Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Kyndryl Holdings Inc (NYSE:KD) presented its fourth quarter and full-year fiscal 2025 earnings on May 8, 2025, highlighting its return to revenue growth and substantial margin expansion. The IT services provider, which spun off from IBM (NYSE:IBM) in 2021, has been executing a multi-year transformation strategy focused on expanding higher-margin services while optimizing its legacy business.

Trading at $33.14 as of May 7, 2025, Kyndryl’s stock has shown resilience, trading well above its 52-week low of $21.34 while positioning itself at the intersection of several key technology trends including artificial intelligence, cybersecurity, and cloud migration.

Quarterly Performance Highlights

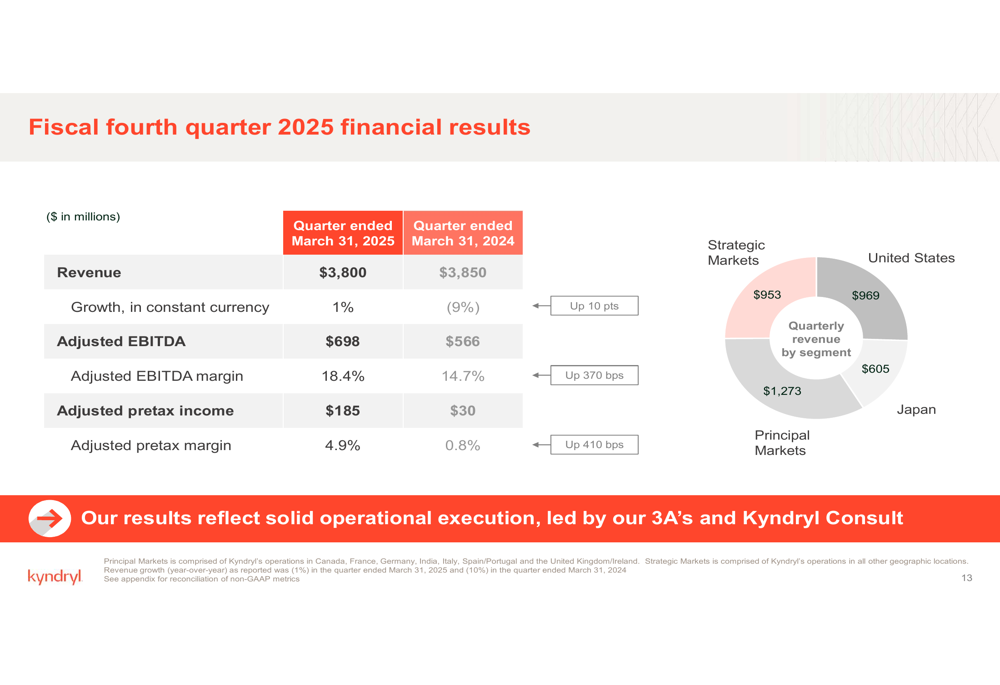

In the fourth quarter of fiscal 2025, Kyndryl achieved a significant milestone by returning to revenue growth. The company reported Q4 revenue of $3.8 billion, representing 1% growth in constant currency compared to a 9% decline in the same period last year.

Profitability metrics showed substantial improvement, with Q4 adjusted EBITDA reaching $698 million (18.4% margin) compared to $566 million (14.7% margin) in Q4 FY24. Adjusted pretax income surged to $185 million (4.9% margin) from $30 million (0.8% margin) in the prior-year quarter.

As shown in the following quarterly financial results:

The company’s revenue is diversified across geographic regions, with the U.S. representing its largest market, followed by principal markets, strategic markets, and Japan.

Full-Year Financial Analysis

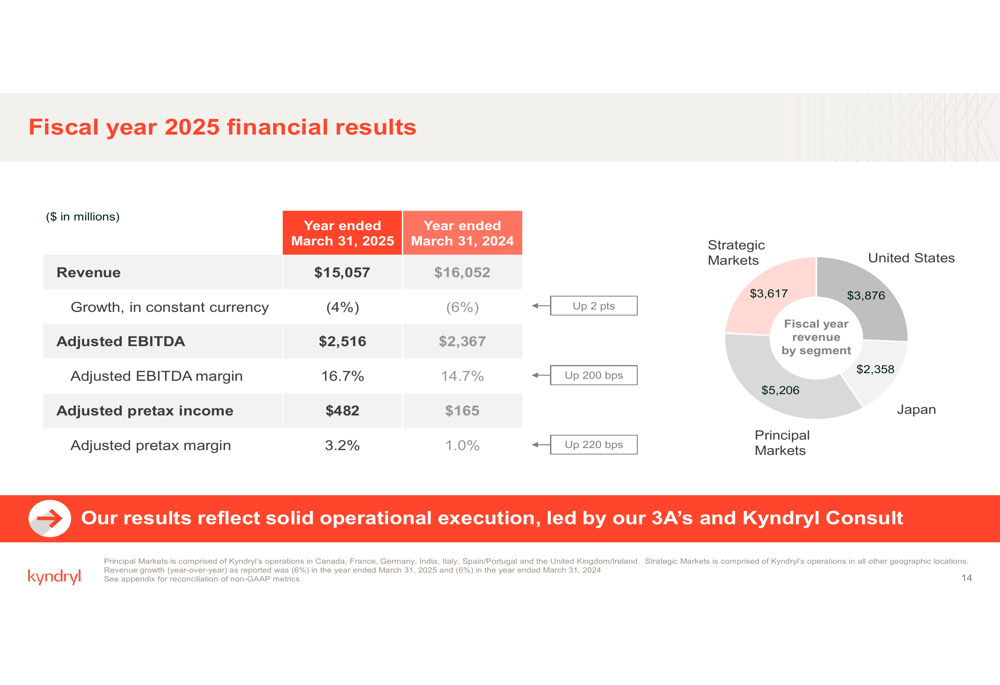

For the full fiscal year 2025, Kyndryl reported revenue of $15.1 billion, representing a 4% decline in constant currency compared to a 6% decline in fiscal 2024. Despite the full-year revenue decline, the company demonstrated significant progress in improving profitability.

Full-year adjusted EBITDA increased to $2.52 billion (16.7% margin) from $2.37 billion (14.7% margin) in fiscal 2024. Adjusted pretax income nearly tripled to $482 million (3.2% margin) from $165 million (1.0% margin) in the prior year.

The company’s full-year financial results are illustrated below:

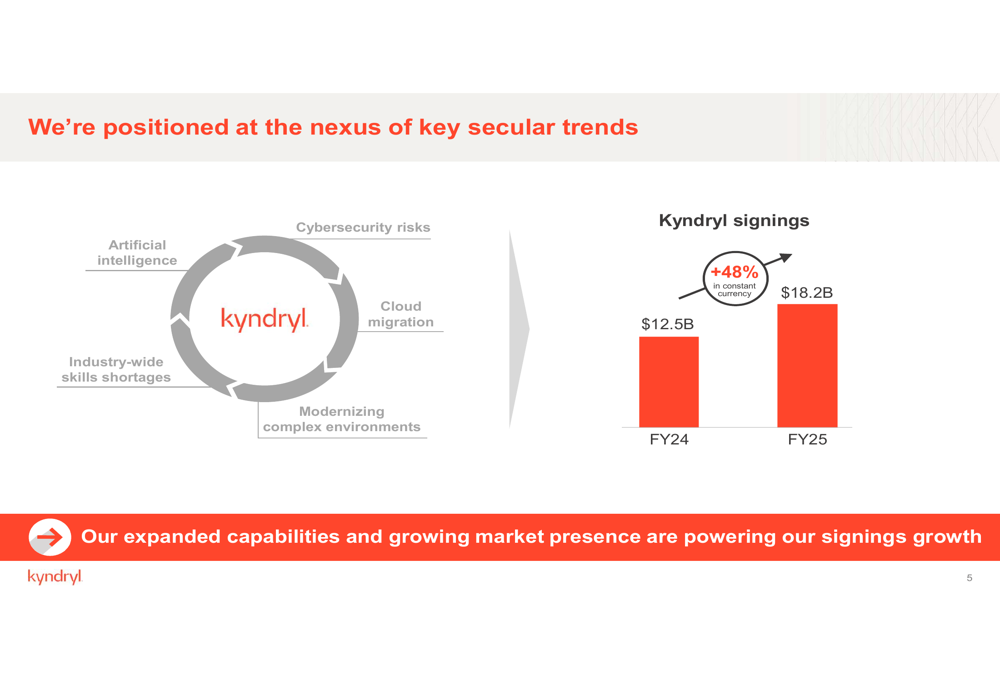

Kyndryl’s signings growth was particularly impressive, reaching $18.2 billion in fiscal 2025, up 48% year-over-year in constant currency. This growth was driven by the company’s positioning at the nexus of several secular technology trends, as shown in the following illustration:

The signings growth was broad-based across geographies and industries, with 55 large contract signings totaling $10 billion across 22 different countries, compared to 40 large signings in fiscal 2024.

Strategic Initiatives

Kyndryl’s strategic initiatives are centered around three key areas, which the company refers to as its "3A’s": Alliances, Advanced Delivery, and Accounts.

In the Alliances category, Kyndryl reported hyperscaler revenue of $1.2 billion, more than double the prior year, reflecting the company’s success in cloud partnerships. Advanced Delivery generated $775 million in annualized savings in Q4, exceeding the fiscal 2025 target. The Accounts initiative delivered $900 million in annualized profit in Q4, also exceeding the fiscal 2025 target.

Kyndryl Consult, the company’s advisory business, has been a particular bright spot, with revenue growing 29% in constant currency to $3.0 billion in fiscal 2025. Signings for this business were up 50% in fiscal 2025.

The company’s projected margins on signings remain strong, with post-spin signings expected to generate 26% gross margin and 9% pretax margin, supporting Kyndryl’s high-single-digit margin target:

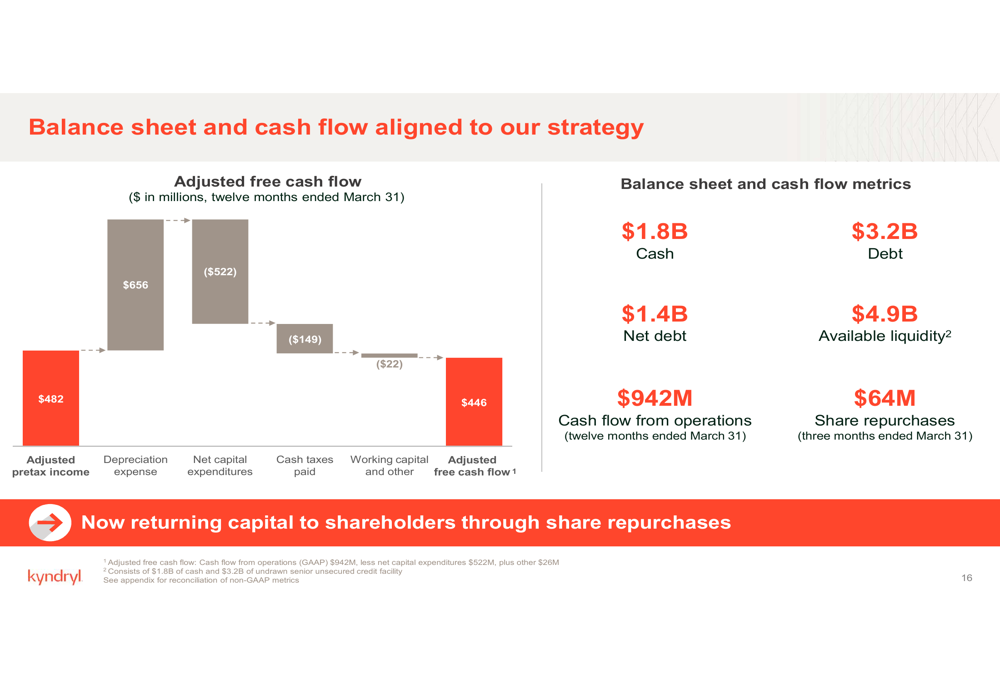

Kyndryl’s balance sheet remains solid, with $1.8 billion in cash, $3.2 billion in debt, and $4.9 billion in available liquidity as of March 31, 2025. The company generated $942 million in cash flow from operations for the twelve months ended March 31, 2025, and reported adjusted free cash flow of $446 million.

The following illustration shows how Kyndryl’s adjusted free cash flow is derived:

Forward-Looking Statements

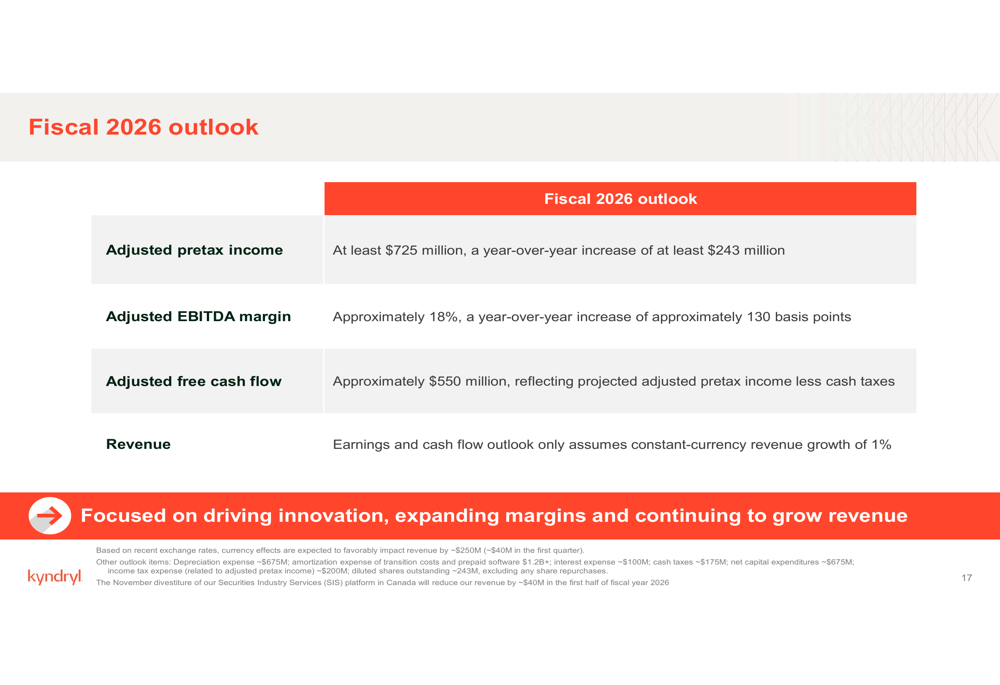

Looking ahead to fiscal 2026, Kyndryl provided an optimistic outlook, projecting adjusted pretax income of at least $725 million, representing a year-over-year increase of at least $243 million. The company expects adjusted EBITDA margin to reach approximately 18%, a year-over-year increase of approximately 130 basis points. Adjusted free cash flow is projected at approximately $550 million.

As illustrated in the company’s fiscal 2026 outlook:

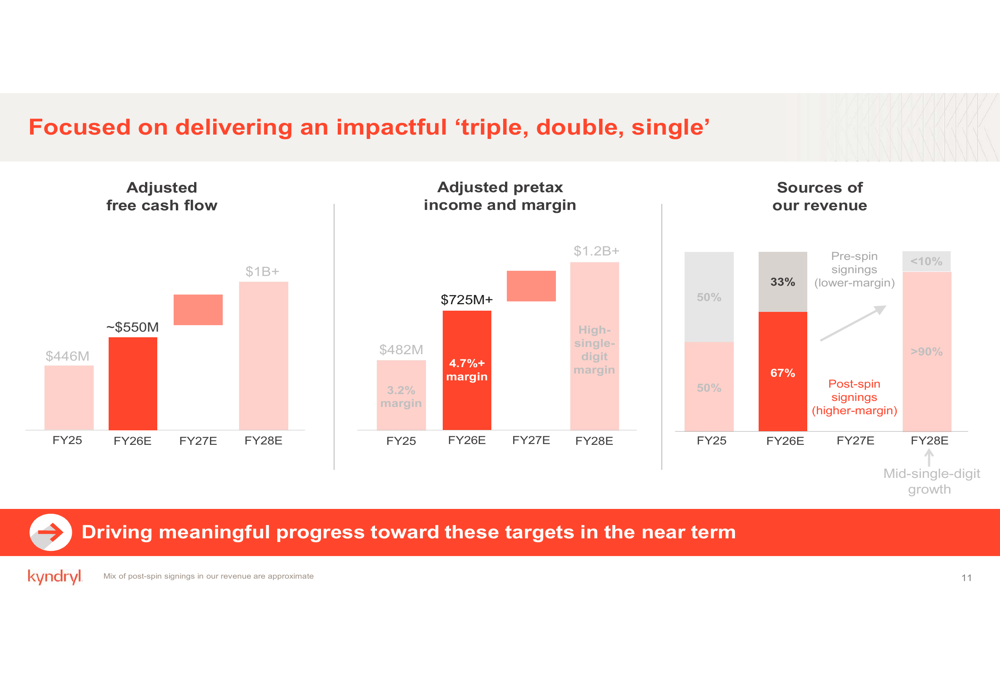

Beyond fiscal 2026, Kyndryl outlined ambitious "triple, double, single" goals through fiscal 2028:

- Triple: Grow adjusted free cash flow from $446 million in FY25 to over $1 billion in FY28

- Double: Increase adjusted pretax income from $482 million in FY25 to over $1.2 billion in FY28

- Single: Achieve mid-single-digit revenue growth

The company expects to achieve these goals through a continued shift from pre-spin signings (lower margin) to post-spin signings (higher margin):

CEO Martin Schroeter emphasized the company’s strong execution in fiscal 2025 and positioned Kyndryl for continued growth by leveraging its expertise in mission-critical enterprise technology services. With its focus on cloud, security, data, and AI services, Kyndryl aims to capitalize on increasing demand while expanding its share of wallet with existing customers and adding new customers.

As Kyndryl enters fiscal 2026, the company appears well-positioned to build on its return to revenue growth while continuing to expand margins and generate increasing cash flow.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.