5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Kemira Oyj (HEL:KEMIRA) released its Q3 2025 results on October 24, 2025, demonstrating resilience in profitability despite facing revenue headwinds in a challenging global economic environment. The company’s stock responded positively to the results, rising 3.39% to €20.14 following the announcement, suggesting investor confidence in Kemira’s strategic direction despite slight earnings underperformance.

CEO Antti Salminen emphasized the company’s ability to maintain strong margins during the earnings call, stating, "We maintained good profitability in the weak end market environment." This sentiment captures Kemira’s Q3 performance, which showed revenue declines across all business segments but preserved healthy profit margins through operational excellence initiatives.

Quarterly Performance Highlights

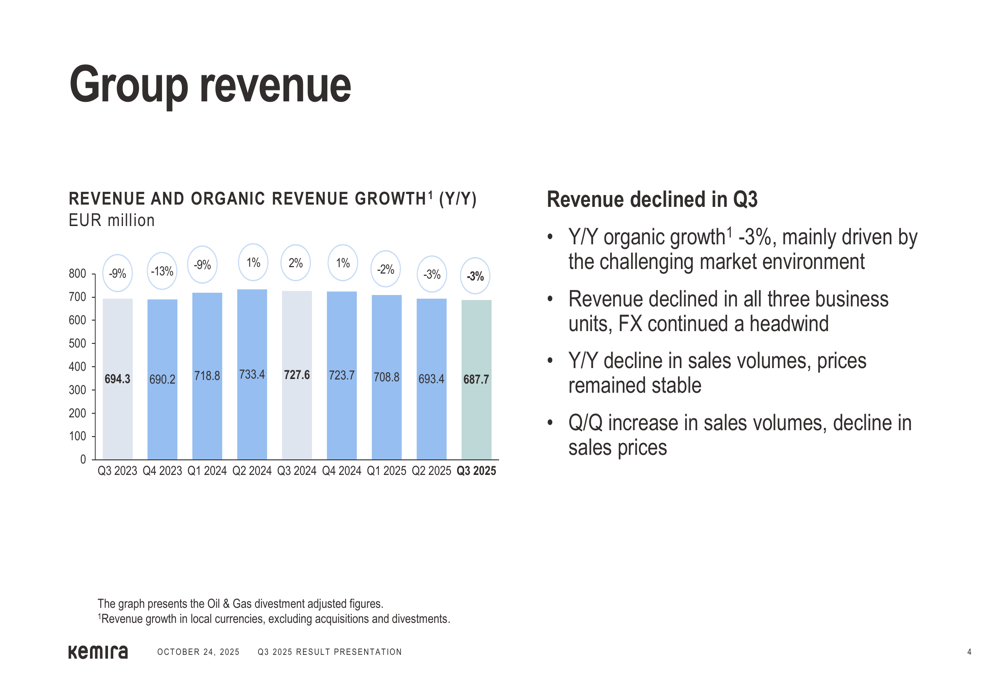

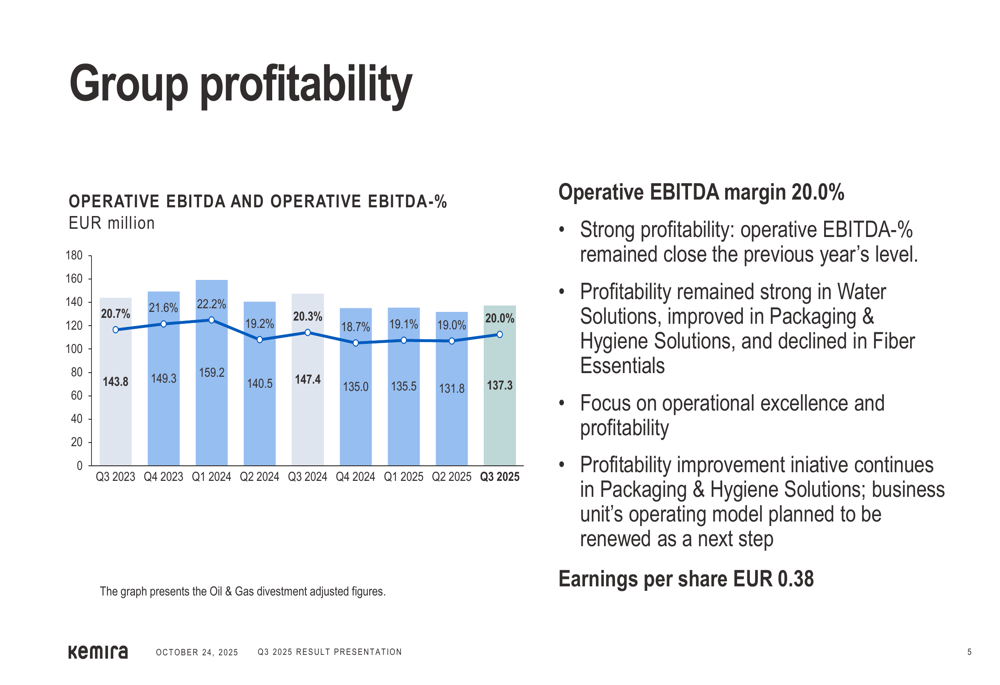

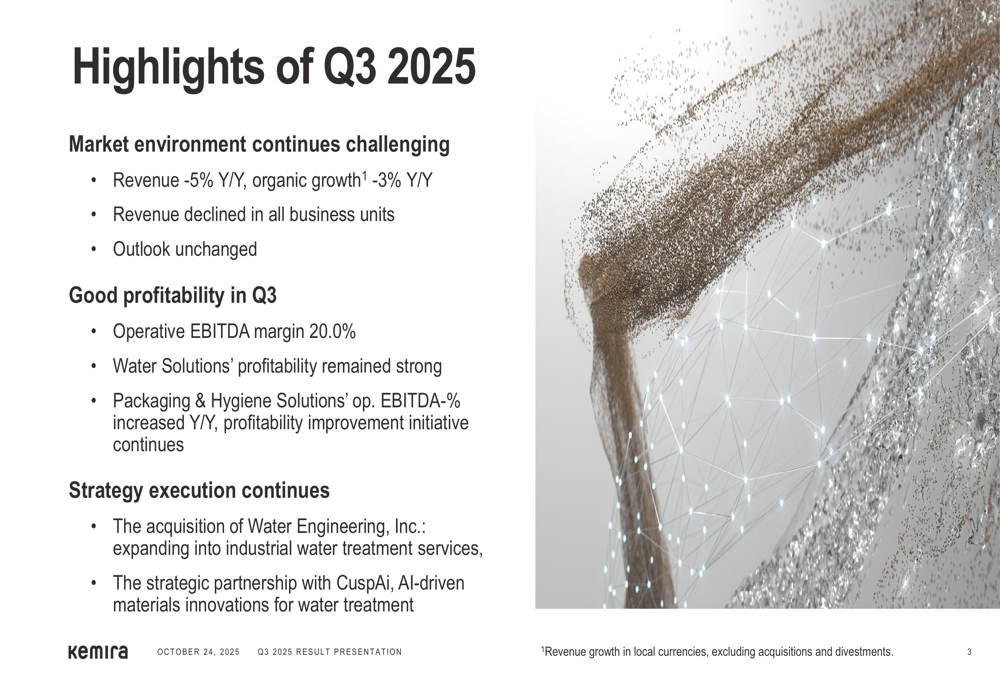

Kemira reported Q3 2025 revenue of €687.7 million, representing a 5% year-over-year decline, with organic growth down 3%. Despite this revenue contraction, the company maintained an impressive operative EBITDA margin of 20.0%, only slightly below the 20.3% achieved in Q3 2024.

As shown in the following revenue trend chart, Kemira has experienced a gradual decline in revenue over recent quarters, reflecting the challenging market environment:

The company’s earnings per share came in at €0.38, slightly below analyst expectations of €0.3948. However, this minor miss didn’t dampen investor sentiment, likely due to the company’s strong profitability metrics and strategic initiatives.

The following chart illustrates Kemira’s consistent profitability performance despite revenue challenges:

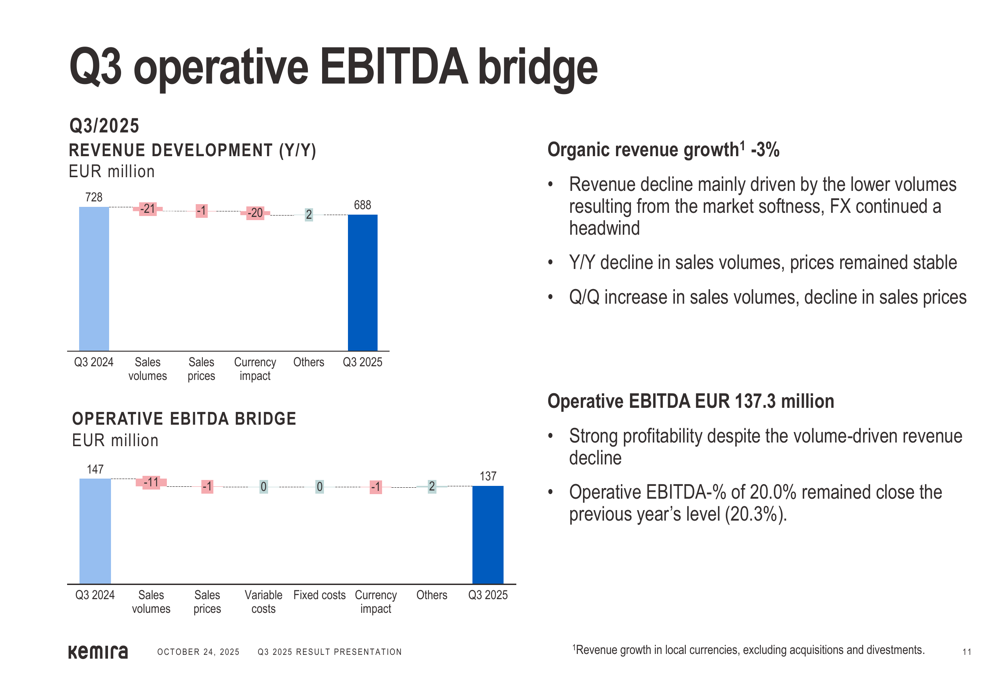

A detailed breakdown of the factors affecting operative EBITDA reveals that volume declines were the primary driver behind the year-over-year reduction, while the company maintained stable pricing:

Business Segment Performance

Kemira’s three business segments showed varying performance in the challenging market environment:

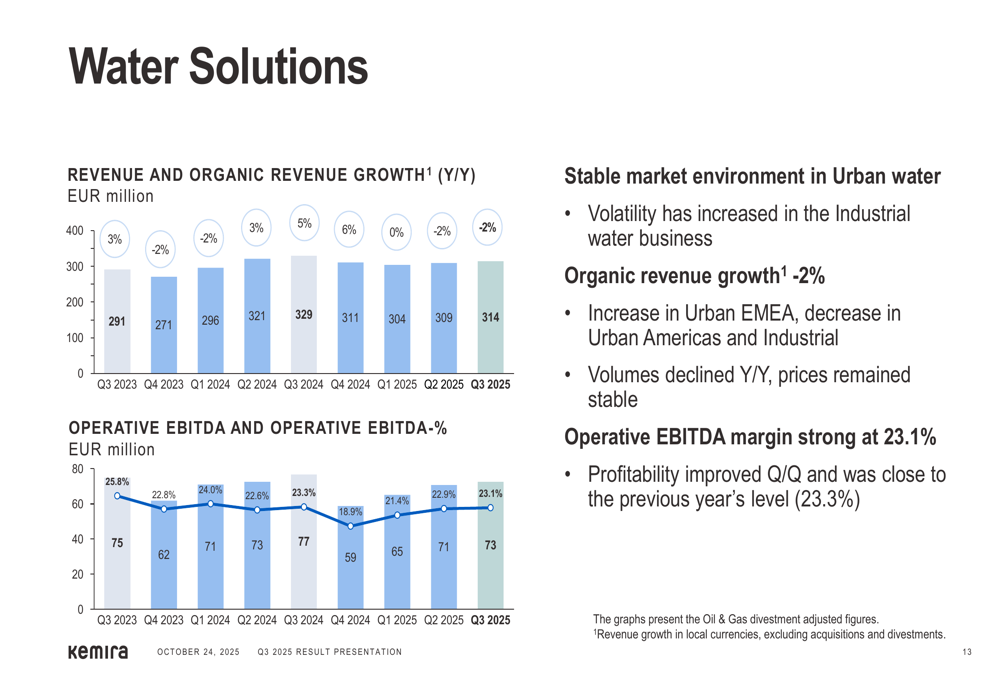

The Water Solutions segment, which represents Kemira’s largest business unit, demonstrated resilience with revenue of €314 million and a strong operative EBITDA margin of 23.1%. While organic revenue declined by 2%, profitability remained robust, nearly matching the previous year’s level.

As shown in the following chart, the Water Solutions segment has maintained relatively stable performance compared to other business units:

The Packaging & Hygiene Solutions segment faced more significant challenges with revenue of €239 million, representing an organic decline of 3%. However, the segment’s operative EBITDA margin improved to 13.6% from 11.8% in Q3 2024, demonstrating the effectiveness of the company’s profitability improvement initiatives.

The Fiber Essentials segment experienced the most significant challenges, with revenue of €134 million and organic growth down 5%. The segment’s operative EBITDA margin declined to 24.1% from 28.2% in the previous year, primarily due to volume decreases in a sluggish market environment, particularly in the Nordic region.

Strategic Initiatives

Kemira’s Q3 presentation highlighted several strategic initiatives aimed at positioning the company for future growth despite current market challenges.

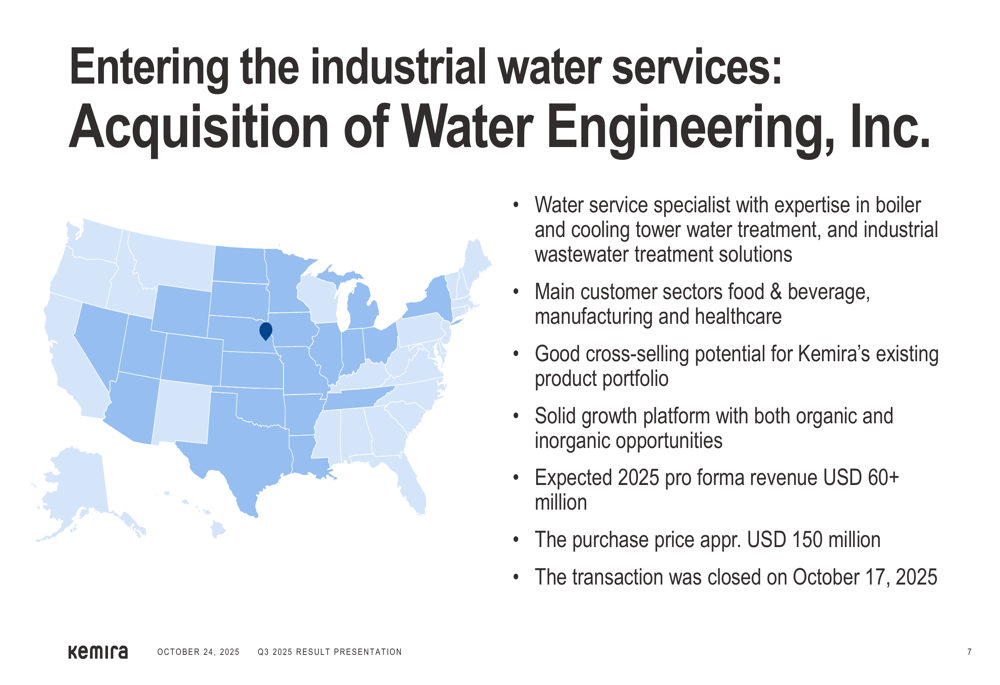

The most significant development was the acquisition of Water Engineering, Inc., a water service specialist with expertise in boiler and cooling tower water treatment and industrial wastewater treatment solutions. The USD 150 million acquisition, which closed on October 17, 2025, provides Kemira with a solid growth platform in the industrial water treatment services market.

As shown in the following map, the acquisition expands Kemira’s presence in key U.S. markets:

Additionally, Kemira announced a strategic partnership with CuspAI for AI-driven materials innovations for water treatment, with an initial focus on removing PFAS from water. The company also approved an investment in an activated carbon reactivation site in Helsingborg, Sweden, which will be the first facility of its kind in the Nordic region.

Financial Position & Outlook

Kemira has significantly strengthened its financial position, with net debt reduced to €292 million from €771 million in 2022, resulting in a leverage ratio of just 0.5. This improved financial flexibility provides the company with resources to pursue strategic investments and acquisitions.

Cash flow from operations showed strong improvement, reaching €132.2 million in the first nine months of 2025, an 18% increase compared to the same period in 2024. This robust cash generation occurred despite increased net working capital compared to the end of 2024.

Kemira maintained its outlook for 2025, expecting revenue between €2,700 and €2,950 million and operative EBITDA between €510 and €580 million. The outlook assumes continued global economic uncertainty resulting in softer volume demand, particularly in the packaging and pulp markets, while the water treatment market is expected to grow.

The following slide summarizes the company’s key highlights for Q3 2025:

Leadership Changes

Kemira announced the appointment of Tuomas Mäkipeska as the company’s new CFO. Mäkipeska, who will join Kemira from YIT where he has served as CFO and Deputy to the CEO since 2021, will start in his new position by May 2026 at the latest. He will succeed current CFO Petri Castrén, who will be leaving the company as previously announced.

The following image shows the newly appointed CFO:

Conclusion

Kemira’s Q3 2025 results demonstrate the company’s ability to maintain strong profitability despite revenue challenges in a difficult market environment. The strategic acquisition of Water Engineering, Inc. and other initiatives position the company for future growth, particularly in the water treatment sector, which continues to show resilience.

While the company faces headwinds in its Packaging & Hygiene and Fiber Essentials segments due to sluggish market conditions, the ongoing profitability improvement initiatives and operational excellence focus have helped maintain healthy margins. The strengthened financial position, with reduced debt and strong cash flow generation, provides Kemira with flexibility to weather current market challenges while investing for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.