German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

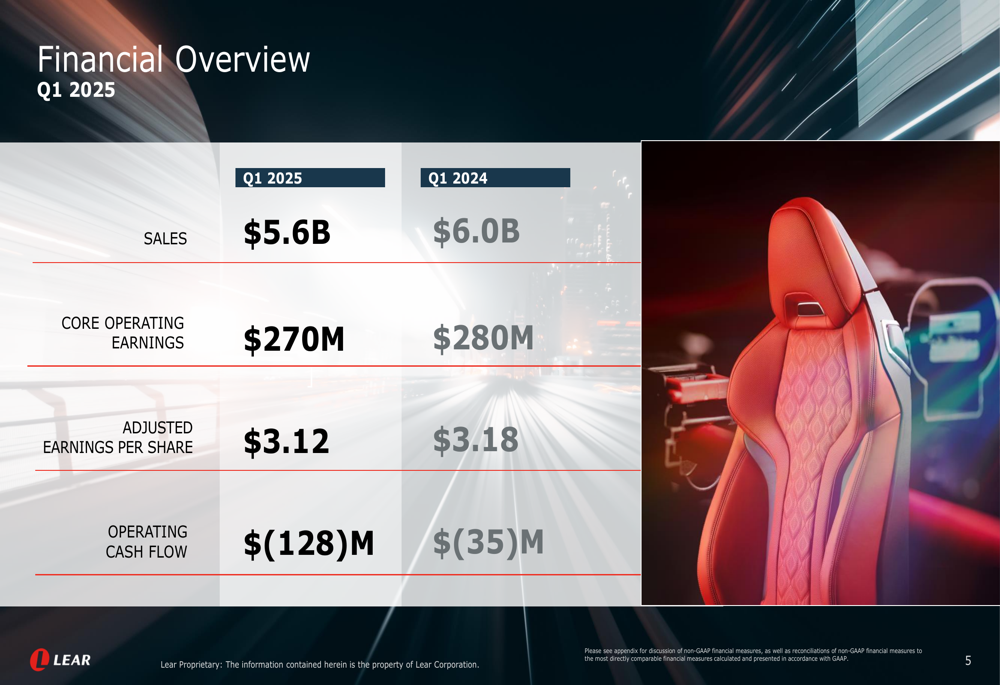

Lear Corporation (NYSE:LEA), a global automotive technology leader in seating and electrical systems, reported its first quarter 2025 financial results on May 6, 2025, revealing revenue declines amid challenging market conditions while maintaining slight margin improvements. The company also announced the withdrawal of its full-year 2025 outlook, citing uncertainties in light vehicle production and ongoing global trade policy negotiations.

The automotive supplier reported Q1 2025 sales of $5.6 billion, down 6.7% from $6.0 billion in the same period last year, while core operating earnings decreased 3.6% to $270 million. Despite these declines, Lear managed to improve operating margins in both its Seating and E-Systems segments.

As shown in the following financial overview, Lear’s performance reflected broader industry challenges:

Quarterly Performance Highlights

Lear’s adjusted earnings per share reached $3.12 in Q1 2025, a slight decrease from $3.18 in Q1 2024. Operating cash flow deteriorated significantly to negative $128 million compared to negative $35 million in the prior year period. The company’s global performance was influenced by regional variations in vehicle production, with global production up 1% year-over-year, but North America down 5% and Europe/Africa down 7%, while China showed strong growth of 12%.

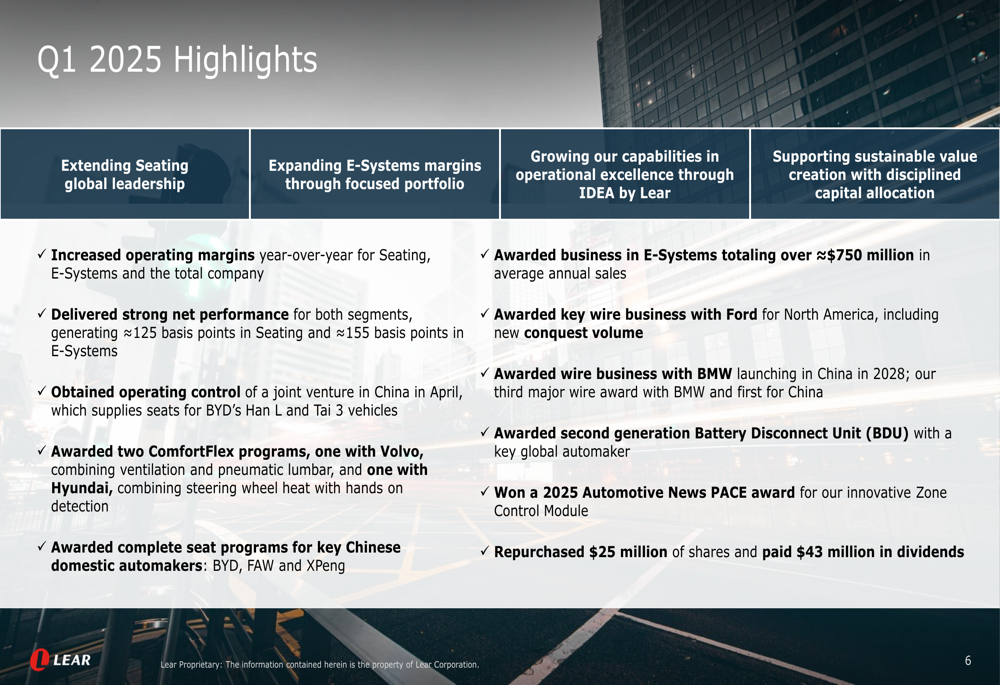

Despite these challenges, Lear highlighted several positive developments in the quarter, including increased operating margins year-over-year across both business segments, strong net performance generating approximately 125 basis points in Seating and 155 basis points in E-Systems, and new business awards in E-Systems totaling over $750 million in average annual sales.

The company’s key achievements and strategic initiatives are summarized in the following slide:

Detailed Financial Analysis

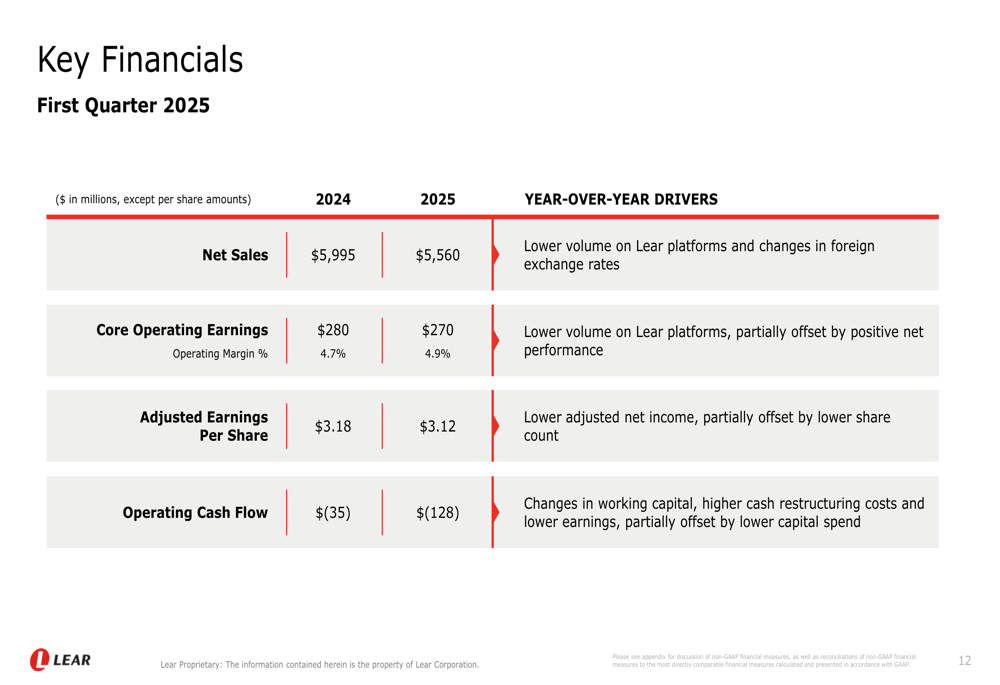

Lear’s financial performance showed mixed results across key metrics. While sales and earnings declined year-over-year, the company maintained relatively stable margins through cost control measures and operational improvements.

The following table provides a comprehensive overview of Lear’s key financial metrics for Q1 2025:

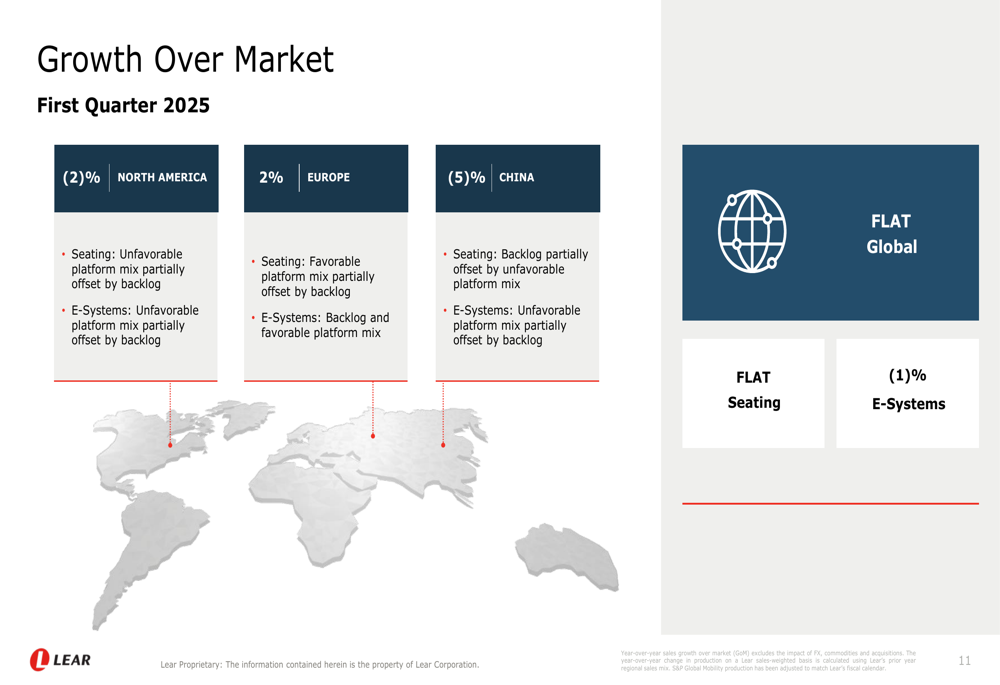

In terms of market performance, Lear’s growth relative to the overall market varied by region. The company reported flat global growth over market, with 2% outperformance in Europe offset by underperformance in North America (-2%) and China (-5%). This regional performance is illustrated in the following growth over market slide:

Segment Analysis

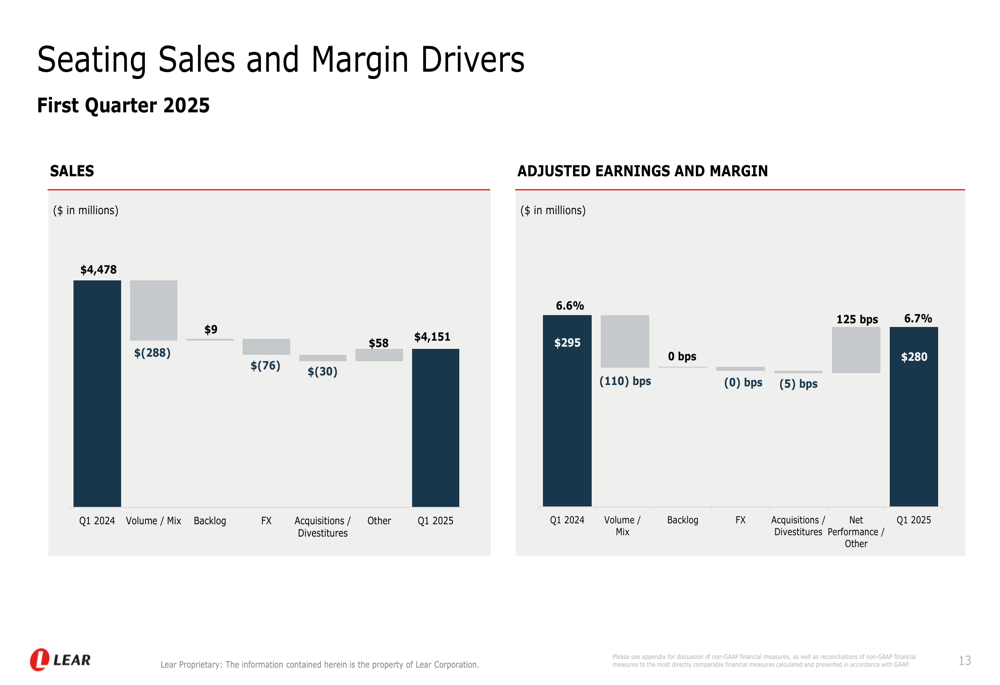

Lear’s Seating segment, which represents approximately 75% of total revenue, reported sales of $4.15 billion in Q1 2025, down from $4.48 billion in Q1 2024. Despite the revenue decline, the segment’s adjusted margin improved slightly to 6.7% from 6.6% in the prior year period. This improvement was primarily driven by strong net performance, which contributed approximately 125 basis points to the margin, offsetting negative impacts from volume/mix.

The following chart details the drivers behind the Seating segment’s performance:

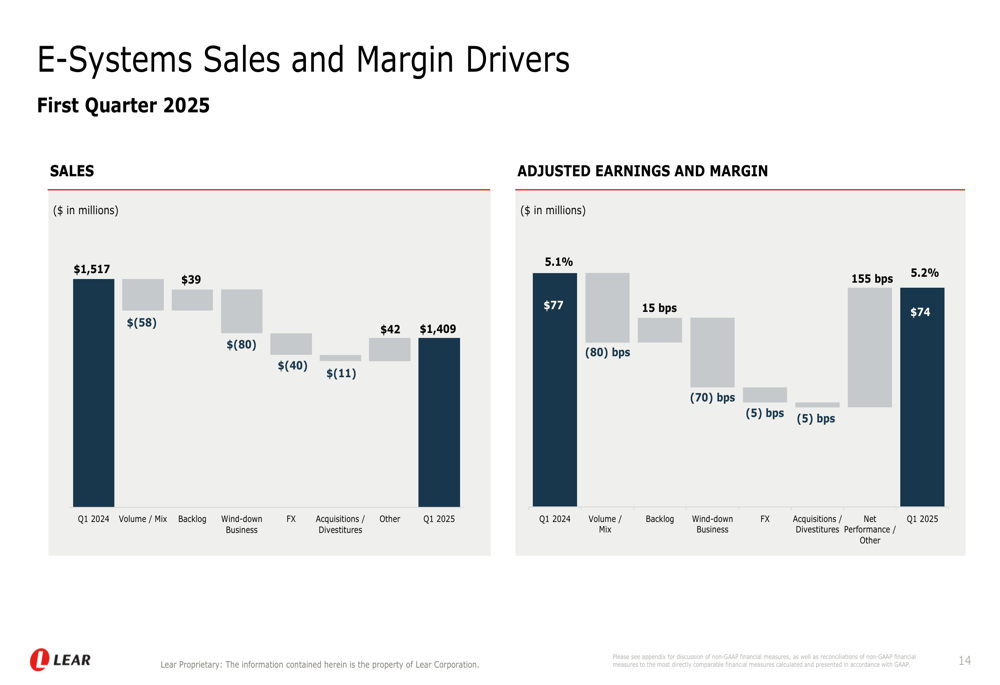

Similarly, the E-Systems segment reported sales of $1.41 billion, down from $1.52 billion in Q1 2024. The segment’s adjusted margin improved to 5.2% from 5.1%, with net performance contributing approximately 155 basis points, helping to offset headwinds from backlog and wind-down business.

The E-Systems segment’s performance drivers are illustrated in the following slide:

Strategic Initiatives

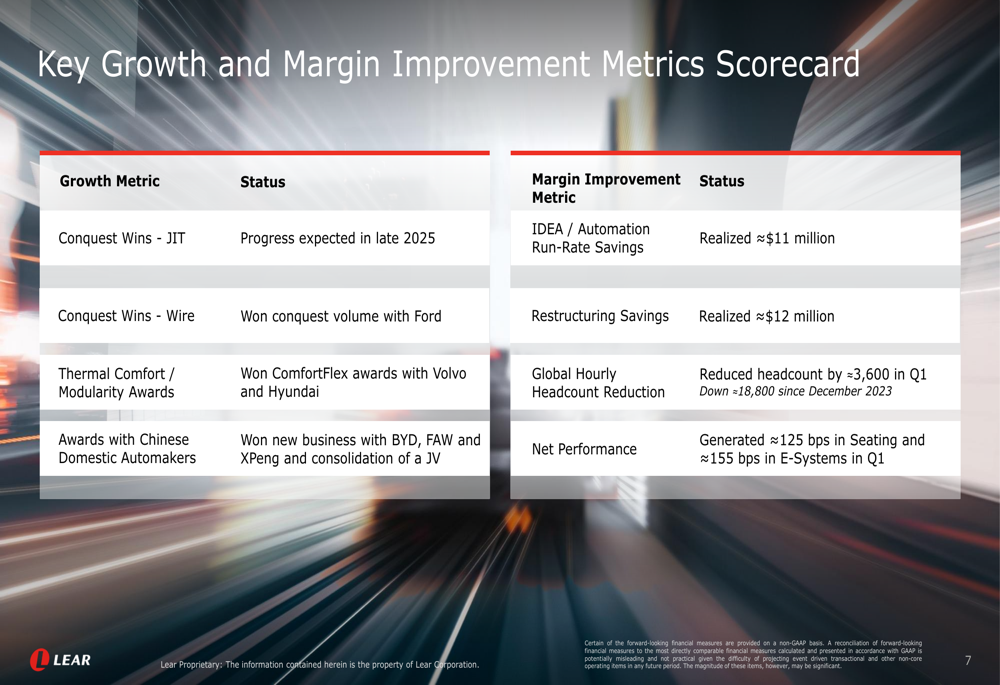

Lear continues to execute on its strategic growth and margin improvement initiatives, as evidenced by its metrics scorecard. The company reported progress in several key areas, including conquest wins with Ford in its wire business, thermal comfort awards with Volvo (OTC:VLVLY) and Hyundai (OTC:HYMTF), and new business with Chinese automakers including BYD (SZ:002594), FAW, and XPeng (NYSE:XPEV).

The company also made significant progress in cost reduction efforts, realizing approximately $11 million in savings from its IDEA automation initiatives and $12 million from restructuring actions. Notably, Lear reduced its global hourly headcount by approximately 3,600 in Q1 2025, bringing the total reduction to approximately 18,800 since December 2023.

These strategic initiatives are detailed in the following scorecard:

Market Challenges

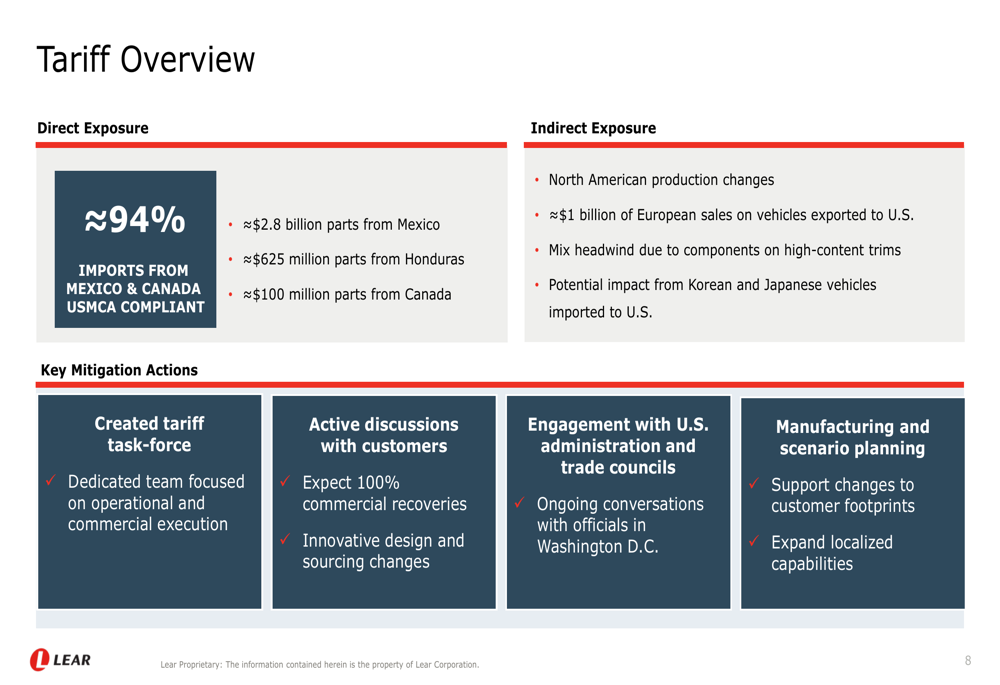

A significant challenge facing Lear is the potential impact of tariffs on its global operations. The company provided a detailed overview of its tariff exposure, noting that approximately 94% of its imports are from Mexico and Canada and are USMCA compliant. Lear imports approximately $2.8 billion in parts from Mexico, $625 million from Honduras, and $100 million from Canada.

To address these challenges, Lear has established a tariff task force, engaged in active discussions with customers, and is working with the U.S. administration and trade councils. The company is also conducting manufacturing and scenario planning to mitigate potential impacts.

The following slide outlines Lear’s tariff exposure and mitigation strategies:

Forward-Looking Statements

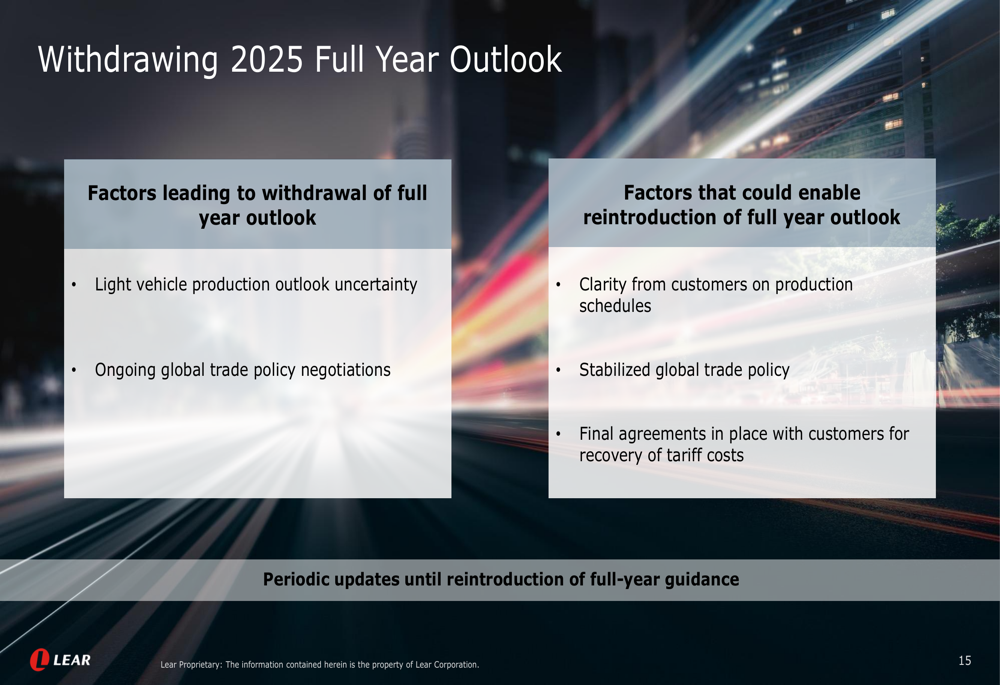

In a significant development, Lear announced the withdrawal of its 2025 full-year outlook, citing uncertainties in light vehicle production and ongoing global trade policy negotiations. The company indicated that it would provide periodic updates and could reintroduce guidance once there is greater clarity from customers on production schedules, stabilized global trade policy, and final agreements with customers for recovery of tariff costs.

This cautious approach reflects the challenging and uncertain operating environment facing automotive suppliers in 2025. The factors leading to the withdrawal and conditions for reinstatement are detailed in the following slide:

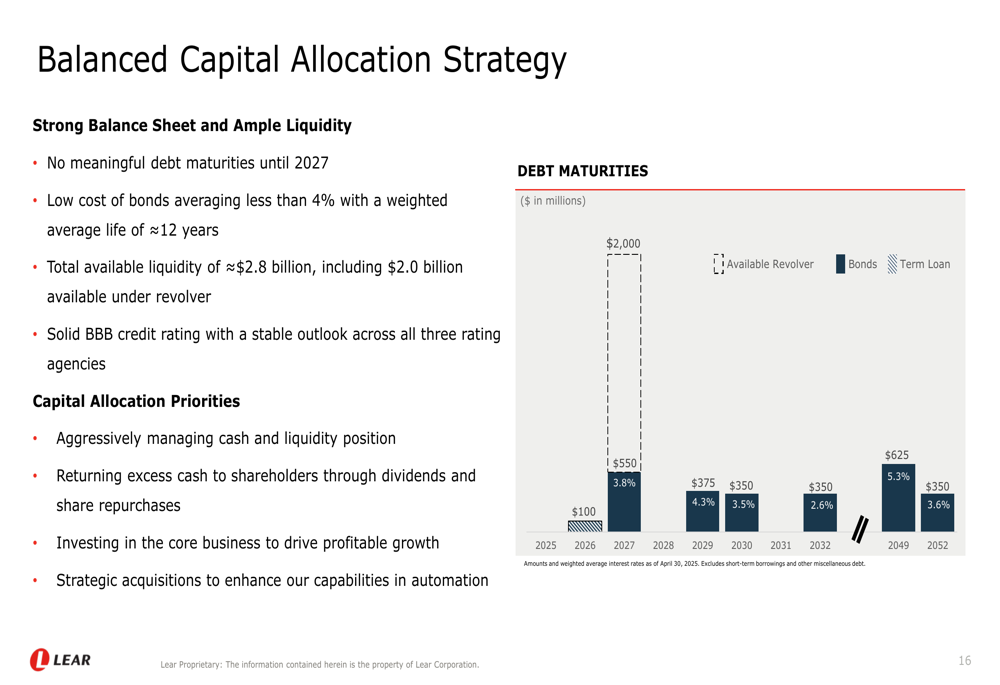

Capital Allocation and Financial Position

Despite the challenging operating environment, Lear maintains a strong financial position with a balanced capital allocation strategy. The company has no meaningful debt maturities until 2027, with low-cost bonds averaging less than 4% and a weighted average life of approximately 12 years. Lear’s total available liquidity stands at approximately $2.8 billion, including $2.0 billion available under its revolving credit facility.

During Q1 2025, Lear returned capital to shareholders through $25 million in share repurchases and $43 million in dividends. The company maintains a solid BBB credit rating with a stable outlook across all three rating agencies.

Lear’s capital allocation priorities include aggressively managing its cash and liquidity position, returning excess cash to shareholders, investing in the core business to drive profitable growth, and pursuing strategic acquisitions to enhance its capabilities in automation.

The company’s balanced capital allocation strategy is illustrated in the following slide:

Looking ahead, Lear remains focused on extending its global leadership in Seating, expanding margins through its focused portfolio in E-Systems, growing capabilities in operational excellence, and supporting sustainable value creation with disciplined capital allocation. Despite near-term challenges, the company believes it is well-positioned for long-term success in the evolving automotive industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.