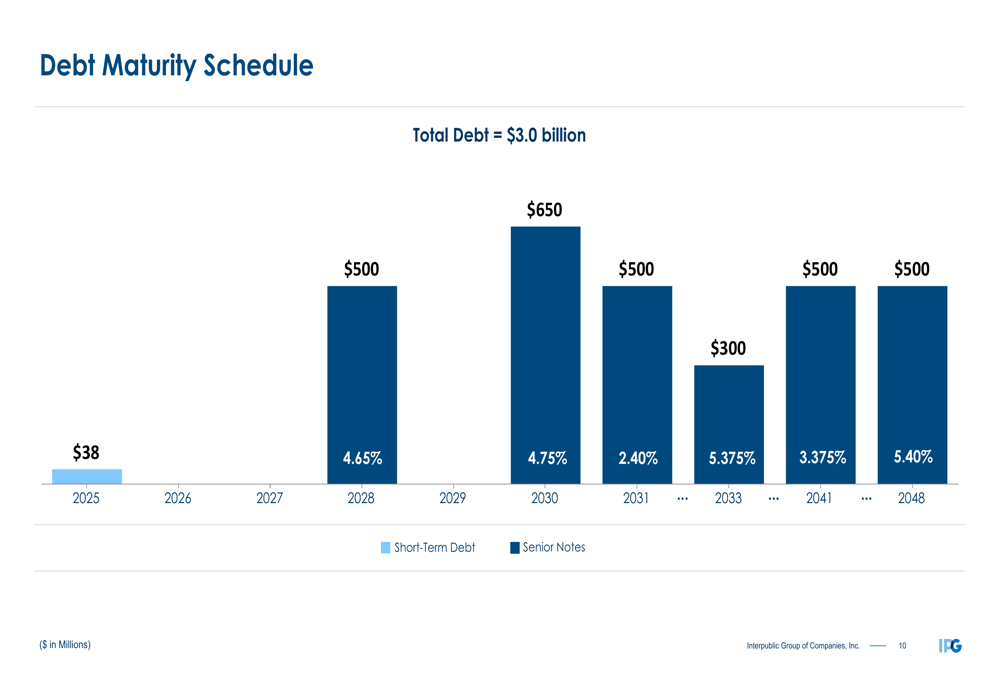

IPG’s balance sheet remains solid with $1.56 billion in cash and cash equivalents as of June 30, 2025. The company maintains a well-structured debt profile of $3.0 billion with maturities spread through 2048, providing financial flexibility.

The debt maturity schedule is illustrated below:

Forward-Looking Statements

IPG continues to make progress toward its acquisition by Omnicom, with closing expected in the second half of 2025. The deal-related costs are impacting current financial results but are viewed as a one-time expense related to the strategic transaction.

The company’s Q2 results indicate a continued organic revenue decline (-3.5%) that exceeds the full-year guidance provided after Q1 results (organic decrease of 1-2%). This suggests potential challenges in meeting the annual revenue targets unless performance improves in the second half of the year.

Cash flow remains an area of concern, with net cash used in operating activities of $96.0 million in Q2 2025, compared to $120.7 million provided in Q2 2024. This negative operating cash flow warrants monitoring as the company progresses through its restructuring program and merger process.

While the revenue environment remains challenging, IPG’s margin improvements demonstrate that its restructuring initiatives are delivering the intended cost savings. The company’s adjusted earnings per share of $0.75 for Q2 2025 shows resilience in the face of top-line pressures, positioning IPG to potentially deliver improved shareholder value as it moves toward the Omnicom merger completion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.