Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

Lemonsoft Oyj (HEL:LEMON) presented its Q2 2025 half-year report on August 14, 2025, revealing a significant slowdown in growth compared to previous quarters. The Finnish software company, currently trading at €6.94, announced the completion of its technology platform transition and organizational restructuring, marking the end of a transformative period for the business.

Following a strong Q1 2025 performance that saw 10% year-over-year revenue growth, Lemonsoft’s Q2 results indicate more challenging conditions with growth decelerating to 5.3%. The company’s stock has remained relatively stable despite the slowdown, trading well above its 52-week low of €4.65 but still below its high of €7.90.

Quarterly Performance Highlights

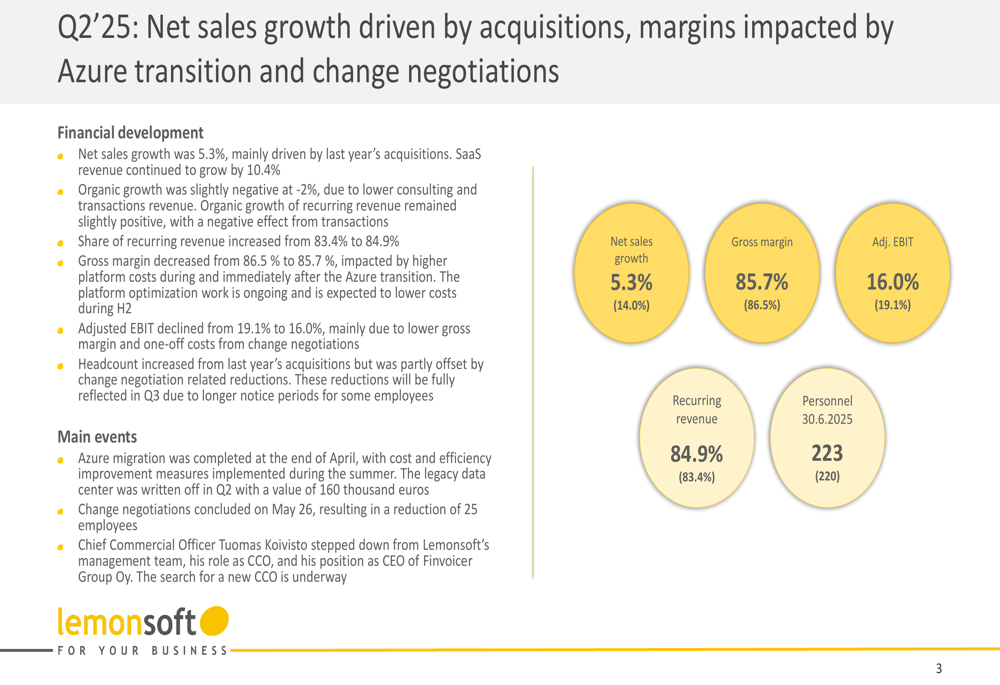

Lemonsoft reported net sales growth of 5.3% for Q2 2025, a significant decrease from the 14.0% growth recorded in the same period last year. The company’s adjusted EBIT margin contracted to 16.0%, down from 19.1% in Q2 2024, while gross margin slightly decreased to 85.7% from 86.5%.

As shown in the following performance highlights:

A notable concern is the negative organic growth of -2.0% for the quarter, with the company attributing its overall growth primarily to acquisitions. On a more positive note, recurring revenue increased to 84.9% of total revenue, up from 83.4% in the previous year, demonstrating progress in the company’s strategic shift toward more stable revenue streams.

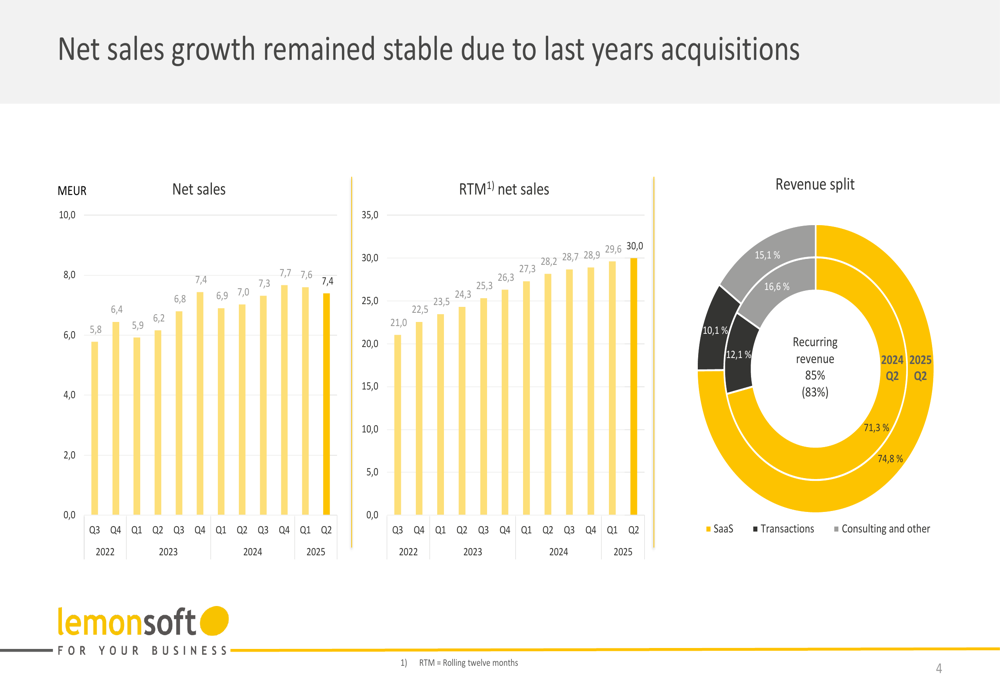

The company’s net sales and revenue split over time shows the progression of its business model:

Detailed Financial Analysis

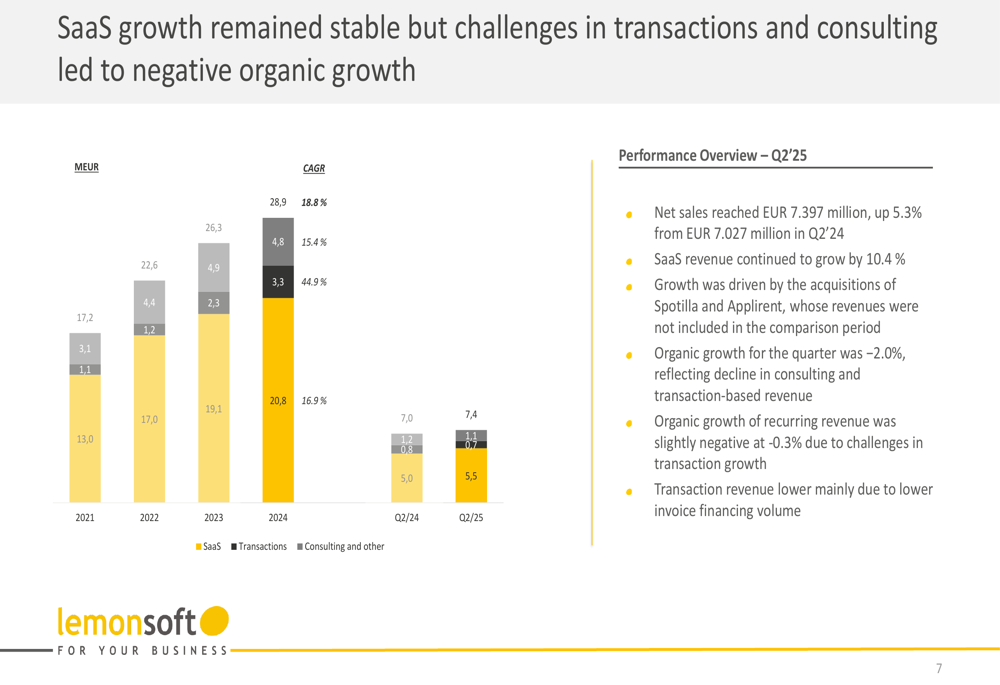

Lemonsoft’s SaaS revenue continued to show strength with 10.4% growth, serving as the primary driver of the company’s performance amid challenges in transactions and consulting segments. The company’s presentation revealed that these challenges led to the negative organic growth experienced during the quarter.

The following chart illustrates the SaaS growth analysis:

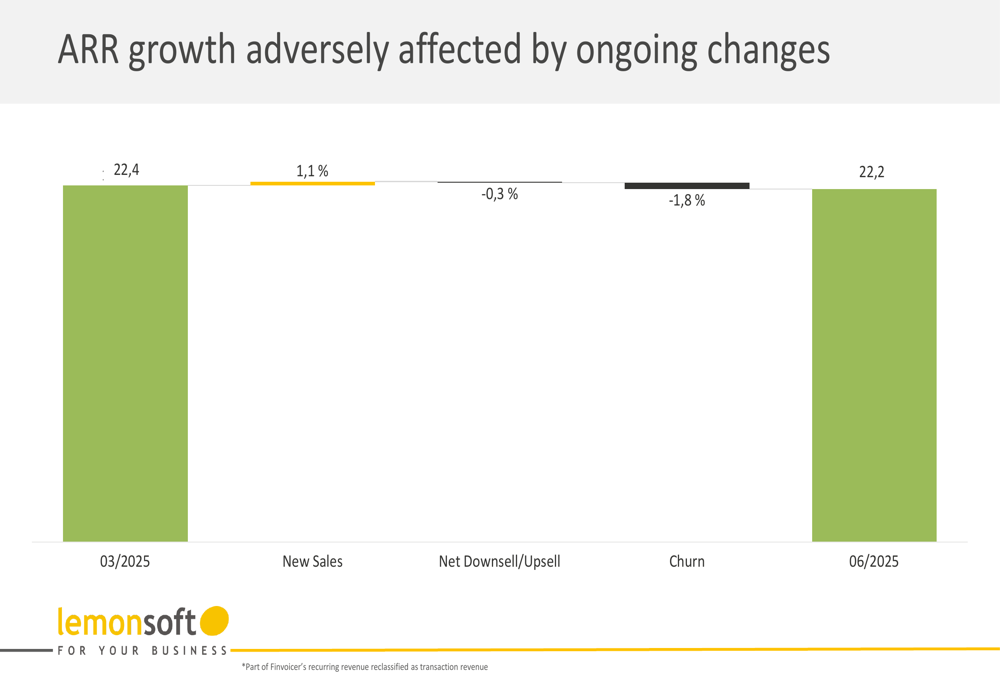

Annual Recurring Revenue (ARR) showed a concerning trend, decreasing from €22.4 million in March 2025 to €22.2 million in June 2025. This decline contrasts with the ARR growth reported in Q1, which increased from €21.9 million to €22.4 million.

The ARR analysis reveals the factors behind this decline:

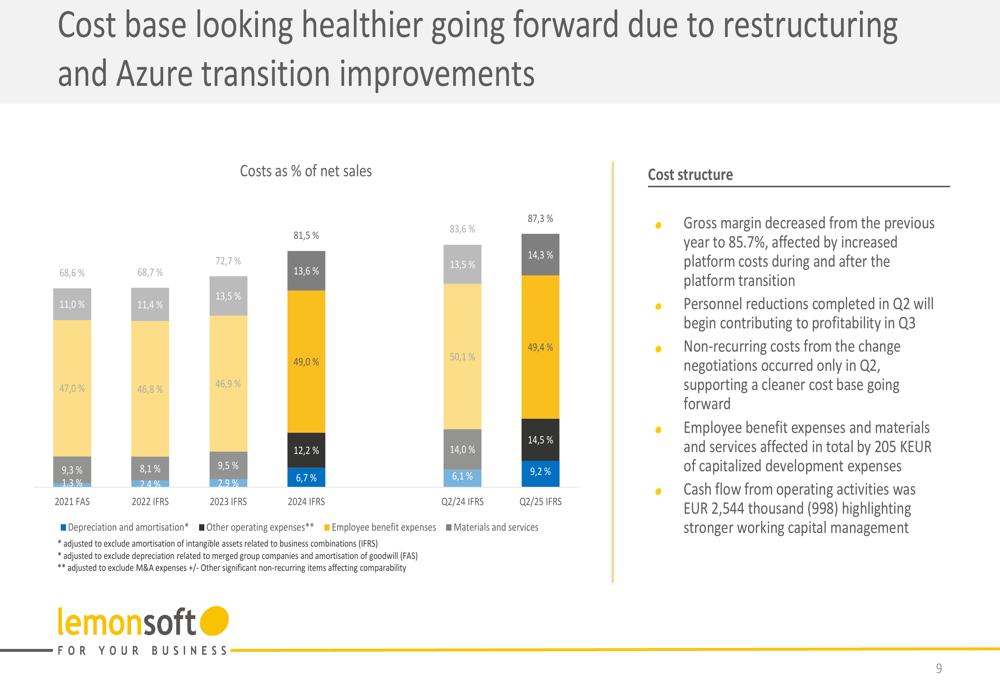

The company’s cost structure showed some improvements following restructuring efforts and the Azure transition. Cash flow from operating activities remained positive at €2,544 thousand, providing some financial stability despite the growth challenges.

The cost base analysis demonstrates these changes:

Strategic Initiatives

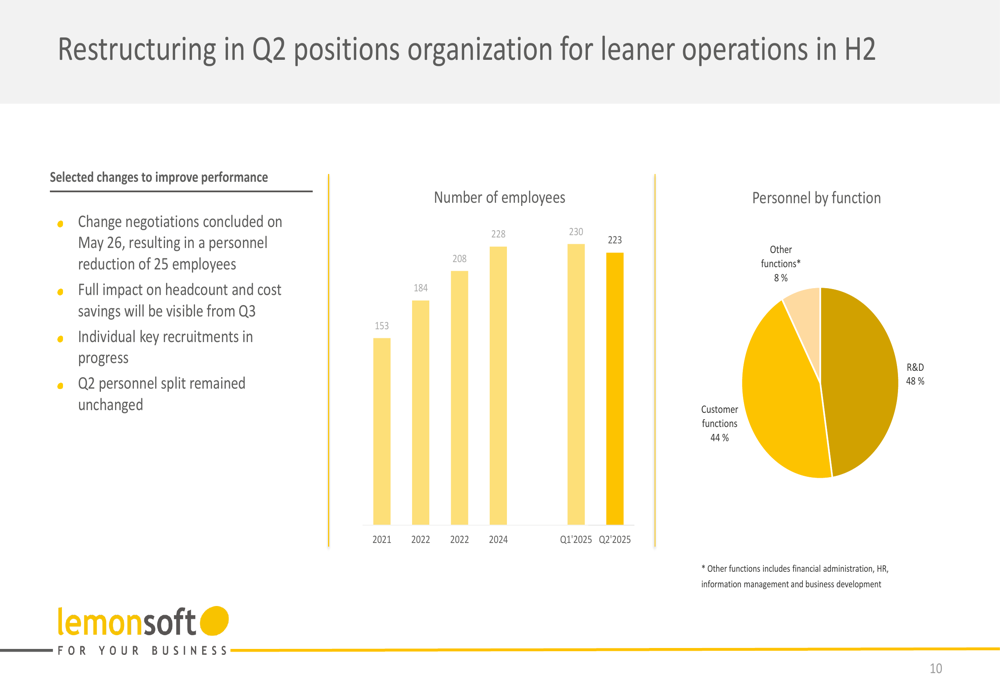

Lemonsoft completed several significant operational changes during Q2 2025, most notably concluding its Azure migration in April and finalizing change negotiations on May 26, which resulted in a reduction of 25 employees. The company’s total personnel count stood at 223 at the end of Q2, compared to 220 in the previous year.

The restructuring efforts are evident in the personnel changes:

The company has also restructured its sales organization and reported strong Monthly Recurring Revenue (MRR) growth for subsidiaries Spotilla and Applirent. Additionally, Lemonsoft launched a new share buyback program, signaling confidence in its long-term prospects despite current challenges.

CEO Alpo Luostarinen, who presented the results, emphasized that the personnel reductions from the change negotiations are expected to contribute to improved profitability beginning in Q3 2025, with the full effect of cost savings to be realized in subsequent quarters.

Forward-Looking Statements

Lemonsoft expects the completed technology platform transition and organizational restructuring to yield benefits in the coming quarters. The company highlighted that non-recurring costs occurred only in Q2, suggesting improved profitability metrics in future periods.

The focus on growing SaaS revenue remains central to Lemonsoft’s strategy, with the company working to address challenges in its transactions and consulting segments. Management indicated that part of Finvoicer’s recurring revenue was reclassified as transaction revenue, which may impact how investors interpret recurring revenue trends going forward.

Lemonsoft will release its Interim Report for January-September 2025 on October 31, 2025, which will provide further insights into whether the company’s restructuring efforts are delivering the anticipated financial improvements.

While the company did not provide specific guidance figures in this presentation, the previous earnings call indicated expectations for stable quarterly growth and approximately €2 million in cost savings through organizational changes. The Q2 results suggest that achieving these targets may be more challenging than initially anticipated, particularly given the negative organic growth and declining ARR.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.