5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Kemira Oyj (HEL:KEMIRA) reported its second quarter 2025 results on July 18, demonstrating resilience in a challenging market environment. While the company faced headwinds in certain segments, it maintained solid profitability levels and announced strategic initiatives including a significant share buyback program.

The Finnish chemical company’s stock closed at €19.05 on October 14, 2025, down 1% for the day. The shares have traded between €16.95 and €22.48 over the past 52 weeks, reflecting moderate volatility in a challenging chemical sector environment.

Quarterly Performance Highlights

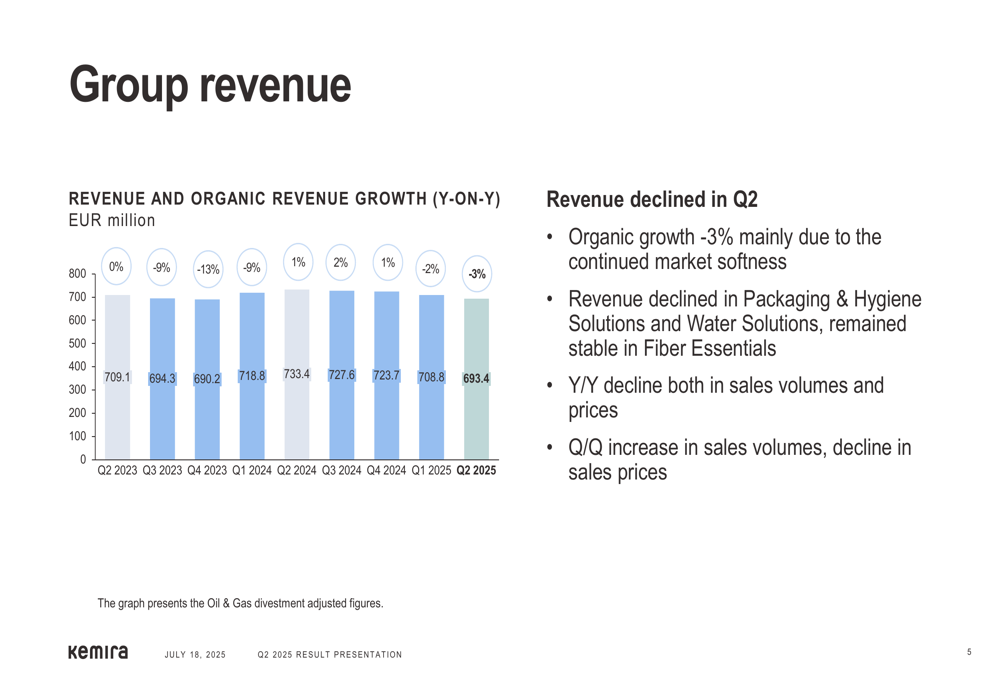

Kemira reported Q2 2025 revenue of €693.4 million, representing an organic decline of 3% year-over-year. Despite this revenue drop, the company maintained an operative EBITDA margin of 19.0%, demonstrating the resilience of its business model in difficult market conditions.

As shown in the following revenue chart, the company has experienced a gradual decline in quarterly revenue since mid-2024:

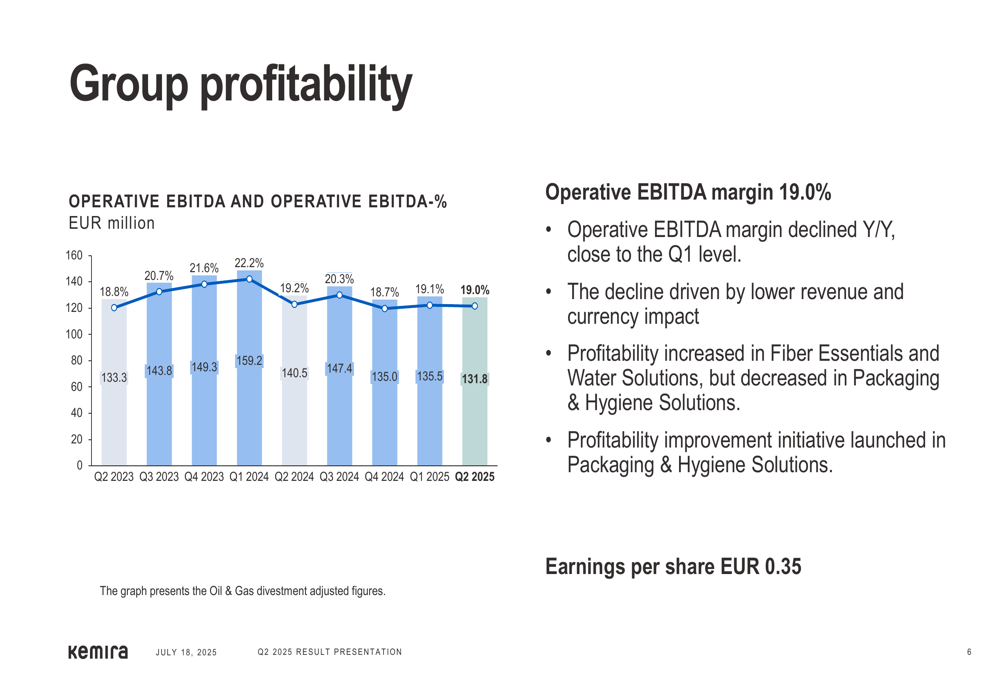

The operative EBITDA for Q2 2025 was €131.8 million, with the company maintaining its profitability level close to Q1 2025 despite revenue challenges. The following chart illustrates Kemira’s consistent EBITDA margin performance:

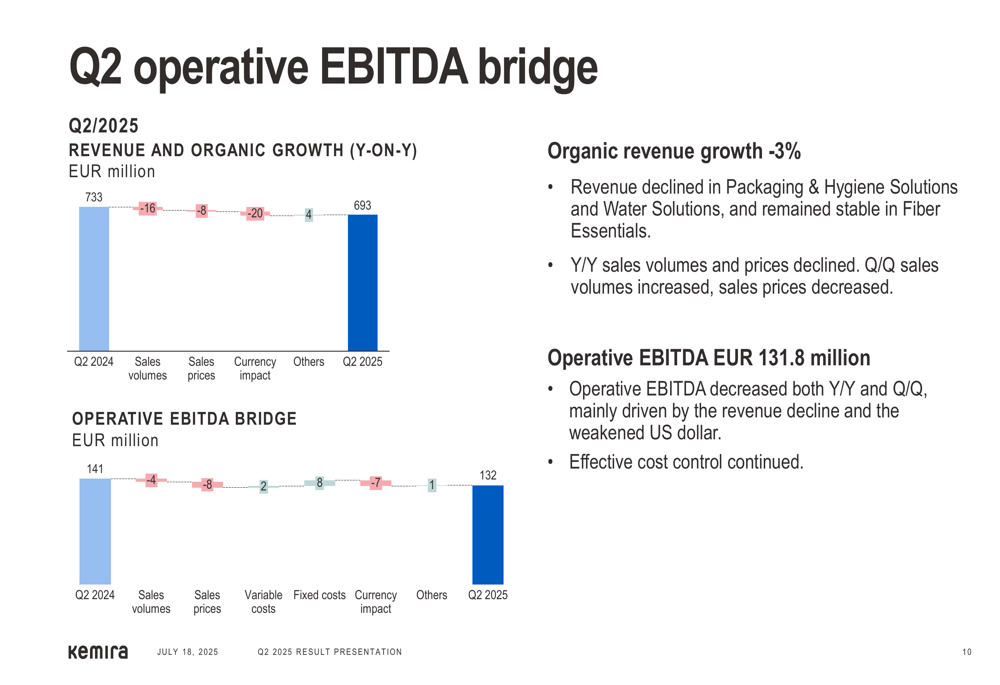

The company’s Q2 operative EBITDA bridge reveals that the decline was primarily driven by lower revenue and negative currency impact, partially offset by effective cost control:

Segment Performance

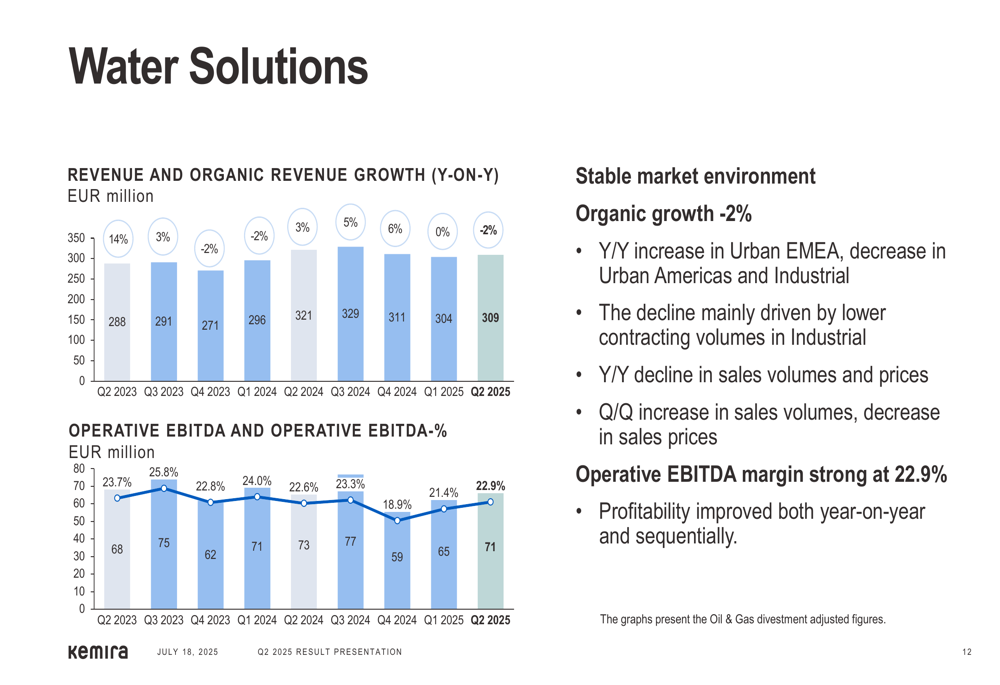

Kemira’s business performance showed significant divergence across its three segments. The Water Solutions segment demonstrated resilience with a 22.9% operative EBITDA margin, improving both year-on-year and sequentially despite a 2% organic revenue decline.

The following chart shows the Water Solutions segment’s stable performance:

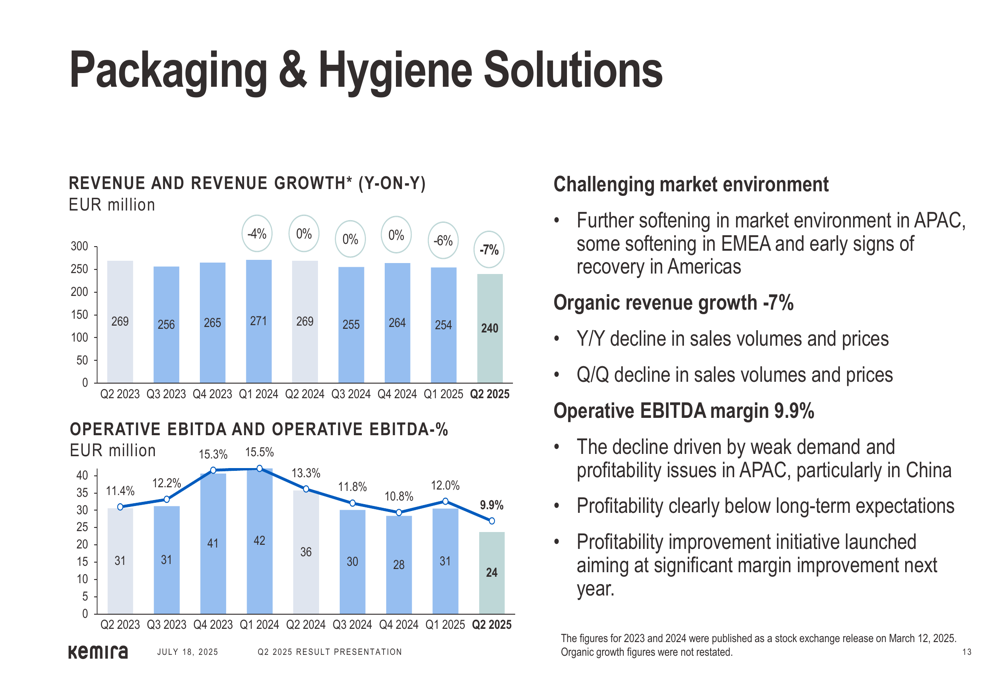

In contrast, the Packaging & Hygiene Solutions segment faced significant challenges, with organic revenue declining 7% and operative EBITDA margin falling to 9.9%. The company cited a challenging market environment, particularly in APAC, and has launched a profitability improvement initiative aimed at significant margin improvement next year.

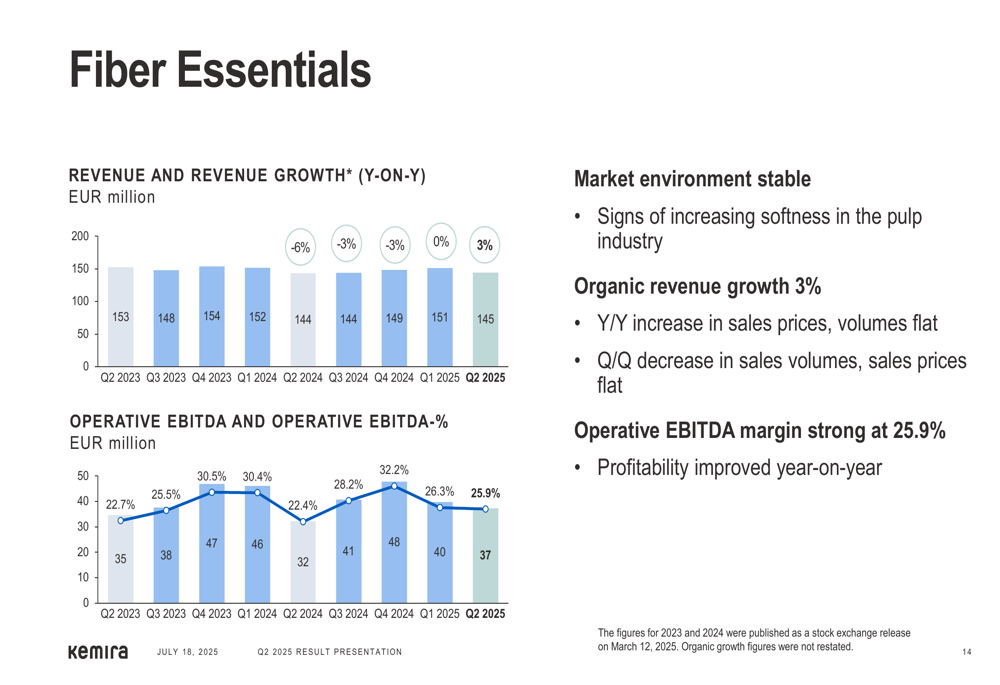

The Fiber Essentials segment maintained strong profitability with a 25.9% operative EBITDA margin, improving year-on-year despite market softness in the pulp industry:

Strategic Initiatives

Despite market challenges, Kemira continues to execute its growth strategy through targeted investments and partnerships. The company announced an expansion of its sodium borohydride powder capacity in Finland with an investment of less than €10 million to support the growing pharmaceutical industry.

Additionally, Kemira completed the acquisition of Thatcher Group’s iron sulfate coagulant business in the US at the beginning of Q2, with an annual revenue impact of less than $10 million.

The company also announced several innovation partnerships, including a collaboration with Bluepha to commercialize fully bio-based barrier coatings in APAC, a partnership with Metsä Group to develop new Kuura textile fiber, and a collaboration with CuspAl to enhance material innovation through AI technologies.

In a significant move to enhance shareholder value, Kemira announced a €100 million share buyback program to be launched on July 22, 2025. The program will allow the company to repurchase up to 5 million shares (approximately 3.2% of total shares) through September 20, 2026.

Financial Position and Cash Flow

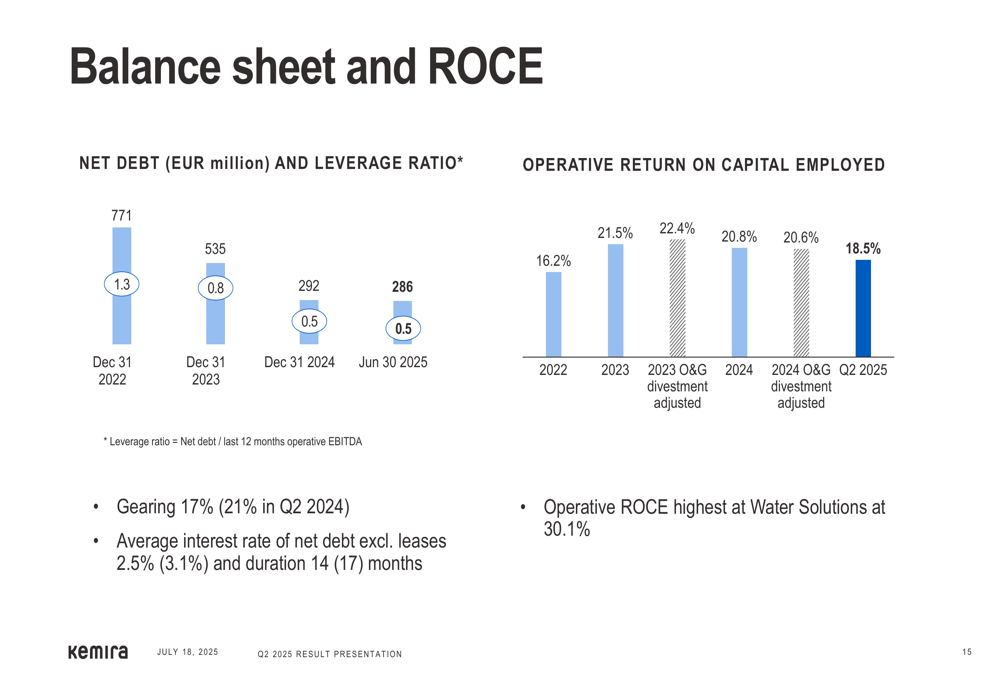

Kemira maintained a strong balance sheet with net debt of €286 million as of June 30, 2025, resulting in a gearing ratio of 17% (down from 21% in Q2 2024). The company’s average interest rate on net debt excluding leases was 2.5%, down from 3.1% a year earlier.

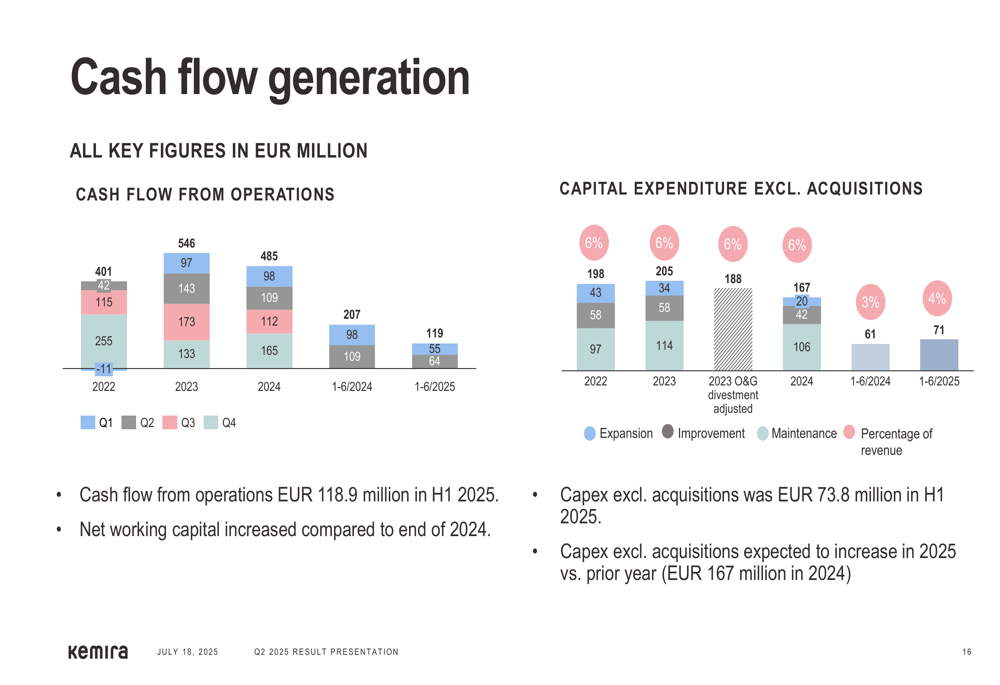

Cash flow from operations was €118.9 million in H1 2025, with capital expenditure excluding acquisitions at €73.8 million. The company noted that net working capital increased compared to the end of 2024, and capital expenditure is expected to increase in 2025 compared to the prior year (€167 million in 2024).

Outlook and Guidance

Kemira updated its outlook for 2025 on July 10, reflecting the challenging market conditions. The company now expects revenue to be between €2,700 and €2,950 million in 2025, compared to reported 2024 revenue of €2,948.1 million. Operative EBITDA is expected to be between €510 and €580 million, compared to €585.4 million in 2024.

The outlook assumes continued global economic uncertainty resulting in softer volume demand, particularly in the packaging and pulp markets, while the water treatment market is expected to grow in all regions. The company also assumes no major disruptions to manufacturing operations, supply chain, or energy-generating assets in Finland, and that the US dollar will remain approximately at the same level as at the end of Q2 2025.

Additional Insights

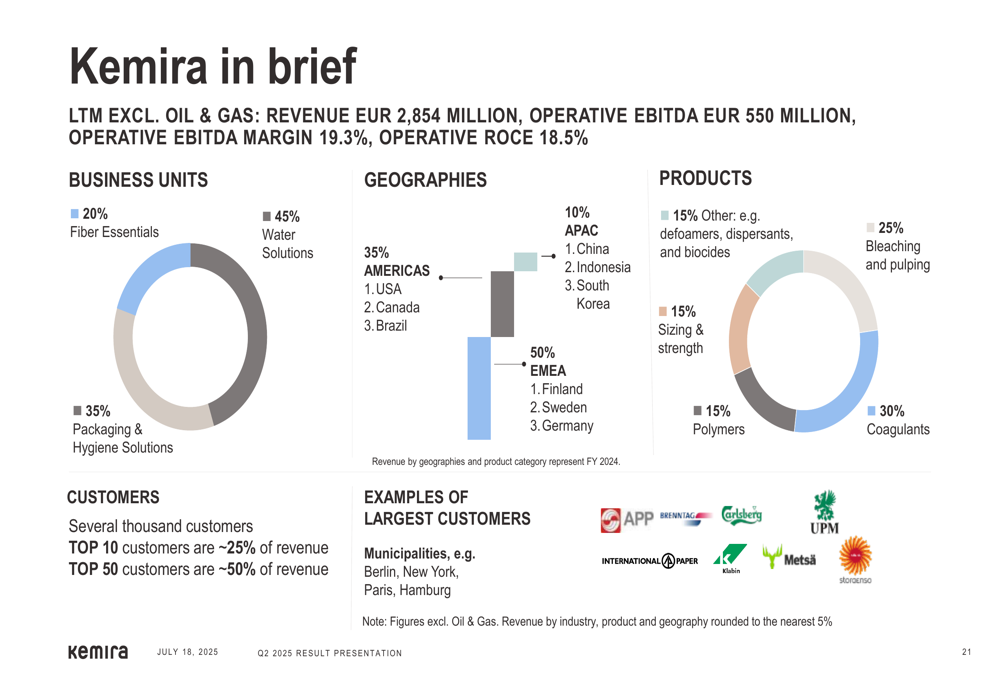

Kemira’s business is diversified across multiple segments and geographies, providing some resilience against regional market challenges. The company’s revenue distribution shows EMEA accounting for 50% of revenue, Americas 35%, and APAC 10%, as illustrated in this overview:

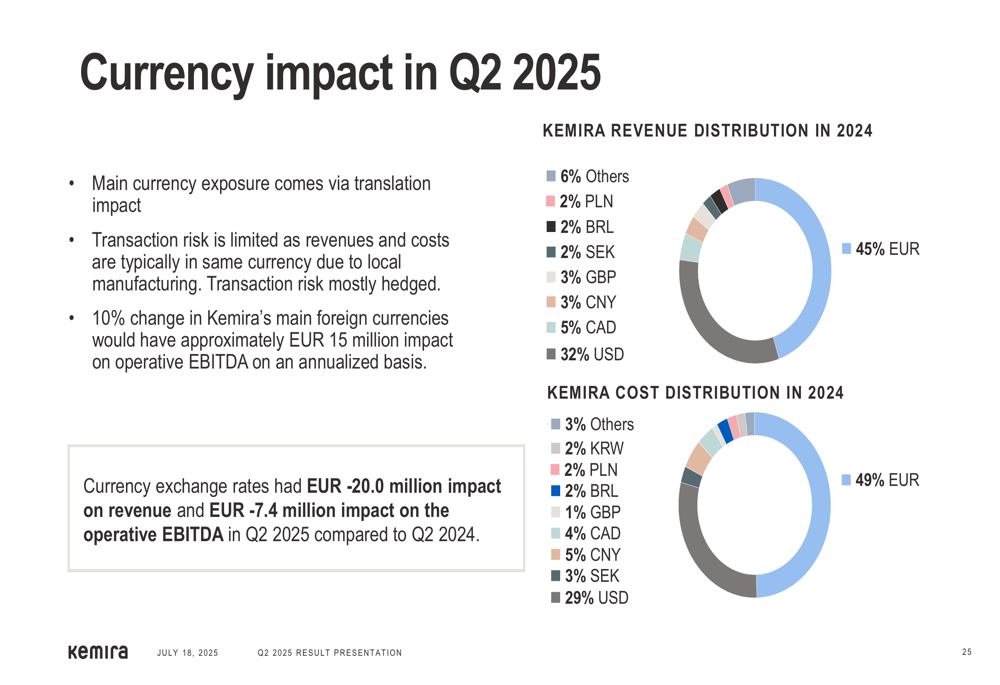

Currency fluctuations had a significant impact on Kemira’s results, with exchange rates causing a €20.0 million reduction in revenue and €7.4 million decrease in operative EBITDA in Q2 2025 compared to Q2 2024. The company’s main currency exposure comes from the US dollar, which accounts for 32% of revenue and 29% of costs.

Despite market challenges, Kemira reported strong customer satisfaction with a Net Promoter Score of 65, an all-time high and up from 59 in 2024. Employee engagement remained stable at 80, well above the industry average of 73, indicating strong internal alignment during challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.