5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Interpublic Group (NYSE:IPG) released its second quarter 2025 earnings presentation on July 22, 2025, revealing a challenging revenue environment offset by record-high margins amid ongoing restructuring efforts. The advertising and marketing services conglomerate continues to make progress toward its pending acquisition by Omnicom Group, which is expected to close in the second half of 2025.

IPG’s stock closed slightly up at $26.11 in regular trading on the day of the announcement, though it fell 1.72% in premarket trading to $25.66, reflecting mixed investor sentiment about the results.

Quarterly Performance Highlights

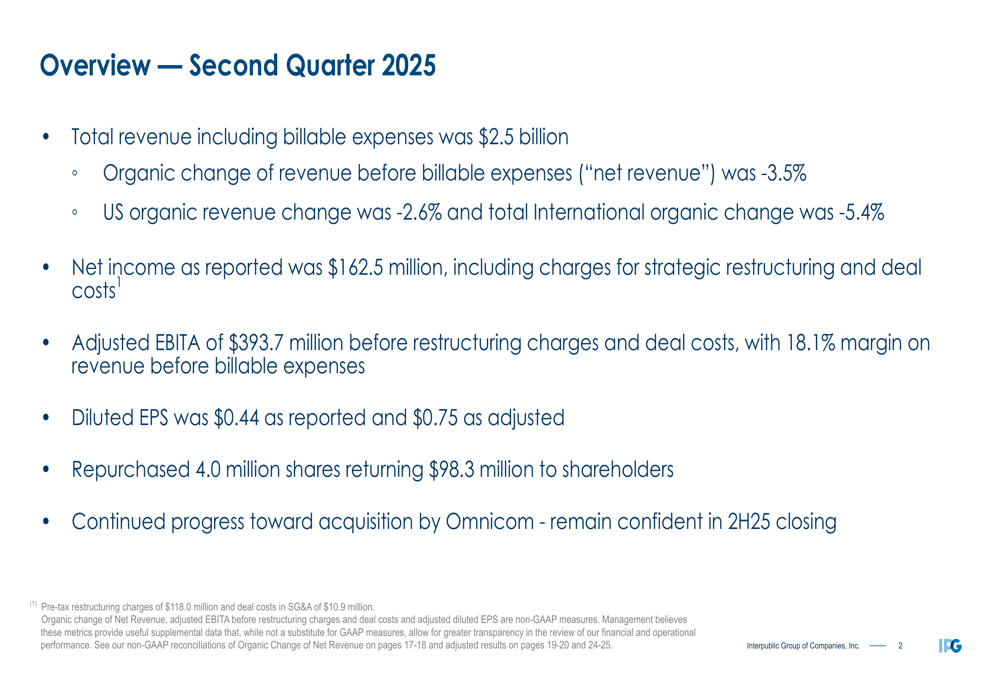

IPG reported total revenue including billable expenses of $2.5 billion for Q2 2025, with an organic decline in net revenue of 3.5% compared to the same period last year. The company’s U.S. operations performed relatively better with a 2.6% organic revenue decline, while international markets saw a steeper 5.4% drop.

As shown in the following overview of key financial metrics:

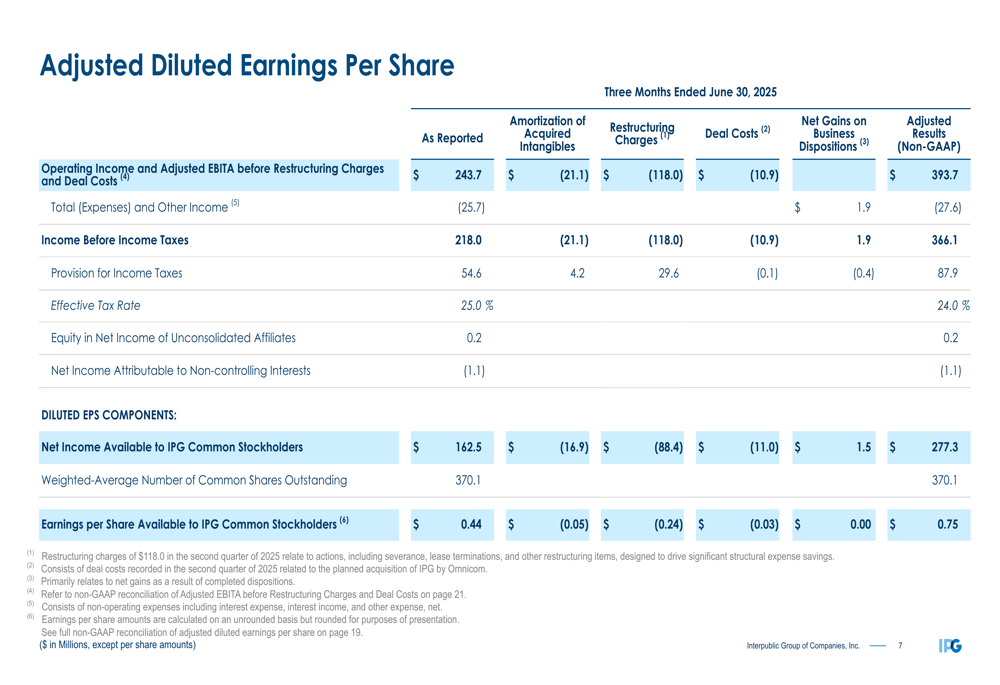

Despite revenue challenges, IPG achieved an adjusted EBITA of $393.7 million before restructuring charges and deal costs, representing an 18.1% margin on revenue before billable expenses – a historic high for a second quarter. Net income was reported at $162.5 million, with diluted earnings per share of $0.44 as reported and $0.75 as adjusted.

The company continued its shareholder return program, repurchasing 4.0 million shares for $98.3 million during the quarter.

Regional Performance Analysis

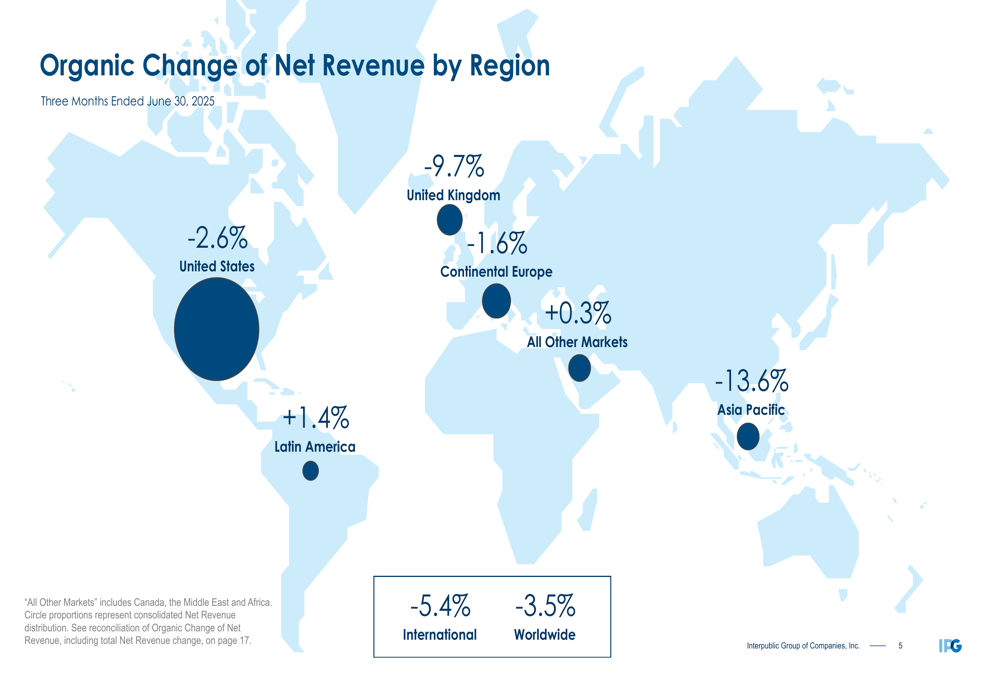

IPG’s performance varied significantly across regions, with some markets showing resilience while others faced substantial declines. The following geographical breakdown illustrates these regional disparities:

The United Kingdom and Asia Pacific regions experienced the most severe downturns, with organic revenue declines of 9.7% and 13.6%, respectively. Continental Europe fared somewhat better with a 1.6% decline, while Latin America and All Other Markets (including Canada, Middle East, and Africa) showed modest growth of 1.4% and 0.3%, respectively.

CEO Philippe Krakowsky addressed these challenges during the earnings call, noting: "We believe that the significant changes we’ve already made in the business, combined with a very strong strategic fit with the capabilities and geographies at Omnicom Group, means that our resulting offerings will be significantly strengthened."

Segment Performance

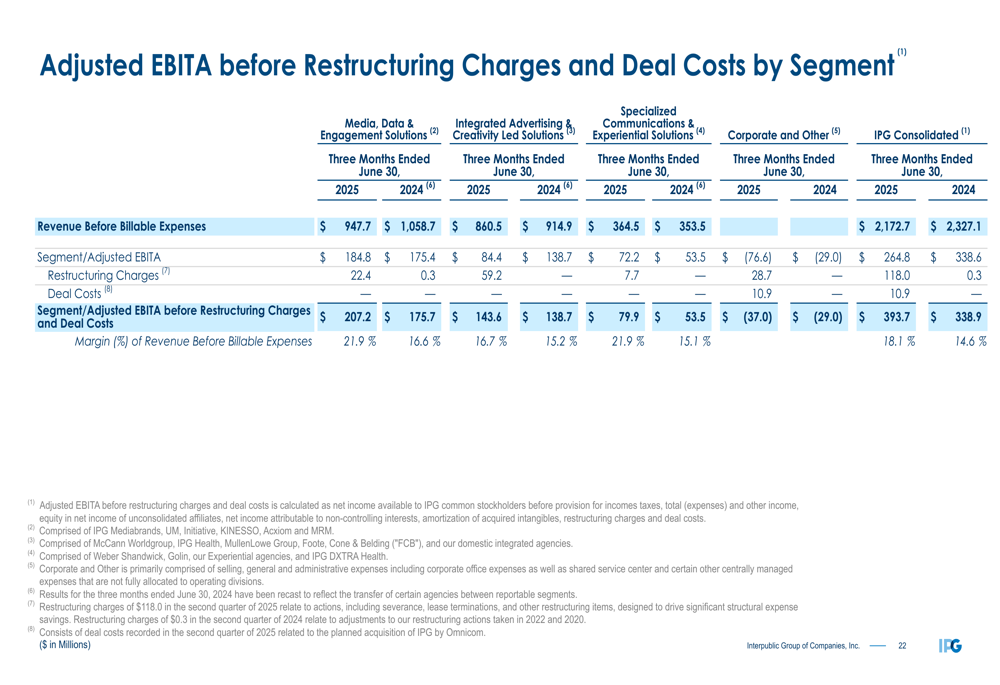

IPG’s business segments showed varying degrees of resilience in the challenging environment. The company’s Specialized Communications & Experiential Solutions segment was the only one to achieve positive organic growth at 2.3%, while the other segments experienced declines.

The following breakdown shows the adjusted EBITA performance by segment:

Media, Data & Engagement Solutions, the company’s largest segment with $947.7 million in quarterly revenue, delivered an 18.1% adjusted EBITA margin despite a 3.1% organic revenue decline. Integrated Advertising & Creativity Led Solutions faced the steepest decline at 6.3%, with margins of 9.8%. Specialized Communications & Experiential Solutions achieved the highest margin at 19.8%, benefiting from its positive organic growth.

Restructuring and Margin Improvement

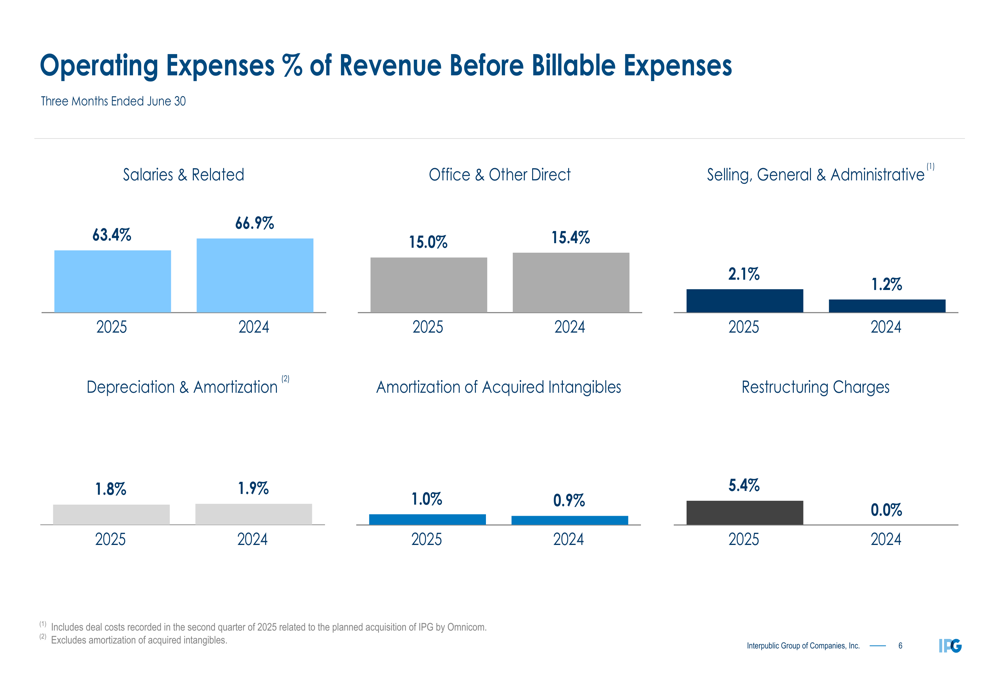

A key element of IPG’s Q2 results was the significant restructuring underway, with charges representing 5.4% of revenue compared to 0.0% in the same period last year. These efforts are part of a broader transformation that includes a 6% organic reduction in headcount.

The company’s focus on cost management is evident in the improvement of salaries and related expenses, which decreased to 63.4% of revenue before billable expenses, compared to 66.9% in Q2 2024:

The reconciliation of adjusted earnings per share provides further insight into the impact of restructuring and other one-time costs:

The company’s adjusted diluted EPS of $0.75 excludes $0.31 in charges related to restructuring, amortization of acquired intangibles, and deal costs associated with the pending Omnicom acquisition.

Balance Sheet and Liquidity

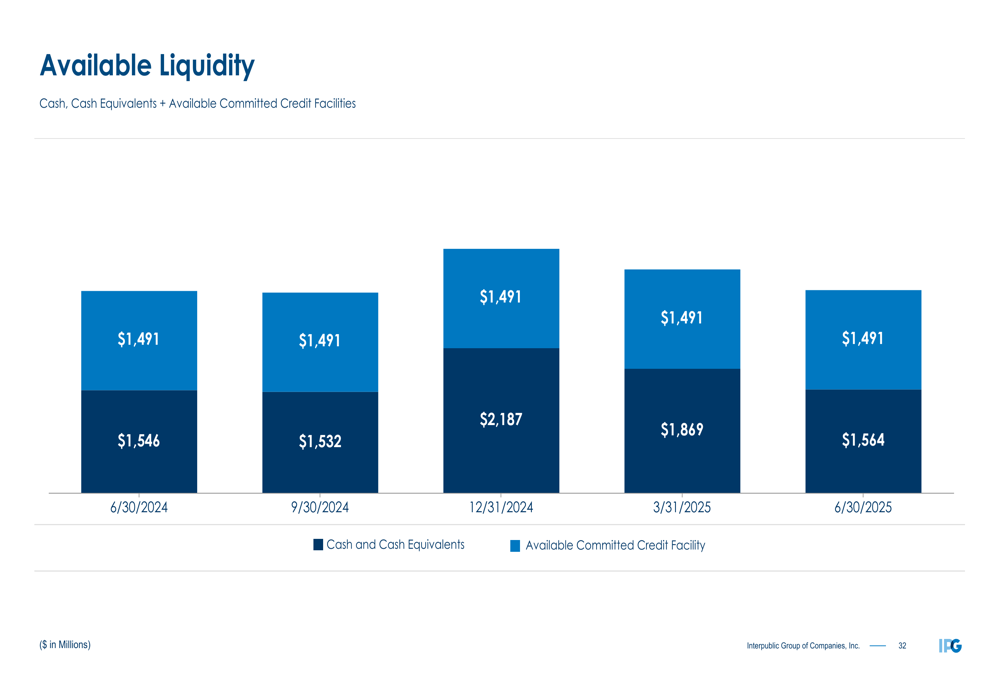

Despite the challenging revenue environment, IPG maintained a strong financial position with $1.56 billion in cash and total available liquidity of $3.06 billion as of June 30, 2025:

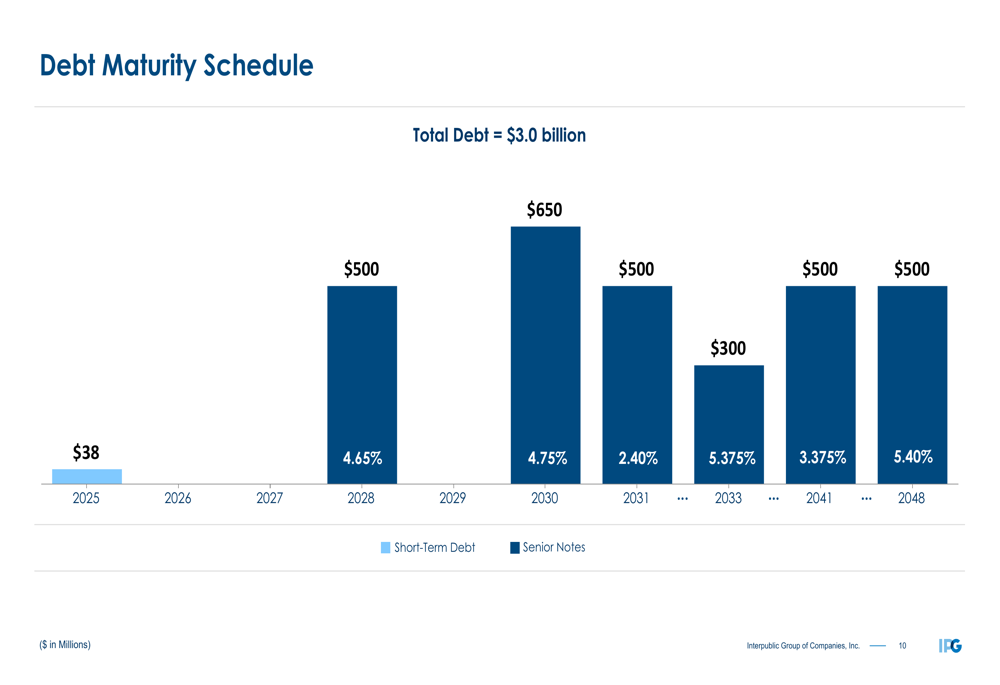

The company’s debt maturity schedule shows a well-structured long-term debt profile, with only $38 million due in 2025 and the next major maturity not until 2028:

IPG’s leverage ratio stood at 1.90x, well below the credit facility covenant maximum of 3.50x, indicating significant financial flexibility.

Forward-Looking Statements

Looking ahead, IPG projects a full-year organic net revenue decline of 1% to 2%, suggesting some improvement in the second half of 2025. The company expects Q3 and Q4 performance to be relatively similar, with adjusted EBITA margin remaining significantly above 16.6%.

The restructuring charges for the full year have been increased to $375-400 million, reflecting the company’s continued focus on operational efficiency ahead of the Omnicom merger.

Technology integration remains a strategic priority, with the launch of the Interact AI platform processing over 1 million prompts. Krakowsky highlighted this initiative during the earnings call, stating: "Interact is equipping them with the tools to enhance efficiencies, but also to deepen insights and unlock new ways to deliver more innovative and effective solutions for our clients."

While IPG faces ongoing revenue challenges, particularly in key international markets, its focus on margin improvement, technological advancement, and strategic positioning ahead of the Omnicom merger suggests a transformation aimed at long-term competitive strength in the evolving marketing services landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.