Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

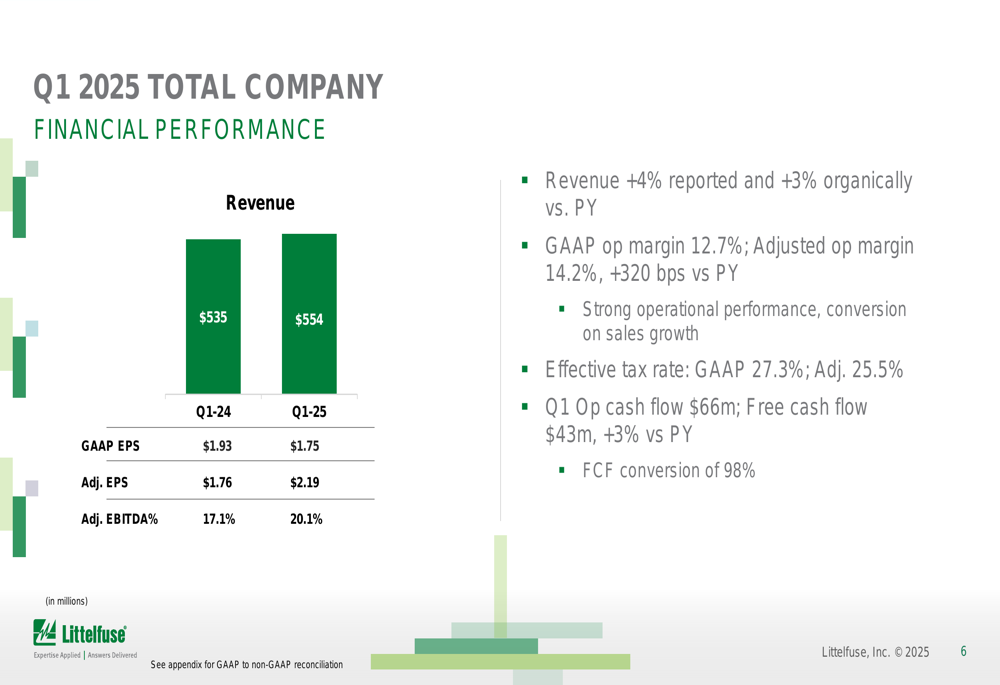

Littelfuse Inc (NASDAQ:LFUS) released its Q1 2025 earnings presentation on April 29, showcasing strong performance that exceeded prior guidance. The electrical protection and power control solutions provider reported a 4% year-over-year revenue increase to $554 million, while adjusted earnings per share jumped 24.4% to $2.19.

The market responded enthusiastically to these results, with Littelfuse shares surging 8.72% in after-hours trading to $194.80, following a relatively flat regular session that closed at $179.04.

The quarter marks the debut of new CEO Dr. Greg Henderson, who outlined his priorities for the company’s future growth while highlighting Littelfuse’s strengthening position in data center infrastructure.

Quarterly Performance Highlights

Littelfuse delivered significant margin improvement across all business segments in Q1 2025. The company achieved an adjusted operating margin of 14.2%, representing a 320 basis point increase compared to the prior year. Adjusted EBITDA margin expanded to 20.1% from 17.1% a year earlier.

As shown in the following chart of the company’s financial performance:

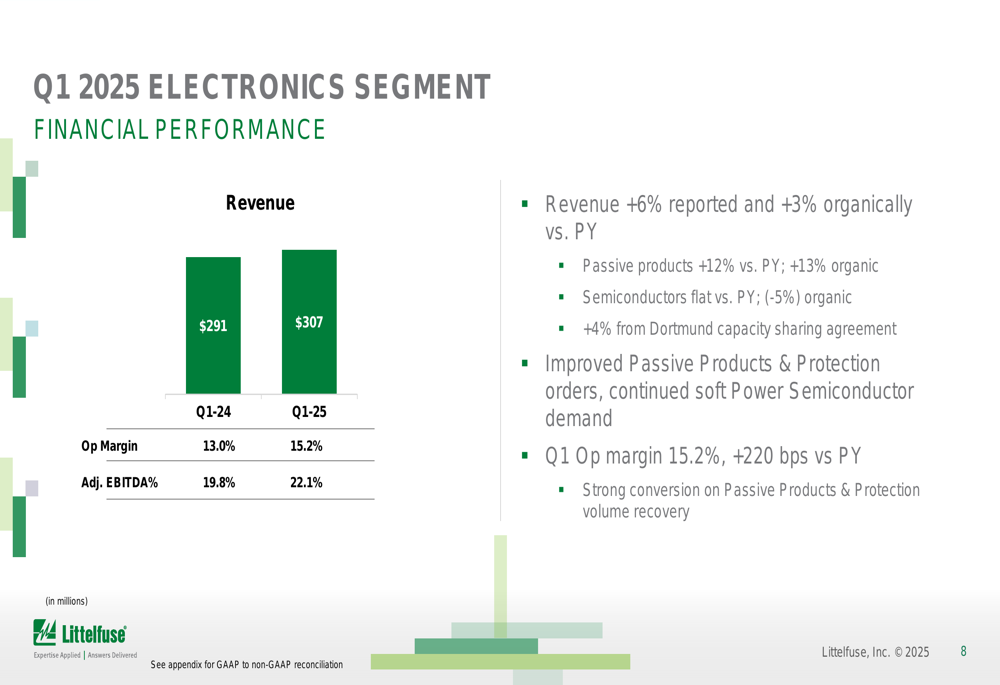

The Electronics segment, Littelfuse’s largest business unit, posted revenue of $307 million, up 6% reported and 3% organically year-over-year. Within this segment, passive products grew impressively at 12% (13% organically), while semiconductors remained flat on a reported basis but declined 5% organically. The segment’s operating margin improved to 15.2%, a 220 basis point increase from Q1 2024.

The segment breakdown reveals strong execution in Electronics:

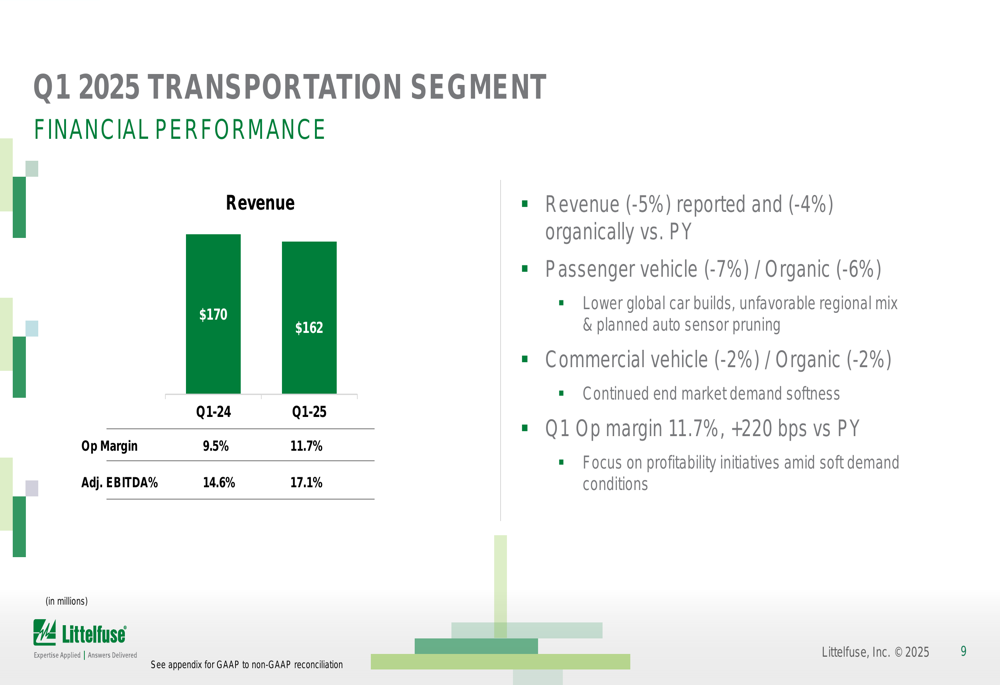

Despite challenging market conditions, the Transportation segment demonstrated improved profitability. While revenue decreased 5% to $162 million due to lower global car builds and unfavorable regional mix, operating margin expanded by 220 basis points to 11.7%. The company attributed this improvement to ongoing profitability initiatives amid soft demand conditions.

The Transportation segment metrics show margin improvement despite revenue decline:

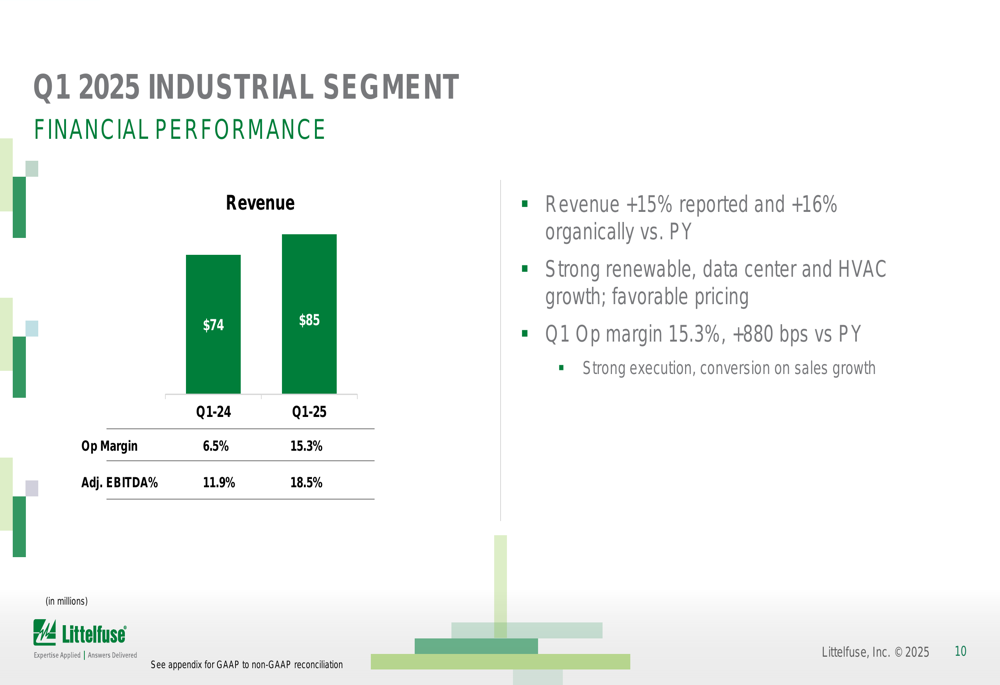

The Industrial segment emerged as the standout performer, with revenue surging 15% to $85 million, driven by strong growth in renewable energy, data centers, and HVAC applications. Operating margin in this segment skyrocketed by 880 basis points to 15.3%, reflecting exceptional execution and conversion on sales growth.

The Industrial segment’s impressive performance is illustrated here:

Strategic Initiatives

Dr. Greg Henderson, who recently took the helm as CEO, outlined his observations and priorities for Littelfuse. He emphasized the company’s leadership in developing smart solutions for electrical energy transfer, its talented team, well-positioned global operating model, and history of strong profitability.

The new CEO’s strategic vision includes:

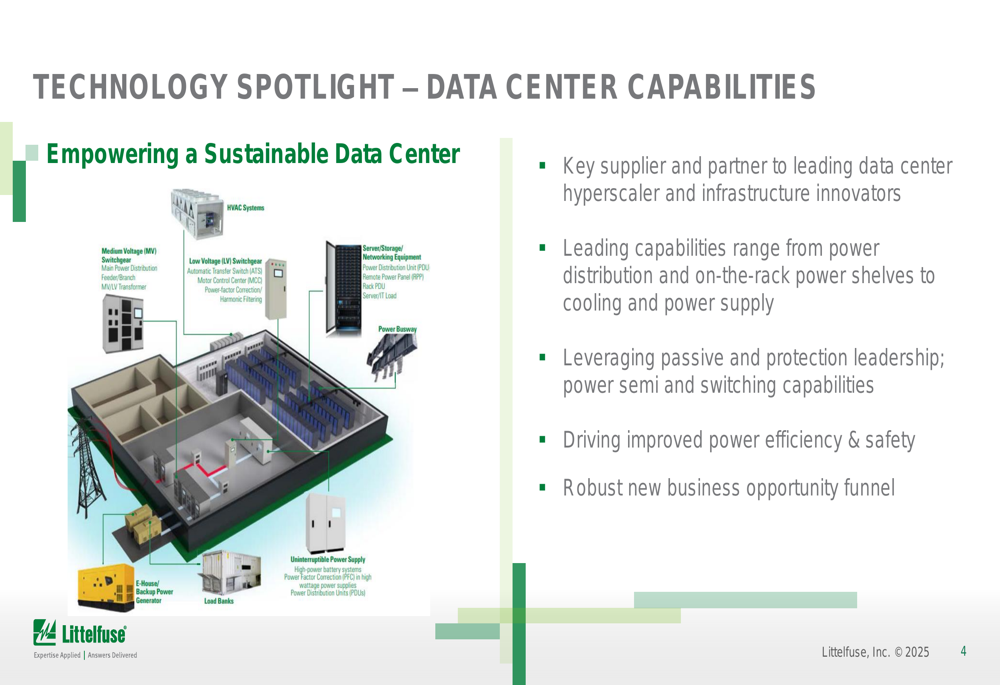

A key strategic focus highlighted in the presentation is Littelfuse’s expanding role in data center infrastructure. The company positioned itself as a crucial supplier to leading data center hyperscalers and infrastructure innovators, with capabilities spanning power distribution, cooling, and power supply components.

The data center opportunity is illustrated in this technical overview:

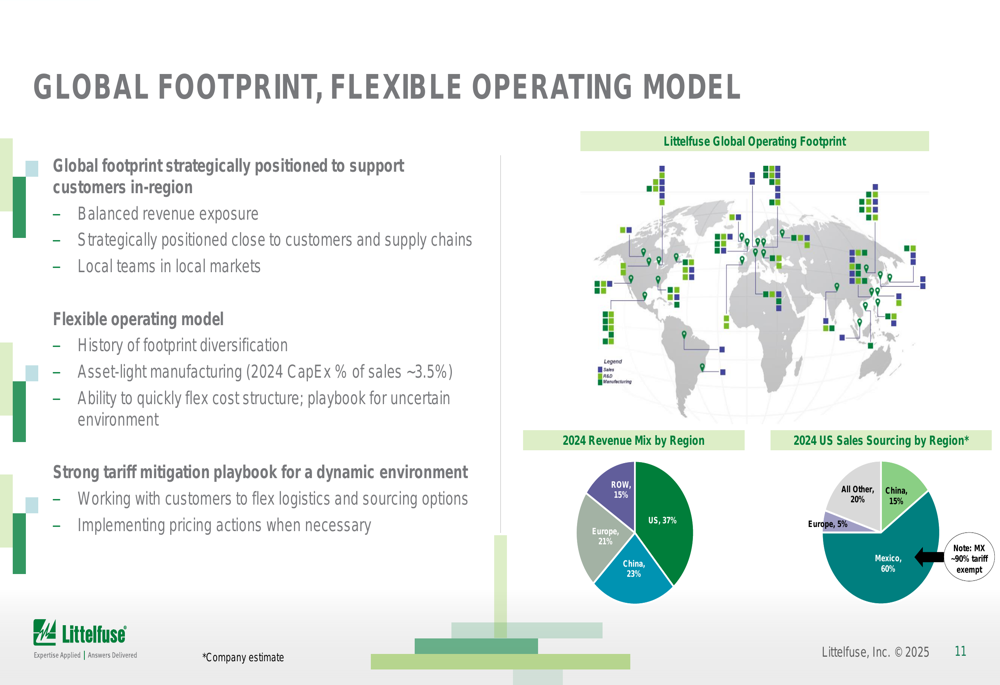

Littelfuse also emphasized its flexible global operating model as a competitive advantage. With strategically positioned manufacturing facilities and an asset-light approach (capital expenditures at approximately 3.5% of sales), the company maintains the ability to quickly adapt its cost structure to changing market conditions. This flexibility includes a comprehensive tariff mitigation playbook, which has become increasingly important in the current trade environment.

The global footprint breakdown shows balanced regional exposure:

Forward-Looking Statements

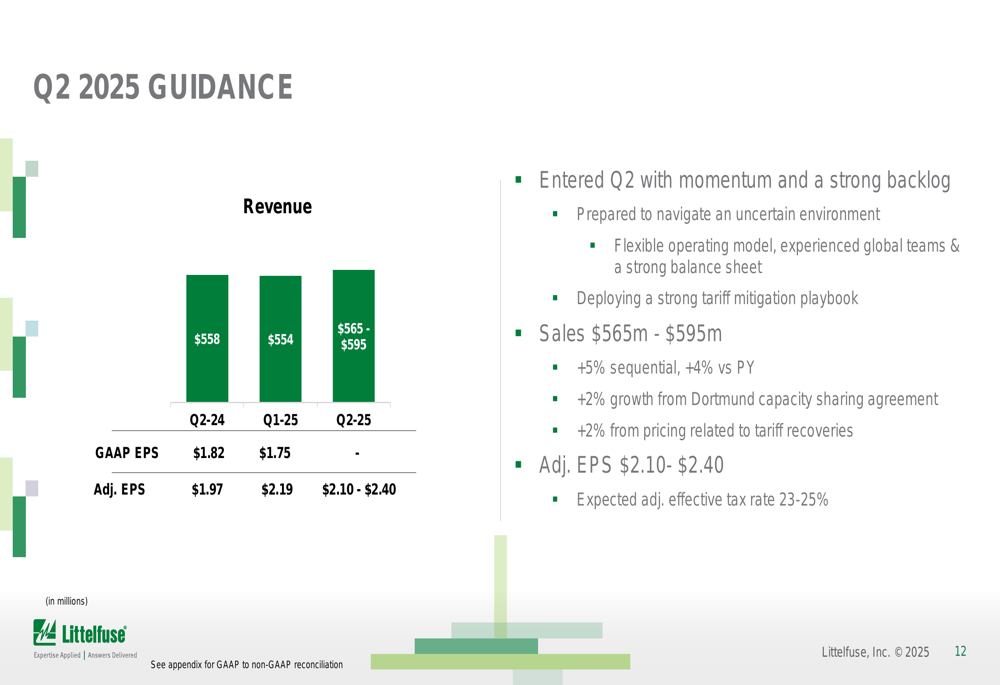

Looking ahead to Q2 2025, Littelfuse provided optimistic guidance, projecting sales of $565-595 million, representing a 5% sequential increase and 4% year-over-year growth. This includes a 2% contribution from the Dortmund capacity sharing agreement and 2% from pricing related to tariff recoveries. Adjusted EPS is expected to range between $2.10 and $2.40.

The Q2 guidance shows continued momentum:

For the full year 2025, Littelfuse expects the Dortmund capacity sharing agreement to contribute 2% to company sales with a neutral EPS impact. Foreign exchange and commodities are projected to provide a 1% tailwind to sales and approximately $0.40 benefit to EPS, with a 60 basis point margin benefit at current rates.

The company anticipates generating approximately 100% free cash flow conversion for the year while investing $90-95 million in capital expenditures. Management emphasized its focus on "executing through an uncertain environment while not losing sight of strategic priorities."

Detailed Financial Analysis

Littelfuse demonstrated strong cash generation in Q1, with operating cash flow of $66 million and free cash flow of $43 million, up 3% year-over-year. The company achieved a free cash flow conversion rate of 98%, reflecting efficient working capital management.

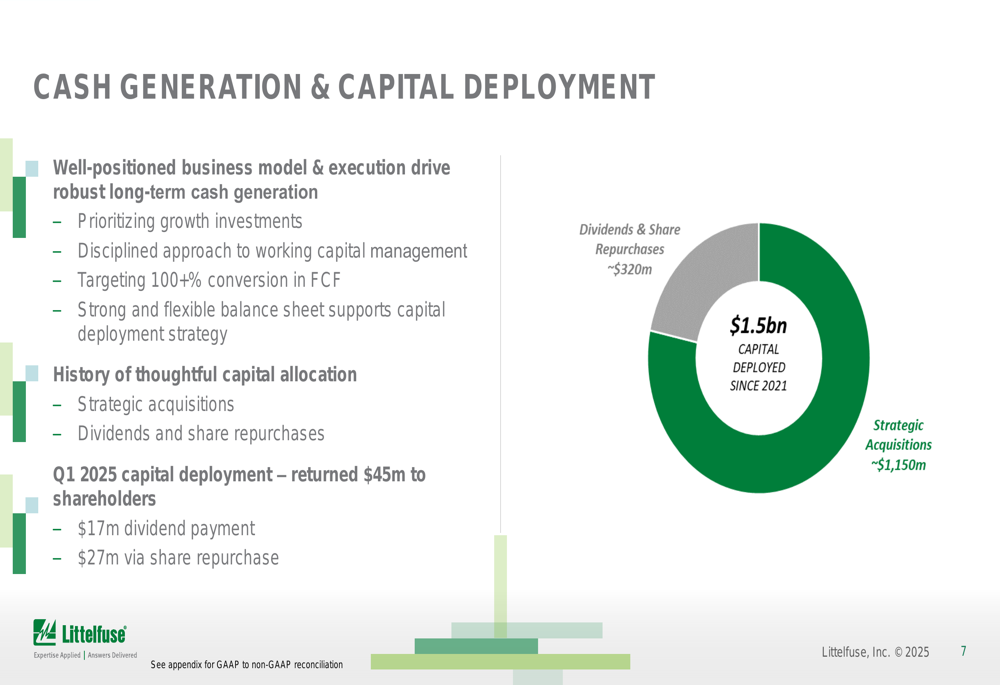

The company’s capital deployment strategy prioritizes growth investments while maintaining shareholder returns. In Q1 2025, Littelfuse returned $45 million to shareholders through $17 million in dividend payments and $27 million in share repurchases. Since 2021, the company has deployed approximately $1.5 billion in capital, with about $1.15 billion directed toward strategic acquisitions and $320 million returned to shareholders.

The capital allocation strategy is visualized here:

Littelfuse maintains a strong balance sheet with a consolidated total debt of $805.7 million as of March 29, 2025. With consolidated EBITDA of $470.4 million for the trailing twelve months, the company’s net leverage ratio stands at a comfortable 1.3x, providing financial flexibility for future investments and navigating economic uncertainties.

This financial strength represents a significant improvement from the previous quarter. In Q4 2024, Littelfuse had missed EPS forecasts but slightly exceeded revenue expectations. The strong Q1 2025 performance suggests the company’s operational improvements and strategic initiatives are gaining traction, particularly in margin expansion across all business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.