BitMine stock falls after CEO change and board appointments

Introduction & Market Context

Finnish software company Lemonsoft Oyj (HEL:LEMON) presented its Q1 2025 interim results on April 25, showing signs of recovery with positive organic growth and improved profitability. The company’s stock, which had faced pressure following challenging Q4 2024 results, responded positively, trading at €5.60, up 2.5% on the day of the presentation.

The Q1 results come after a difficult period for Lemonsoft, which saw its stock drop 6.45% following its Q4 2024 earnings announcement. The company appears to be executing on previously announced strategic initiatives, including its Azure migration and organizational restructuring, with management emphasizing that effects of these changes are expected to become more visible in the second half of 2025.

Quarterly Performance Highlights

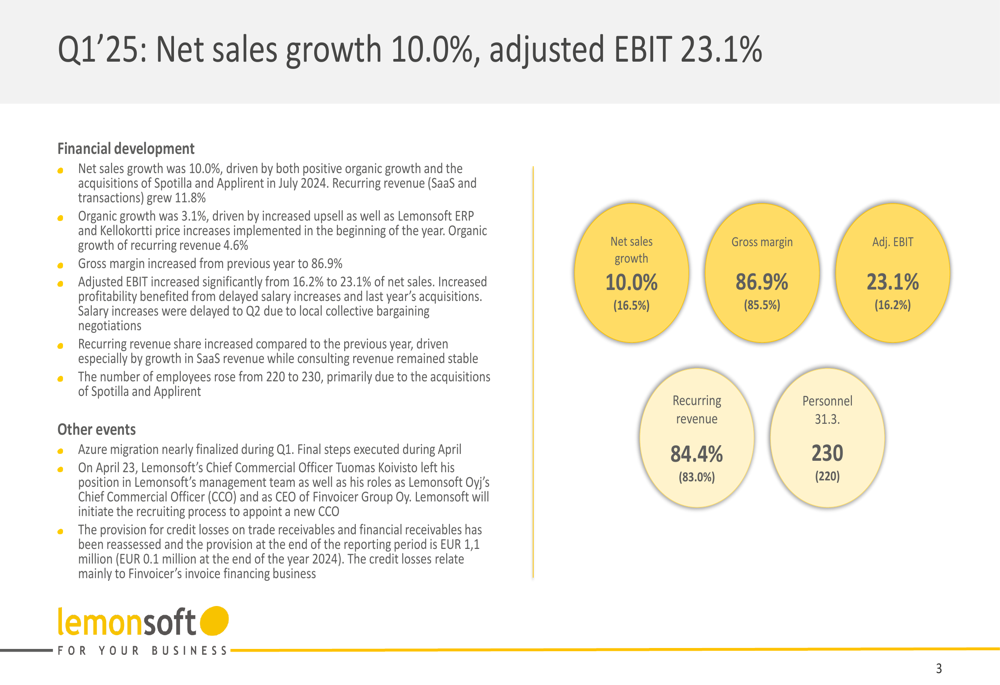

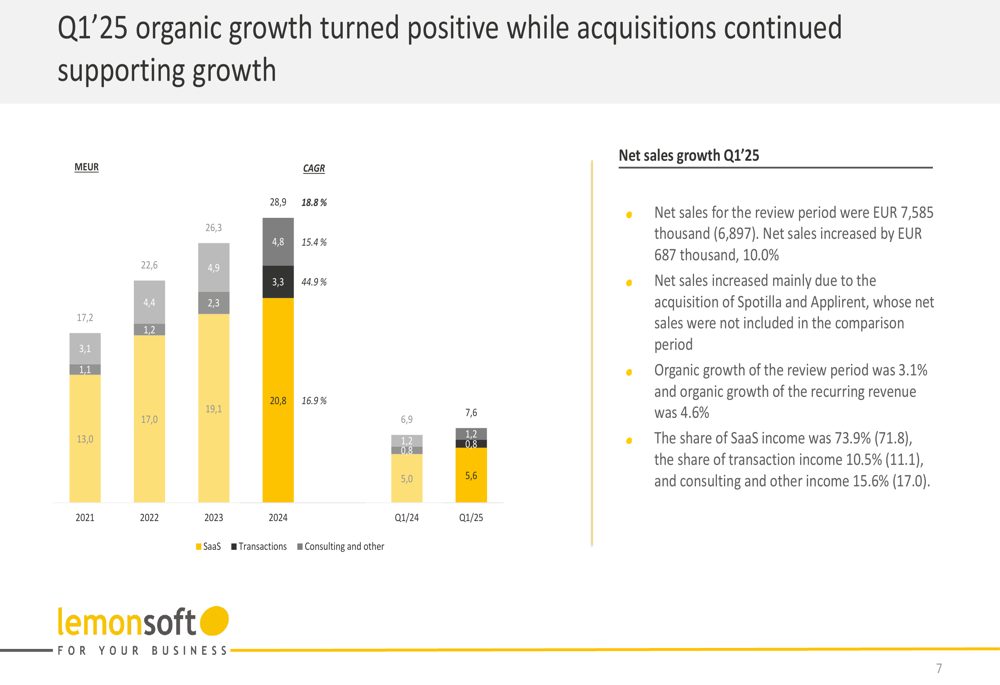

Lemonsoft reported net sales growth of 10.0% for Q1 2025, reaching €7.59 million, driven by both organic growth and the acquisitions of Spotilla and Applirent completed in July 2024. Notably, organic growth turned positive at 3.1%, with recurring revenue showing even stronger organic growth at 4.6%.

As shown in the following financial highlights chart, the company significantly improved its adjusted EBIT margin to 23.1%, up from 16.2% in the same period last year:

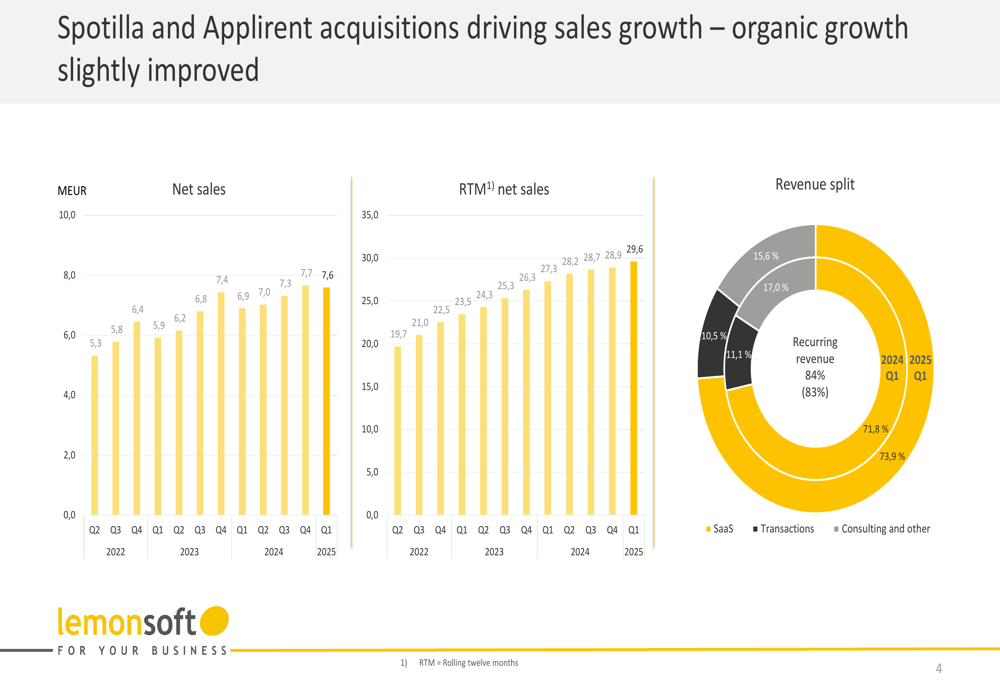

The company’s revenue mix continues to shift toward higher-margin recurring revenue streams, with SaaS and transaction revenue now accounting for 84.4% of total revenue, up from 83.0% in the previous year. The share of SaaS income specifically increased to 73.9% from 71.8% a year earlier.

The following chart illustrates the evolution of Lemonsoft’s sales and revenue composition:

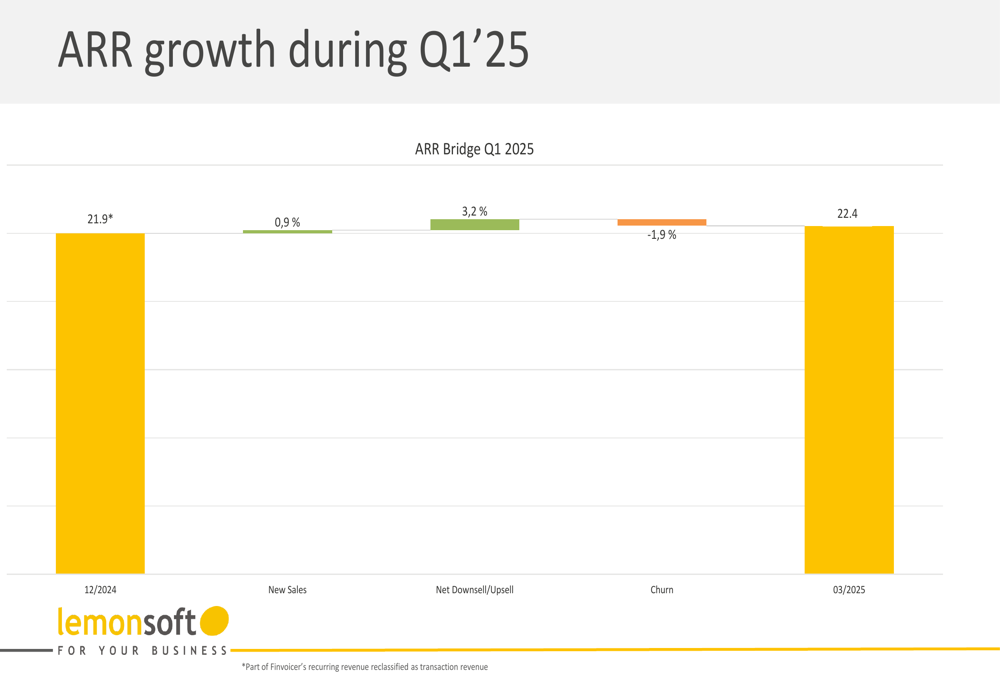

Annual Recurring Revenue (ARR), a key metric for software companies, grew to €22.4 million by the end of Q1 2025. This growth was driven by new sales contributing 0.9% and net upsell adding 3.2%, partially offset by a 1.9% churn rate:

Strategic Initiatives

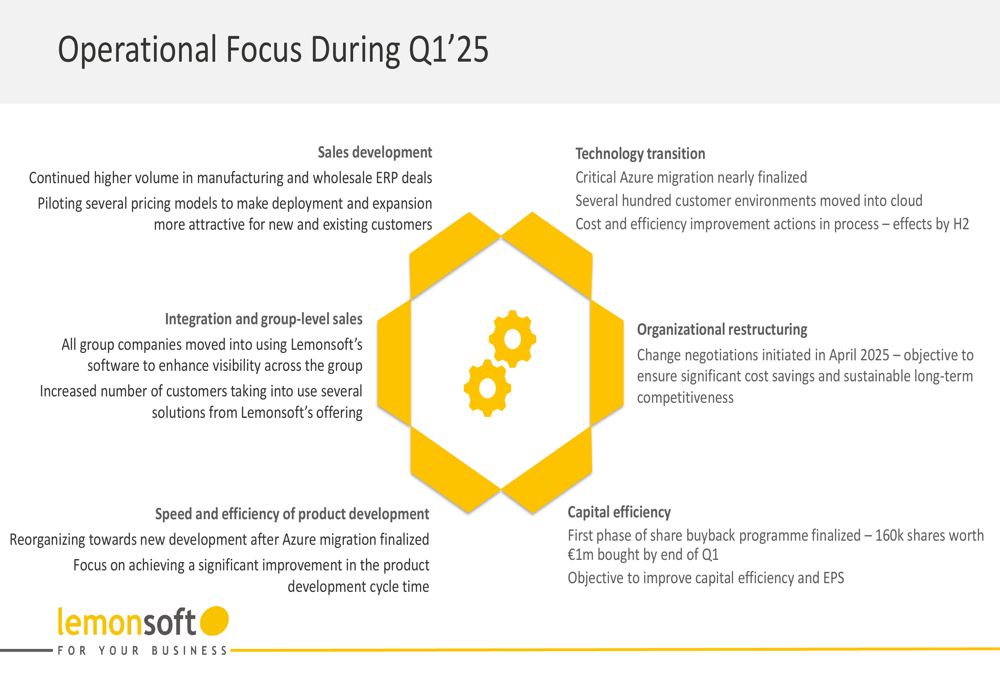

Lemonsoft highlighted several key strategic initiatives underway during Q1 2025, with their critical Azure migration nearly completed. The company moved several hundred customer environments to the cloud during the quarter, with final steps executed in April. Management expects this transition to yield cost and efficiency improvements in the second half of the year.

The company’s operational focus areas are outlined in the following chart:

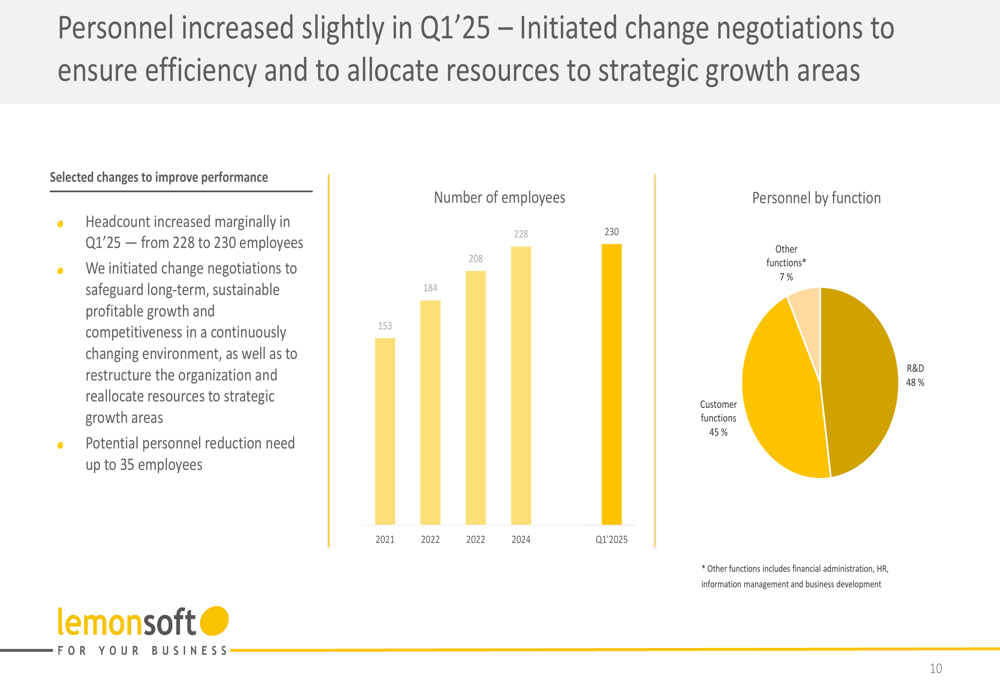

In a significant move toward cost optimization, Lemonsoft initiated change negotiations in April 2025 that could potentially reduce its workforce by up to 35 employees. The company frames this as ensuring "significant cost savings and sustainable long-term competitiveness." This comes as the company’s headcount had increased from 220 to 230 employees, primarily due to the acquisitions of Spotilla and Applirent.

Lemonsoft also completed the first phase of its share buyback program, purchasing 160,000 shares worth €1 million by the end of Q1, with the stated aim of improving capital efficiency and earnings per share.

Financial Analysis

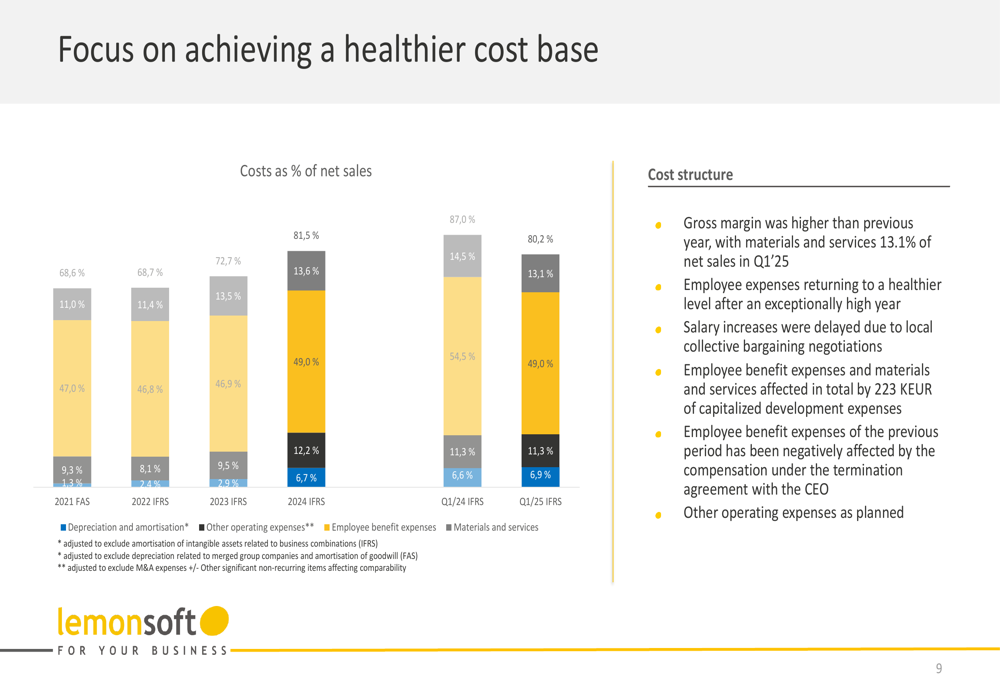

Lemonsoft’s improved profitability in Q1 2025 benefited from both delayed salary increases due to local collective bargaining negotiations and contributions from recent acquisitions. The company’s gross margin increased to 86.9% from 85.5% in the previous year.

The following cost structure analysis provides insight into the company’s improving profitability:

The company’s personnel distribution shows a focus on R&D and customer functions, which together account for 93% of the workforce:

One concerning development was the significant increase in provisions for credit losses, which rose to €1.1 million from €0.1 million at the end of 2024. The company noted these credit losses relate mainly to Finvoicer’s invoice financing business.

Forward-Looking Statements

Lemonsoft’s presentation emphasized that the significant changes currently underway are expected to show their effects in the second half of 2025. The company is focusing on several key areas to drive future growth:

1. Sales development with continued higher volume in manufacturing and wholesale ERP deals

2. Piloting several pricing models to make deployment and expansion more attractive

3. Reorganizing product development to achieve significant improvements in cycle time

4. Enhancing cross-selling across the group, with all group companies now using Lemonsoft’s software

The following chart details the company’s organic growth trajectory, which management aims to improve:

While Lemonsoft did not provide specific numerical guidance for the full year 2025 in this presentation, the previous earnings report indicated expectations for net sales growth between 0% and 10%. The positive Q1 results suggest the company may be on track to achieve the upper end of this range if the current momentum continues.

Investors will be watching closely to see if the strategic changes and cost-cutting measures translate into sustained organic growth and profitability improvements in the coming quarters, with the next financial update scheduled for August 14, 2025, when the company will release its half-year report.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.