S&P 500 struggles for direction as investor await inflation data

Introduction & Market Context

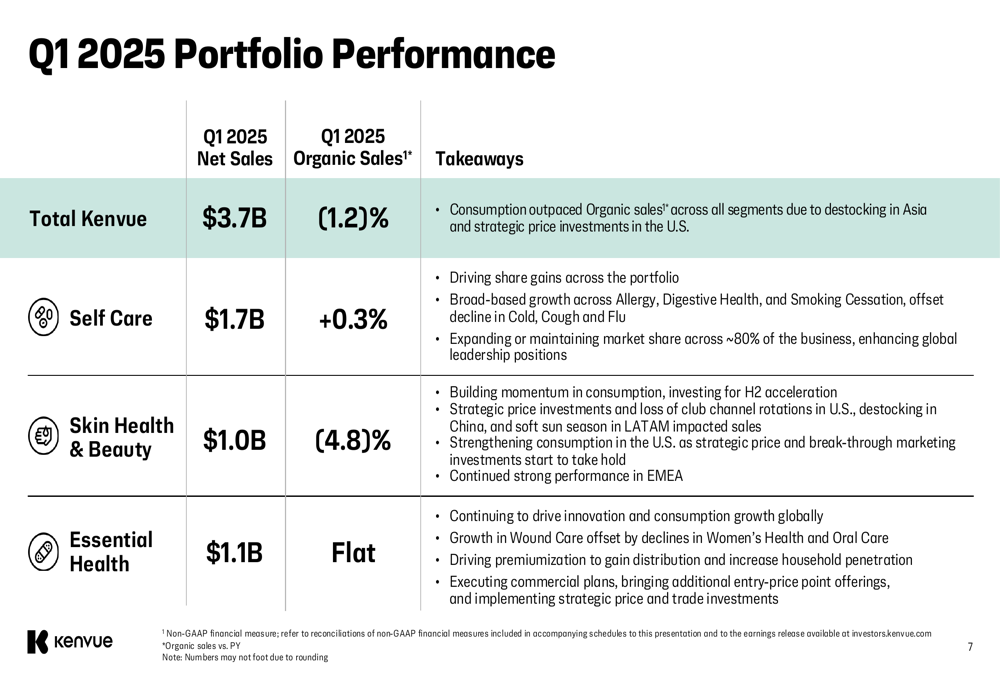

Kenvue Inc . (NYSE:KVUE) presented its first quarter 2025 earnings results on May 8, 2025, revealing a 1.2% decline in organic sales while maintaining its full-year organic sales growth outlook. The consumer health company, which was spun off from Johnson & Johnson (NYSE:JNJ) in 2023, reported that consumption outpaced organic sales across all segments due to destocking in Asia and strategic price investments in the United States.

In premarket trading following the release, Kenvue shares rose 4.11% to $24.06, suggesting investors were encouraged by the company’s maintained sales outlook despite the quarterly decline.

Quarterly Performance Highlights

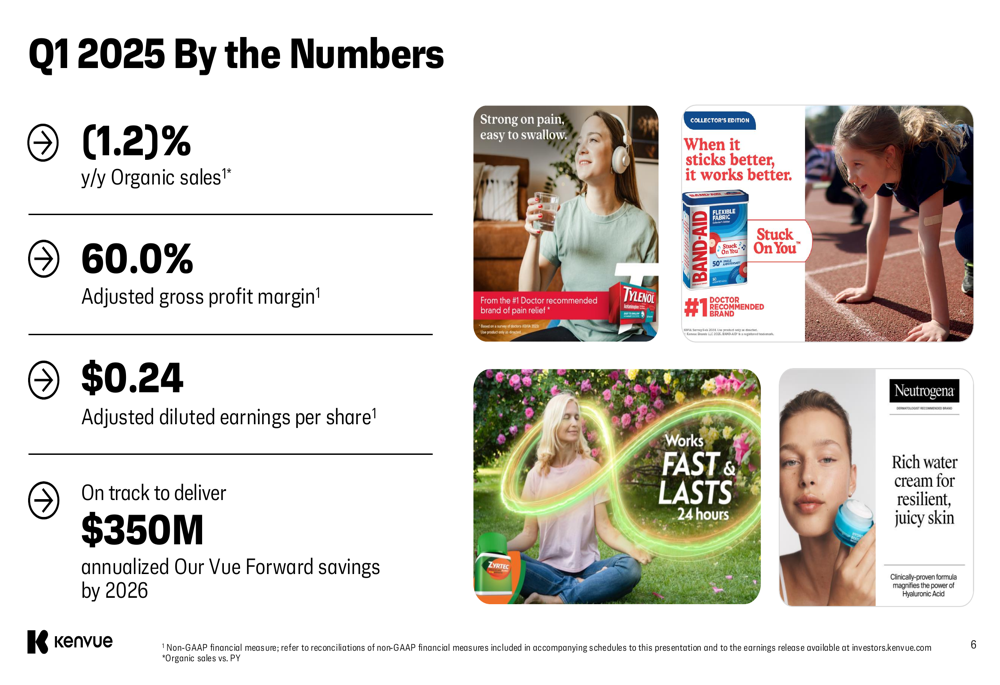

Kenvue reported net sales of $3.7 billion for Q1 2025, down from $3.9 billion in the same period last year. The company’s adjusted diluted earnings per share came in at $0.24, compared to $0.28 in Q1 2024. Despite these declines, the company highlighted several positive developments, including share gains across its portfolio and the completion of its transition from Johnson & Johnson.

As shown in the following key performance metrics:

Performance varied across Kenvue’s three business segments. The Self Care segment, which includes brands like Tylenol and Zyrtec, posted 0.3% organic sales growth. The Skin Health & Beauty segment, featuring brands such as Neutrogena, experienced a 4.8% decline in organic sales. The Essential Health segment, which includes Listerine and Band-Aid, reported flat organic sales.

The following breakdown illustrates performance across all segments:

Detailed Financial Analysis

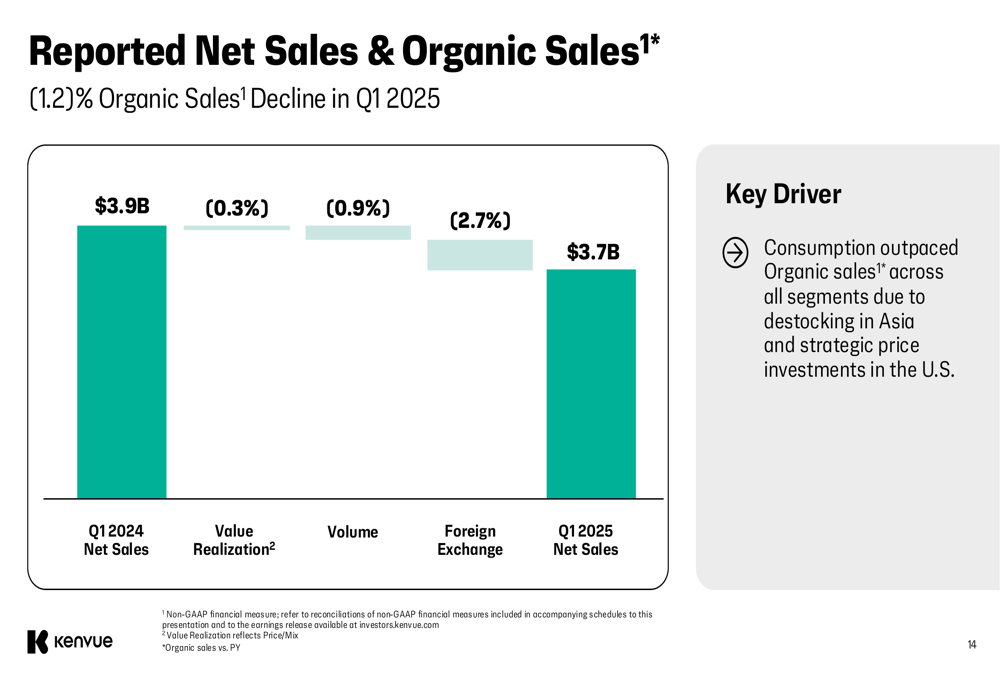

A closer examination of Kenvue’s sales performance reveals that the 1.2% organic sales decline was driven by negative volume (-0.9%) and value realization (-0.3%), with foreign exchange creating an additional 2.7% headwind. This resulted in reported net sales declining from $3.9 billion in Q1 2024 to $3.7 billion in Q1 2025.

The following chart illustrates these factors:

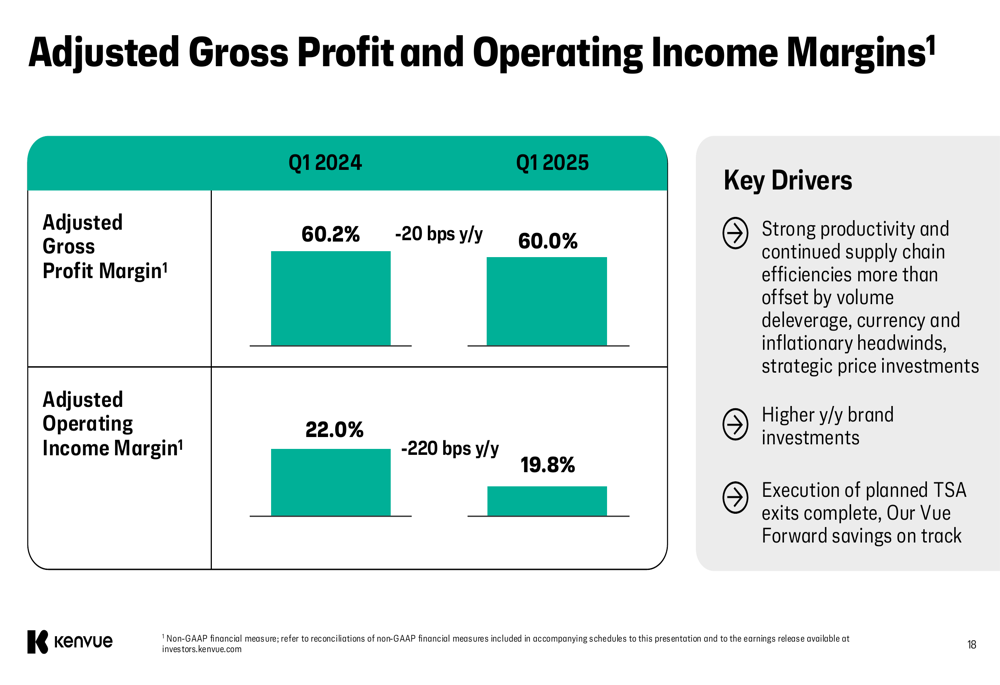

Kenvue’s adjusted gross profit margin held relatively steady at 60.0%, down slightly from 60.2% in the prior year. However, the adjusted operating income margin declined significantly to 19.8%, a 220 basis point decrease from 22.0% in Q1 2024. The company attributed this decline to volume deleverage, currency and inflationary headwinds, strategic price investments, and higher year-over-year brand investments.

This margin performance is visualized in the following chart:

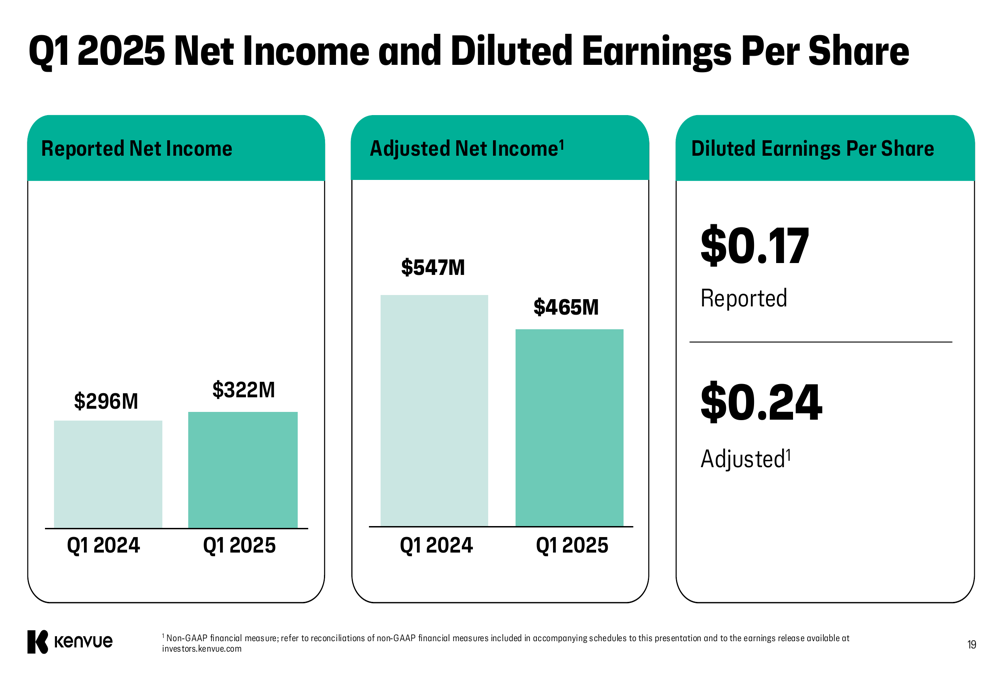

Despite the decline in adjusted metrics, Kenvue’s reported net income increased to $322 million from $296 million in the prior year. However, adjusted net income decreased to $465 million from $547 million. The company’s diluted earnings per share was $0.17 on a reported basis (up from $0.15), while adjusted diluted EPS was $0.24 (down from $0.28).

The earnings performance is summarized in this visual:

Strategic Initiatives

Kenvue highlighted several strategic initiatives during its presentation. The company completed the exit of over 2,300 transition services, marking a significant milestone in its separation from Johnson & Johnson. It also consolidated its U.S. office footprint to drive efficiencies, collaboration, and speed.

The company emphasized that it is leveraging what it calls its "Five Extraordinary Powers" and remains on track to deliver $350 million in annualized "Our Vue Forward" savings by 2026.

In the Skin Health & Beauty segment, which experienced the largest decline, Kenvue noted that strategic price investments and breakthrough marketing efforts are beginning to show positive results, with strengthening consumption in the U.S. The company also mentioned that it is driving premiumization in the Essential Health segment to gain distribution and increase household penetration.

Forward-Looking Statements

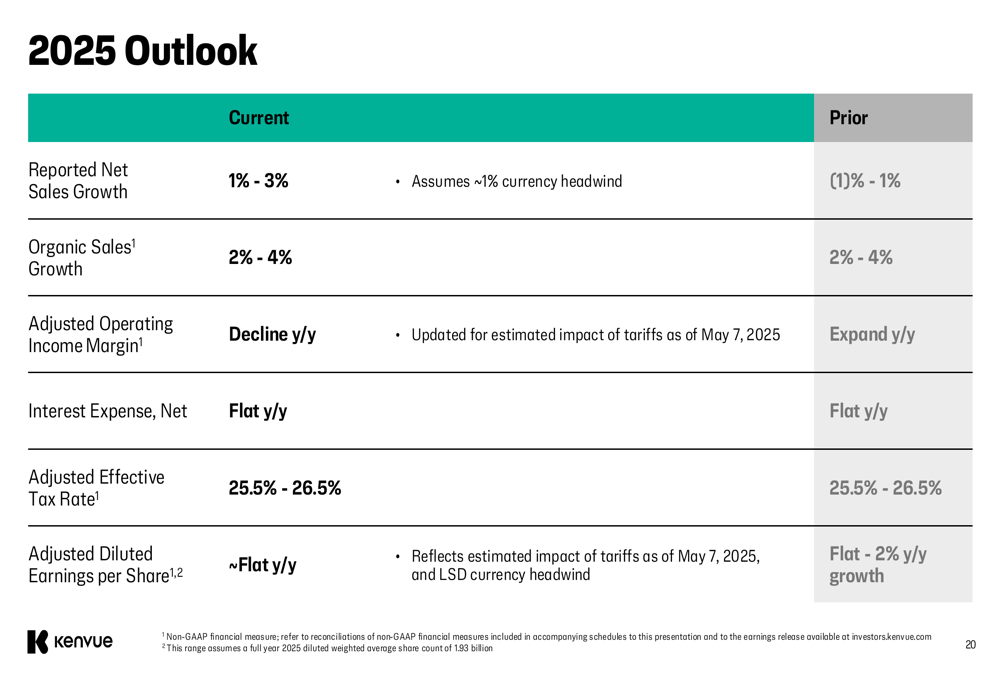

Despite the Q1 challenges, Kenvue maintained its organic sales growth outlook of 2-4% for 2025, suggesting confidence in improved performance for the remainder of the year. However, the company updated its adjusted operating income margin outlook from "expand y/y" to "decline y/y," citing the estimated impact of tariffs as of May 7, 2025.

Similarly, Kenvue revised its adjusted diluted earnings per share outlook from "flat to 2% y/y growth" to "approximately flat y/y," reflecting both the estimated impact of tariffs and a low single-digit currency headwind.

The following chart details the updated outlook compared to prior guidance:

The company also announced a leadership change, with Amit Banati set to join as the new Chief Financial Officer. Banati brings 30 years of experience in global consumer products companies and a track record in both financial and operational roles.

Competitive Industry Position

Despite the challenging quarter, Kenvue emphasized its strong competitive positioning, noting that it is expanding or maintaining market share across approximately 80% of its Self Care business. The company is enhancing its global leadership positions across multiple categories.

In the Skin Health & Beauty segment, while sales declined, Kenvue highlighted strengthening consumption in the U.S. as strategic price and marketing investments begin to take hold. The company also noted continued strong performance in the EMEA region.

For the Essential Health segment, Kenvue is focusing on driving innovation and consumption growth globally. The company is pursuing premiumization strategies to gain distribution and increase household penetration, while also implementing strategic price and trade investments.

As Kenvue navigates the dynamic consumer health landscape, the company’s ability to balance strategic investments with profitability will be crucial for achieving its maintained organic sales growth outlook for the full year 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.