US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

KBC Group (EBR:KBC) released its Q2 2025 company presentation on August 7, 2025, revealing a strong financial performance with a net profit of €1,018 million, nearly doubling the €546 million reported in Q1 2025. The Belgian bank-insurer demonstrated resilience in a decreasing policy rate environment, leveraging its geographically diversified business model across mature markets (Belgium, Czech Republic) and growth markets (Slovakia, Hungary, Bulgaria).

The presentation highlighted KBC’s continued transformation into a digital-first, data-driven and AI-led integrated bank-insurer, with its digital assistant Kate now reaching 5.7 million users. The company’s shares closed at €74.74, showing a minor decrease of 0.21% on the day of the presentation.

Quarterly Performance Highlights

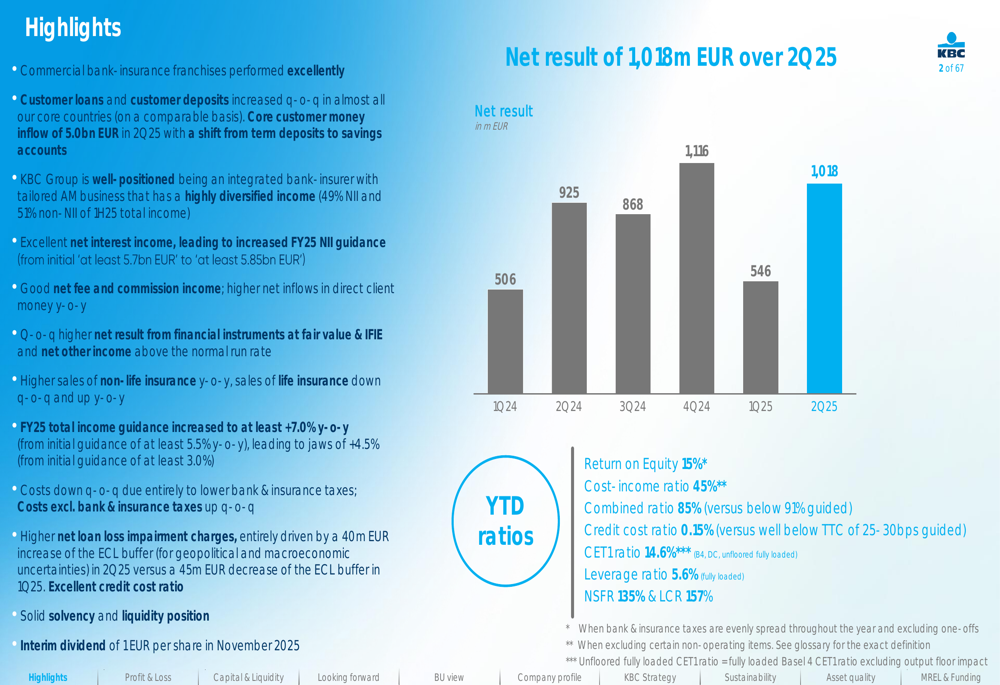

KBC Group reported a substantial improvement in quarterly performance, with net profit rising to €1,018 million in Q2 2025 compared to €546 million in Q1 2025 and €925 million in Q2 2024. This performance was driven by excellent commercial bank-insurance franchises, strong net interest income, and higher sales of non-life insurance products.

As shown in the following chart of quarterly net results, KBC has maintained a generally positive trend over the past six quarters, with Q2 2025 representing the second-highest quarterly result in this period:

Key performance metrics for the first half of 2025 include a return on equity of 15%, a cost-income ratio of 45%, and a combined ratio of 85% (versus the guided figure of below 91%). The credit cost ratio stood at 0.15%, well below the through-the-cycle guidance of 25-30 basis points, while the CET1 ratio remained solid at 14.6%.

Detailed Financial Analysis

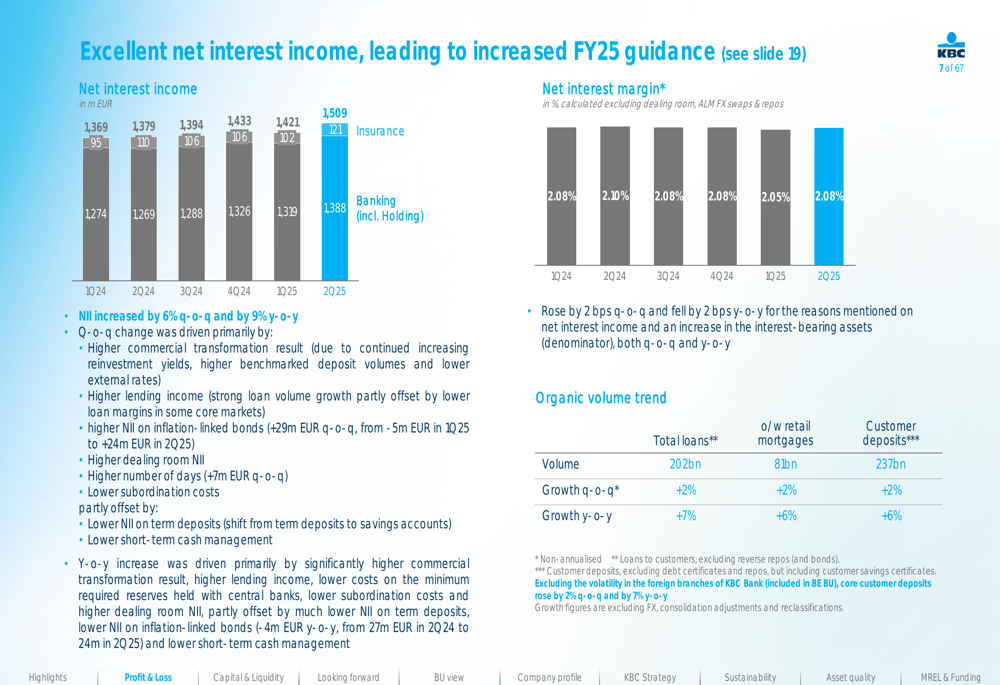

Net interest income (NII) showed impressive growth, increasing by 6% quarter-on-quarter and 9% year-on-year to €1,509 million in Q2 2025. This growth was attributed to higher commercial transformation results, increased lending income, higher NII on inflation-linked bonds, and higher dealing room NII, partially offset by lower NII on term deposits.

The following chart illustrates the consistent growth in net interest income over the past six quarters:

Organic volume growth remained strong, with total loans increasing by 7% year-on-year to €202 billion and customer deposits growing by 6% to €237 billion. This represents a significant acceleration from the 2.43% loan growth reported in Q1 2025, as mentioned in the company’s previous earnings report.

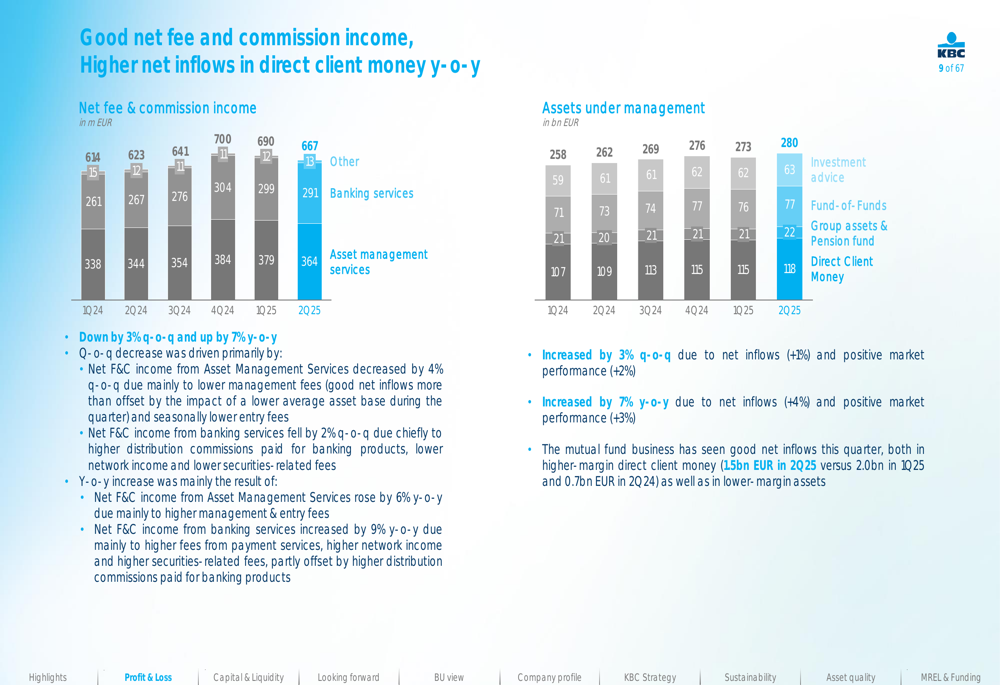

Net fee and commission income reached €364 million in Q2 2025, showing a slight decrease from €379 million in Q1 2025 but an increase from €344 million in Q2 2024. Assets under management continued to grow, reaching €118 billion for direct client money, up from €115 billion in the previous quarter.

The following chart shows the evolution of net fee and commission income and assets under management:

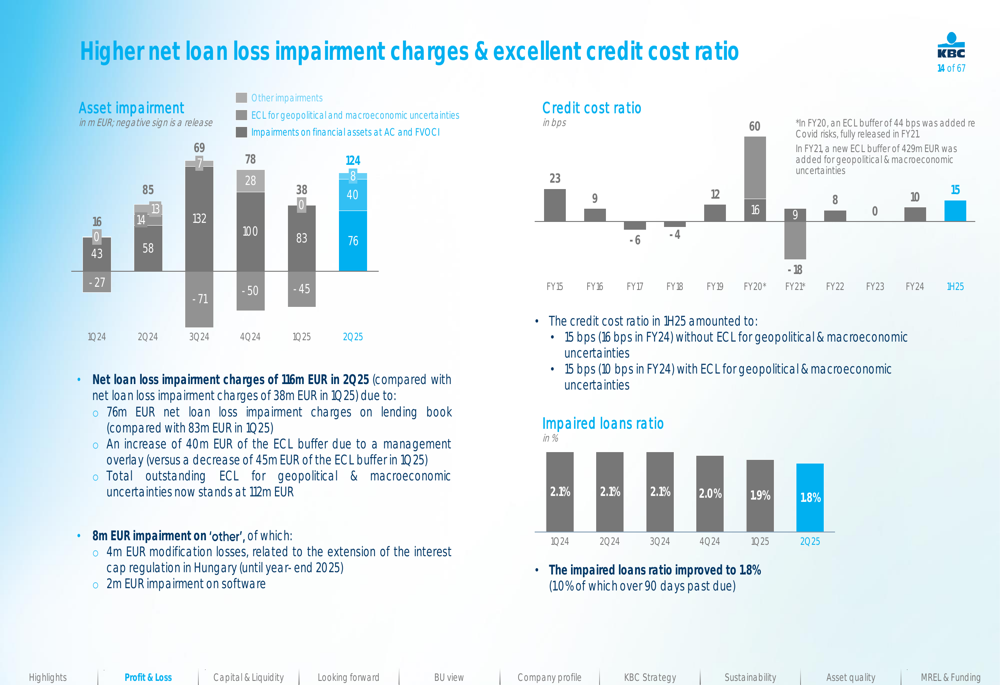

Asset quality metrics showed some deterioration, with net loan loss impairment charges increasing to €116 million in Q2 2025 compared to €38 million in Q1 2025. This included a €40 million increase in the ECL buffer for geopolitical and macroeconomic uncertainties, bringing the total buffer to €112 million. The impaired loans ratio remained stable at 1.8%.

The following chart illustrates the evolution of asset impairments and credit cost ratio:

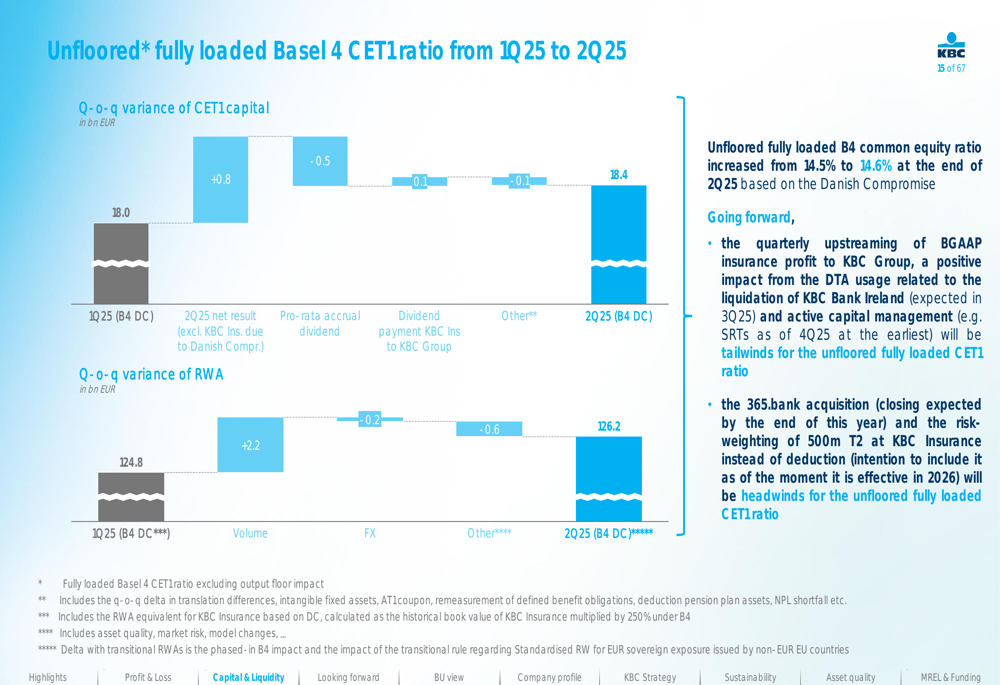

KBC’s capital position remained strong, with the unfloored fully loaded Basel 4 CET1 ratio increasing slightly to 14.6% at the end of Q2 2025, up from 14.5% in the previous quarter. This improvement was driven by the strong quarterly net result of €0.8 billion, partially offset by the pro-rata accrual of dividends.

The following chart shows the evolution of KBC’s CET1 capital and risk-weighted assets:

Strategic Initiatives

KBC continues to position itself as a reference for bank-insurance in its core markets, focusing on profitability, solvency, sustainability, and digitalization. The company’s integrated bank-insurance model contributed significantly to its results, with 18% of the €1,018 million Group net result originating from insurance activities.

The digital-first approach through Kate has gained significant traction, with 5.7 million users and an autonomy rate of 71% in both Belgium and the Czech Republic. This digital assistant has been recognized as the number one mobile banking app worldwide by Sia Partners.

In terms of sustainability, KBC ranks in the 3rd percentile of 254 diversified banks assessed by Sustainalytics, underscoring its commitment to responsible business practices.

The presentation also referenced integration costs for Raiffeisenbank Bulgaria, indicating ongoing efforts to consolidate its position in growth markets. This aligns with the company’s previous announcement regarding the acquisition of 365 Bank in Slovakia, which is expected to position KBC as a top player in that market with projected synergies of €75 million pre-tax by 2028.

Forward-Looking Statements

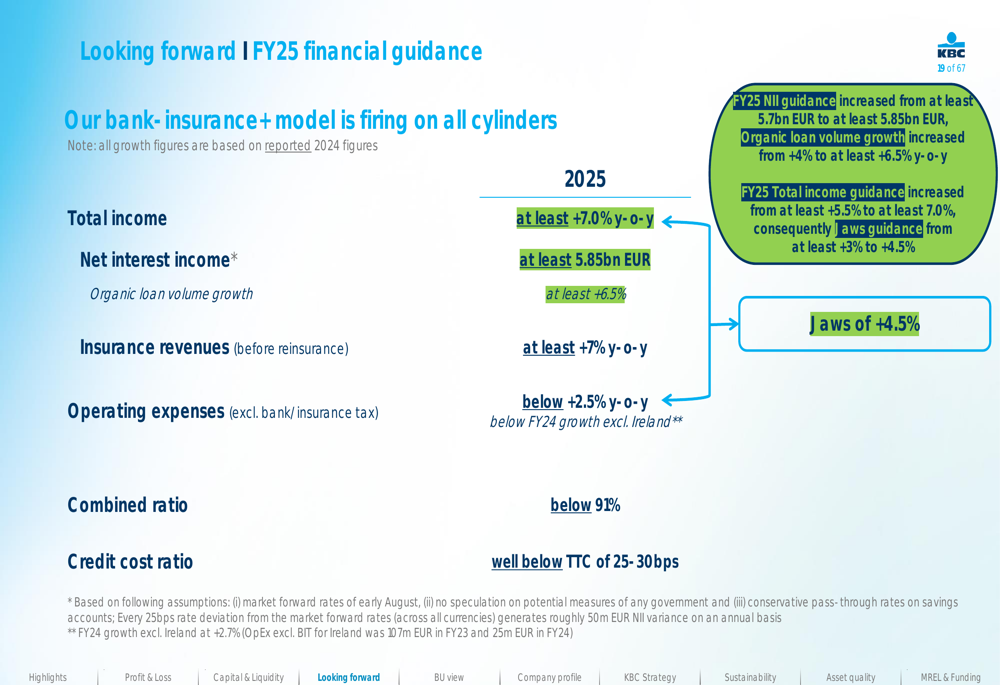

Based on its strong performance, KBC has raised its financial guidance for FY25. The company now expects total income growth of at least 7.0% year-on-year, up from its previous guidance. Net interest income is projected to reach at least €5.85 billion, while organic loan volume growth is expected to be at least 6.5%.

The following slide details the updated FY25 financial guidance:

For the longer term, KBC maintained its FY27 guidance, projecting a total income CAGR of at least 6% for 2024-2027, with net interest income growing at a CAGR of at least 5% even in a decreasing policy rate environment. Insurance revenues are expected to grow at a CAGR of at least 7% during the same period.

Operating expenses (excluding bank/insurance tax) are projected to grow at a CAGR below 3% for 2024-2027, resulting in positive jaws of at least 3%. The combined ratio is expected to remain below 91%, while the credit cost ratio is anticipated to stay well below the through-the-cycle level of 25-30 basis points.

KBC also announced an interim dividend of €1 per share to be paid in November 2025, reflecting confidence in its financial strength and commitment to shareholder returns.

In conclusion, KBC Group’s Q2 2025 presentation portrays a company with strong financial performance, solid growth in key business areas, and a clear strategic direction focused on digital transformation and geographic diversification. The raised guidance for FY25 suggests management’s confidence in maintaining this positive momentum despite the challenging macroeconomic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.