Hedge funds are buying these two big tech stocks while selling two rivals

Introduction & Market Context

Life Time Group Holdings Inc (NYSE:LTH) presented its Q3 2025 earnings supplement on November 4, 2025, revealing an accelerated expansion strategy and strong membership trends. The stock rose 4.14% in pre-market trading to $25.75 following the company's earnings beat, with reported EPS of $0.41 exceeding forecasts by 24.24% and revenue reaching $782.6 million, up 12.9% year-over-year.

The premium fitness operator's presentation highlighted its continued focus on high-quality membership growth and enhanced club experiences, positioning itself strategically in the competitive wellness market.

Executive Summary

Life Time's Q3 2025 results demonstrated the effectiveness of its premium wellness strategy, with net income soaring 147% to $102 million compared to the previous year. The company emphasized its strengthening membership mix, with a notable shift toward couples and family memberships, which typically generate higher revenue per membership.

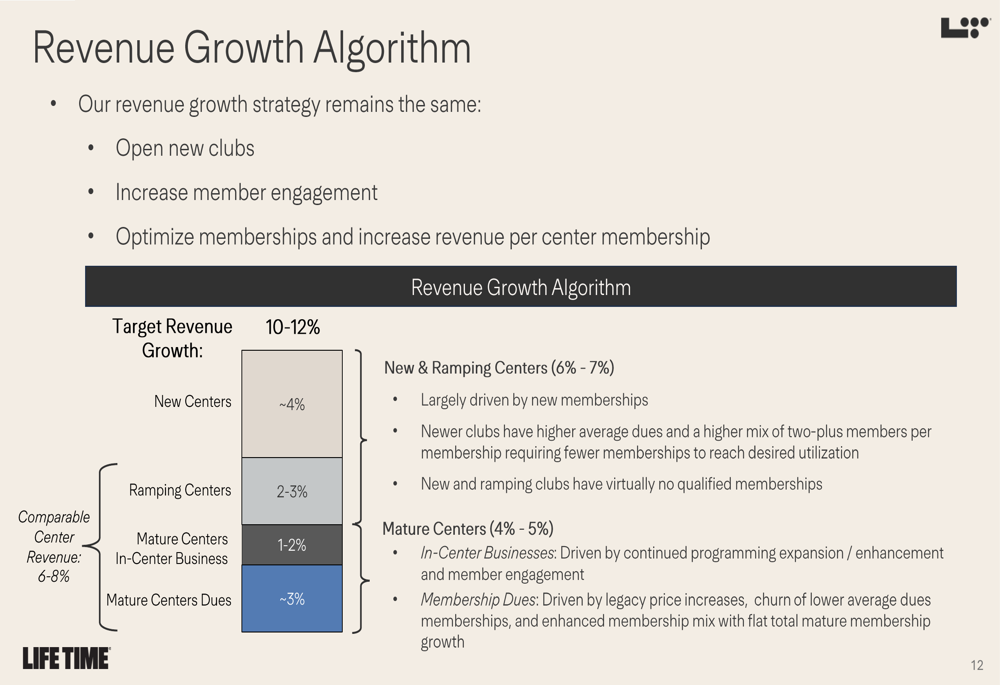

As shown in the following slide detailing the company's revenue growth algorithm, Life Time is targeting 10-12% overall revenue growth through a combination of new centers, ramping centers, and mature center growth:

The actual Q3 2025 revenue growth of 12.9% indicates the company is executing at the high end of its target range, validating its strategic approach. CEO Bahram Akradi emphasized this success during the earnings call, stating, "Our strategy is working. Life Time is working."

Expansion Strategy

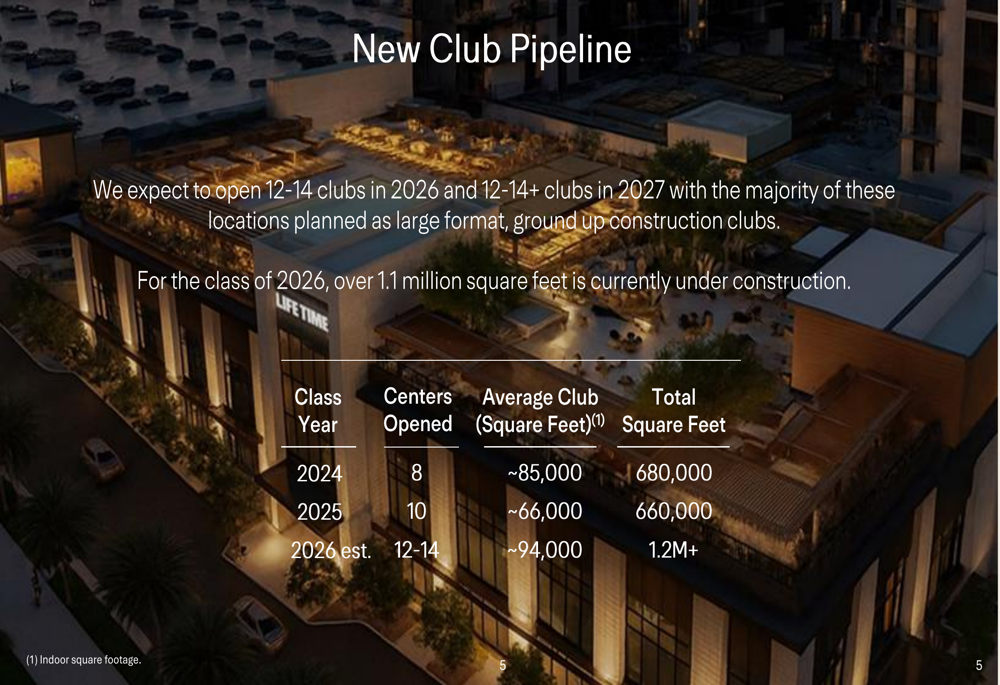

Life Time announced an acceleration of its club opening plans, increasing its target from 10-12 to 12-14 new clubs annually for 2026 and beyond. The company already has 13 clubs under construction for the 2026 class, representing over 1.2 million square feet of new premium fitness space.

The following slide details the company's new club pipeline across 2024-2026, showing a significant increase in both the number and average size of clubs planned for 2026:

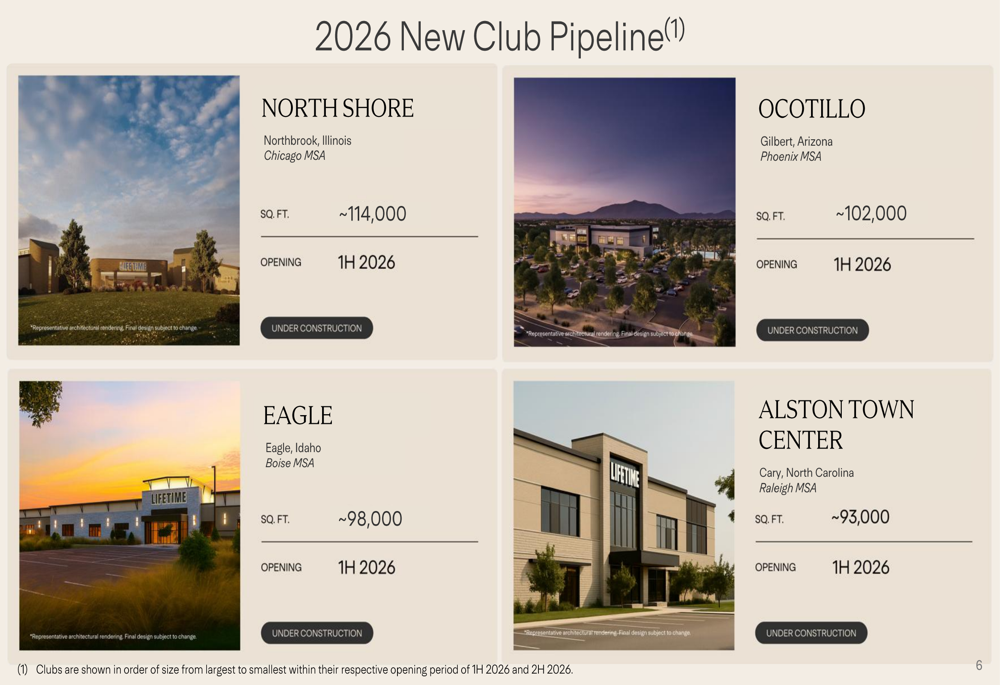

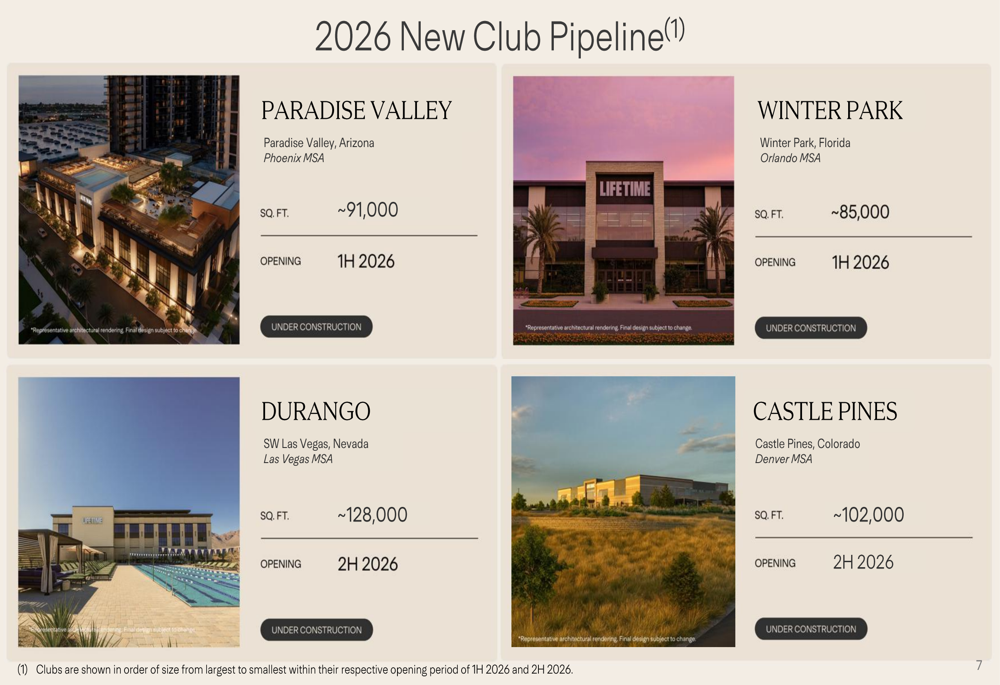

The 2026 club pipeline features locations across key growth markets including Arizona, Florida, Illinois, New York, and Nevada. Most notably, the 2026 openings will average approximately 94,000 square feet per club, substantially larger than the 2025 average of 66,000 square feet, indicating a strategic shift toward more comprehensive facilities.

The detailed expansion plans include a mix of suburban locations with extensive amenities and strategic urban sites, as illustrated in this breakdown of specific 2026 openings:

This accelerated expansion aligns with the company's stated revenue growth algorithm, where new and ramping centers are expected to contribute approximately 6-7% of the targeted 10-12% annual revenue growth.

Membership Growth & Engagement

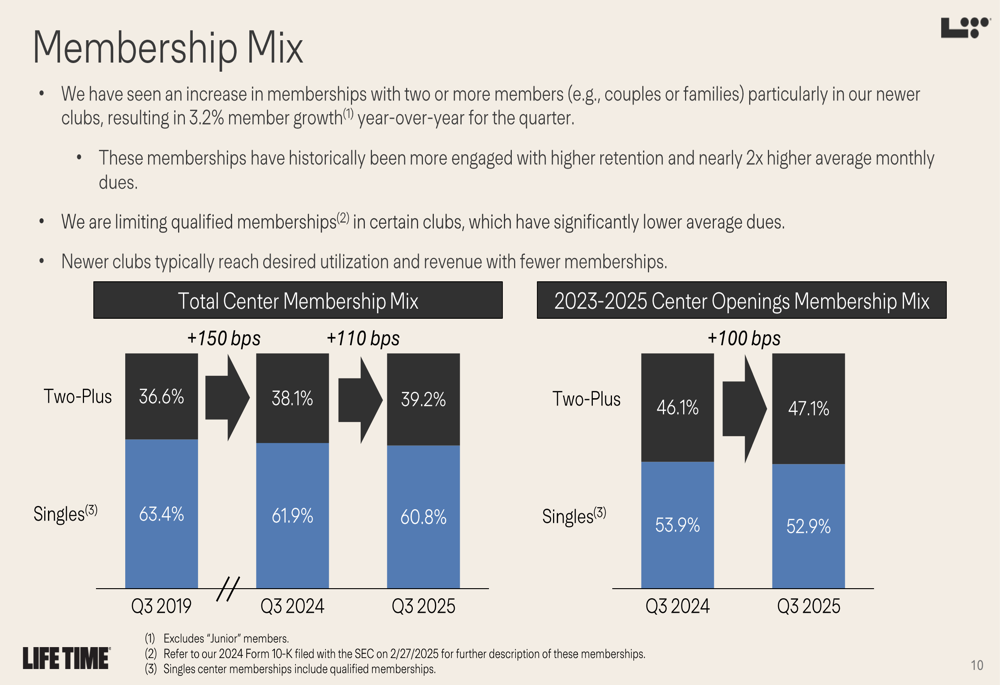

Life Time's presentation highlighted a strategic shift in membership composition, with an increasing focus on higher-value "Two-Plus" memberships (couples and families). This shift has been consistent across both established and newer clubs.

As shown in the following membership mix analysis, the percentage of Two-Plus memberships has increased from 36.6% in Q3 2019 to 39.2% in Q3 2025:

This trend is even more pronounced in newer clubs opened between 2023-2025, where Two-Plus memberships represented 47.1% of the total in Q3 2025, indicating the company's successful targeting of this more lucrative demographic in its expansion markets.

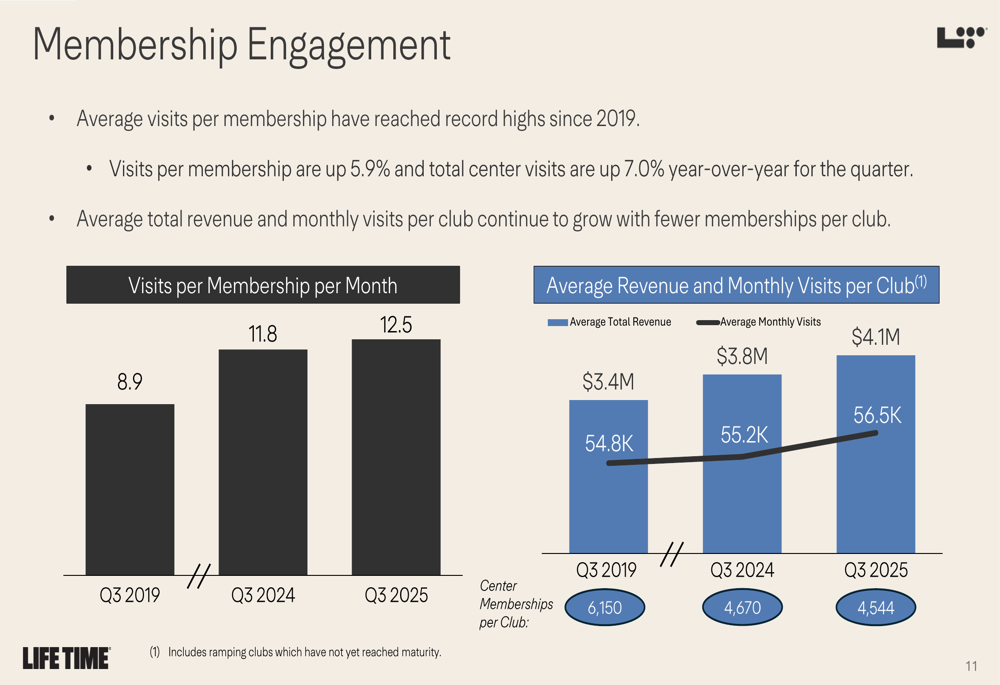

Member engagement metrics further validate Life Time's premium strategy, with significant increases in visits per membership and revenue per club:

The data shows visits per membership per month increasing from 8.9 in Q3 2019 to 12.5 in Q3 2025, a 40% improvement that indicates stronger member engagement. Simultaneously, average total revenue per club rose from $3.4 million to $4.1 million over the same period, while the number of memberships per club decreased, suggesting a successful shift toward higher-value, more engaged members.

Financial Performance

Life Time's Q3 2025 financial results exceeded market expectations, with the 12.9% revenue increase to $783 million driven by a 10.0% increase in average monthly dues and a 10.6% rise in comparable center revenue. The company's adjusted EBITDA reached $220 million, up 22% year-over-year, while net cash from operations increased 66% to $251 million.

These strong results prompted management to raise full-year guidance for comparable center revenue to 10.8%-11.0%, aligning with the company's long-term revenue growth algorithm presented in the earnings supplement.

The market responded positively to these results, with the stock trading at $25.75 in pre-market, representing a 3.54% increase. However, this remains well below the 52-week high of $34.99, suggesting potential upside if the company continues to execute on its growth strategy.

Forward-Looking Statements

Looking ahead, Life Time's presentation emphasized its continued focus on enhancing the customer experience while executing its accelerated expansion plans. The company's revenue growth algorithm targets consistent 10-12% annual growth, with contributions from both new club openings and improvements in existing center performance.

Management highlighted the importance of maintaining membership quality over quantity, as evidenced by the strategic limitation of qualified memberships in certain clubs to maintain average dues. This approach appears to be working, with the earnings report showing a 10.0% increase in average monthly dues.

While the presentation focused primarily on growth opportunities, potential investors should consider risks including economic downturns affecting consumer spending on premium wellness services, increased competition from boutique fitness studios, and possible supply chain disruptions that could affect the timely opening of new clubs.

Overall, Life Time's Q3 2025 presentation and corresponding financial results demonstrate a company successfully executing its premium wellness strategy, with accelerated expansion plans backed by strong operational performance and increasing member engagement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.