Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Kemper Corporation (NYSE:KMPR) delivered strong financial results in the first quarter of 2025, according to its earnings presentation released on May 7. The specialty insurer, which focuses on underserved markets including Latino, Hispanic, and urban communities, reported significant growth in its core auto insurance business while maintaining solid profitability metrics.

The company’s strategic positioning in specialty markets appears to be paying dividends as it reported double-digit growth in policies and premiums while maintaining a healthy combined ratio. This performance comes amid persistent hard market conditions in California and increasing competition in selective markets.

Quarterly Performance Highlights

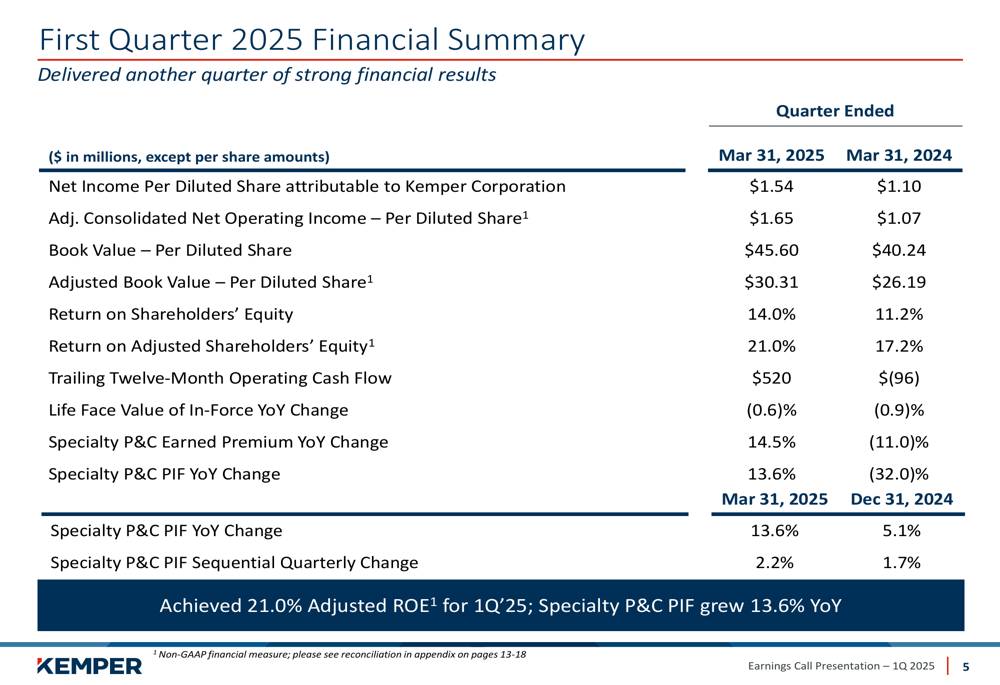

Kemper reported net income of $99.7 million or $1.54 per diluted share for Q1 2025, compared to $71.3 million or $1.10 per share in the same period last year. Adjusted consolidated net operating income reached $106.4 million or $1.65 per diluted share, representing substantial year-over-year growth.

The company achieved a return on equity (ROE) of 14.0% and an adjusted ROE of 21.0% for the quarter, demonstrating strong profitability. Book value per share increased 13.3% year-over-year to $45.60, while adjusted book value per share grew 15.7% to $30.31.

As shown in the following comprehensive financial summary from the presentation:

Particularly noteworthy is the dramatic improvement in trailing twelve-month operating cash flow, which reached $520 million compared to negative $96 million in the prior year period. This cash generation strengthens Kemper’s financial flexibility and supports its growth initiatives.

Specialty P&C Segment Analysis

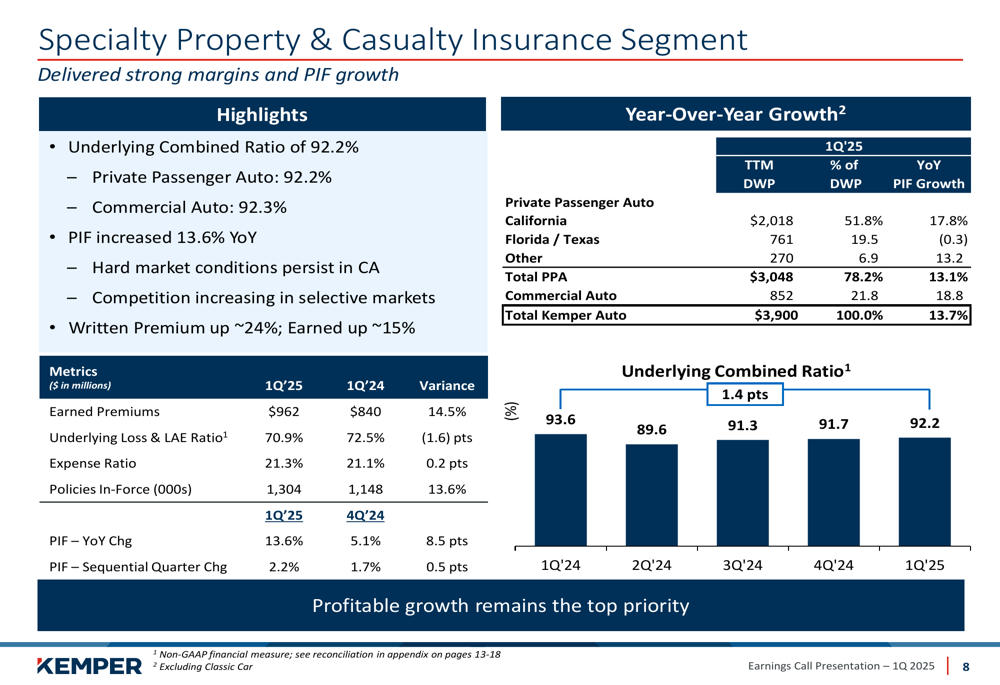

The Specialty Property & Casualty segment was a standout performer in Q1 2025, delivering an underlying combined ratio of 92.2%, slightly higher than the 91.7% reported in Q4 2024 but improved from 93.6% in Q1 2024. Both private passenger auto and commercial auto businesses maintained healthy combined ratios of 92.2% and 92.3%, respectively.

Policies in force (PIF) increased 13.6% year-over-year and 2.2% sequentially, demonstrating continued momentum in customer acquisition. Written premiums grew approximately 24% year-over-year, while earned premiums increased by about 15%.

The following chart illustrates the segment’s performance metrics and geographic distribution:

California remains Kemper’s largest market, representing 51.8% of private passenger auto business and showing strong growth of 17.8% year-over-year. The company noted that hard market conditions persist in California, while competition is increasing in selective markets.

Life Insurance (NSE:LIFI) Segment Performance

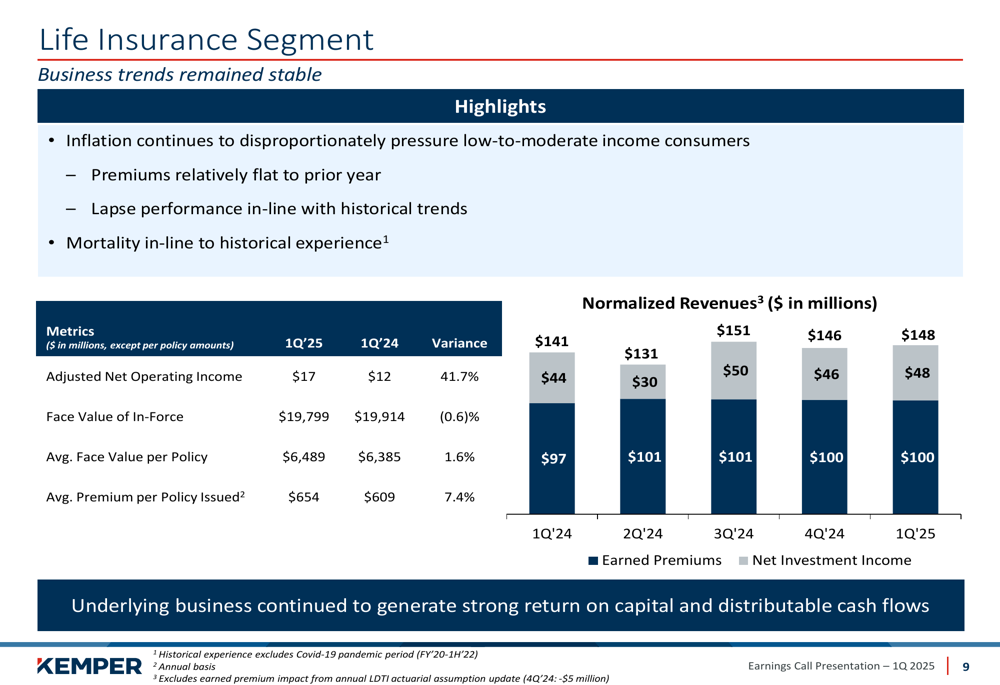

Kemper’s Life Insurance segment, which targets low to moderate-income customers, continued to generate consistent returns despite facing challenges from inflation that disproportionately pressures its target demographic. The segment reported adjusted net operating income of $17 million in Q1 2025, up from $12 million in Q1 2024.

The face value of in-force policies declined slightly by 0.6% year-over-year to $19.8 billion. However, the average face value per policy increased to $6,489 from $6,385 a year earlier, and the average premium per policy issued rose to $654 from $609.

The following chart shows the segment’s normalized revenues and key metrics:

Management noted that lapse performance remained in line with historical trends, and mortality experience was consistent with historical patterns. The business continues to generate strong return on capital and distributable cash flows, supporting Kemper’s overall financial strength.

Investment Portfolio and Capital Position

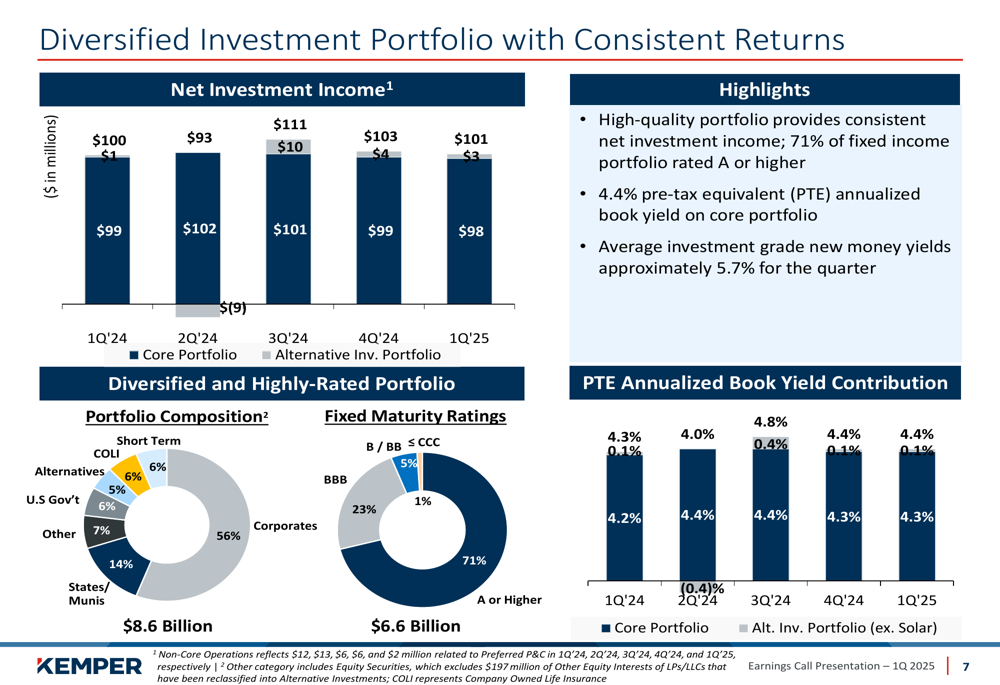

Kemper maintains a diversified investment portfolio that provided consistent net investment income of $101 million in Q1 2025, comparable to $100 million in Q1 2024. The portfolio is predominantly high-quality, with 71% of fixed income investments rated A or higher.

The pre-tax equivalent annualized book yield on the core portfolio was 4.4%, while new money yields for investment-grade securities averaged approximately 5.7% for the quarter.

As illustrated in the following chart of the investment portfolio composition and performance:

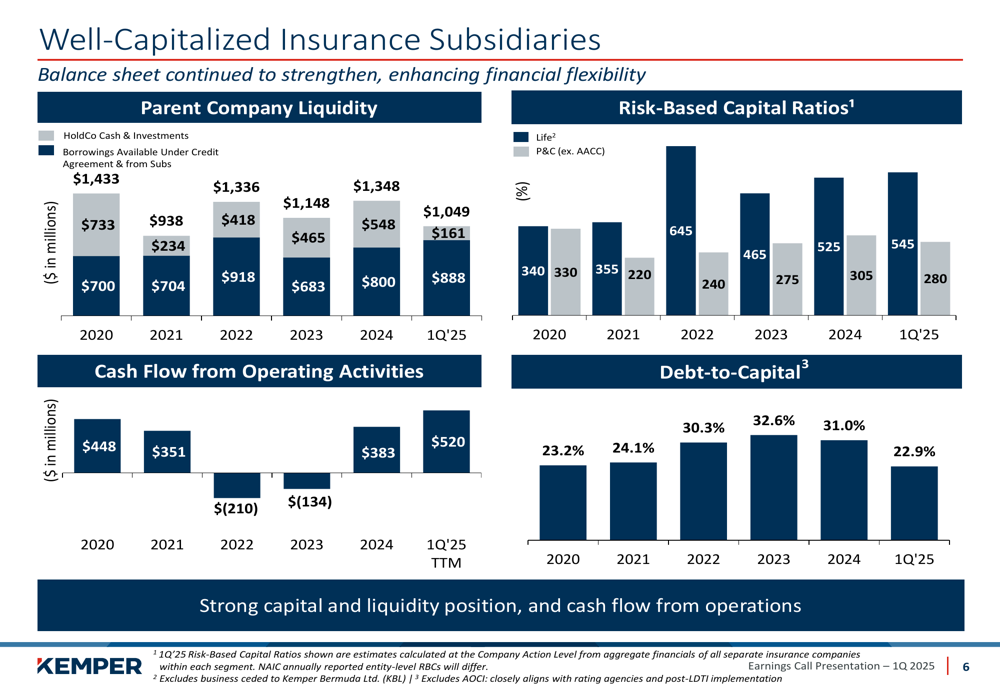

The company’s capital position strengthened significantly, with the debt-to-capital ratio improving by 8.1 percentage points year-over-year to 22.9%. Parent company liquidity remained robust at approximately $1 billion, and all insurance subsidiaries maintained strong risk-based capital ratios.

The following chart details Kemper’s capital strength and liquidity position:

During the quarter, Kemper repurchased $4 million of stock, with approximately $130 million remaining under its current repurchase program.

Forward-Looking Statements

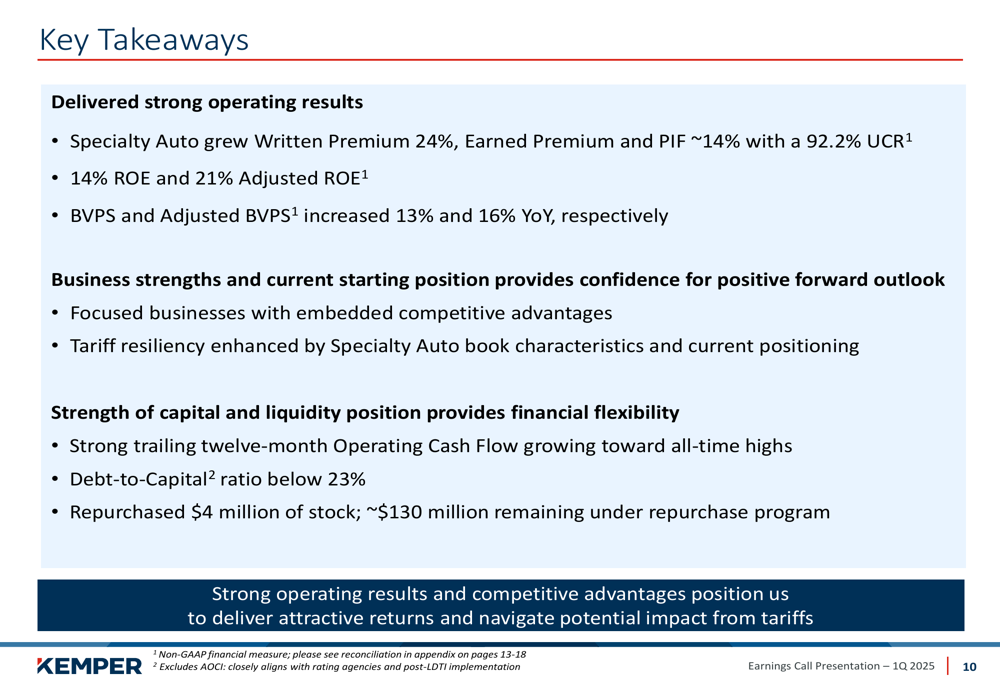

Looking ahead, Kemper emphasized that profitable growth remains its top priority, particularly in the Specialty Auto business. The company believes its strong operating results and competitive advantages position it well to deliver attractive returns and navigate potential impacts from tariffs.

Management highlighted the company’s tariff resiliency, which is enhanced by the characteristics of its Specialty Auto book and current market positioning. With strong trailing twelve-month operating cash flow approaching all-time highs and a significantly improved debt-to-capital ratio, Kemper appears well-positioned for continued financial strength.

As summarized in the key takeaways slide from the presentation:

Kemper’s focus on specialty and underserved markets, combined with its differentiated capabilities in low-cost management, ease of use, distribution, and product sophistication, continues to drive its strategy of targeting top-quartile value creation for customers, employees, and shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.