U.S. stocks edge higher after weekly jobless claims; Salesforce gains

Introduction & Market Context

Lamor Corporation Oyj (HEL:LAMOR) presented its Q2 2025 interim results on July 31, 2025, revealing a mixed financial performance. The environmental protection and recovery company saw its stock decline by 5.71% to €1.32 during the trading session, despite some positive developments in its business fundamentals.

The company’s presentation highlighted a challenging global economic environment with continued volatility affecting customer decision-making, particularly for larger service projects. Despite these headwinds, Lamor emphasized that market demand for environmental protection technologies remains strong, with the company securing several significant equipment orders during the quarter.

Quarterly Performance Highlights

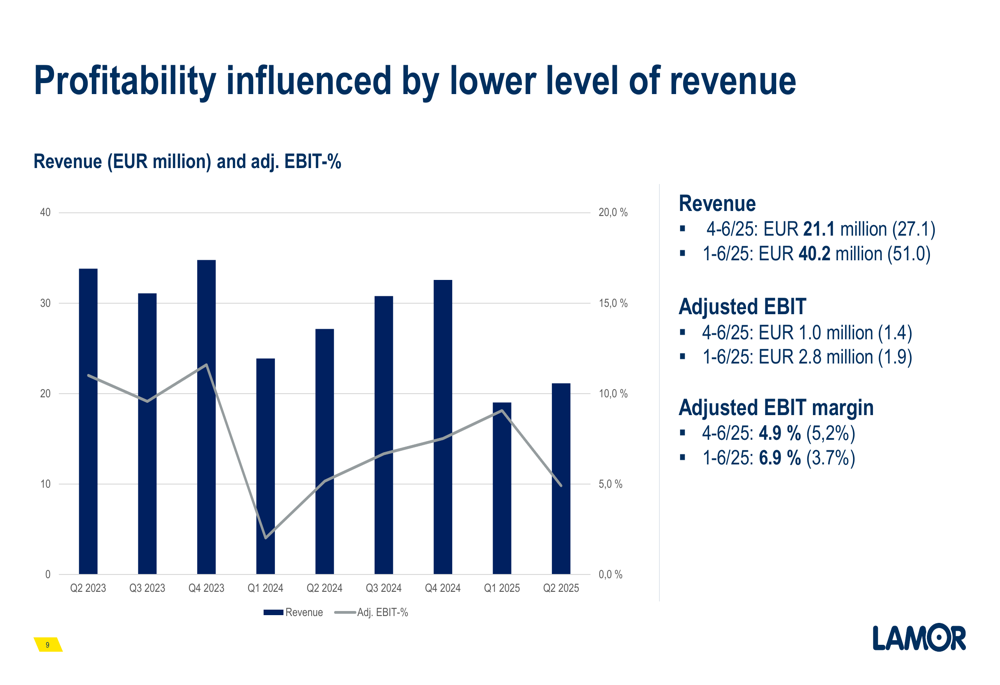

Lamor reported Q2 2025 revenue of €21.1 million, down from €27.1 million in the same period last year. This 22% decline was primarily attributed to the completion of the NCEC project, which significantly contributed to the comparison period, as well as lower revenue recognition from the Kuwait project.

Despite the revenue decline, the company maintained relatively stable profitability with an adjusted operating profit of €1.0 million in Q2 2025, compared to €1.4 million in Q2 2024. The adjusted EBIT margin stood at 4.9%, slightly below the 5.2% recorded in the comparison period.

As shown in the following chart of quarterly revenue and adjusted EBIT trends:

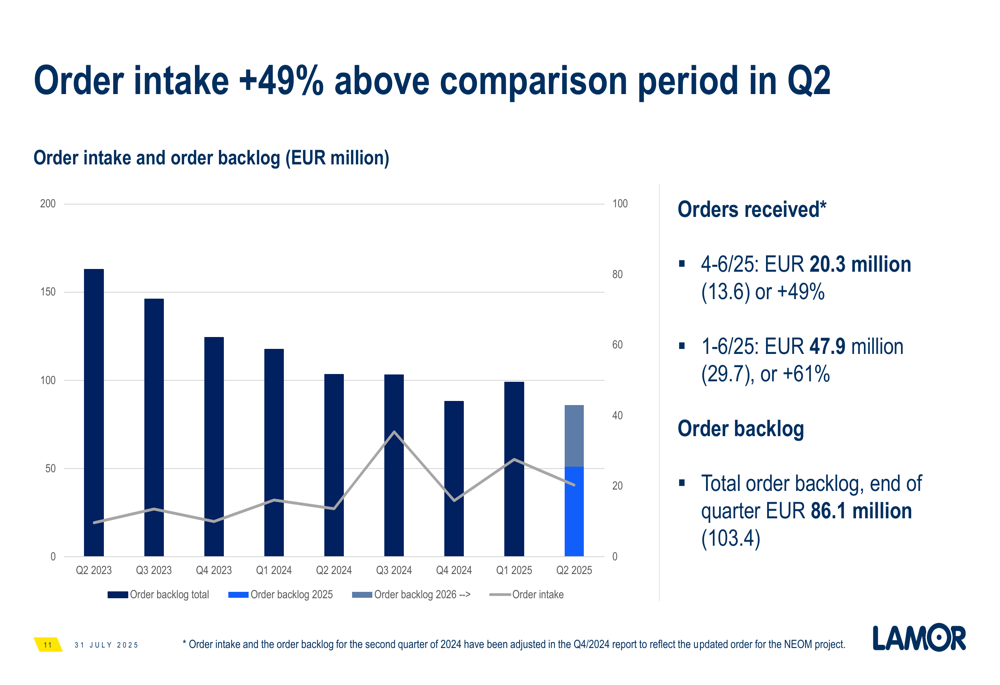

A particularly encouraging development was the 49% increase in order intake, which reached €20.3 million in Q2 2025 compared to €13.6 million in Q2 2024. For the first half of 2025, order intake grew by an impressive 61% to €47.9 million. This strong order intake suggests potential revenue growth in upcoming quarters, despite the current period’s decline.

The order backlog and intake development is illustrated in this chart:

Detailed Financial Analysis

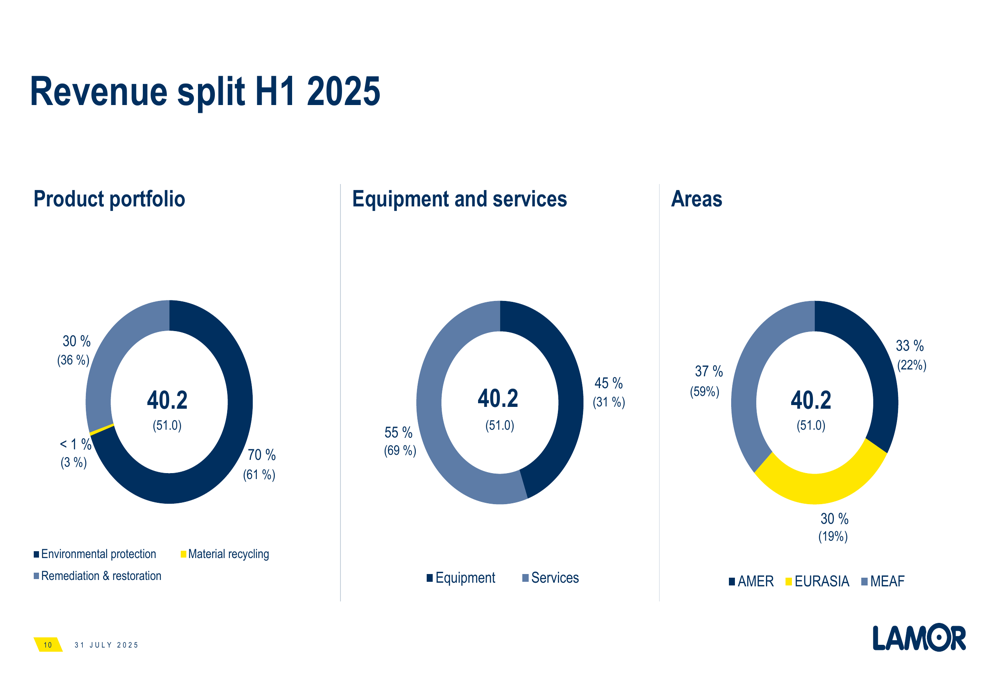

For the first half of 2025, Lamor’s revenue totaled €40.2 million, down from €51.0 million in H1 2024. However, H1 2025 adjusted operating profit improved to €2.8 million (6.9% margin) from €1.9 million (3.7% margin) in the comparison period, demonstrating enhanced operational efficiency despite lower revenue.

The company’s revenue breakdown shows a shift in business mix, with remediation and restoration services growing in importance:

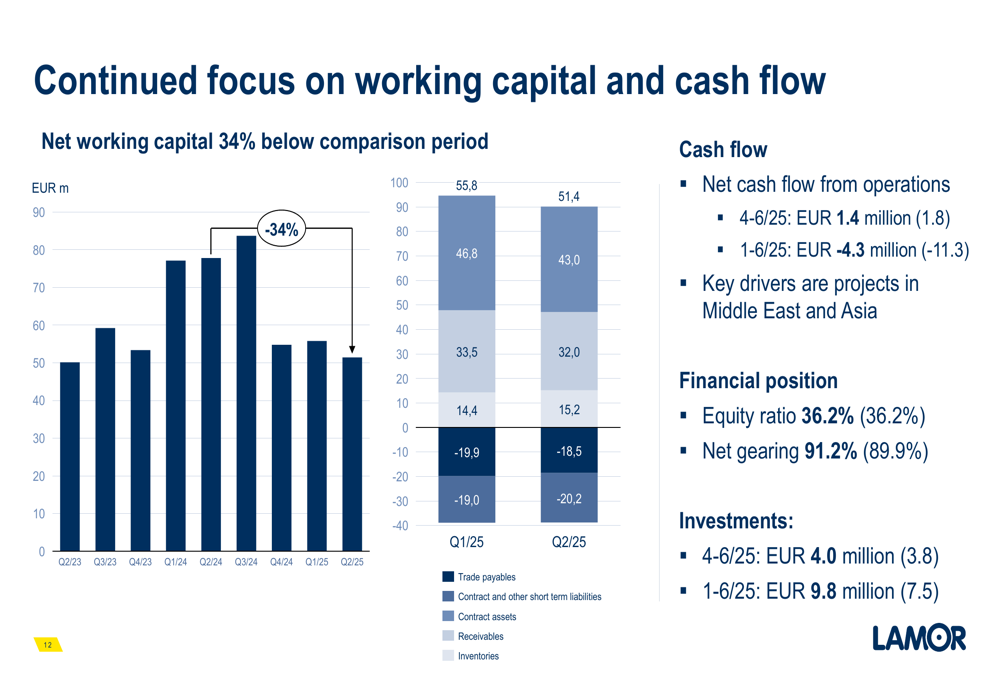

Lamor’s financial position remained relatively stable with an equity ratio of 36.2% (unchanged from the comparison period) and net gearing at 91.2% (slightly up from 89.9%). The high gearing ratio represents a potential financial risk, as also noted in the earnings call where management acknowledged being close to covenant limits but not breaking them.

The company has maintained focus on working capital management and cash flow optimization, with net working capital 34% below the comparison period. Net cash flow from operations for Q2 2025 was €1.4 million, slightly down from €1.8 million in Q2 2024, while H1 2025 saw a significant improvement to -€4.3 million from -€11.3 million in H1 2024.

Strategic Initiatives

Lamor highlighted several strategic developments during the quarter, including strengthening its presence in the Middle East with a Saudi Service Center and making progress with its agent network, resulting in the largest African order ever received from Angola (€2 million).

The company also reported strategic wins in soil remediation, securing its first remediation project in Europe and a feasibility study project in Peru. These developments align with Lamor’s strategy to expand its environmental services portfolio beyond its traditional oil spill response equipment business.

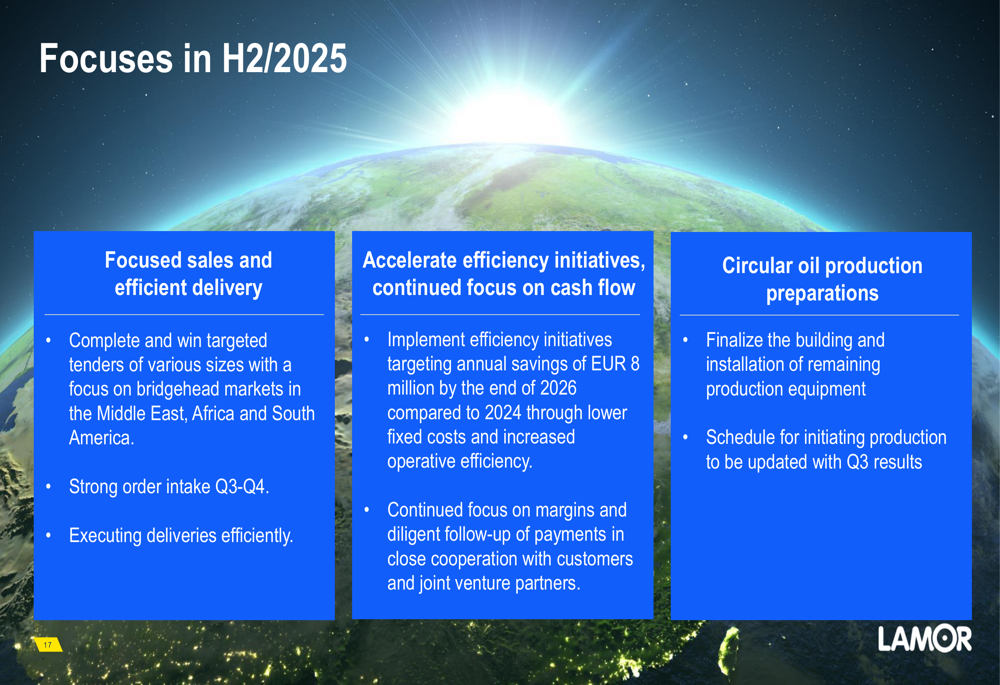

A key announcement was the acceleration of Lamor’s efficiency program, which targets €8 million in annual savings by the end of 2026 compared to 2024 levels. These savings will be achieved through lower fixed costs and increased operational efficiency.

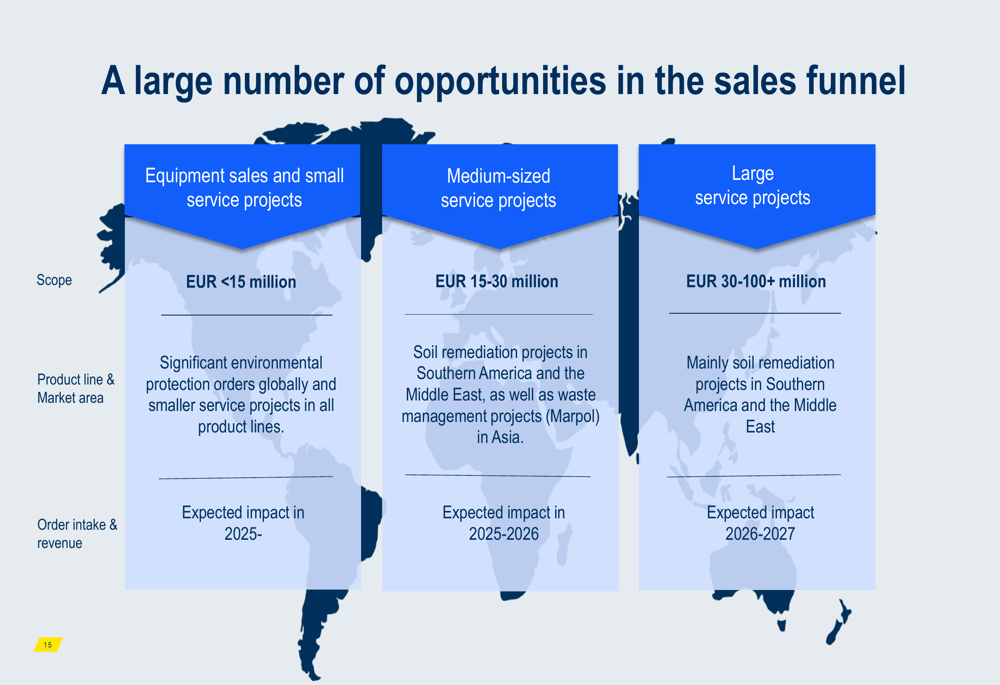

The company’s sales pipeline remains robust, with opportunities across different project sizes and geographies:

Forward-Looking Statements

Lamor maintained its guidance for 2025, expecting revenue and adjusted operating profit to increase compared to 2024 (€114.4 million and €6.4 million, respectively). However, the company noted that revenue is expected to be below the comparison period in Q3 2025 before exceeding it in Q4 2025.

Management emphasized that achieving the revenue guidance requires strong order intake in Q3 2025. The company is currently negotiating several significant equipment sales and medium-sized service contracts across all market areas.

For the second half of 2025, Lamor outlined three key focus areas: focused sales and efficient delivery, accelerated efficiency initiatives with continued focus on cash flow, and preparations for circular oil production.

The company’s ability to convert its strong order intake into revenue while successfully implementing its efficiency program will be crucial for meeting its full-year guidance and improving its financial position. While market demand for environmental protection remains strong, Lamor continues to navigate a volatile global economic environment with cautious optimism.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.