German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Light & Wonder Inc. (NASDAQ:LNW) presented its first quarter 2025 earnings results on May 7, 2025, highlighting continued operational momentum across its gaming, social casino, and iGaming segments. Despite reporting modest revenue growth, the company achieved double-digit increases in profitability metrics, demonstrating improved operational efficiency.

The gaming technology company’s stock reacted negatively in aftermarket trading, falling 2.52% to $91.27, despite the positive results presented. This suggests investors may have expected stronger performance following the company’s robust Q4 2024 results, when Light & Wonder beat EPS expectations by 51%.

Quarterly Performance Highlights

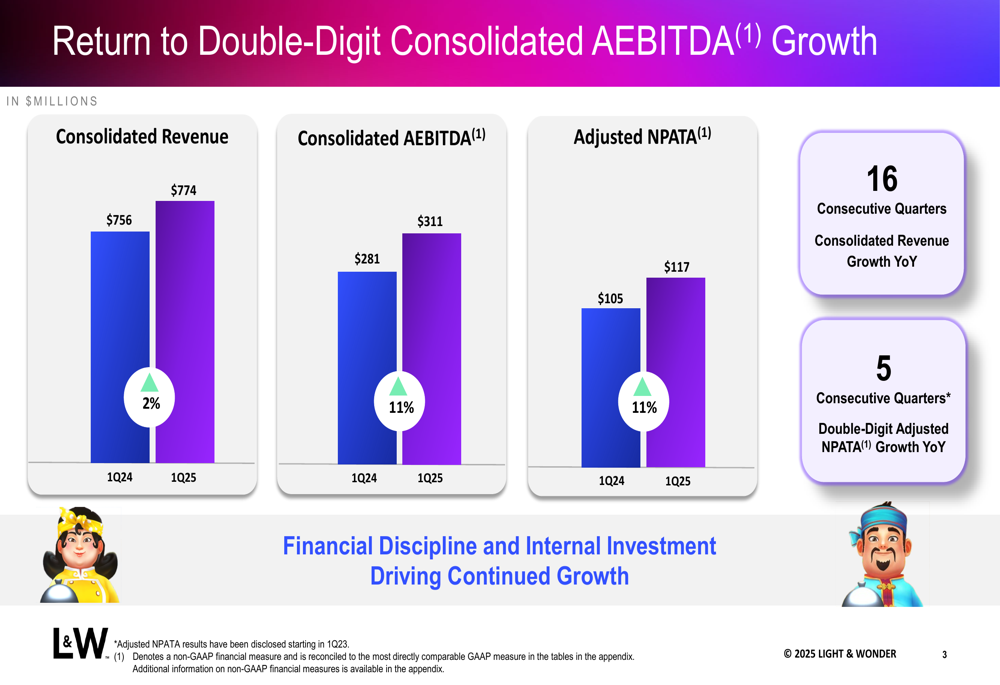

Light & Wonder reported consolidated revenue of $774 million for Q1 2025, representing a 2% year-over-year increase from $756 million in Q1 2024. More impressively, consolidated AEBITDA (Adjusted Earnings Before Interest, Taxes, Depreciation, and Amortization) grew 11% to $311 million, compared to $281 million in the prior year period.

As shown in the following chart of key financial metrics:

The company’s Adjusted NPATA (Net Profit After Tax and Amortization) increased 11% year-over-year to $117 million, while Adjusted NPATA per share jumped over 20% to $1.35 compared to $1.12 in the prior year period. Consolidated AEBITDA margin expanded 300 basis points to 40%, reflecting the company’s focus on operational efficiency.

Light & Wonder highlighted that Q1 2025 marked its 16th consecutive quarter of consolidated revenue growth year-over-year and 5th consecutive quarter of double-digit Adjusted NPATA growth.

Detailed Financial Analysis

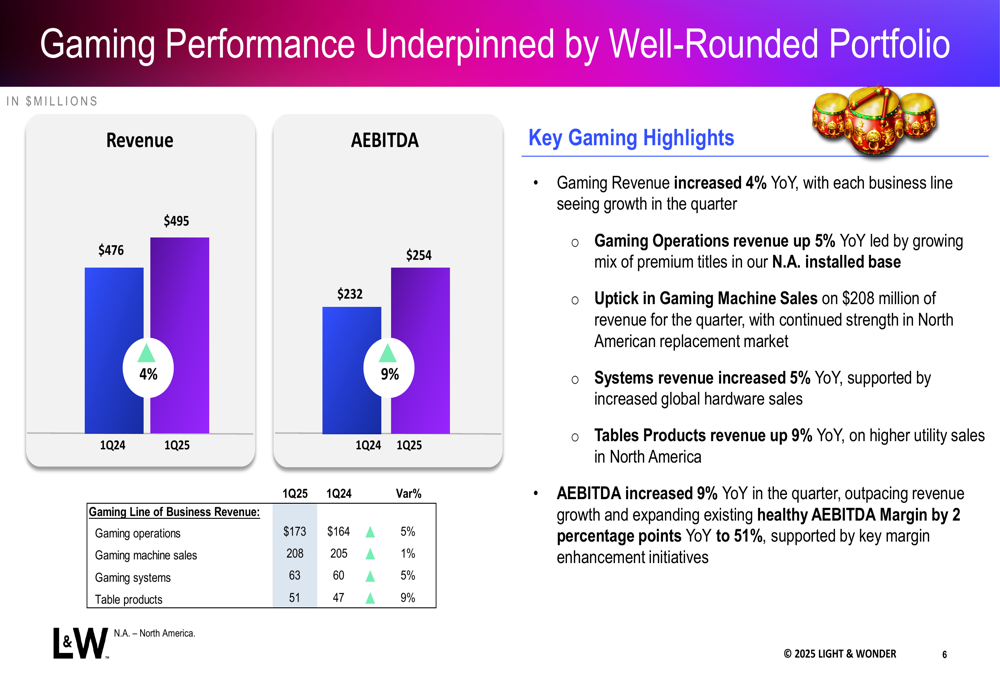

The Gaming segment showed solid performance with revenue increasing 4% year-over-year. Gaming Operations revenue rose 5%, Systems revenue grew 5%, and Table Products revenue increased 9% compared to Q1 2024. The segment’s AEBITDA increased 9% year-over-year to 51% with a two percentage point margin improvement.

The following breakdown illustrates the Gaming segment’s performance:

Key operational metrics in the Gaming segment remained strong, with North American installed base increasing 9% year-over-year to over 34,500 units. North American premium units grew for the 19th consecutive quarter, while North American unit shipments surged 30% year-over-year to over 5,750 units.

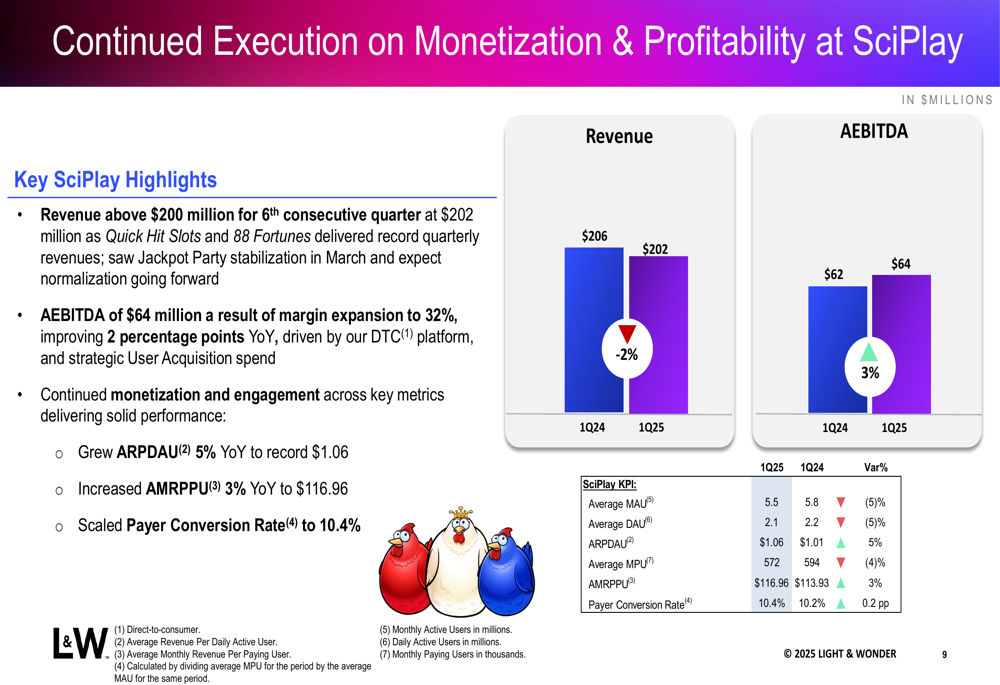

SciPlay (NASDAQ:SCPL), the company’s social casino business, maintained revenue above $200 million for the sixth consecutive quarter at $202 million. AEBITDA reached $64 million with margin expansion to 32%. Average Revenue Per Daily Active User (ARPDAU) grew 5% year-over-year to a record $1.06, while Average Monthly Revenue Per Paying User (AMRPPU) increased 3% to $116.96.

The following chart details SciPlay’s performance metrics:

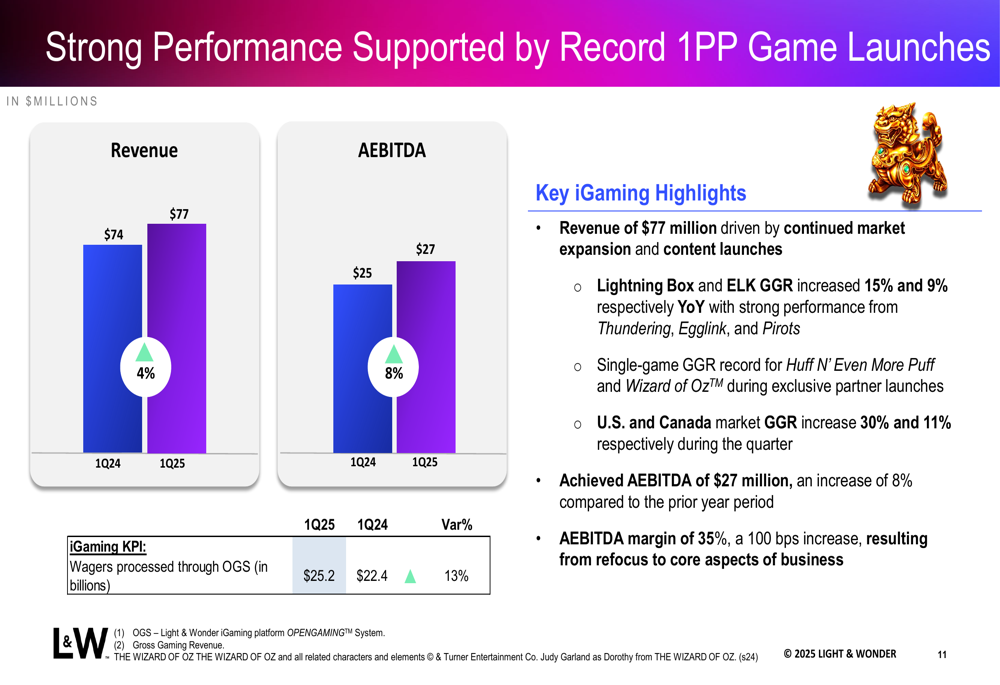

The iGaming segment reported revenue of $77 million, driven by continued market expansion and content launches. U.S. and Canada market Gross Gaming Revenue (GGR) increased 30% and 11% respectively during the quarter. The segment achieved AEBITDA of $27 million, an 8% increase compared to the prior year period, with AEBITDA margin expanding 100 basis points to 35%.

The following chart highlights iGaming’s strong performance:

Free Cash Flow generation remained robust at $111 million in the quarter, up 19% compared to $93 million in the prior year period. This improvement was primarily driven by increased net cash provided by operating activities, which rose to $185 million from $171 million in Q1 2024.

Strategic Initiatives

Light & Wonder continues to optimize its capital structure, ending the quarter with a principal face value of debt outstanding of $3.9 billion and a net debt leverage ratio of 3.0x, a significant improvement from 6.2x in Q4 2021. Interest expense decreased 9% year-over-year, from $75 million in Q1 2024 to $68 million in Q1 2025.

The company returned $166 million to shareholders in Q1 2025 through share repurchases, completing approximately 45% of its total $1 billion program authorization. Additionally, Light & Wonder’s lead arranger has received commitments for a three-year $800 million Term Loan A credit facility for financing the pending Grover Gaming Acquisition.

In the Gaming segment, Light & Wonder is capitalizing on its strong content and hardware roadmap. The company highlighted several successful game launches, including:

For iGaming, the company is fueling growth through an extensive content roadmap for the first half of 2025, focusing on releases in the UK, Canada, and US markets. Lightning Box and ELK studios showed particularly strong performance with GGR increases of 15% and 9% respectively year-over-year.

Forward-Looking Statements

While Light & Wonder did not provide specific guidance for the remainder of 2025 in this presentation, the company’s Q4 2024 earnings call had targeted an EBITDA of $1.4 billion for 2025. With Q1 2025 AEBITDA of $311 million, the company appears to be on track to meet this target if it maintains similar performance throughout the year.

The company’s business resiliency and continued growth across all segments position it well for sustainable long-term growth. However, investors will likely monitor revenue growth closely in upcoming quarters, as the modest 2% increase in Q1 2025 represents a slowdown from the 4% growth reported in Q4 2024 and 10% for full-year 2024.

Light & Wonder’s strategic focus on internal investment and financial discipline continues to drive margin expansion and profitability improvements, even as revenue growth moderates. The company’s ability to generate strong free cash flow while simultaneously reducing debt and returning capital to shareholders demonstrates its financial strength and operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.