5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Lithia Motors Inc. (NYSE:LAD), the largest automotive retailer in the United States, presented its updated investor strategy on July 29, 2025, following strong second-quarter results that saw the company’s stock rise 3.54% to $302.59. The presentation outlined Lithia’s progress toward becoming a more diversified, digitally-enabled automotive retailer with ambitious long-term revenue targets.

The company’s Q2 2025 performance validated its strategic direction, with record revenue of $9.6 billion representing a 4% year-over-year increase in same-store sales. Diluted earnings per share rose to $9.87, with adjusted EPS of $10.24 reflecting 25-30% growth compared to the previous year.

As shown in the following highlights chart, Lithia has maintained impressive 10-year growth rates across key metrics, positioning itself as a leader in the fragmented automotive retail market:

Strategic Growth Initiatives

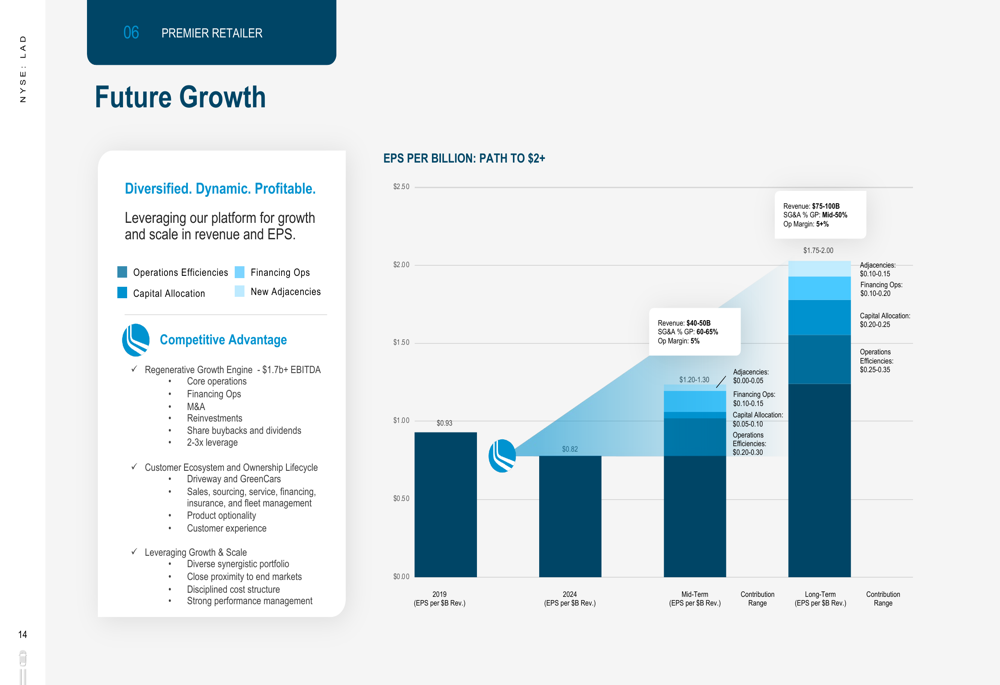

Lithia Motors has established a clear roadmap for growth, progressing from $36.2 billion in revenue for 2024 toward mid-term targets of $40-50 billion and long-term ambitions of $75-100 billion. This growth strategy is supported by improving operational efficiency, with SG&A as a percentage of gross profit projected to decrease from 67% in 2024 to the mid-50s long-term, while operating margins are expected to expand from 4.4% to over 5%.

The company’s path to achieving $2+ EPS per billion in revenue is illustrated in this strategic growth chart:

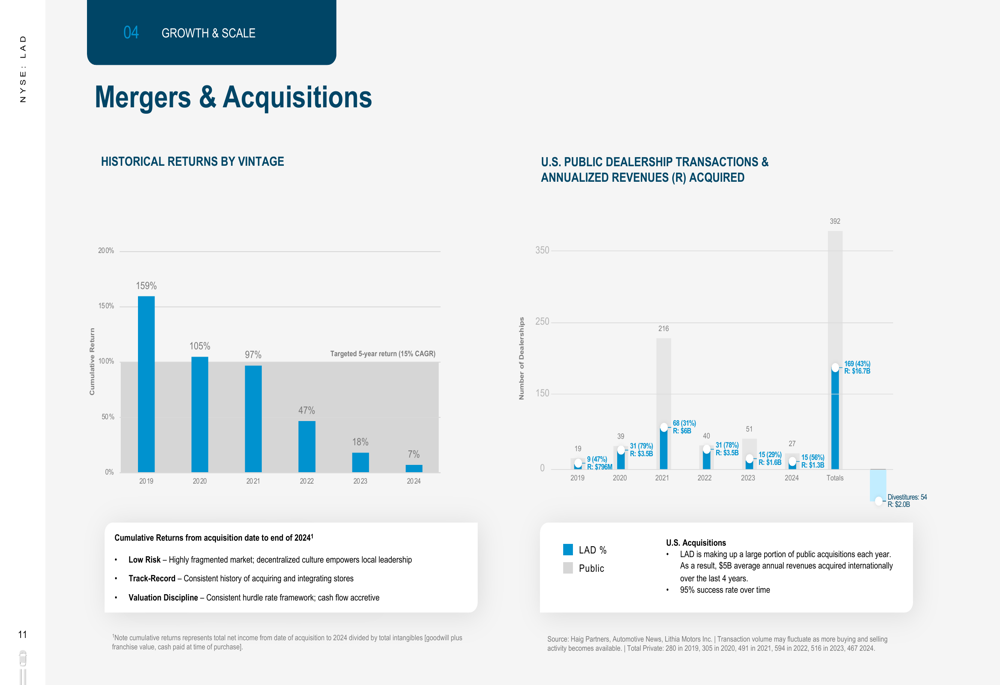

Mergers and acquisitions remain a cornerstone of Lithia’s growth strategy. The company has acquired an average of $5 billion in annual revenues internationally over the past four years, with strong returns on these investments. As shown in the following M&A performance chart, Lithia has consistently captured a significant portion of public dealership transactions:

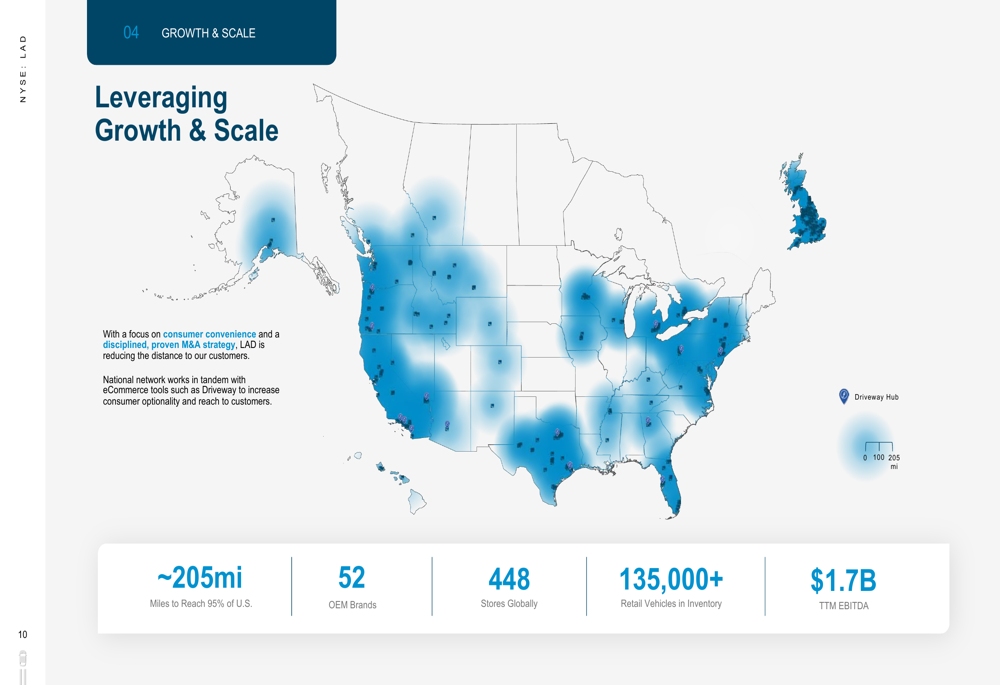

Lithia’s national expansion has resulted in a network of 448 stores globally representing 52 OEM brands, with an inventory of over 135,000 retail vehicles. The company’s geographic distribution provides access to 95% of the U.S. population within approximately 205 miles:

Digital Transformation & Diversification

Central to Lithia’s strategy is its consumer ecosystem, designed to create lifetime customer relationships through an integrated approach to automotive retail, financing, and services. This ecosystem encompasses traditional dealerships under the Lithia brand, the digital Driveway platform, GreenCars for electric vehicles, and various other business segments:

The Driveway digital platform has gained significant traction, with customers purchasing 90,000 vehicles through the digital ecosystem in the first six months of 2025. The platform averaged 1.3 million unique visitors per month in Q2 2025, contributing to Lithia’s omnichannel sales approach, which accounted for 25.5% of vehicles sold during the quarter.

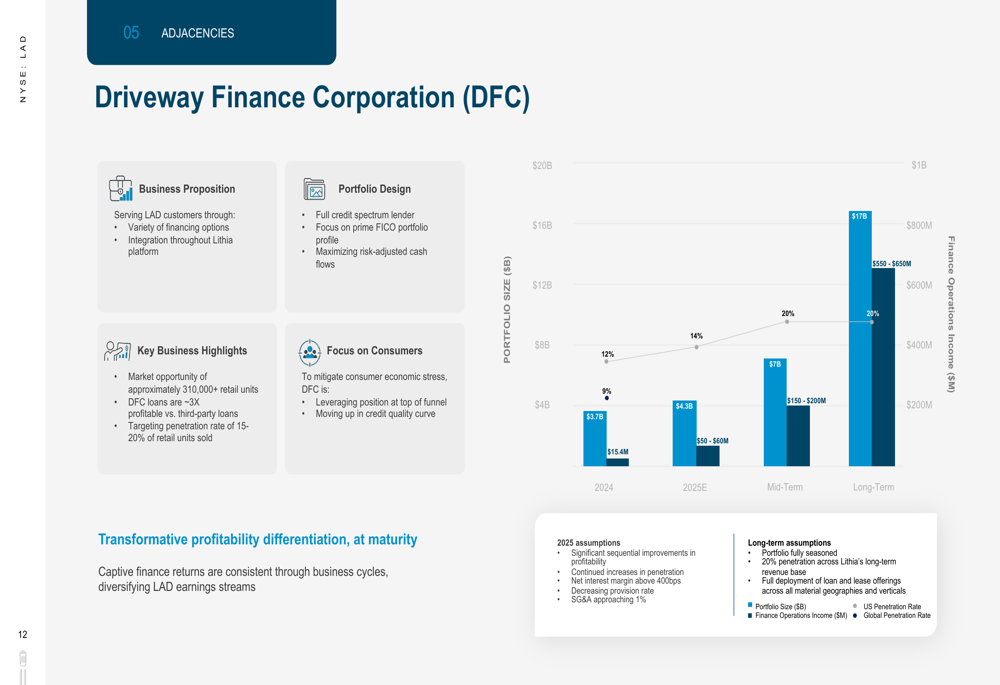

Driveway Finance Corporation (DFC) represents a key growth adjacency for Lithia, with the portfolio expanding from $3.7 billion in 2024 to $4.3 billion in 2025. The financial services division has seen dramatic improvement in profitability, with finance operations income projected to reach $50-60 million in 2025, up from $15.4 million in 2024. Long-term, Lithia targets a $17 billion DFC portfolio generating $550-650 million in finance operations income:

Financial Performance & Outlook

Lithia’s Q2 2025 financial results demonstrate the effectiveness of its strategy, with adjusted EBITDA reaching $489 million, representing a 20% year-over-year increase. The company’s financing operations income showed particularly strong growth, increasing from $7 million to $20 million.

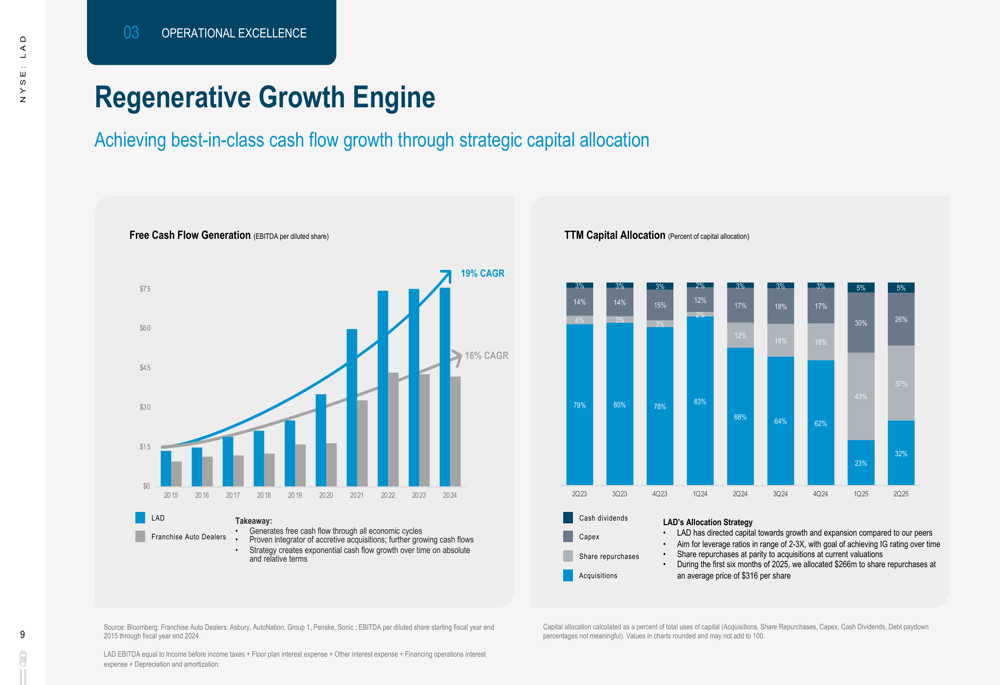

The company’s capital allocation strategy prioritizes high-return investments while returning value to shareholders. As illustrated in the following chart, Lithia has shifted its capital allocation mix to include more share repurchases, which now account for 37% of capital deployment compared to 17% in Q2 2023:

Management has indicated plans to accelerate share buybacks, using up to 50% of free cash flow, with CEO Bryan DeBoer emphasizing this commitment by stating, "We’re going to back up the truck and continue to buy shares back."

Competitive Positioning & Challenges

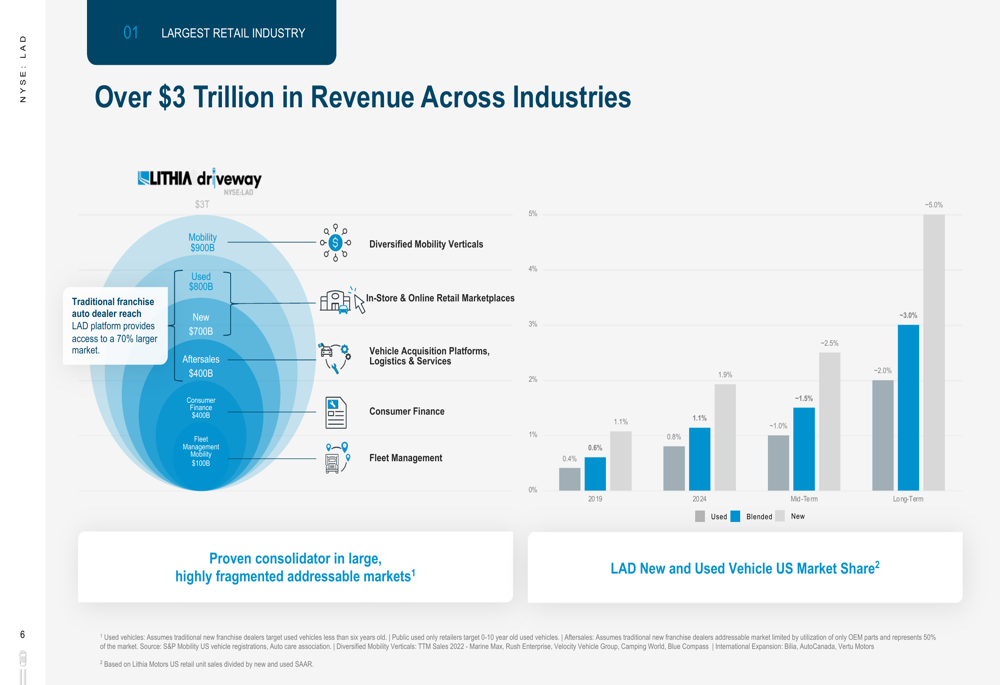

Lithia operates in a massive market, with an addressable opportunity of over $3 trillion across various automotive segments. The company’s current U.S. market share is approximately 2% on a blended basis, with higher penetration in new vehicles (~5%) and room for growth in used vehicles (~3%):

The company’s business model is designed to be resilient through diversification across vehicle types, brands, and revenue streams. Lithia’s new vehicle mix is well-balanced, with import brands accounting for 42% of sales, luxury brands for 32%, and domestic brands for 26%.

Despite strong performance, Lithia faces several challenges, including potential tariff impacts on vehicle pricing and affordability, competition from Chinese OEMs entering markets like the UK, supply chain disruptions, and economic uncertainties affecting consumer spending. The company’s operational optimization initiatives aim to address these challenges by improving efficiency and reducing costs.

Looking forward, Lithia is targeting $2-4 billion in annual acquired revenues and aims to increase DFC penetration from 15% to 20%. The company also expects a full rollout of its Pinewood AI partnership by 2027-2028, further enhancing its technological capabilities and operational efficiency.

With a strong financial foundation evidenced by a healthy current ratio of 1.22 and an Altman Z-Score of 3.07, Lithia Motors appears well-positioned to execute its ambitious growth strategy while navigating the evolving automotive retail landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.