Gold rally takes a breather amid Gaza ceasefire, Fed minutes

Shares plunge nearly 20% in premarket trading as company cuts dividend and reports sharp profit decline

Introduction & Market Context

Krispy Kreme Inc. (NASDAQ:DNUT) presented its first quarter 2025 earnings results on May 8, revealing significant financial challenges that sent shares tumbling in premarket trading. The donut chain’s stock fell 19.17% to $3.50 before market open, extending losses that have already pushed the stock to multi-year lows.

The company’s presentation outlined a substantial decline in profitability despite expanding its points of access, prompting management to announce the discontinuation of its dividend program as part of a broader effort to improve financial flexibility and reduce leverage.

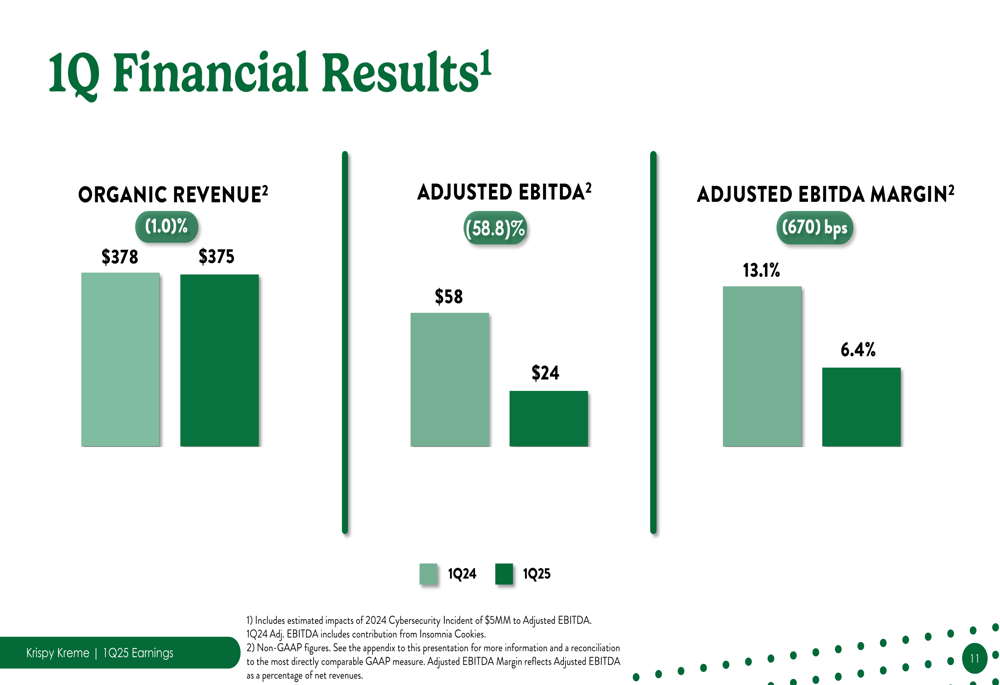

Quarterly Performance Highlights

Krispy Kreme reported disappointing financial results for Q1 2025, with declines across all key metrics. Organic revenue decreased by 1.0% year-over-year to $375 million, while adjusted EBITDA plummeted 58.8% to $24 million. Most concerning was the collapse in adjusted EBITDA margin, which fell 670 basis points to 6.4%.

As shown in the following chart of quarterly financial results:

The company’s adjusted earnings per share turned negative at -$0.05 compared to positive $0.07 in the same quarter last year. This significant deterioration in profitability comes despite continued expansion in points of access across all segments.

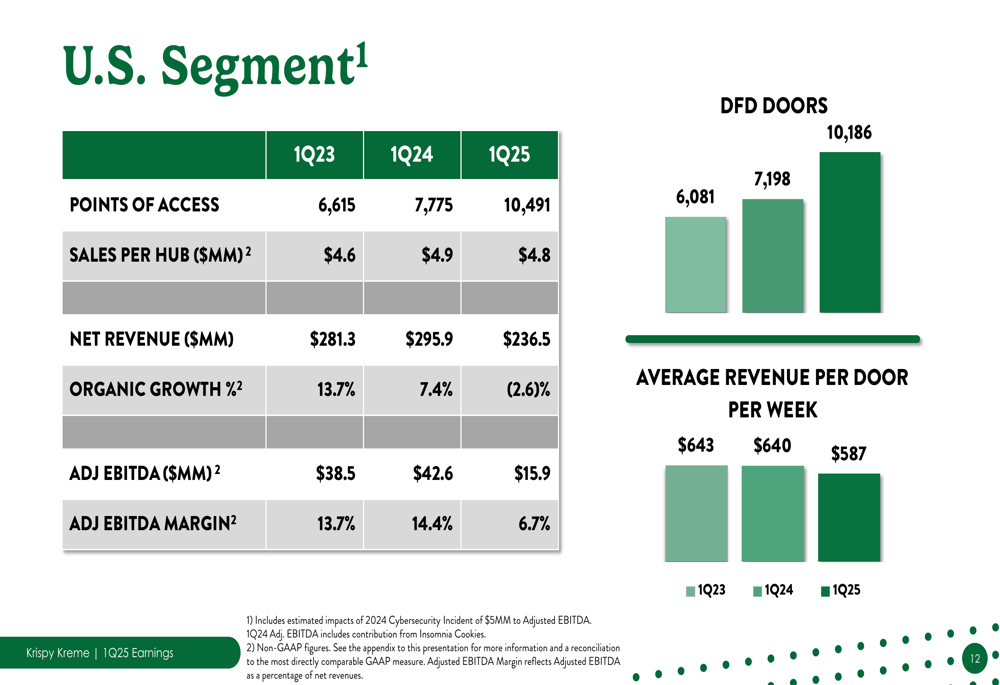

Segment Performance Analysis

The U.S. segment, Krispy Kreme’s largest market, showed particularly troubling results. While points of access increased from 7,775 in Q1 2024 to 10,491 in Q1 2025, organic revenue declined by 2.6%. More alarmingly, adjusted EBITDA for the U.S. segment collapsed from $42.6 million to $15.9 million, with margins shrinking from 14.4% to 6.7%.

The segment breakdown is illustrated in the following chart:

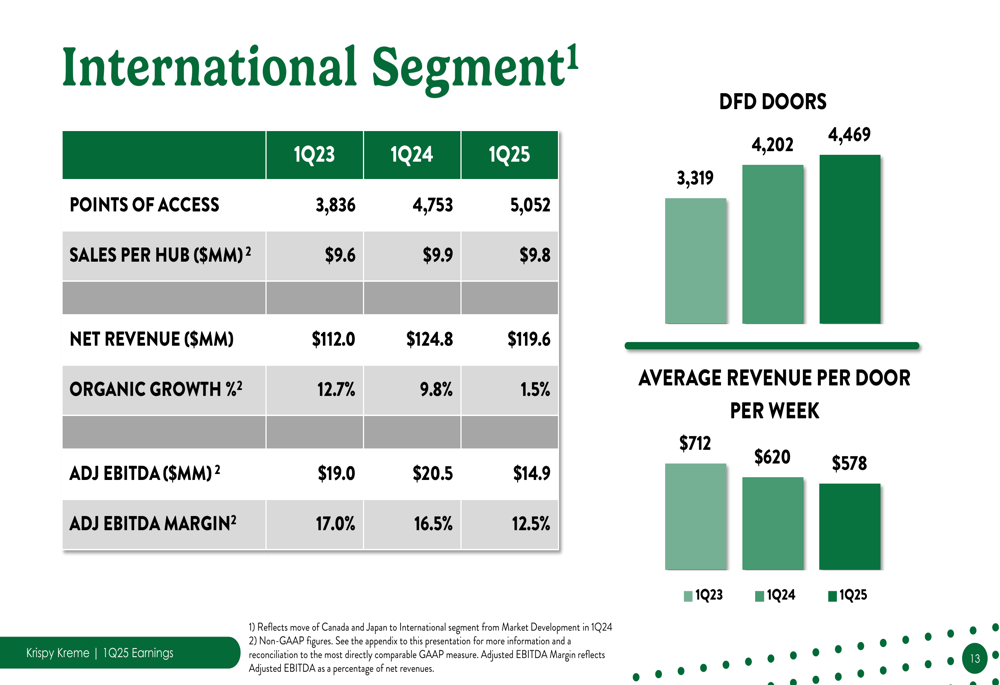

The International segment showed modest organic growth of 1.5%, but also experienced significant profitability challenges. Adjusted EBITDA declined from $20.5 million to $14.9 million, with margins contracting from 16.5% to 12.5%.

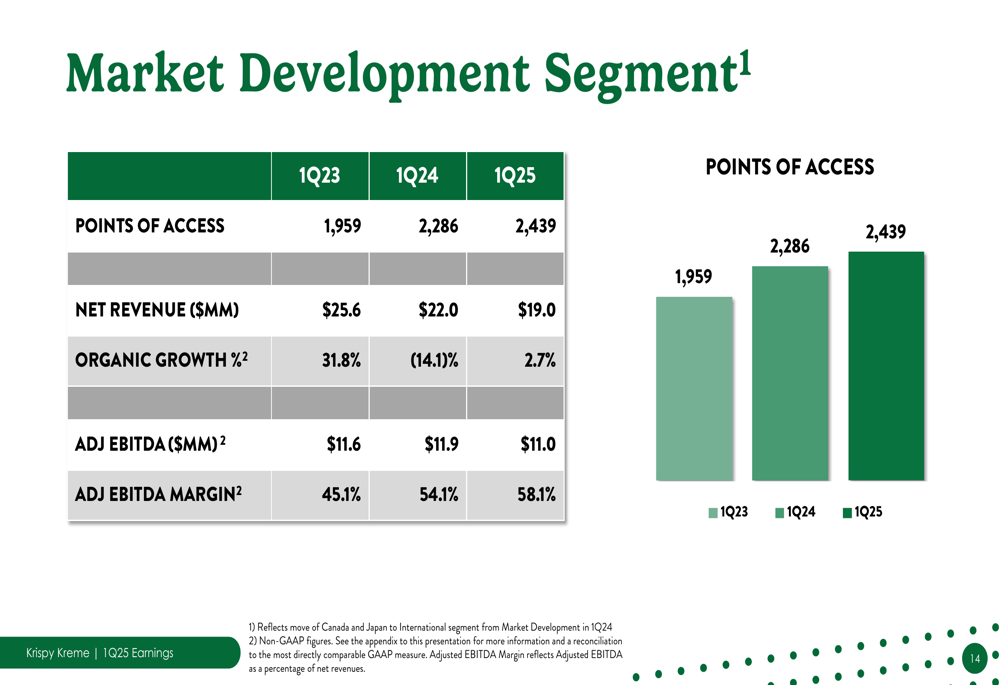

Only the Market Development segment maintained relatively stable performance, with organic growth of 2.7% and an improved adjusted EBITDA margin of 58.1%, up from 54.1% in the prior year.

Strategic Initiatives

In response to these challenges, Krispy Kreme outlined several strategic initiatives aimed at improving financial performance. The company is refocusing on its core offerings, particularly the Original Glazed donut, while expanding availability through national distribution partners.

The strategic priorities for 2025 are outlined in the following slide:

A key component of the strategy involves expanding the company’s points of access through profitable U.S. delivered fresh daily (DFD) growth. The company highlighted its presence across various retail channels, including club stores, mass merchants, grocery stores, convenience stores, and quick-service restaurants.

As illustrated in this expansion strategy slide:

To improve operational efficiency, Krispy Kreme has outsourced U.S. logistics and is working to improve staffing and production planning. The company also highlighted the appointment of a new COO, Nicola Steele, who is focused on simplifying operations, delivering efficiencies, and improving drive-thru performance.

Financial Position and Outlook

Krispy Kreme’s financial position has deteriorated significantly, with the net leverage ratio increasing from 4.2x in Q1 2024 to 6.1x in Q1 2025. Cash flow from operations turned negative at -$20.8 million in Q1 2025 compared to positive $45.8 million for the full fiscal year 2024.

In response to these challenges, the company announced several measures to improve its financial position:

The most significant change is the discontinuation of the dividend program, which management described as necessary to "improve financial flexibility and de-leverage the balance sheet." The company also plans to deploy capital only to the highest-returning investments and pursue quality profitable growth based on sustainable revenue streams.

For Q2 2025, Krispy Kreme provided guidance of $375-385 million in net revenue and $30-35 million in adjusted EBITDA, suggesting some sequential improvement in profitability but still well below historical levels.

These results come after a challenging Q4 2024, when the company missed earnings expectations and was impacted by a cybersecurity incident that reportedly cost approximately $10 million in revenue. The continued deterioration in Q1 2025 suggests the company faces significant structural challenges beyond isolated incidents.

As Krispy Kreme works to implement its turnaround strategy, investors will be closely watching whether the company can stabilize its financial performance and begin to reduce its elevated debt levels. The sharp stock decline indicates significant market skepticism about the company’s near-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.