Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

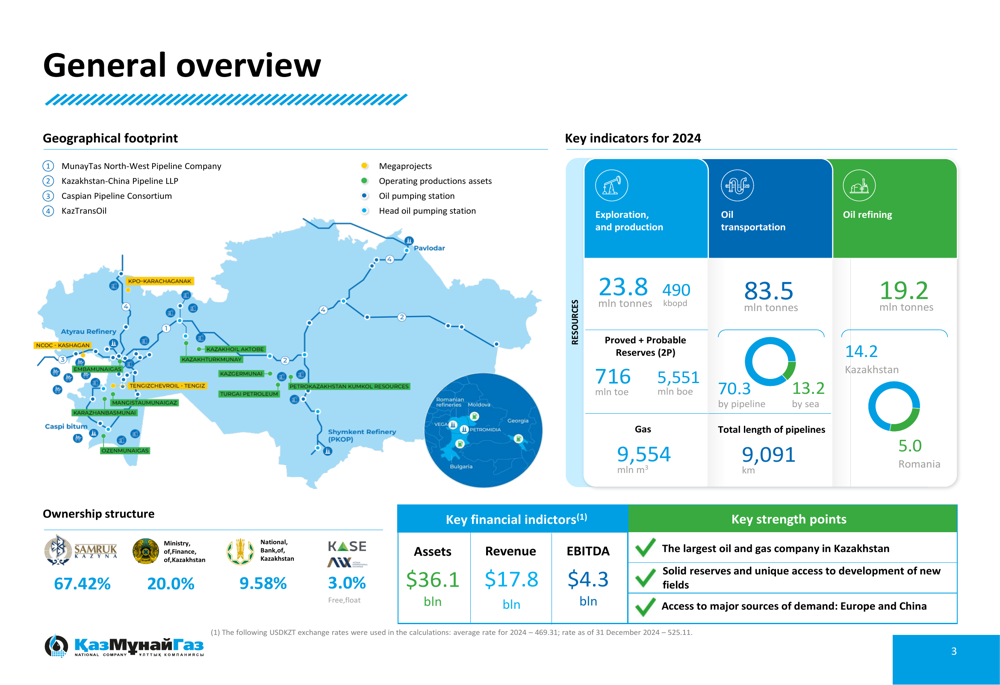

Kazakhstan’s national oil company JSC NC KazMunayGas (KMGZ) presented its fiscal year 2024 operational and financial results in March 2025, revealing a strategic focus on strengthening its balance sheet while navigating a relatively stable oil price environment. As the largest oil and gas company in Kazakhstan, KMG operates across the full hydrocarbon value chain with assets in exploration, production, transportation, refining, and marketing.

The company operated in a macroeconomic environment where Brent crude averaged $80.8 per barrel in 2024, while Kazakhstan’s economy showed resilience with 4.8% GDP growth and inflation moderating to 8.6% from 9.8% in the previous year.

Executive Summary

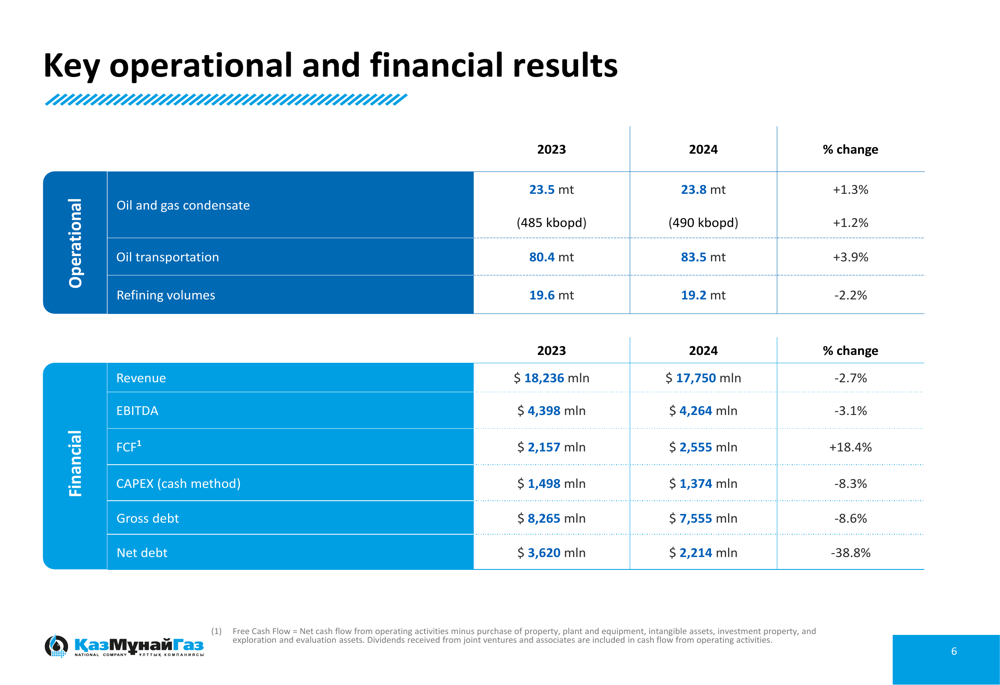

KMG’s FY2024 results demonstrated mixed performance with modest revenue decline offset by improved free cash flow and significant debt reduction. The company reported revenue of $17.8 billion, down 2.7% from $18.2 billion in 2023, while EBITDA decreased slightly to $4.3 billion from $4.4 billion.

Despite these declines, KMG achieved notable improvements in its financial position, with free cash flow increasing 18.5% to $2.6 billion and net debt decreasing by 38.8% to $2.2 billion. The company maintained its dividend payments at 300 billion tenge, representing approximately 25% of free cash flow.

As shown in the following comprehensive performance summary:

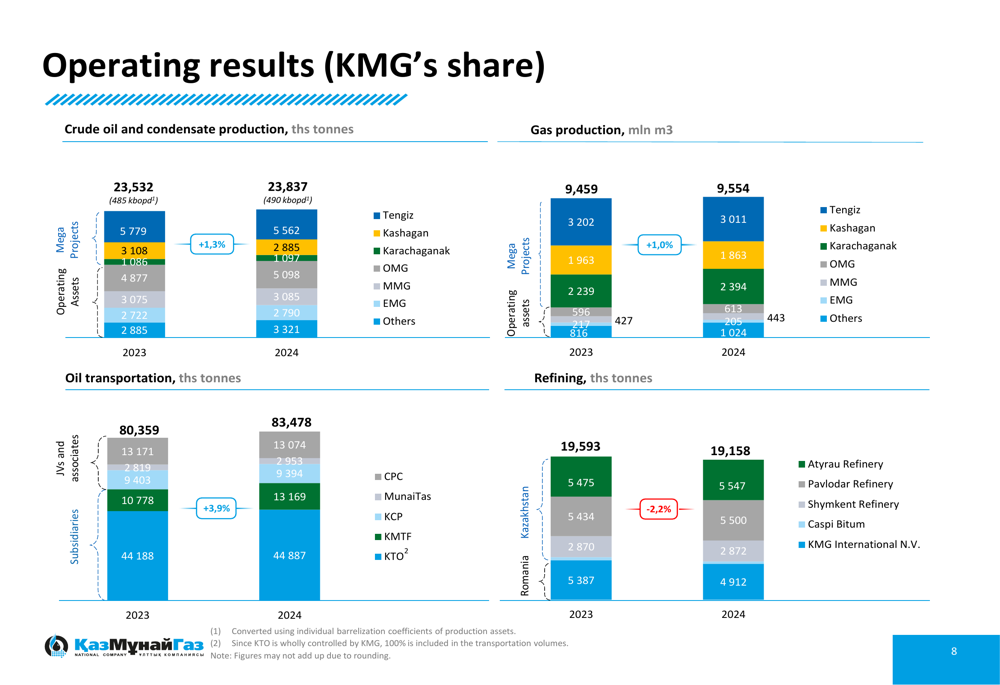

Operationally, KMG increased its oil and gas condensate production to 23.8 million tonnes (490,000 barrels per day), up from 23.5 million tonnes in 2023. Oil transportation volumes also grew to 83.5 million tonnes from 80.4 million tonnes, while refining volumes decreased slightly to 19.2 million tonnes from 19.6 million tonnes.

Detailed Financial Analysis

KMG’s financial performance in 2024 reflected its strategic priorities of strengthening cash position and reducing debt. While revenue and EBITDA showed modest declines, the company’s focus on operational efficiency and capital discipline yielded positive results in other key metrics.

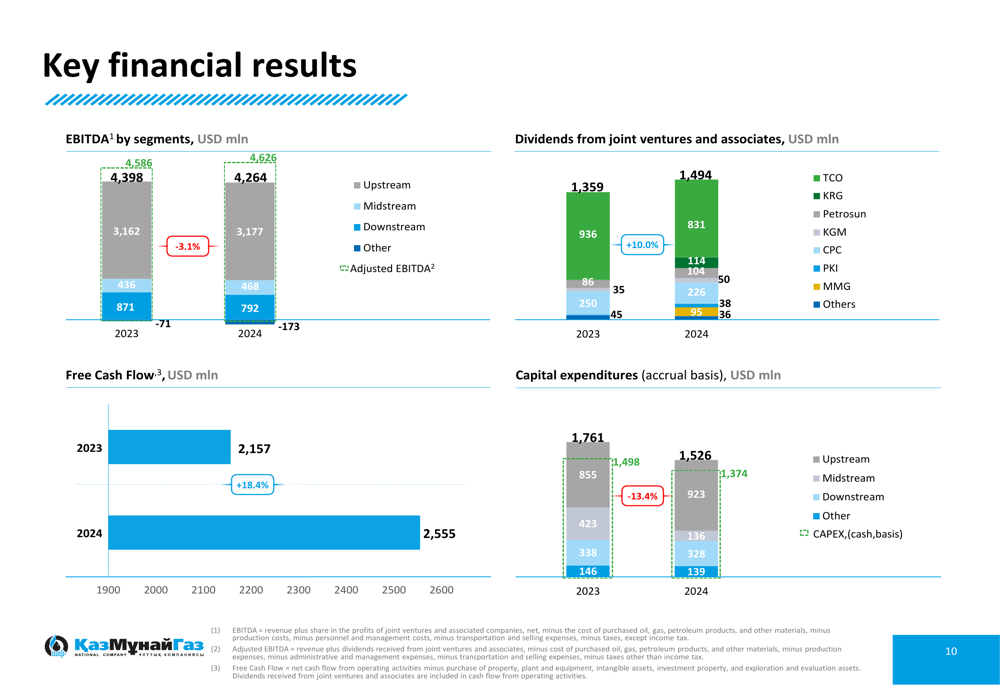

The company’s EBITDA breakdown by segment reveals that upstream operations remained the primary contributor at $3.2 billion, followed by downstream at $792 million and midstream at $468 million. Dividends from joint ventures and associates increased to $1.5 billion from $1.4 billion in 2023.

The following chart illustrates KMG’s EBITDA composition and capital expenditure:

Free cash flow generation was a particular highlight, increasing to $2.6 billion from $2.2 billion in 2023. This improvement was driven by strong operational cash flow and disciplined capital expenditure, which decreased to $1.4 billion from $1.5 billion.

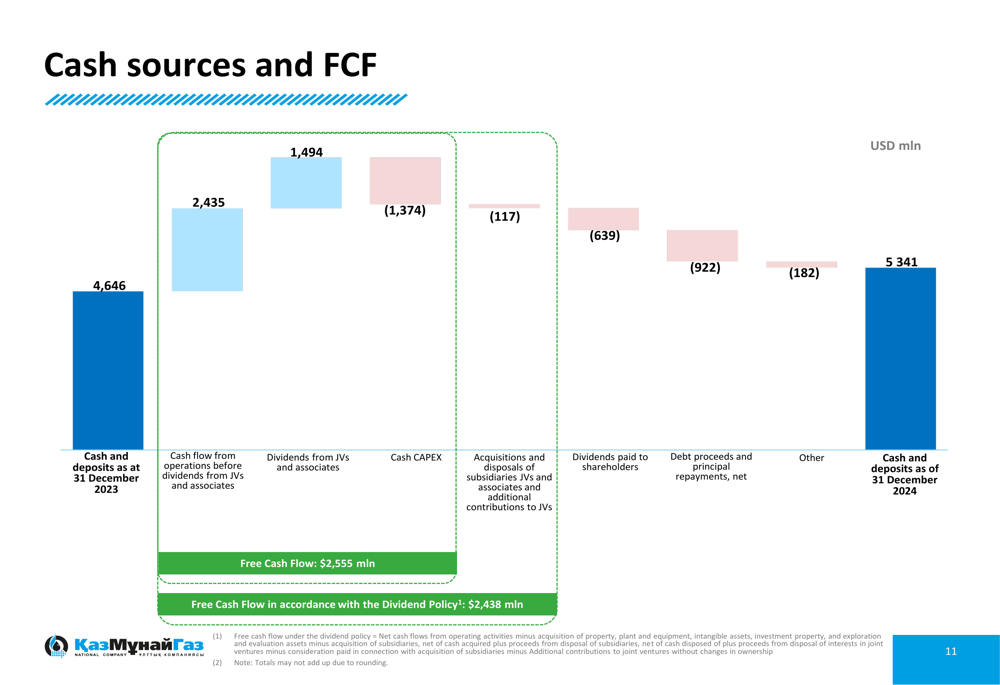

The company’s cash flow waterfall demonstrates how KMG strengthened its cash position throughout the year:

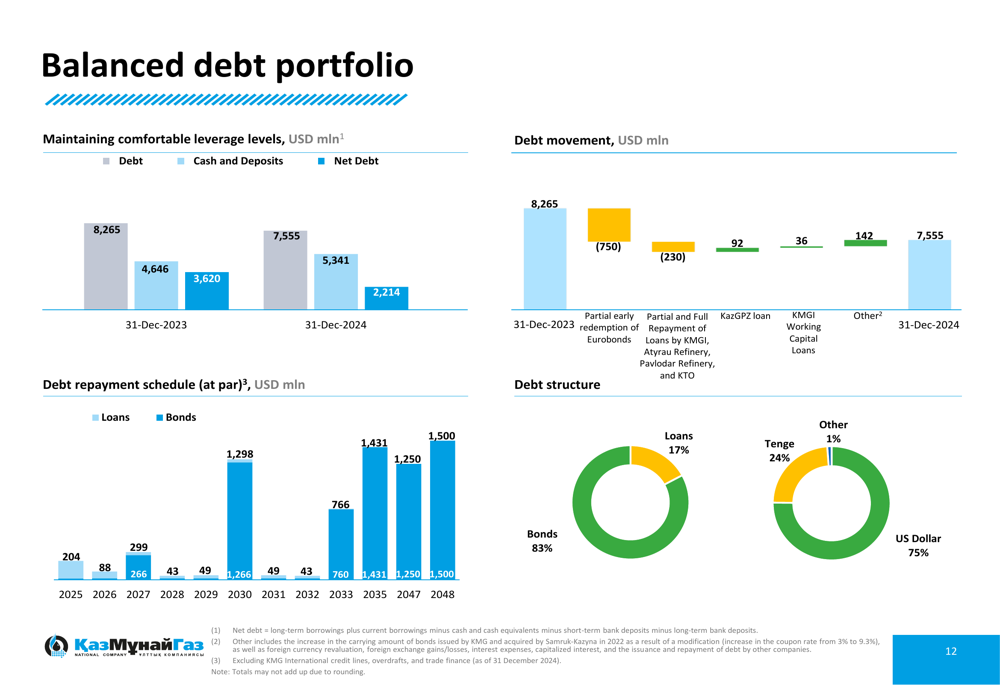

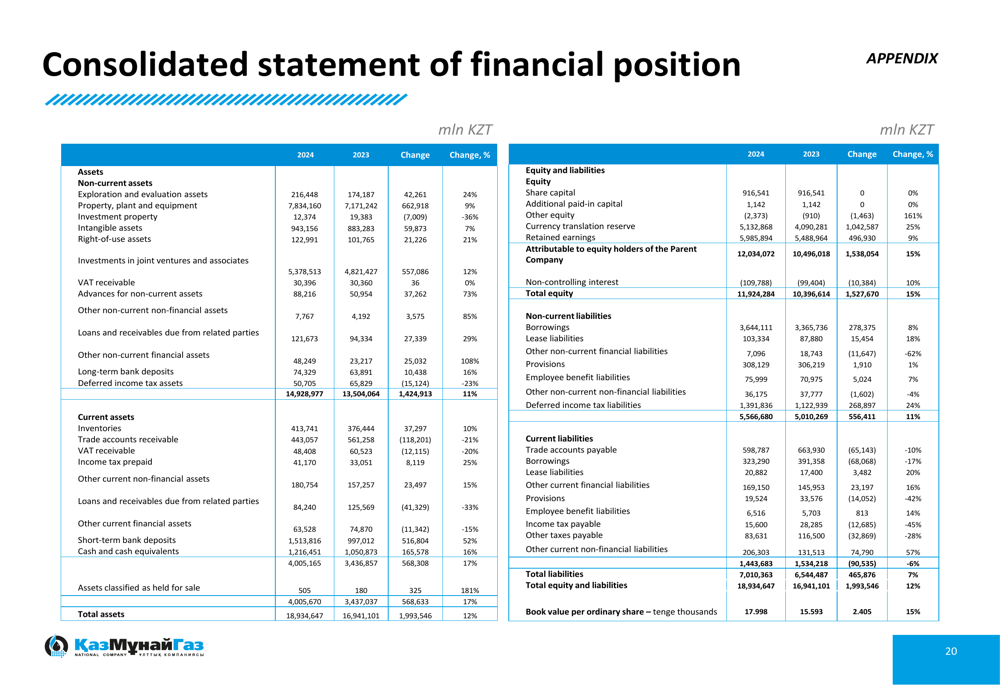

KMG’s balance sheet showed significant improvement, with gross debt decreasing to $7.6 billion from $8.3 billion and net debt falling to $2.2 billion from $3.6 billion. Cash and deposits increased to $5.3 billion from $4.6 billion, providing the company with substantial liquidity.

The debt portfolio remains well-balanced, with 83% in bonds and 75% denominated in USD:

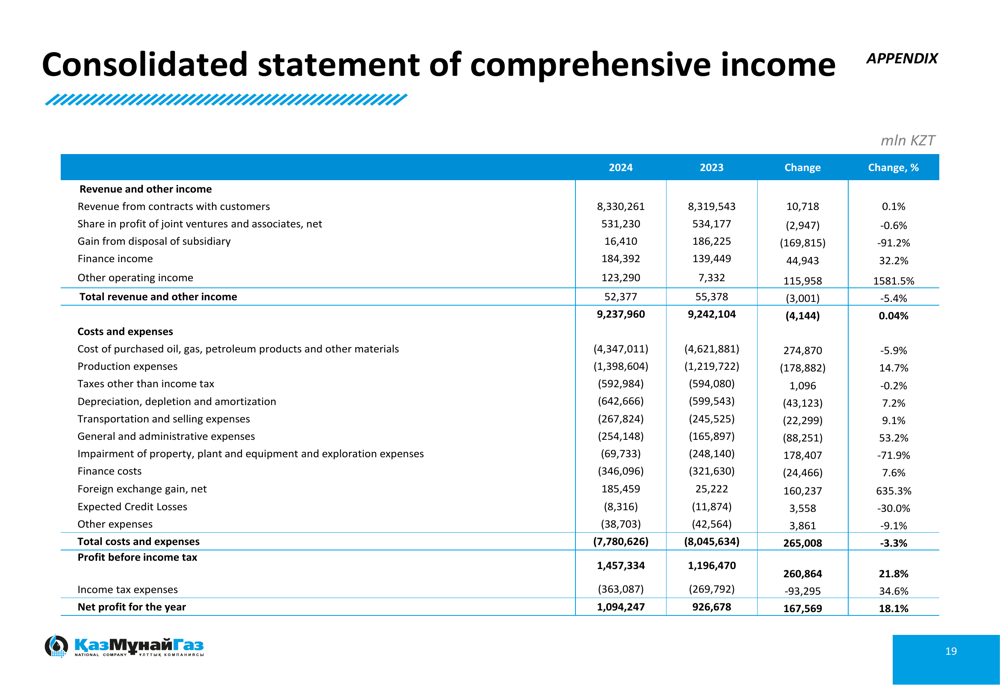

The consolidated financial statements provide a comprehensive view of KMG’s financial position:

Operational Performance

KMG’s operational performance in 2024 showed modest growth in production and transportation volumes, while refining volumes decreased slightly. The company’s diversified asset portfolio helped maintain stable overall performance despite variations across individual assets.

Oil and gas condensate production increased by 1.3% to 23.8 million tonnes, with growth primarily coming from OMG, EMG, and other assets offsetting declines at the Tengiz and Kashagan megaprojects. Gas production showed similar patterns, with overall volumes increasing despite reductions at major fields.

The detailed breakdown of operational results by asset provides insight into the performance of KMG’s diverse portfolio:

The company’s three megaprojects—Tengiz, Kashagan, and Karachaganak—showed mixed performance. Tengiz and Kashagan experienced production declines, while Karachaganak saw slight increases in both oil and gas production. These projects remain critical to KMG’s overall performance, contributing significantly to production volumes and financial results.

Oil transportation increased by 3.9% to 83.5 million tonnes, reflecting higher volumes across KMG’s pipeline and maritime transportation assets. This growth demonstrates the strategic importance of KMG’s midstream operations in connecting Kazakhstan’s oil production to international markets.

Strategic Initiatives

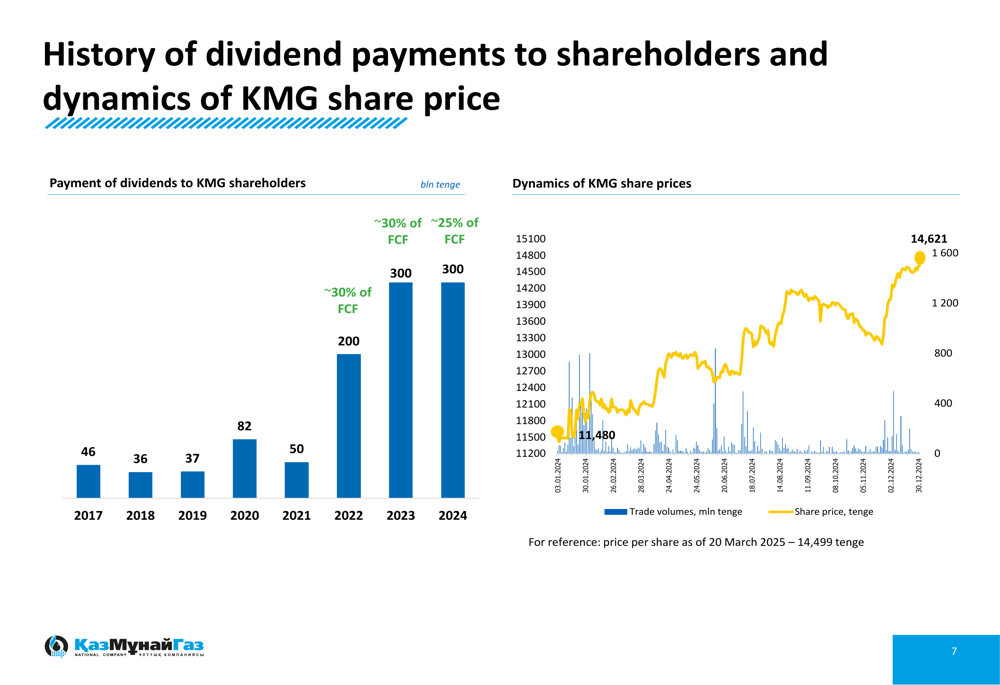

KMG’s strategic focus in 2024 centered on debt reduction, cash preservation, and maintaining shareholder returns. The company made significant progress in strengthening its balance sheet, with a $750 million partial early redemption of Eurobonds and additional loan repayments contributing to the overall debt reduction.

The company maintained its dividend payments at 300 billion tenge, though as a percentage of free cash flow, dividends decreased from approximately 30% to 25%. This approach balances shareholder returns with financial prudence.

The dividend history and share price dynamics illustrate KMG’s commitment to shareholder value:

KMG’s geographical footprint and diversified asset portfolio position it well to serve major markets in Europe and China:

The company continued to advance key operational initiatives in 2024, including drilling operations at various locations, FEED activities at the Kalamkas-Sea project, and construction on the Polyethylene Project. KMG also made progress on its environmental, social, and governance (ESG) agenda, including the approval of its Low-Carbon Development Program and the construction of solar and gas-fired power plants.

Forward-Looking Statements

Looking ahead, KMG appears well-positioned to navigate the evolving energy landscape with its strengthened balance sheet, diversified asset portfolio, and strategic access to key markets. The company’s credit ratings from Moody’s (Baa1 stable), S&P Global Ratings (BBB+), and Fitch Ratings (BBB+) reflect its solid financial position and stable outlook.

Challenges remain, including potential oil price volatility, geopolitical uncertainties affecting transportation routes, and the need to balance traditional oil and gas operations with growing expectations for low-carbon initiatives. However, KMG’s reduced debt levels and strong cash position provide flexibility to address these challenges while pursuing growth opportunities.

The company’s strategic focus on operational efficiency, capital discipline, and balance sheet strength suggests a continued emphasis on financial resilience rather than aggressive expansion in the near term. This approach appears prudent given the uncertain global economic outlook and ongoing energy transition pressures facing the oil and gas industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.