ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Lamor Corporation Oyj (HEL:LAMOR) released its Q1 2025 interim report presentation on May 8, showing mixed financial results with significant improvement in profitability despite lower revenue. The environmental solutions provider’s stock rose 5.22% to €1.32 following the presentation, reflecting investor optimism about the company’s growing order book and margin expansion.

The company operates in a market characterized by increasing environmental awareness and stricter regulations. According to Lamor’s assessment, geopolitical risks continue to materialize, fueling demand especially for environmental protection services, while governments and corporations are increasingly focusing on remediating past contamination and improving waste management systems.

As shown in the following image highlighting market trends:

Quarterly Performance Highlights

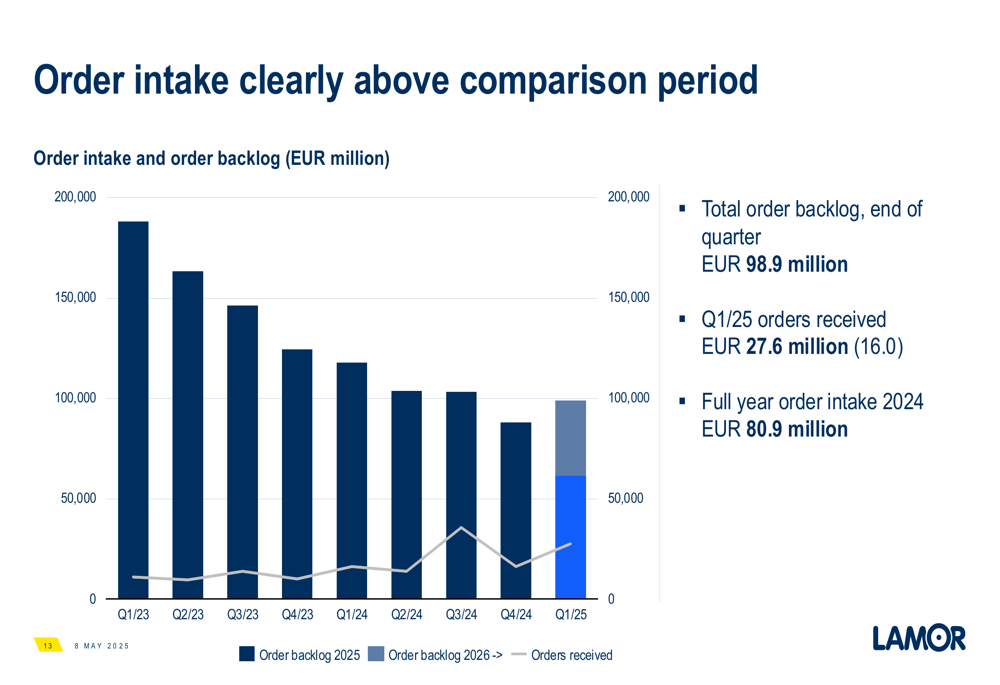

Lamor reported a substantial increase in new orders, which reached €27.6 million in Q1 2025, up from €16.0 million in the same period last year, representing a 72.5% increase. Notable new business included an €8 million order from Kuwait and a €5 million order from Italy. However, revenue decreased to €19.0 million from €23.9 million in Q1 2024.

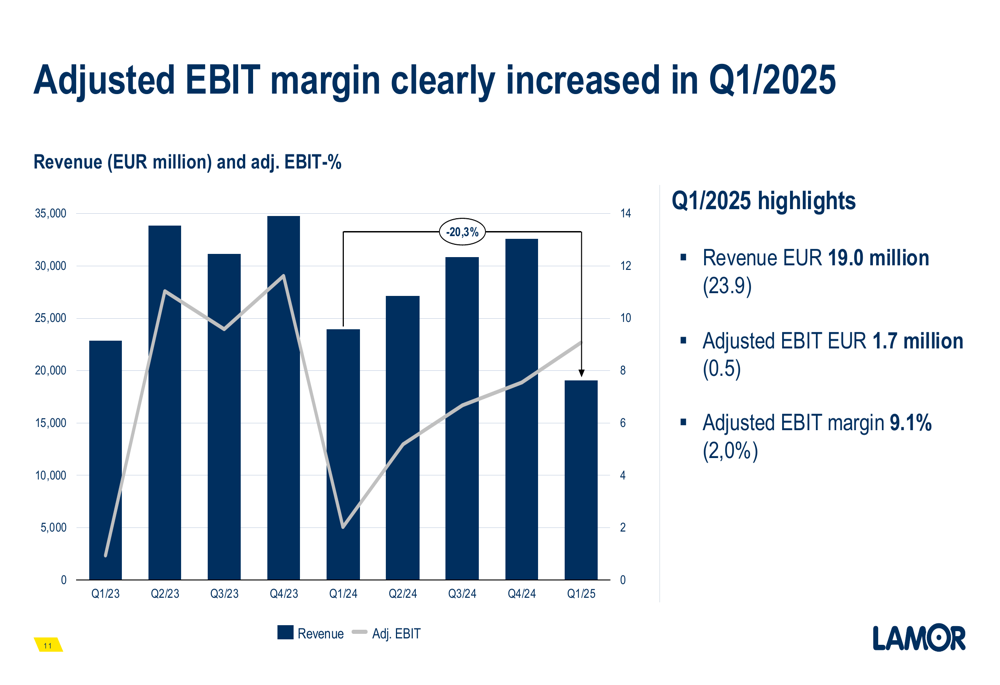

Despite the revenue decline, profitability improved significantly, with adjusted operating profit more than tripling to €1.7 million compared to €0.5 million in the previous year. This resulted in an adjusted EBIT margin of 9.1%, up from 2.0% in Q1 2024, demonstrating the company’s focus on operational efficiency.

The following chart illustrates the company’s improved profitability despite lower revenue:

The order backlog remained strong at €98.9 million at the end of Q1, providing visibility for future revenue. The following chart shows the positive trend in order intake:

Detailed Financial Analysis

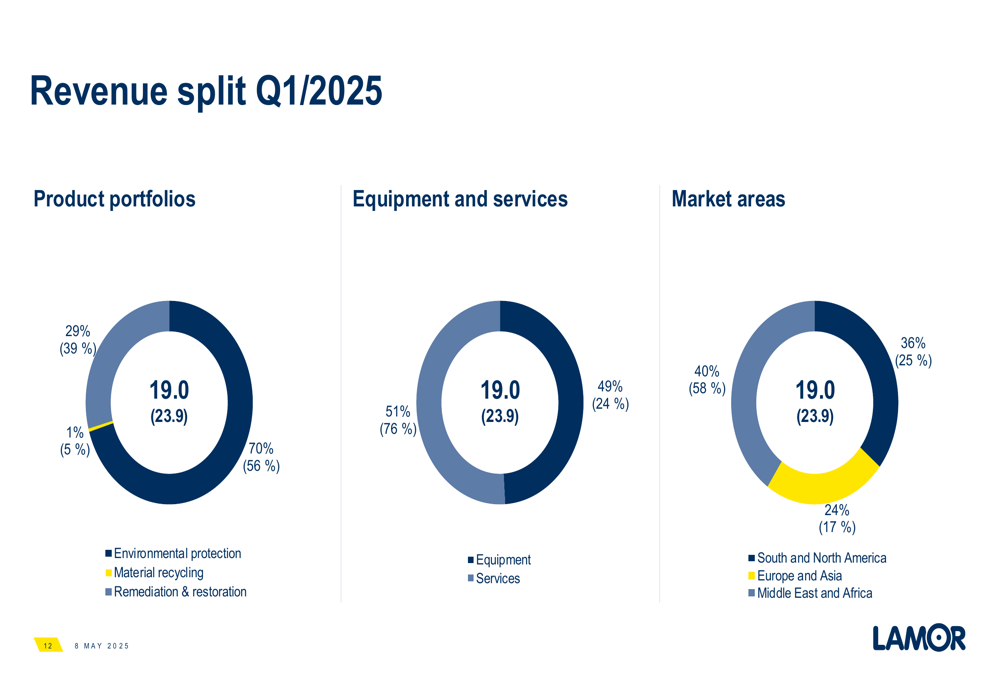

Lamor’s revenue mix shifted significantly in Q1 2025 compared to the same period last year. The remediation and restoration segment accounted for 70% of revenue (up from 56%), while environmental protection decreased to 29% (from 39%) and material recycling fell to 1% (from 5%).

The company also saw a substantial shift in its equipment versus services revenue split, with services increasing to 49% of total revenue compared to just 24% in Q1 2024. This transition toward a more service-oriented business model potentially offers more stable and recurring revenue streams.

The revenue distribution across different market areas also evolved, with Europe and Asia increasing to 36% (from 25%) and Middle East and Africa growing to 24% (from 17%), while South and North America decreased to 40% (from 58%).

As illustrated in the following revenue breakdown:

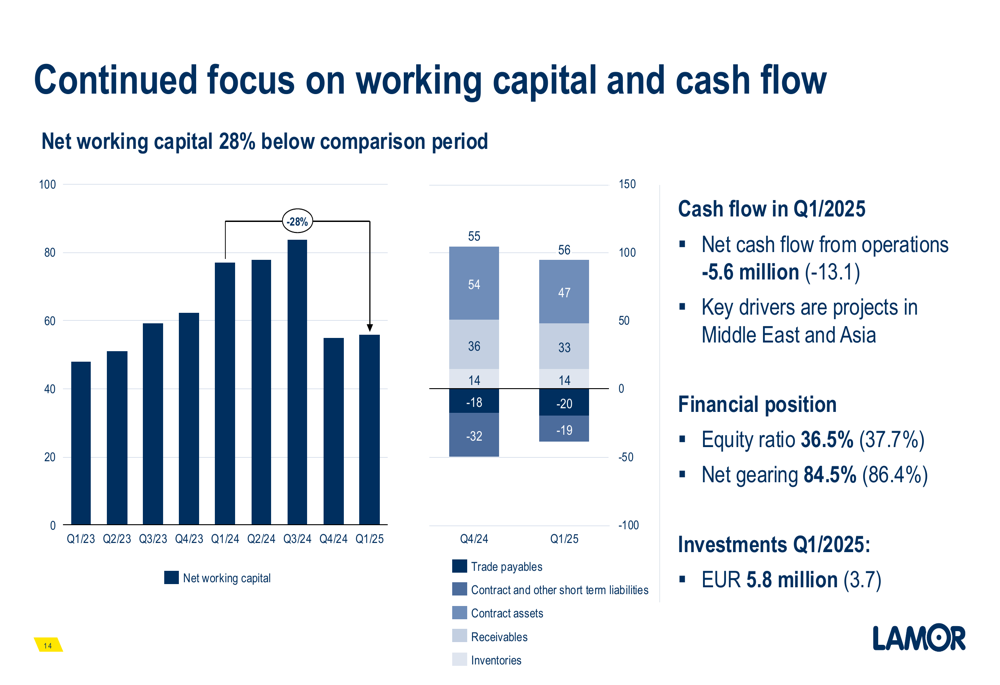

Working capital management improved, with net working capital 28% below the comparison period. However, cash flow from operations remained negative at -€5.6 million, though this represented an improvement from -€13.1 million in Q1 2024. The company maintained a stable financial position with an equity ratio of 36.5% (37.7% in Q1 2024) and net gearing of 84.5% (86.4% in Q1 2024).

The following chart shows the working capital trend:

Strategic Initiatives

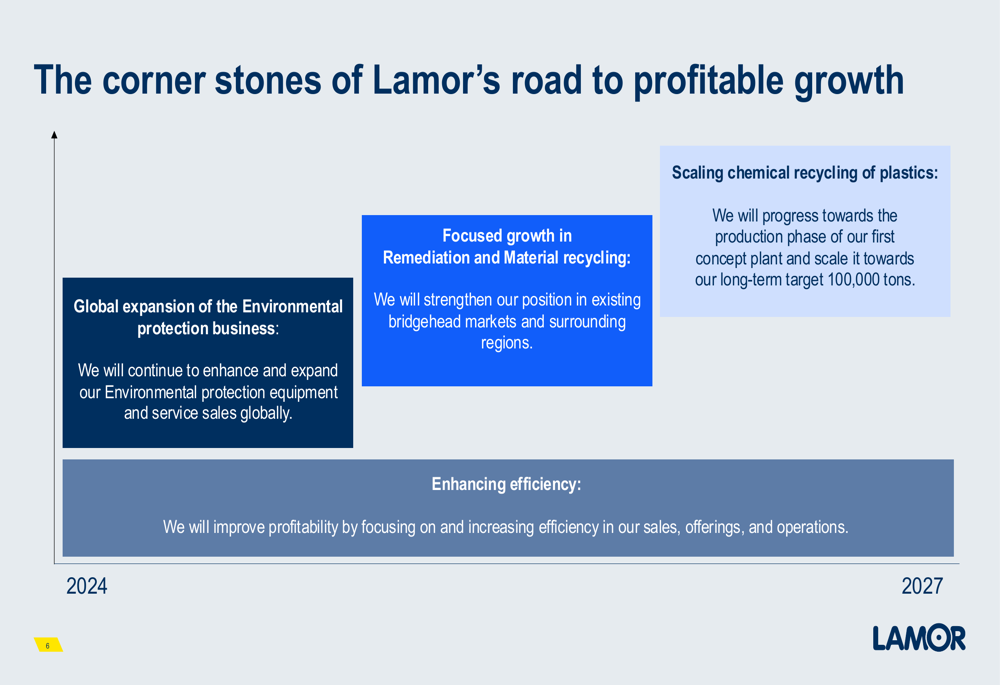

Lamor outlined several strategic initiatives aimed at driving future growth. A key development is the establishment of a new regional service center in Saudi Arabia, which will improve service delivery to Saudi customers and allow the company to supply locally manufactured oil spill response equipment. This aligns with Lamor’s strategy of strengthening its position in existing bridgehead markets.

As shown in the following strategic expansion plan:

The company is also making progress on its Kilpilahti plastic recycling plant, with production expected to commence in Q3 2025. The facility represents a significant step in Lamor’s ambition to scale chemical recycling of plastics, with a long-term target of achieving 100,000 tons of recycling capacity.

This initiative follows the timeline presented in the company’s Q4 2024 earnings call, where management emphasized the strategic importance of the circular oil project and noted high market demand for the product.

Forward-Looking Statements

Lamor maintained its guidance for 2025, expecting both revenue and adjusted operating profit to increase compared to 2024 levels (€114.4 million and €6.4 million, respectively). This guidance appears more conservative than the €170 million revenue and 14% profitability targets mentioned in the Q4 2024 earnings call.

For the first half of 2025, the company identified three key focus areas: completing and winning targeted tenders to maintain strong order intake; improving profitability and cash flow through cost awareness and operational efficiency; and finalizing preparations for circular oil production scheduled to begin in Q3 2025.

The company’s roadmap to profitable growth is illustrated in the following strategic framework:

While Lamor faces market uncertainty and volatility, management remains confident in the company’s ability to capitalize on increasing environmental awareness and regulatory requirements. The significant improvement in profitability and strong order intake in Q1 2025 provide a solid foundation for the company’s growth trajectory, despite the temporary revenue decline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.