German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Lear Corporation (NYSE:LEA) presented its second quarter 2025 financial results on July 25, 2025, reporting flat year-over-year sales but declining earnings amid ongoing industry challenges. Despite the company’s restoration of full-year guidance after previously withdrawing it due to tariff concerns, investors reacted negatively, with shares falling 8.1% during the trading session.

The automotive supplier reported its results against a backdrop of mixed global vehicle production, with China showing strong growth of 9% year-over-year, while North America and Europe declined by 3% and 2% respectively. This uneven production environment, combined with ongoing tariff concerns and margin pressures, contributed to the market’s cautious stance despite management’s optimistic outlook.

Quarterly Performance Highlights

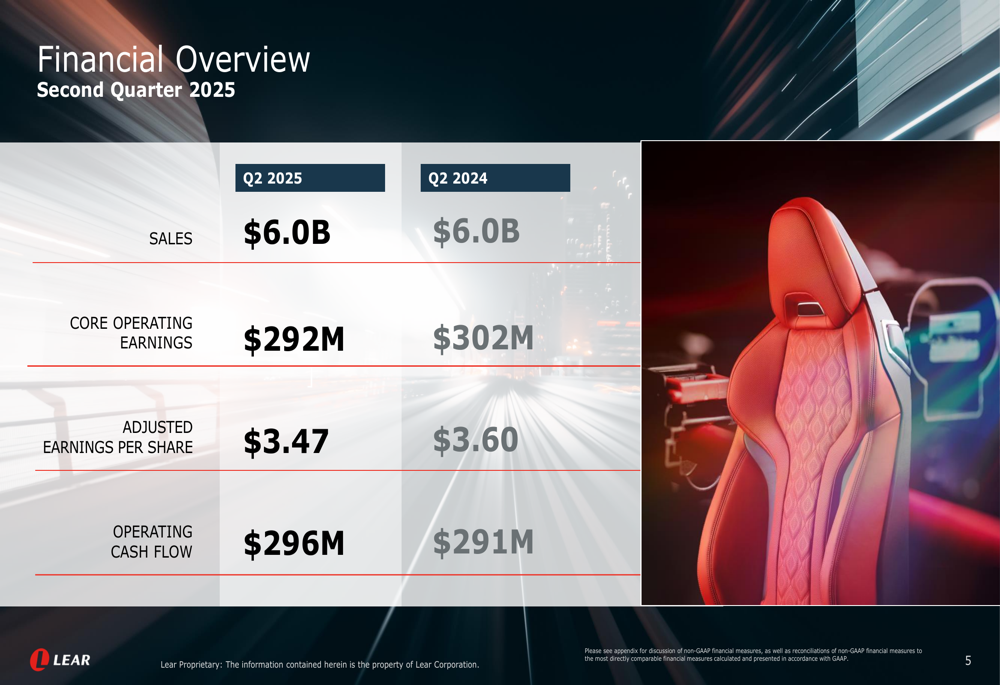

Lear’s second quarter 2025 financial results showed resilience in some areas but weakness in others. The company reported sales of $6.0 billion, essentially flat compared to the same period in 2024, while core operating earnings declined to $292 million from $302 million in the prior year.

As shown in the following financial overview chart, adjusted earnings per share fell to $3.47 from $3.60 in Q2 2024, representing a 3.6% decrease. Operating cash flow, however, showed improvement, increasing to $296 million from $291 million in the prior-year period:

The company highlighted several positive developments during the quarter, including strong net performance in both segments (approximately 45 basis points in Seating and 70 basis points in E-Systems), as well as conquest wins with BMW (ETR:BMWG), Ford, and a global EV automaker. Lear also emphasized its progress in operational efficiency initiatives and restructuring efforts.

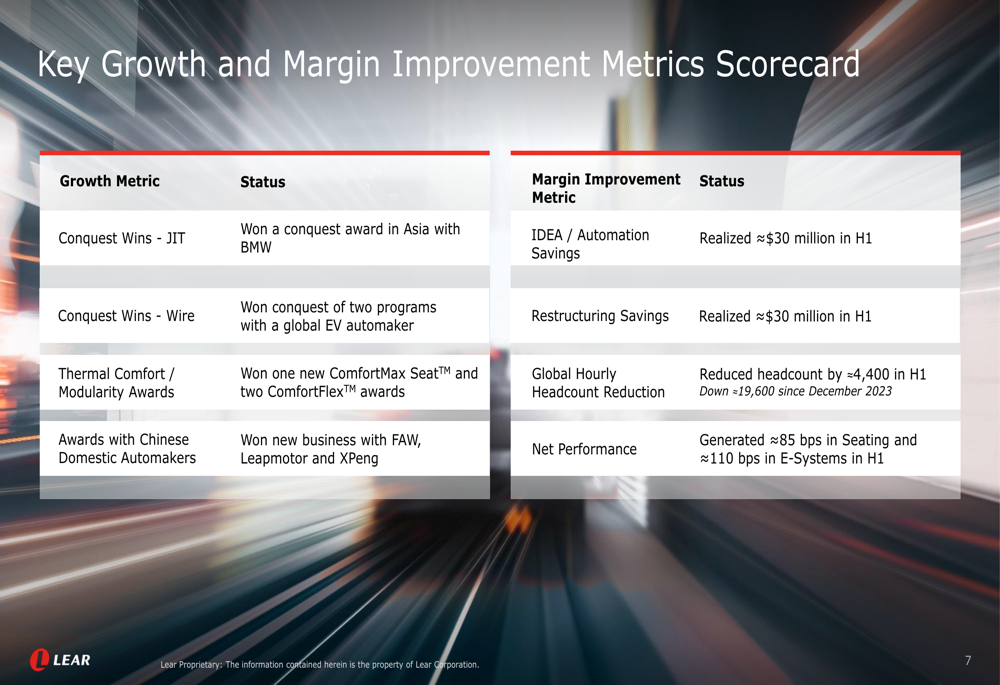

The following slide details the company’s key Q2 2025 highlights across its strategic focus areas:

Lear’s scorecard of key growth and margin improvement metrics shows progress in several areas, including conquest wins in both the JIT (Just-In-Time) and wire segments, as well as thermal comfort and modularity awards. The company also reported significant headcount reductions, with global hourly headcount down by approximately 4,400 in the first half of 2025 and approximately 19,600 since December 2023:

Segment Performance Analysis

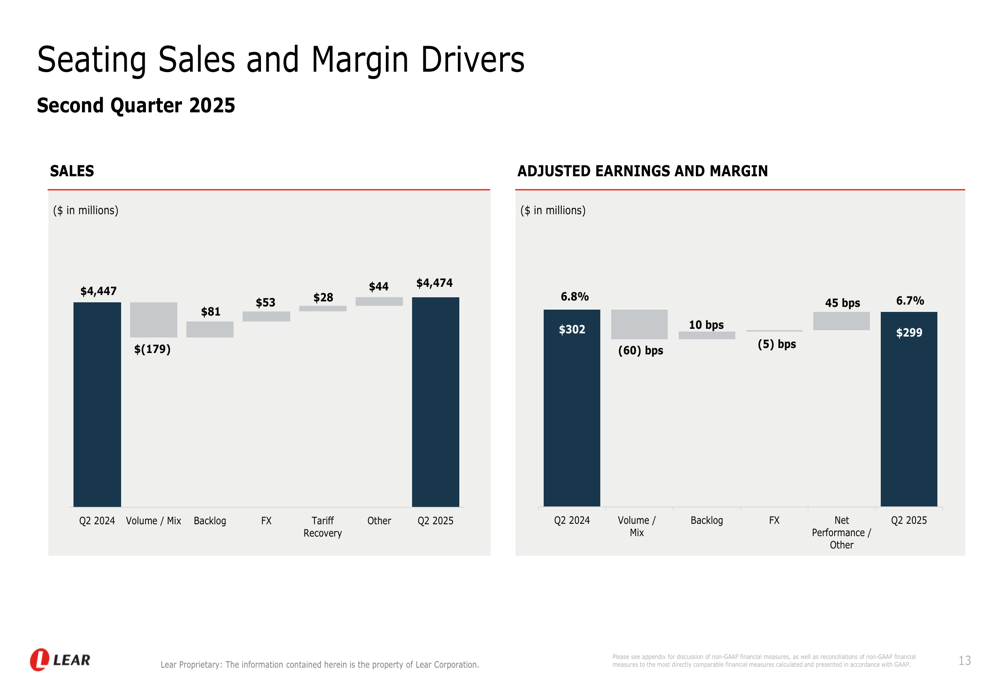

Lear’s Seating segment, which accounts for approximately 74% of total sales, reported revenue of $4.47 billion in Q2 2025, a slight increase from $4.45 billion in Q2 2024. However, adjusted earnings for the segment declined to $299 million from $302 million, with margins contracting slightly to 6.7% from 6.8%.

The following waterfall chart breaks down the key drivers of Seating segment sales and margin performance:

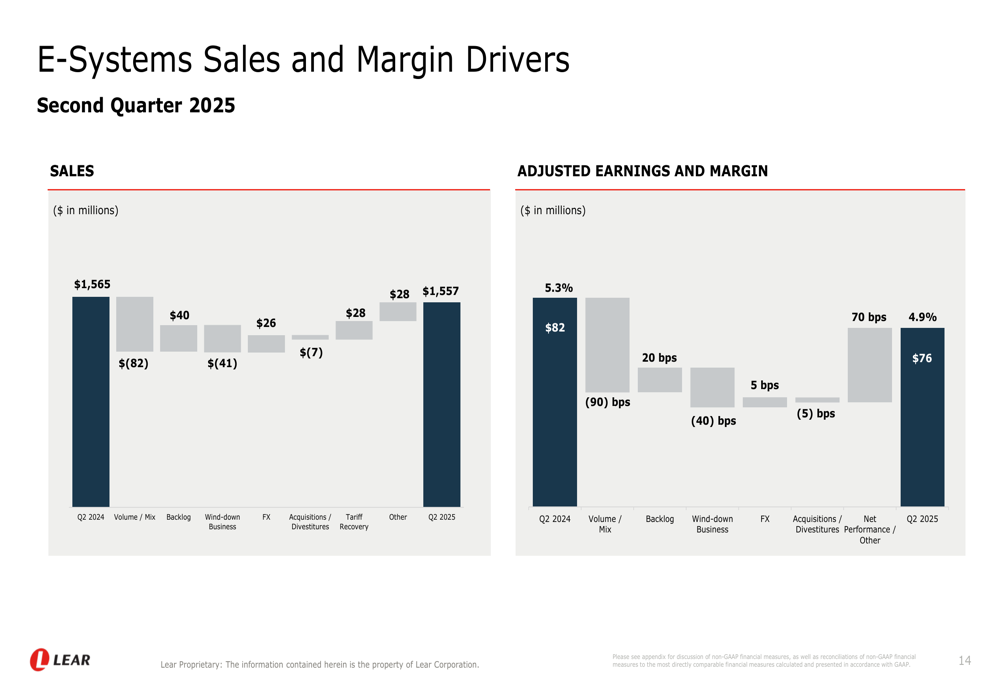

The E-Systems segment faced more significant challenges, with sales declining to $1.56 billion from $1.57 billion in Q2 2024. Adjusted earnings for the segment fell to $76 million from $82 million, with margins declining to 4.9% from 5.3%. The segment was particularly impacted by wind-down business and unfavorable volume/mix effects:

Tariff Exposure and Mitigation

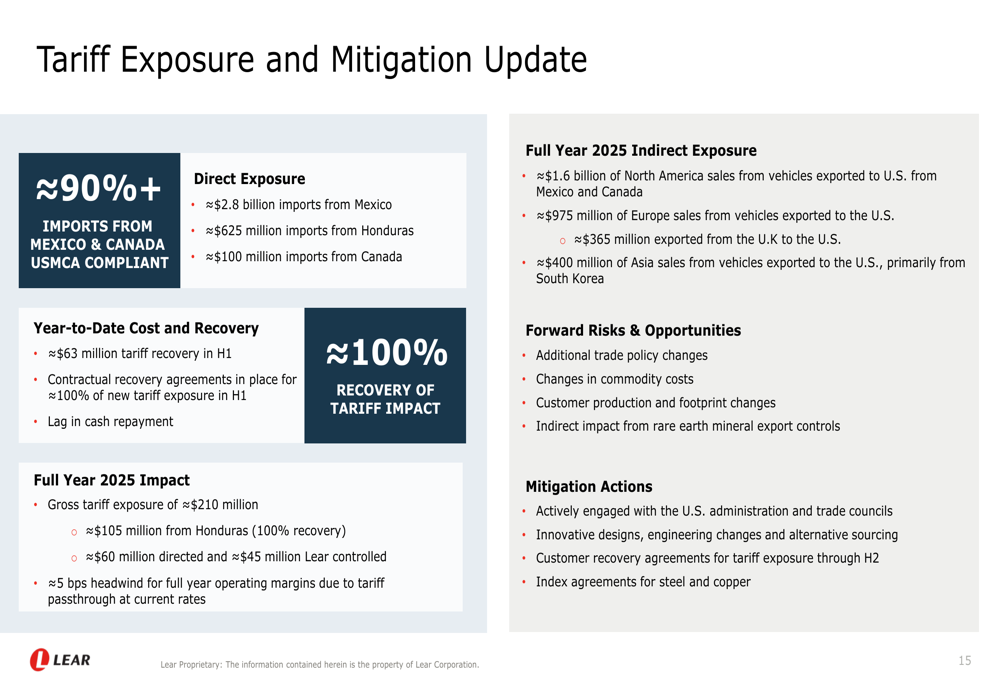

A central focus of Lear’s presentation was its approach to managing tariff exposure, a concern that had previously led the company to withdraw its full-year guidance in Q1 2025. The company now claims to have contractual recovery agreements in place for approximately 100% of new tariff exposure.

Lear detailed its tariff exposure and mitigation strategy, noting that over 90% of its imports from Mexico and Canada are USMCA compliant. The company faces a gross tariff exposure of approximately $210 million for full year 2025, with about $105 million coming from Honduras:

The company reported tariff recovery of approximately $63 million in the first half of 2025 and expressed confidence in its ability to recover 100% of tariff impacts through customer agreements. This increased confidence appears to be a key factor in the company’s decision to restore full-year guidance.

Strategic Initiatives

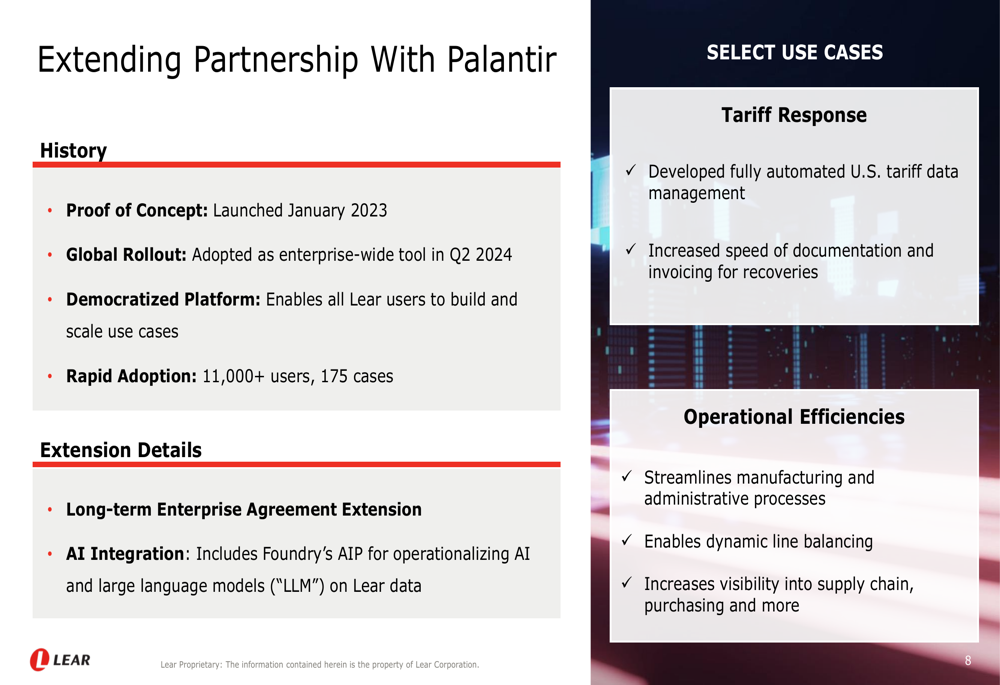

Lear highlighted several strategic initiatives aimed at improving operational efficiency and driving margin expansion. A key development was the extension of its partnership with Palantir Technologies (NASDAQ:PLTR), which includes AI integration and the use of Palantir’s Foundry platform for data management and operational improvements:

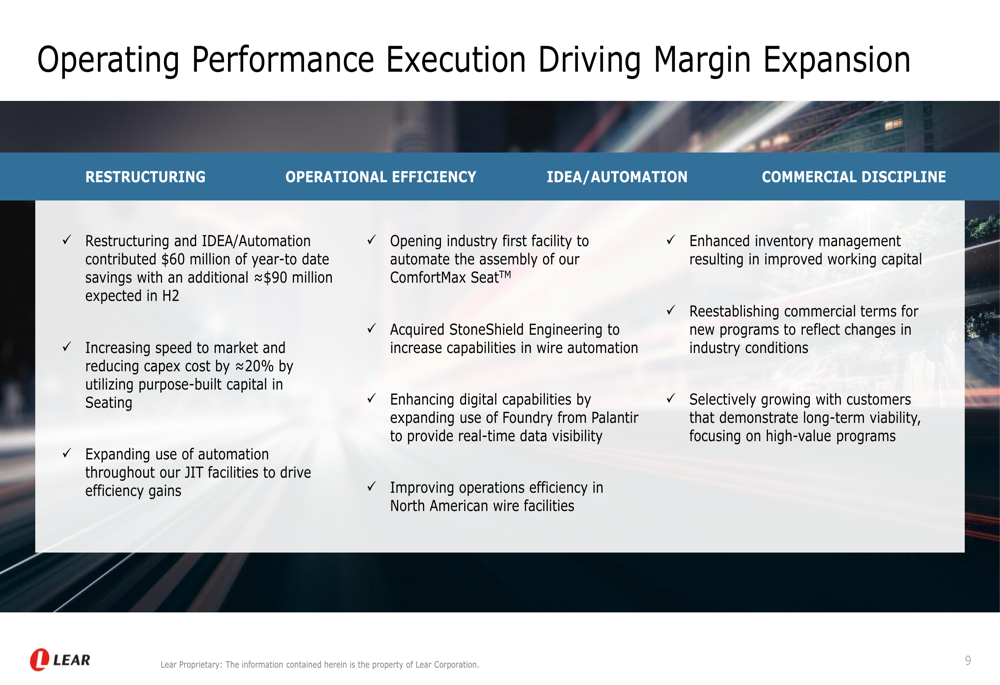

The company also detailed its focus on operational performance execution to drive margin expansion, including restructuring efforts, operational efficiency improvements, and enhanced commercial discipline:

These initiatives contributed to approximately $60 million in year-to-date savings from restructuring and IDEA/automation efforts, with an additional $90 million expected in the second half of 2025.

Forward-Looking Statements

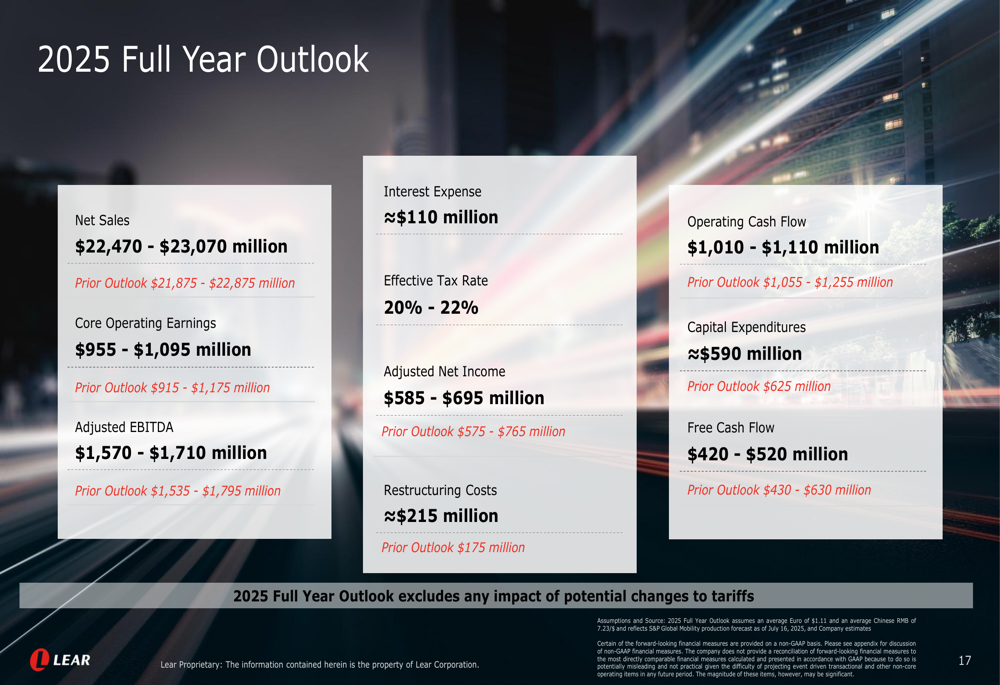

After withdrawing guidance in Q1 2025 due to tariff uncertainties, Lear has now restored its full-year outlook. The company projects 2025 net sales of $22.47 billion to $23.07 billion and core operating earnings of $955 million to $1.095 billion:

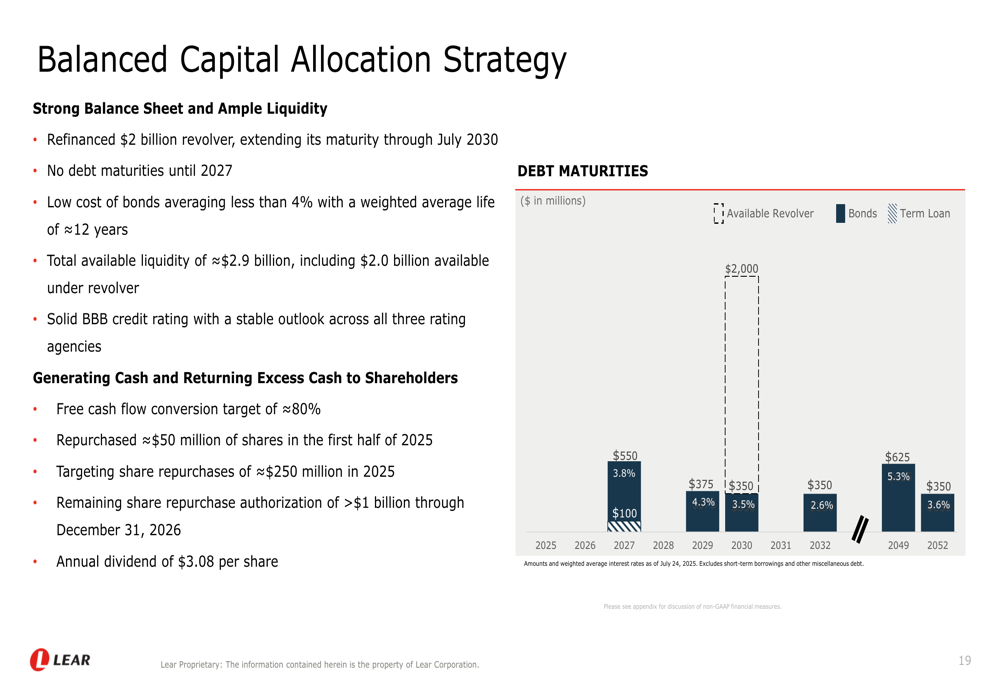

Lear also outlined its capital allocation strategy, emphasizing its strong balance sheet with approximately $2.9 billion in available liquidity and no debt maturities until 2027. The company reported share repurchases of approximately $50 million in the first half of 2025 and is targeting total repurchases of approximately $250 million for the full year:

Despite the company’s restored guidance and positive outlook, investors appeared unconvinced, as evidenced by the 8.1% decline in Lear’s stock price on the day of the presentation. This reaction suggests continued market concerns about the company’s ability to maintain margins and manage tariff impacts in an uncertain global automotive environment.

The sequential improvement in EPS from $3.12 in Q1 2025 to $3.47 in Q2 2025 indicates some positive momentum, but the year-over-year decline from $3.60 in Q2 2024 highlights the ongoing challenges facing the company as it navigates a complex industry landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.