Nvidia’s results, Indian tariffs, French markets - what’s moving markets

Introduction & Market Context

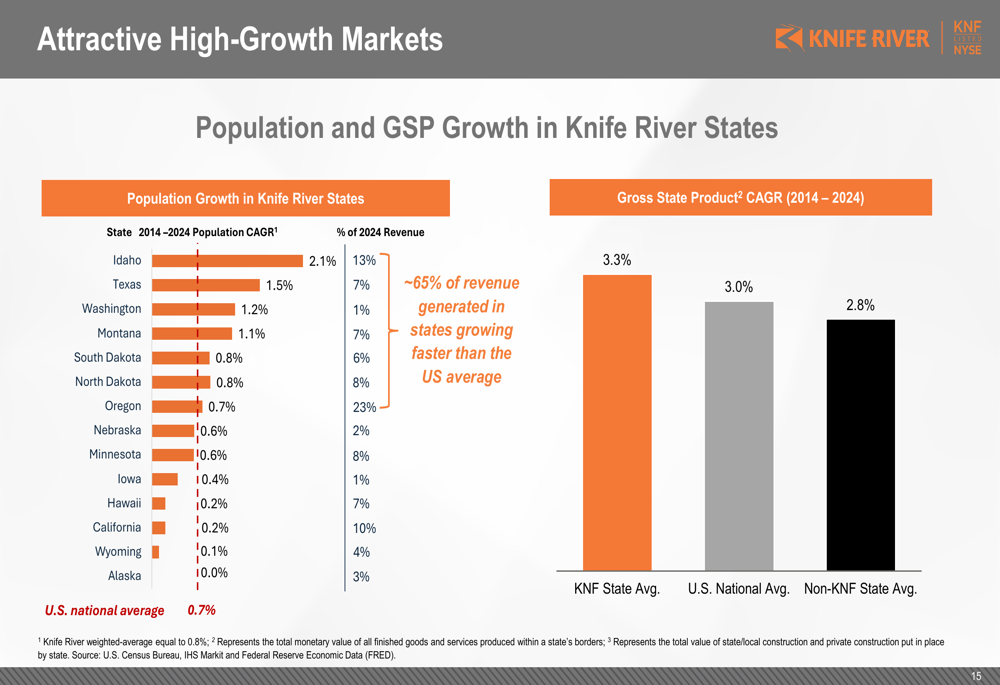

Knife River Corporation (NYSE:KNF) presented its first quarter 2025 results on May 6, highlighting the company’s strategic positioning within a robust infrastructure spending environment despite seasonal challenges. The construction materials and contracting services provider operates in markets with above-average population growth, with its geographic footprint showing a 3.3% gross state product CAGR from 2014-2024, outpacing the U.S. national average of 3.0%.

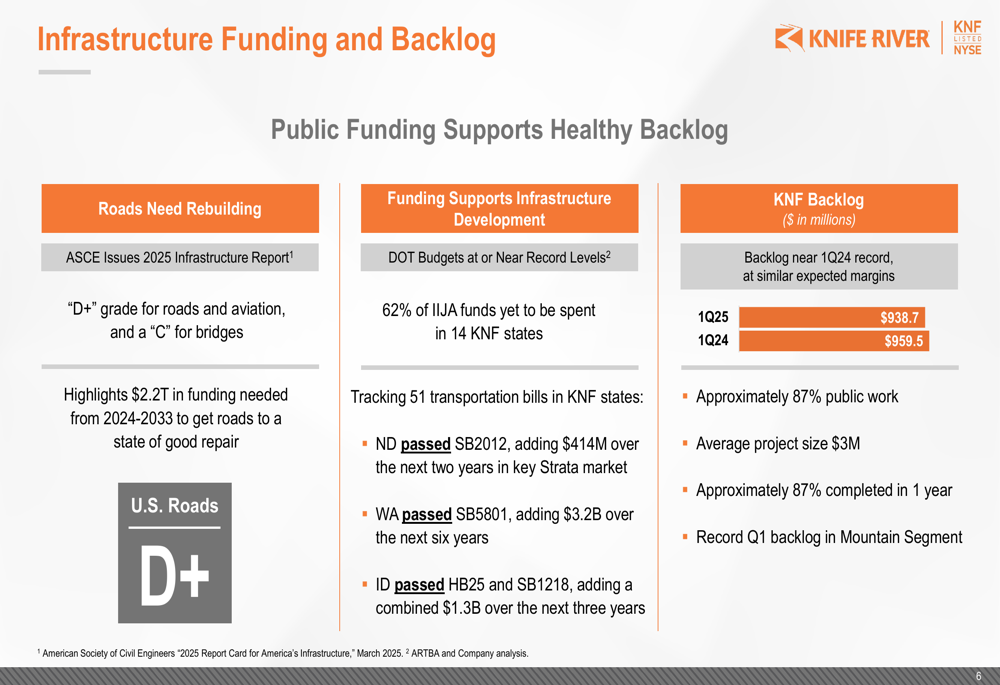

The company emphasized that 62% of Infrastructure Investment and Jobs Act (IIJA) funds are yet to be spent in Knife River’s 14 operating states, providing a substantial runway for future growth. Additionally, the company is tracking 51 transportation bills in its markets, with significant funding already approved in North Dakota ($414 million), Washington ($3.2 billion), and Idaho ($1.3 billion).

As shown in the following map of Knife River’s high-growth markets:

Quarterly Performance Highlights

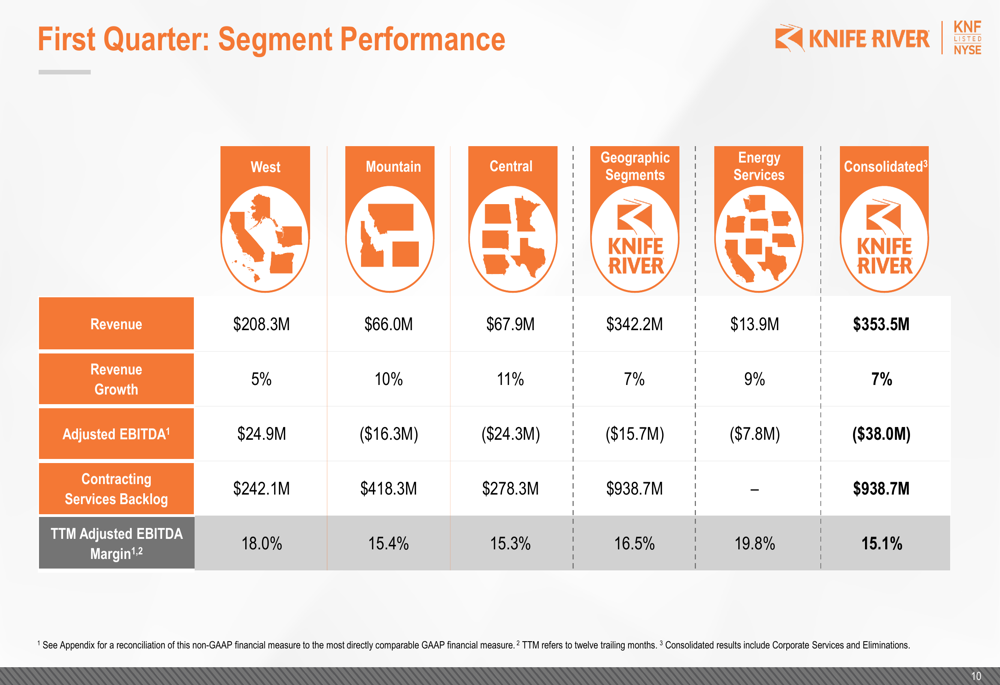

Knife River reported Q1 2025 revenue of $353.5 million, representing a 7% increase from $329.6 million in the same period last year. However, adjusted EBITDA declined to -$38.0 million compared to -$17.7 million in Q1 2024. The company emphasized the seasonal nature of its business, with first-quarter results typically representing negative EBITDA contribution (-8% of annual results) due to weather impacts on construction activity.

The following slide illustrates the company’s first quarter performance metrics across segments:

The company’s backlog remains robust at $938.7 million, nearly matching the record level of $959.5 million from Q1 2024. Approximately 87% of this backlog consists of public infrastructure work, with an average project size of $3 million, providing stability and visibility for the remainder of the year.

The infrastructure funding environment continues to support Knife River’s growth trajectory, as illustrated in this slide:

Strategic Initiatives and Acquisitions

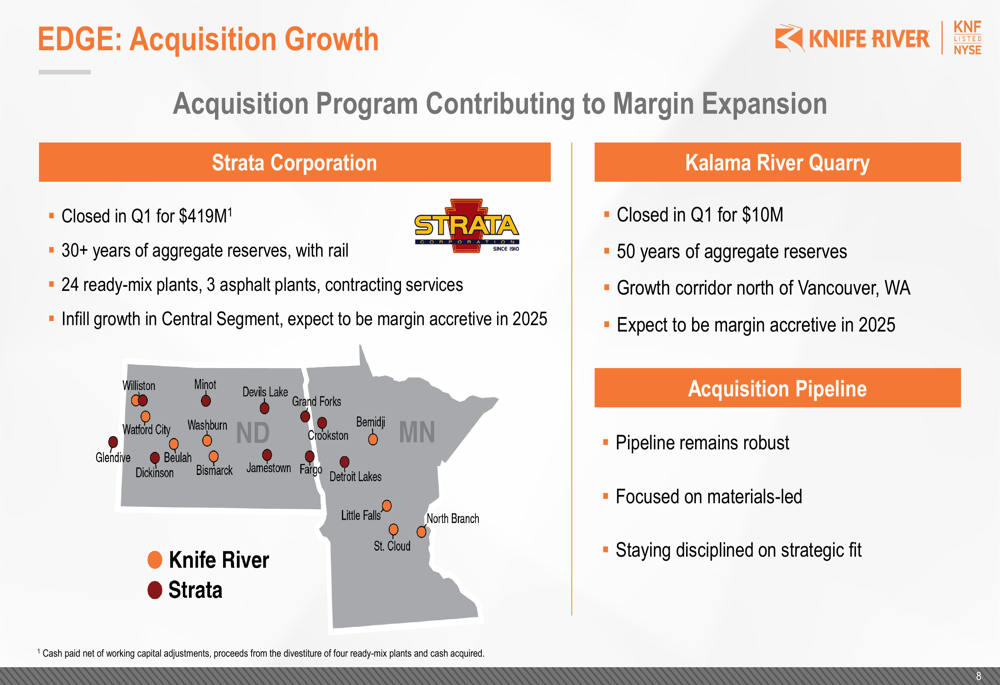

Knife River is executing its "EDGE" strategy (EBITDA Margin Improvement, Discipline, Growth, Excellence) to drive long-term value. A key component of this strategy involves strategic acquisitions, with the company completing two significant transactions in Q1 2025: Strata Corporation for $419 million and Kalama River Quarry for $10 million.

The Strata acquisition provides Knife River with over 30 years of aggregate reserves, 24 ready-mix plants, 3 asphalt plants, and contracting services. The Kalama River Quarry adds 50 years of aggregate reserves in a growth corridor north of Vancouver, Washington. These acquisitions align with the company’s materials-led growth strategy.

The following slide details the company’s recent acquisition activity:

Knife River has also increased its SG&A expenses from $60.2 million in Q1 2024 to $73.1 million in Q1 2025, representing investments in business development and EDGE initiatives. Management characterized this $12.9 million increase as "an investment in our future," with costs front-loaded in the first half of 2025 (approximately $8 million in Q1).

The company’s EDGE strategy framework is illustrated in this comprehensive slide:

Financial Position and Capital Management

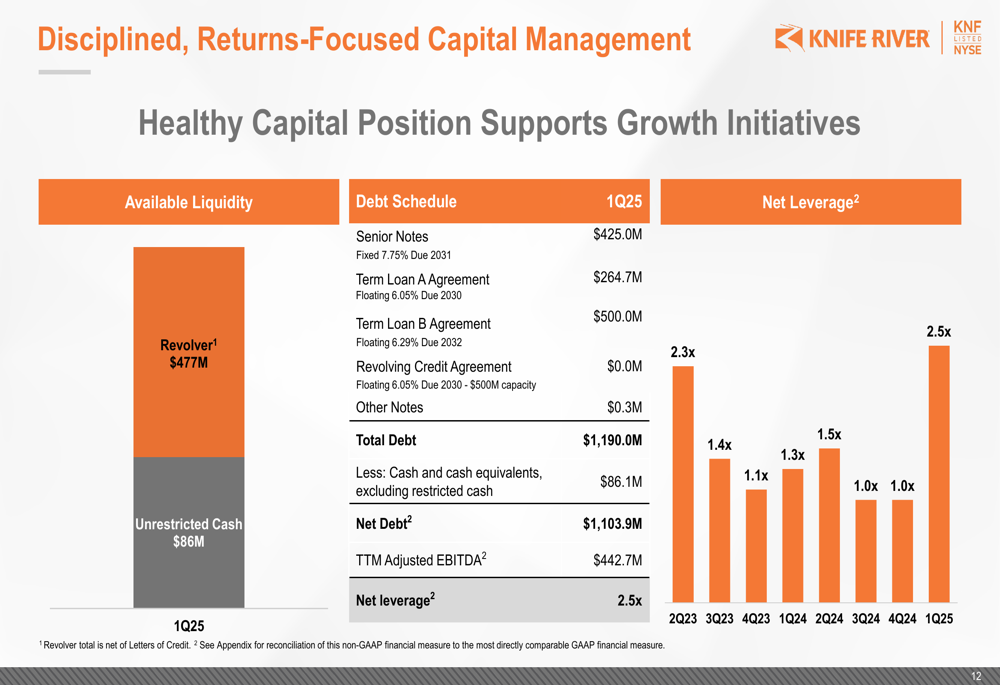

Knife River’s net leverage ratio stood at 2.5x as of March 31, 2025, an increase from 1.3x a year earlier, primarily due to acquisition activity. The company maintains a healthy liquidity position with $477 million available on its revolving credit facility and $86 million in unrestricted cash.

The company’s debt structure includes $425 million in senior notes, a $264.7 million Term Loan A, and a $500 million Term Loan B. Management emphasized its disciplined, returns-focused capital management approach to support both organic growth and strategic acquisitions.

The following slide provides details on the company’s capital position:

Forward Guidance and Outlook

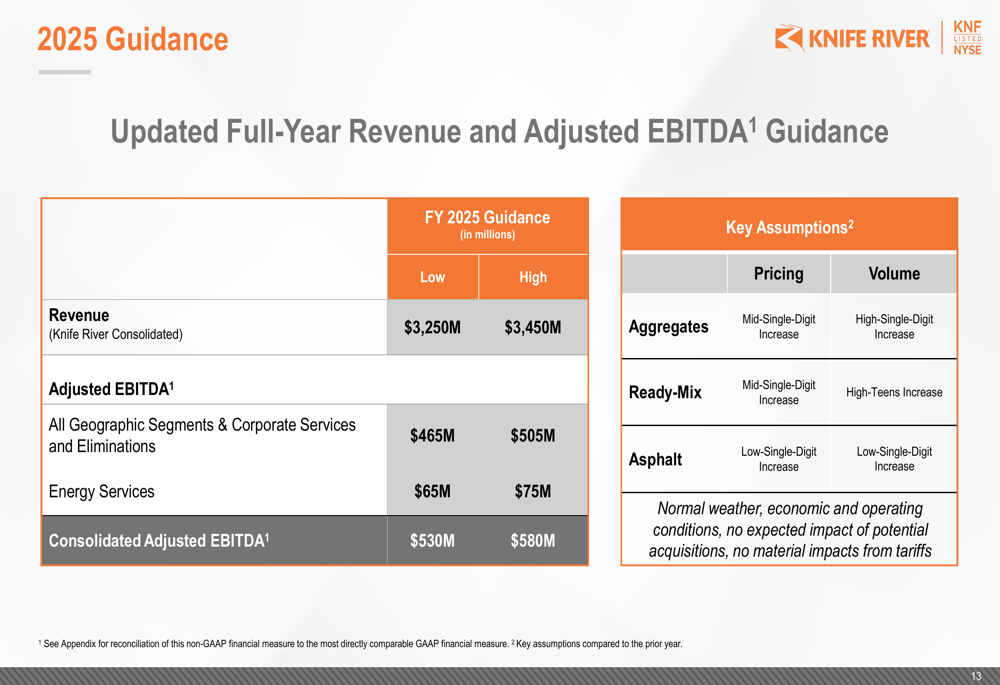

In a significant development, Knife River raised its full-year 2025 guidance, with revenue now expected to range between $3.25 billion and $3.45 billion, up from the previous guidance of $3.0 billion to $3.2 billion. Adjusted EBITDA guidance was also increased to $530 million to $580 million, compared to the previous range of $485 million to $535 million.

The improved outlook reflects the impact of recent acquisitions, strong infrastructure funding, and operational improvements. The company’s PIT Crew initiatives are driving excellence by improving plant production, with throughput improvements at four plants resulting in 30% to 40% average increases in production capacity.

The following slide details the company’s updated 2025 guidance:

Knife River’s first quarter results reflect the highly seasonal nature of its business, with weather conditions significantly impacting construction activity. Management emphasized that the company typically generates 56% of its annual EBITDA in the third quarter, with the first quarter traditionally showing negative results.

Despite the seasonal challenges in Q1, Knife River’s increased full-year guidance, robust backlog, and strategic acquisitions position the company to capitalize on the substantial infrastructure spending environment throughout the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.