Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

Just Eat Takeaway.com ( AMS (VIE:AMS2):TKWY) presented its H1 2025 results on July 30, 2025, showing modest growth in its core markets but flat overall performance as the food delivery giant continues to navigate a challenging market environment. The company’s stock is currently trading near €20.00, close to its 52-week high of €20.16, reflecting continued investor confidence despite the mixed results.

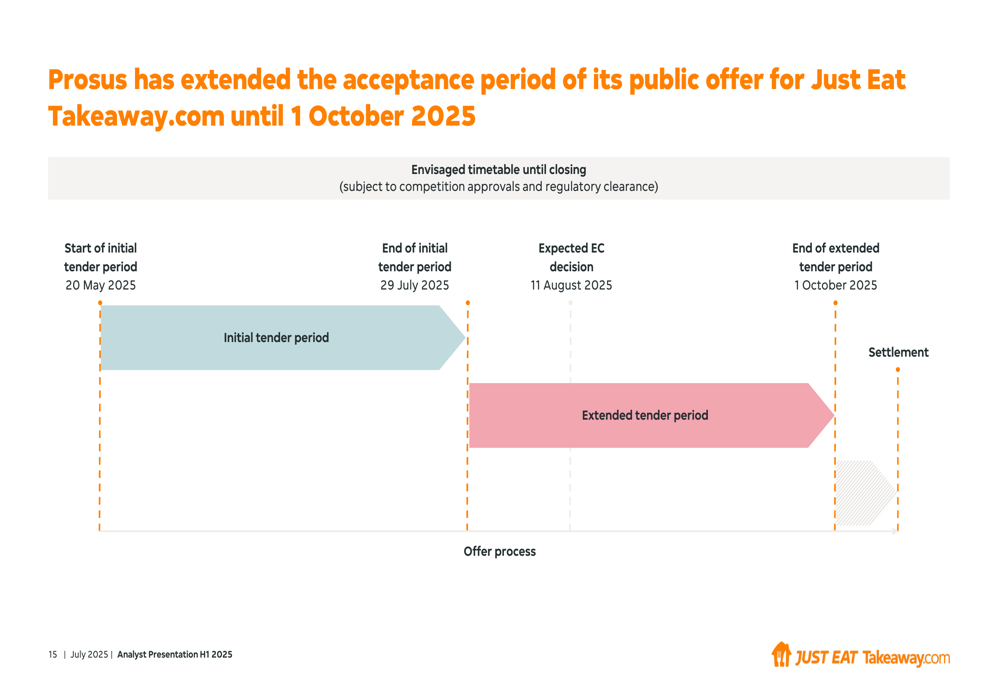

The presentation comes amid an ongoing takeover bid by Prosus (OTC:PROSF), which has extended its offer period until October 1, 2025, adding a layer of strategic uncertainty to the company’s operations.

H1 2025 Performance Highlights

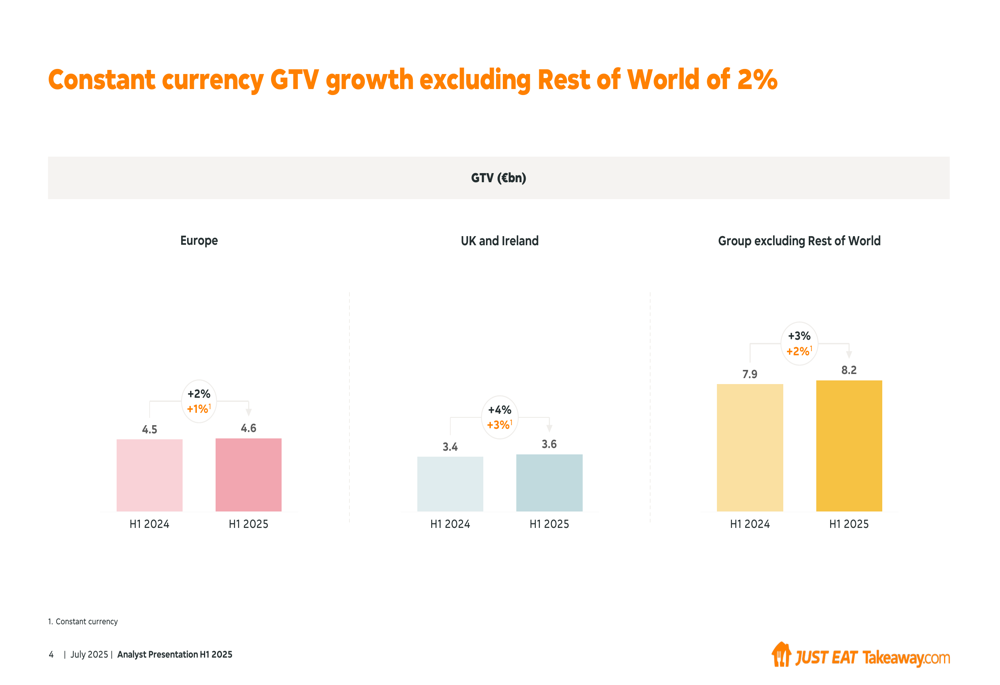

Just Eat Takeaway reported constant currency Gross Transaction (JO:NTUJ) Value (GTV) growth of 2% in its core markets, excluding the Rest of World segment. The company’s European operations grew 2% to €4.6 billion, while the UK and Ireland segment showed stronger performance with 4% growth to €3.6 billion.

As shown in the following chart of regional GTV performance:

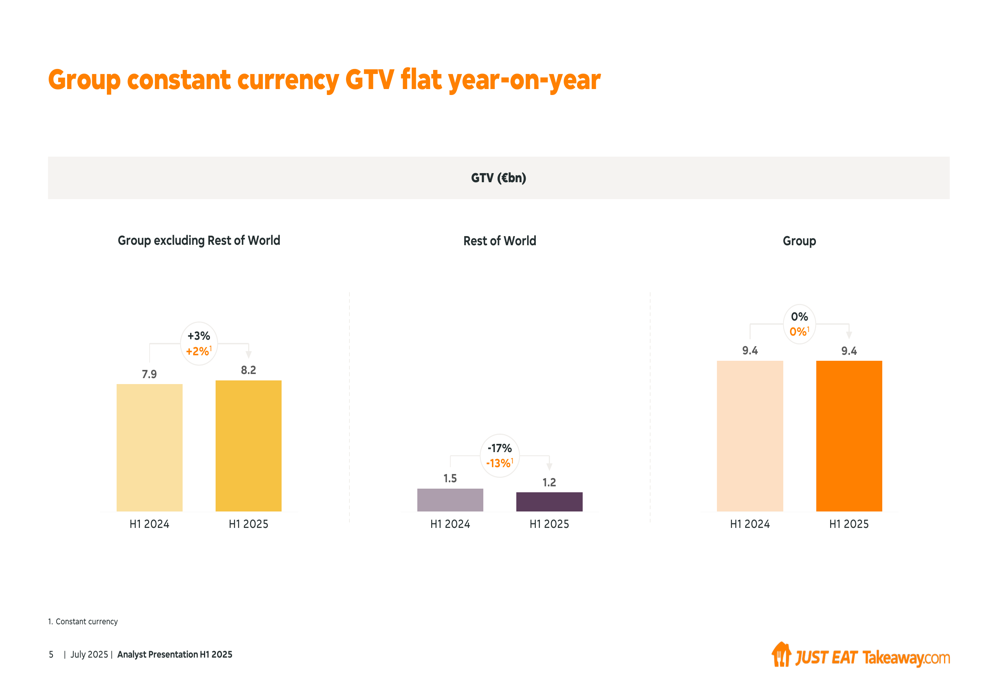

However, when including the Rest of World segment, which declined 17% to €1.2 billion, the group’s overall GTV remained flat year-on-year at €9.4 billion.

As illustrated in this comprehensive GTV breakdown:

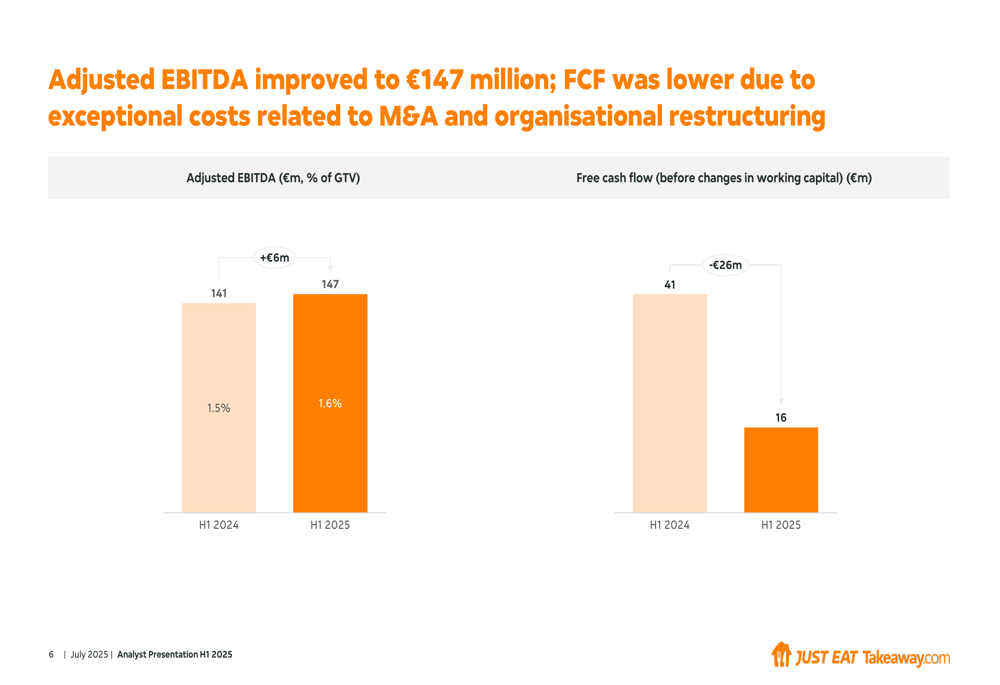

Despite the flat GTV, Just Eat Takeaway improved its profitability metrics, with adjusted EBITDA increasing to €147 million (1.6% of GTV) from €141 million (1.5% of GTV) in H1 2024. This improvement came despite ongoing investments in delivery network expansion and increased marketing efforts.

The company’s profitability and cash flow performance is summarized in this chart:

Detailed Financial Analysis

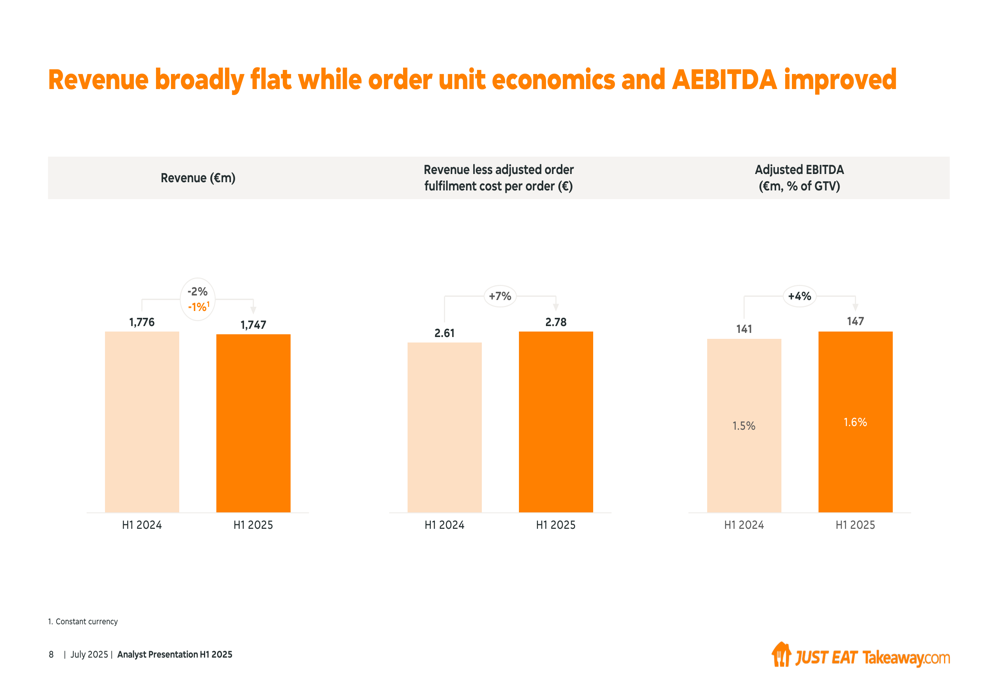

Revenue decreased slightly by 2% to €1,747 million compared to H1 2024, but the company improved its unit economics, with revenue less adjusted order fulfillment cost per order increasing by 7% to €2.78. This improvement in unit economics helped drive the overall EBITDA growth despite the revenue decline.

The following chart illustrates these key financial metrics:

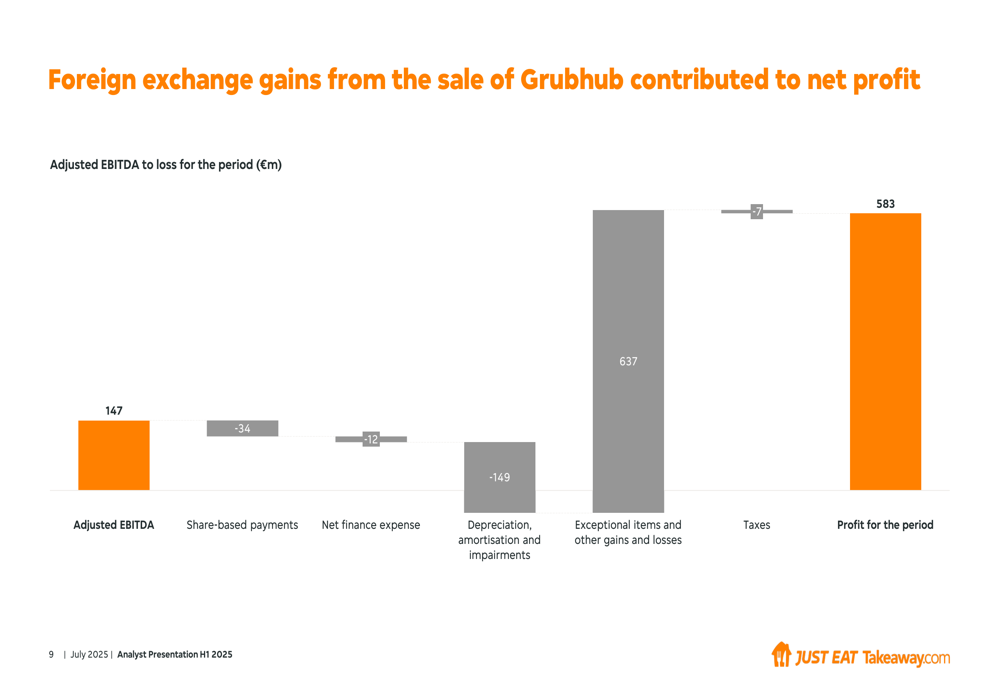

Just Eat Takeaway reported a significant profit of €583 million for the period, largely driven by exceptional items and other gains and losses totaling €637 million. This substantial boost to the bottom line offset the impact of ongoing depreciation, amortization, and impairments of €149 million.

The bridge from adjusted EBITDA to profit is shown in this waterfall chart:

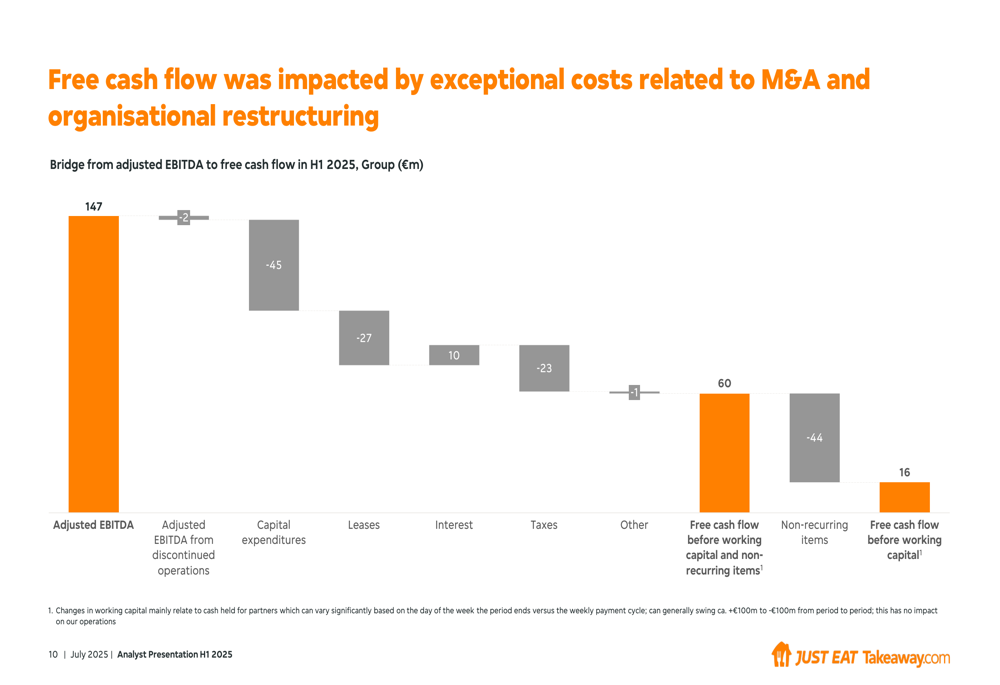

Free cash flow before working capital decreased to €16 million from €41 million in H1 2024, primarily due to non-recurring items related to M&A activities and organizational restructuring, which had a €44 million negative impact.

The components of free cash flow are detailed in this bridge:

The company maintained a strong cash position of €1,294 million at the end of H1 2025, only slightly down from €1,301 million at the end of 2024, despite a €52 million share buyback program.

Strategic Initiatives & Prosus Offer

CEO Jitse Groen emphasized the company’s strategic investments, stating: "We see good progress in the expansion of our delivery network and have ramped up our marketing efforts, which we believe are necessary investments to support future growth. Despite these additional investments, Just Eat Takeaway.com further improved its adjusted EBITDA to €147 million in the first six months of 2025."

A significant development for Just Eat Takeaway is the ongoing takeover bid by Prosus. The initial tender period began on May 20, 2025, and was set to end on July 29, 2025. However, Prosus has extended the acceptance period until October 1, 2025, with a European Commission decision expected by August 11, 2025.

The timeline for the Prosus offer is illustrated here:

Forward Guidance

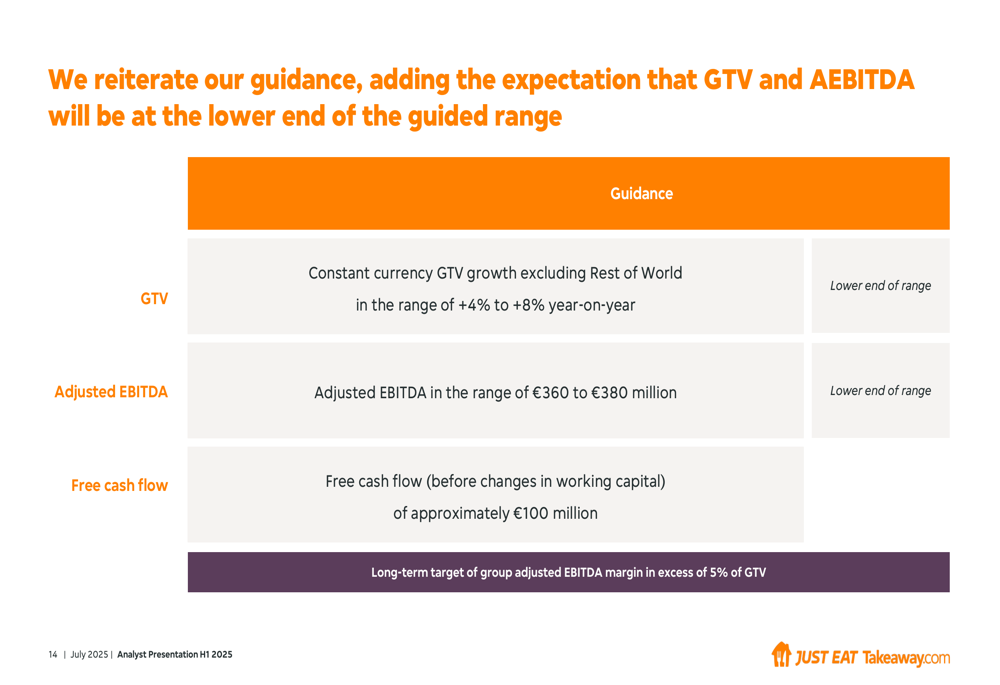

Just Eat Takeaway reiterated its guidance for 2025 but indicated that results are expected to be at the lower end of the guided ranges. The company forecasts:

- Constant currency GTV growth excluding Rest of World in the range of 4-8% year-on-year

- Adjusted EBITDA between €360-380 million

- Free cash flow before changes in working capital of approximately €100 million

The company also maintained its long-term target of achieving a group adjusted EBITDA margin exceeding 5% of GTV.

The full guidance is summarized in this slide:

Conclusion

Just Eat Takeaway’s H1 2025 results present a mixed picture of the company’s performance. While core markets show modest growth and profitability continues to improve, the overall flat GTV and declining Rest of World segment highlight ongoing challenges in certain markets.

The company’s focus on improving unit economics appears to be yielding results, with adjusted EBITDA continuing to grow despite increased investments in delivery network expansion and marketing. However, the lowered expectations for full-year guidance suggest some caution about the pace of growth in the second half of the year.

The pending Prosus offer adds another dimension to Just Eat Takeaway’s story, with the extended acceptance period until October potentially influencing strategic decisions in the coming months. Investors will be watching closely for the European Commission’s decision in August and any further developments in this potential acquisition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.