US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

Kelly Services, Inc. (NASDAQ:KELYA) released its second-quarter 2025 results on August 7, 2025, revealing a mixed performance characterized by acquisition-driven growth against a backdrop of organic revenue challenges. The staffing and workforce solutions provider reported a 4.2% increase in revenue, reaching $1.1 billion, primarily bolstered by its 2024 acquisition of Motion Recruitment Partners (MRP).

The company’s stock has shown signs of recovery in recent months after experiencing a significant decline over the past year. According to available data, Kelly Services shares closed at $12.25 on August 6, 2025, representing a modest 0.25% increase ahead of the earnings presentation.

Quarterly Performance Highlights

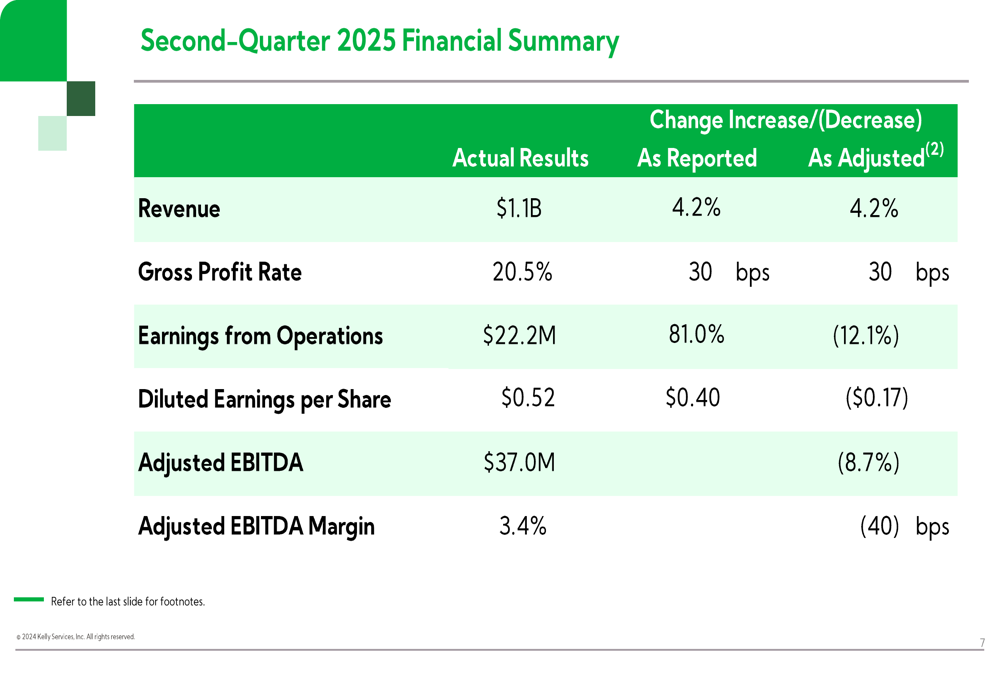

Kelly Services reported total revenue of $1.1 billion for Q2 2025, up 4.2% year-over-year on a reported basis. However, organic revenue declined by 3.3%, which included a 1.4% impact from reduced demand for US federal government contract workers. The company’s gross profit rate improved to 20.5%, up 30 basis points from the prior year.

As shown in the following financial summary:

Earnings from operations increased significantly by 81.0% as reported to $22.2 million, though adjusted earnings from operations decreased by 12.1%. Diluted earnings per share came in at $0.52 as reported, while adjusted EPS was $0.40, representing a year-over-year decline. Adjusted EBITDA fell 8.7% to $37.0 million, with adjusted EBITDA margin contracting 40 basis points to 3.4%.

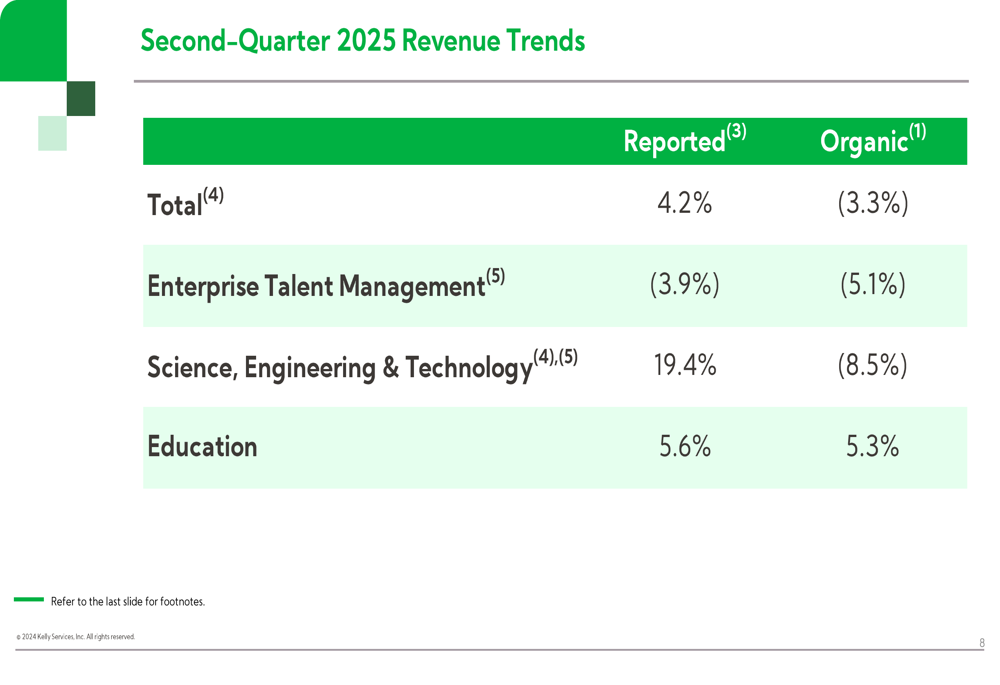

The revenue performance across segments showed divergent trends, with organic growth challenges in most areas:

Segment Analysis

Kelly Services’ performance varied significantly across its three main business segments. The Science, Engineering & Technology (SET) segment showed the strongest reported growth at 19.4%, primarily due to the MRP acquisition, though organic revenue declined by 8.5%. The Education segment demonstrated both reported and organic growth of 5.6% and 5.3% respectively, while Enterprise Talent Management (ETM) experienced declines in both reported (-3.9%) and organic (-5.1%) revenue.

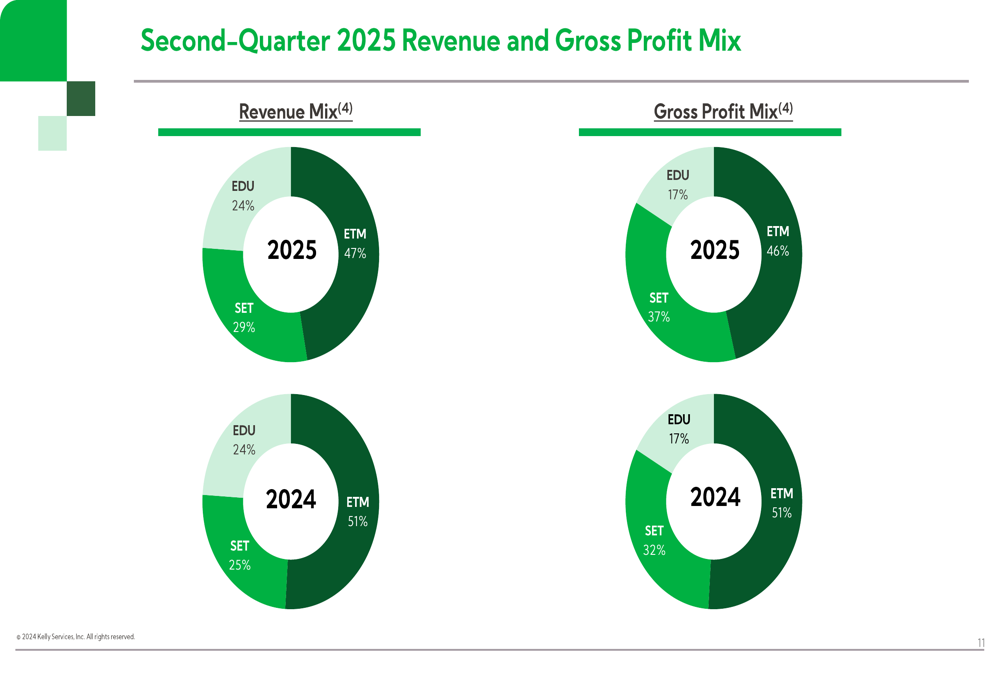

The company’s revenue and gross profit mix has evolved compared to the previous year, with SET gaining share in both metrics:

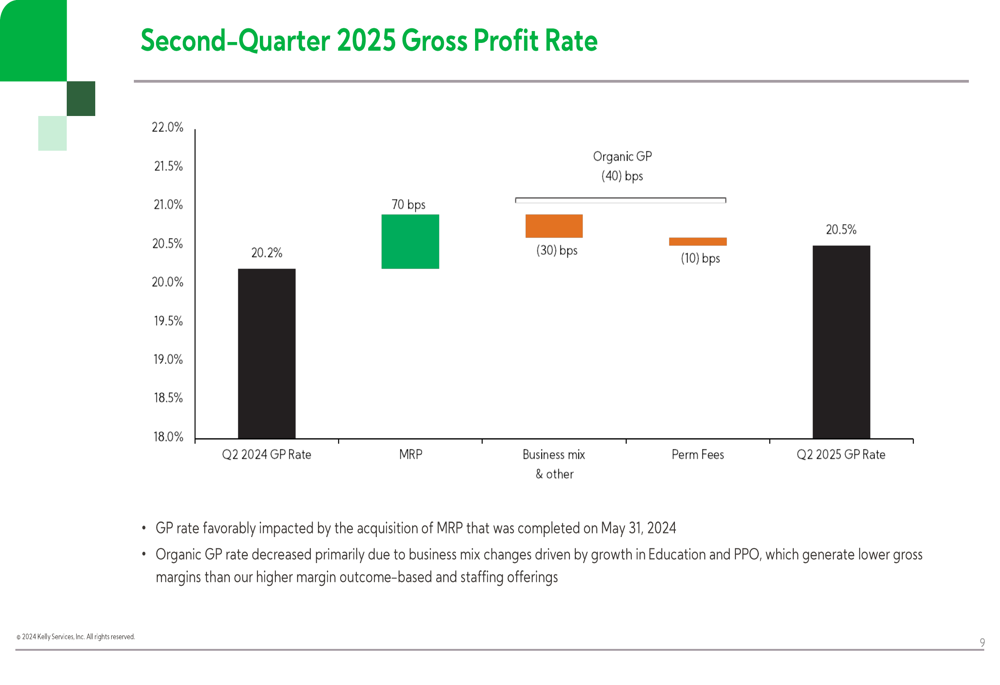

The gross profit rate improvement was primarily driven by the MRP acquisition, which contributed 70 basis points of improvement. However, this was partially offset by unfavorable business mix changes and lower permanent placement fees:

Financial Position and Liquidity

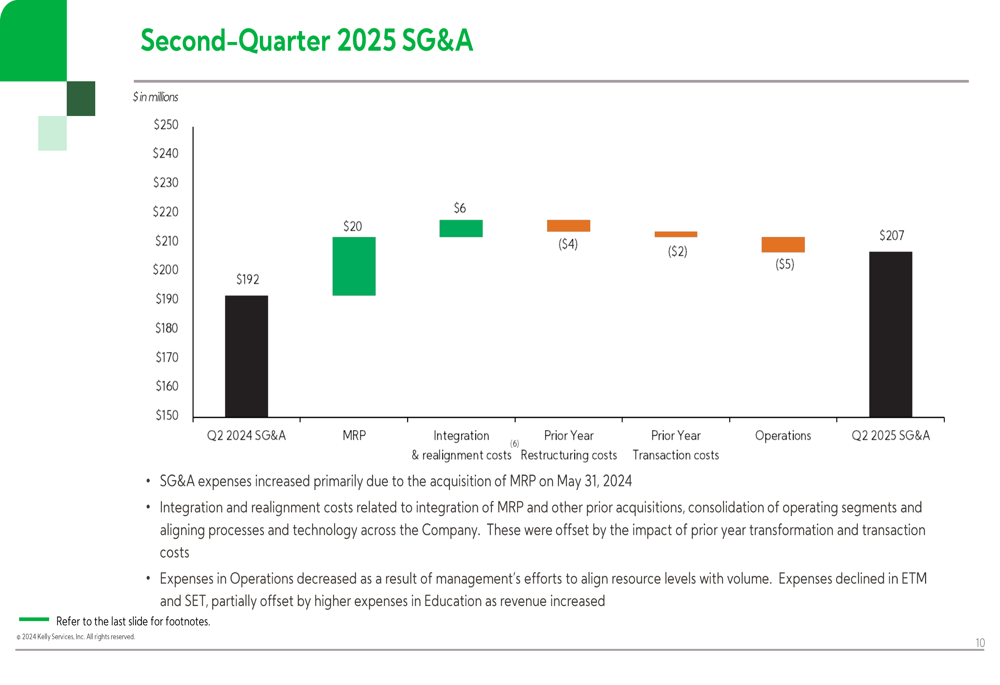

Kelly Services’ SG&A expenses increased to $207 million in Q2 2025, up from $192 million in Q2 2024. This increase was primarily attributed to the MRP acquisition, which added $20 million in expenses, and integration and realignment costs of $6 million. These increases were partially offset by reductions in operations expenses and prior year costs:

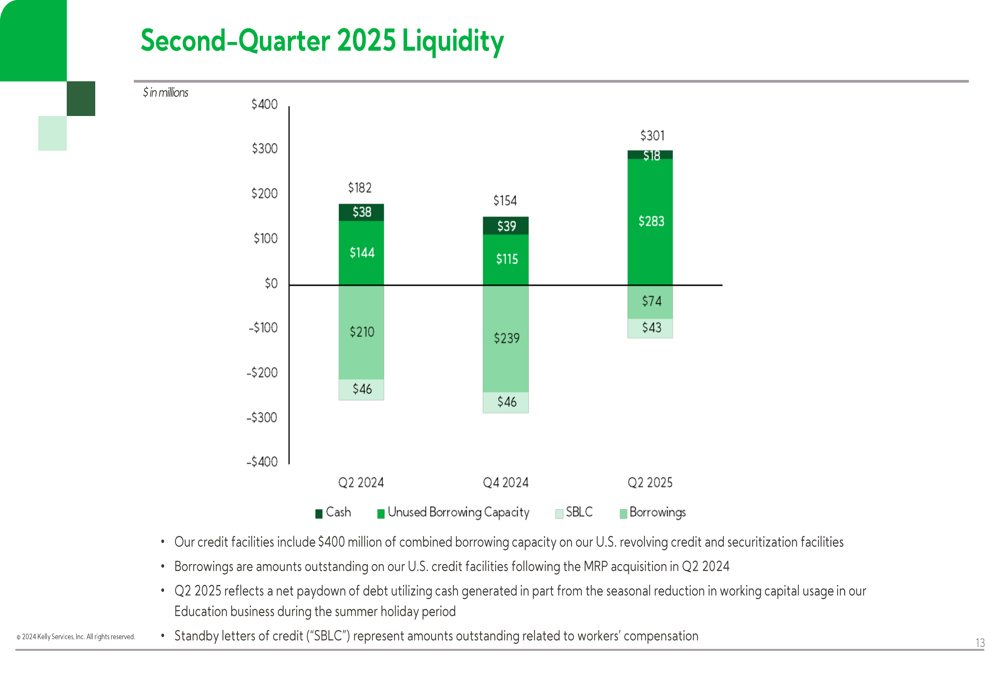

The company’s liquidity position has changed significantly since the MRP acquisition, with cash decreasing to $74 million from $210 million a year ago, while borrowings increased to $301 million from $46 million in Q2 2024:

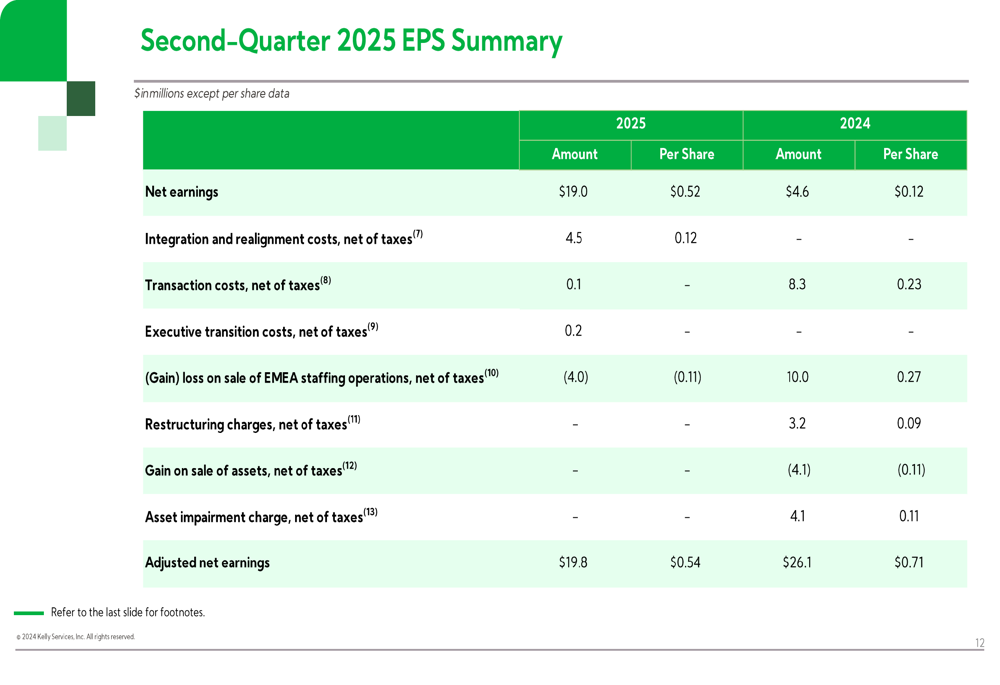

The EPS analysis reveals several one-time items affecting reported results, including integration and realignment costs, transaction costs, and gains on the sale of EMEA staffing operations:

Forward Outlook

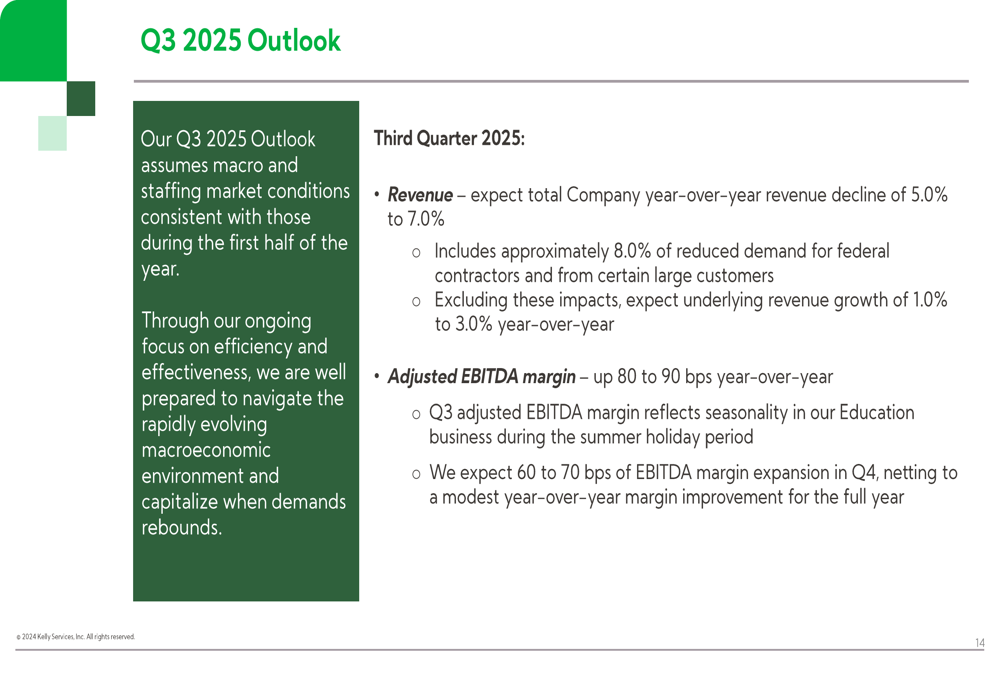

Looking ahead to Q3 2025, Kelly Services expects total company revenue to decline between 5.0% and 7.0% year-over-year. This projection includes approximately 8.0% reduced demand from federal contractors and certain large customers. Excluding these impacts, the company anticipates underlying revenue growth between 1.0% and 3.0%.

Despite the revenue challenges, management expects adjusted EBITDA margin to improve by 80 to 90 basis points year-over-year in Q3, with further expansion of 60 to 70 basis points projected for Q4:

Strategic Positioning

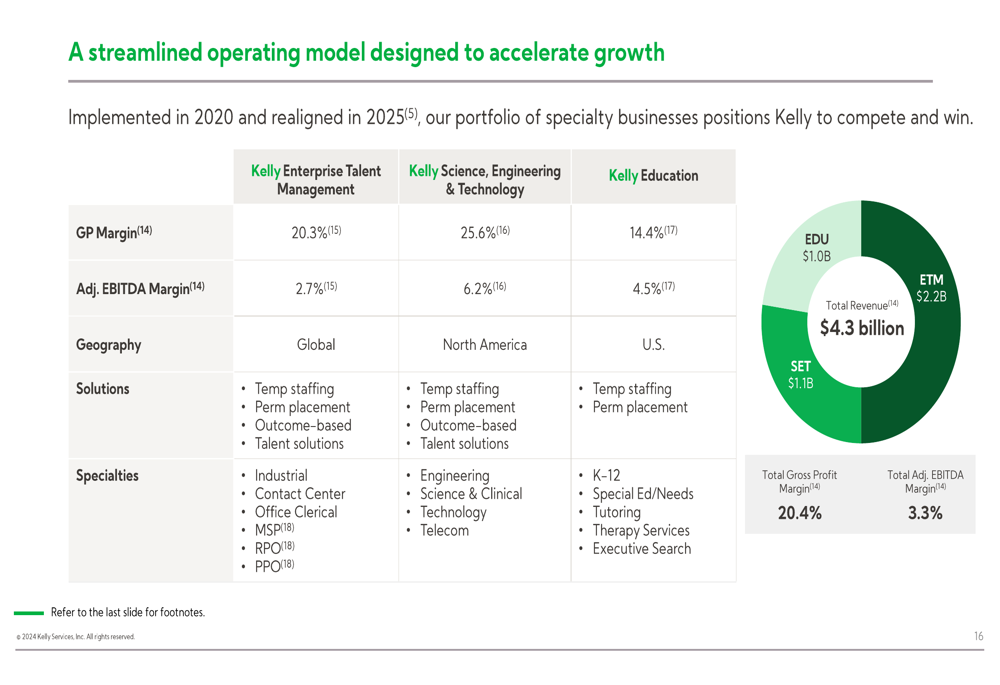

Kelly Services continues to execute its strategy focused on North American specialty staffing and global RPO (Recruitment Process Outsourcing) and MSP (Managed Service Provider) businesses. The company has implemented a streamlined operating model designed to accelerate growth across its three main segments:

This operating model, initially implemented in 2020 and realigned in 2025, shows significant variation in profitability across segments. The Science, Engineering & Technology segment demonstrates the highest gross profit margin at 25.6% and adjusted EBITDA margin at 6.2%, while Education shows the lowest gross profit margin at 14.4% but maintains a solid adjusted EBITDA margin of 4.5%.

Management emphasized their continued focus on profitable growth, including proactive expense management and resource alignment to navigate the evolving macroeconomic environment. The integration of Motion Recruitment Partners remains a key strategic initiative, though it has contributed to increased expenses in the short term.

The company’s Q2 results and Q3 outlook suggest that while Kelly Services continues to face organic growth challenges amid uncertain economic conditions, its strategic acquisitions and focus on margin improvement are positioning it to capitalize on eventual market recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.