Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Littelfuse Inc. (NASDAQ:LFUS) reported strong second-quarter 2025 results on July 30, with revenue and earnings exceeding guidance, though the stock dipped slightly in aftermarket trading. The electronic component manufacturer saw growth across all segments and exited the quarter with its strongest bookings since the first half of 2022.

Quarterly Performance Highlights

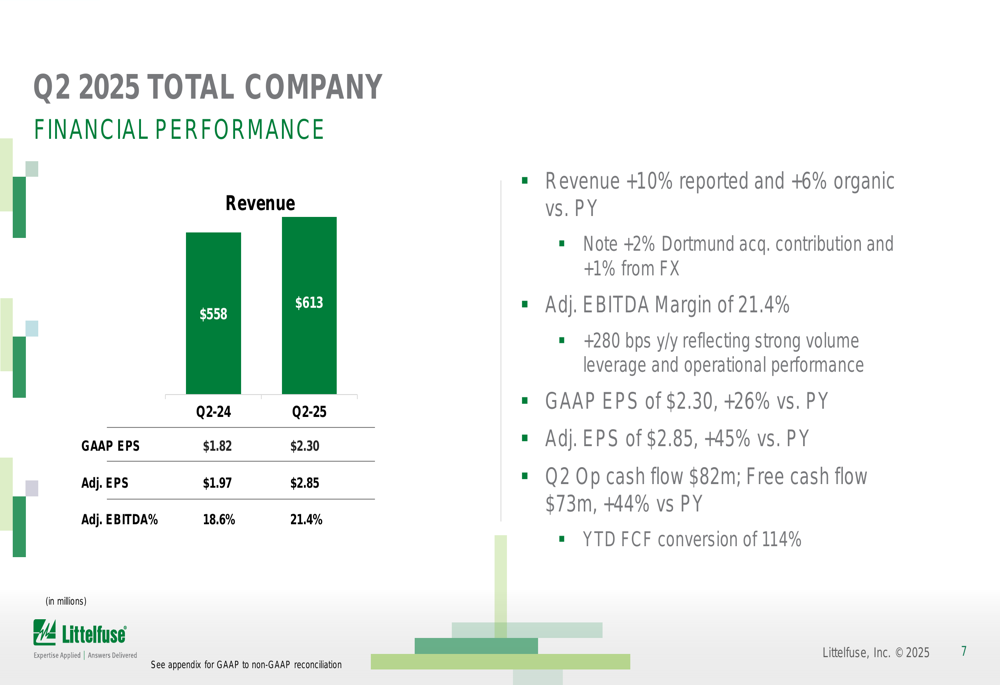

Littelfuse delivered $613 million in Q2 2025 revenue, representing a 10% increase from the prior year, with organic growth of 6%. The company’s adjusted earnings per share jumped 45% to $2.85, while GAAP EPS rose 26% to $2.30. Adjusted EBITDA margin expanded significantly to 21.4%, an improvement of 280 basis points year-over-year.

"Strong second quarter performance with sales and EPS exceeding the high end of the guide," the company noted in its presentation, attributing the upside to "stronger volumes and leverage, as well as solid operational execution."

As shown in the following financial performance chart:

Free cash flow generation was particularly impressive at $73 million, up 44% compared to the previous year, with year-to-date free cash flow conversion reaching 114%. The company returned $17 million to shareholders via dividend payments during the quarter.

Despite these strong results, Littelfuse stock declined 0.95% to $252.09 in aftermarket trading following the earnings release, according to market data.

Segment Performance

All three of Littelfuse’s business segments contributed to the quarter’s growth, with the Industrial segment showing the strongest performance.

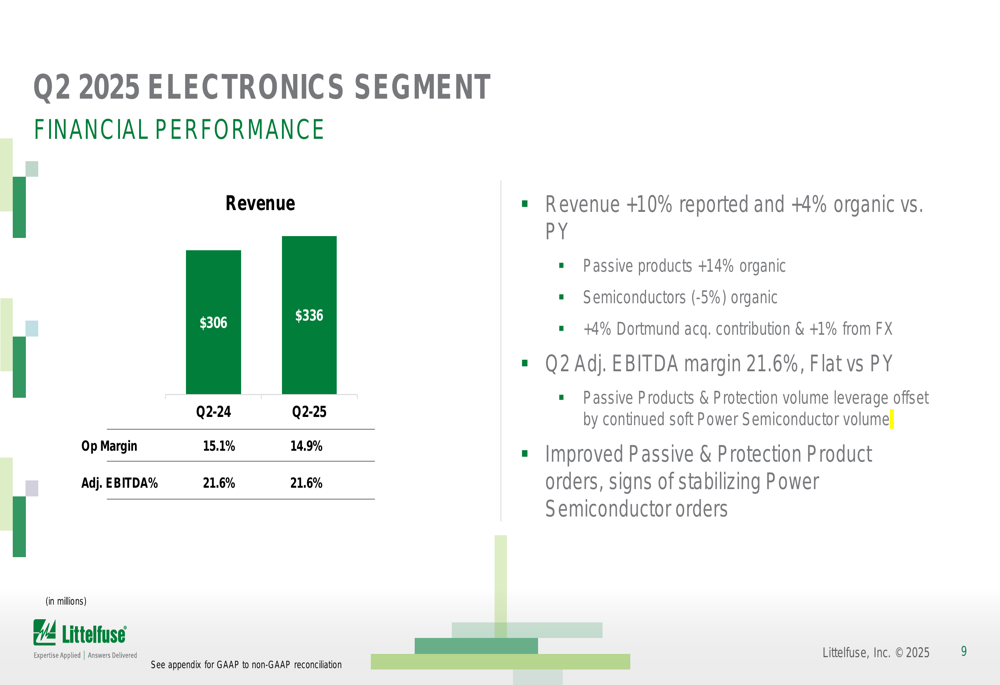

The Electronics segment, which accounts for the largest portion of revenue, generated $336 million, up 10% reported and 4% organic year-over-year. Passive products led the growth with a 14% organic increase, while semiconductors declined 5% organically. The segment’s adjusted EBITDA margin remained flat at 21.6% compared to the prior year.

The Electronics segment performance is illustrated here:

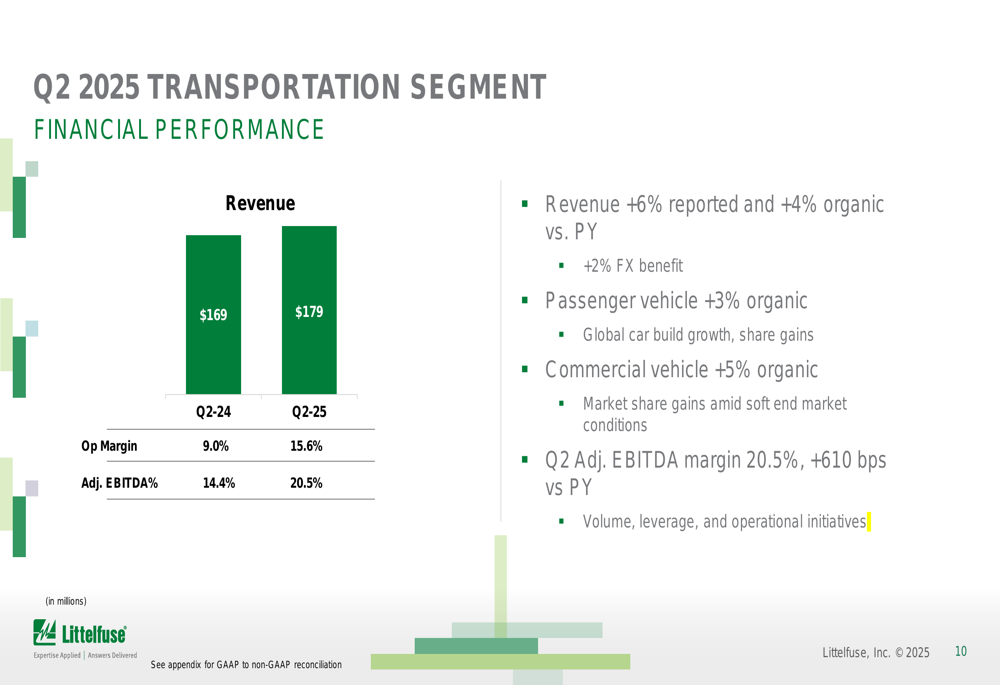

The Transportation segment delivered $179 million in revenue, increasing 6% reported and 4% organic versus Q2 2024. Passenger vehicle sales rose 3% organically, benefiting from global car build growth and share gains, while commercial vehicle revenue grew 5% organically despite soft end market conditions. The segment’s adjusted EBITDA margin improved dramatically to 20.5%, up 610 basis points year-over-year.

As shown in the Transportation segment results:

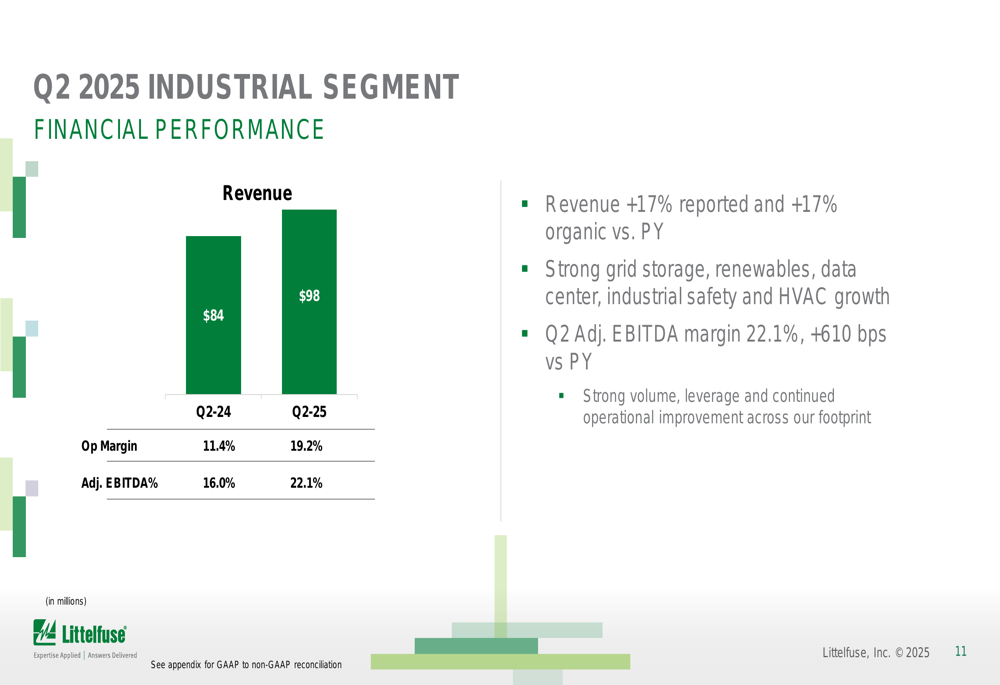

The Industrial segment posted the strongest growth, with revenue of $98 million representing a 17% increase both reported and organic. The company cited "strong grid storage, renewables, data center, industrial safety and HVAC growth" as key drivers. The segment’s adjusted EBITDA margin expanded to 22.1%, up 610 basis points from Q2 2024.

The Industrial segment’s performance is detailed below:

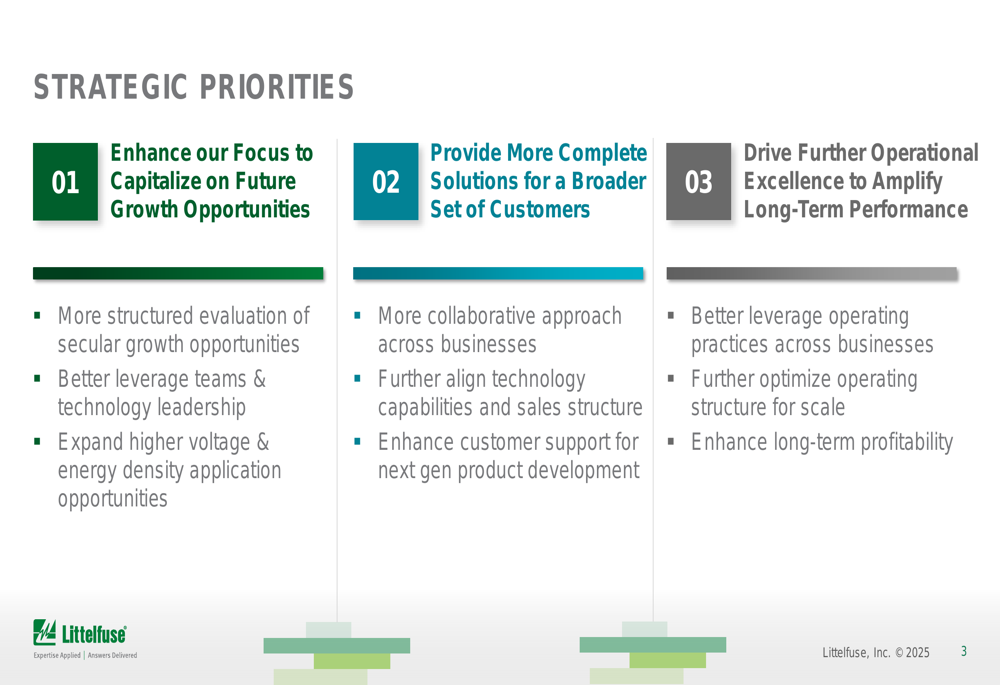

Strategic Initiatives

Littelfuse outlined three strategic priorities aimed at driving long-term growth and operational excellence. These include enhancing focus on future growth opportunities, providing more complete solutions for a broader customer base, and driving operational excellence to improve long-term performance.

The company’s strategic roadmap emphasizes structured evaluation of secular growth opportunities, expanding into higher voltage and energy density applications, and better leveraging technology leadership across the organization.

As detailed in the strategic priorities slide:

The company also highlighted its competitive advantages, including core market leadership in enabling safe and efficient electrical energy transfer, broad multi-technology product offerings, and trusted expertise with customers.

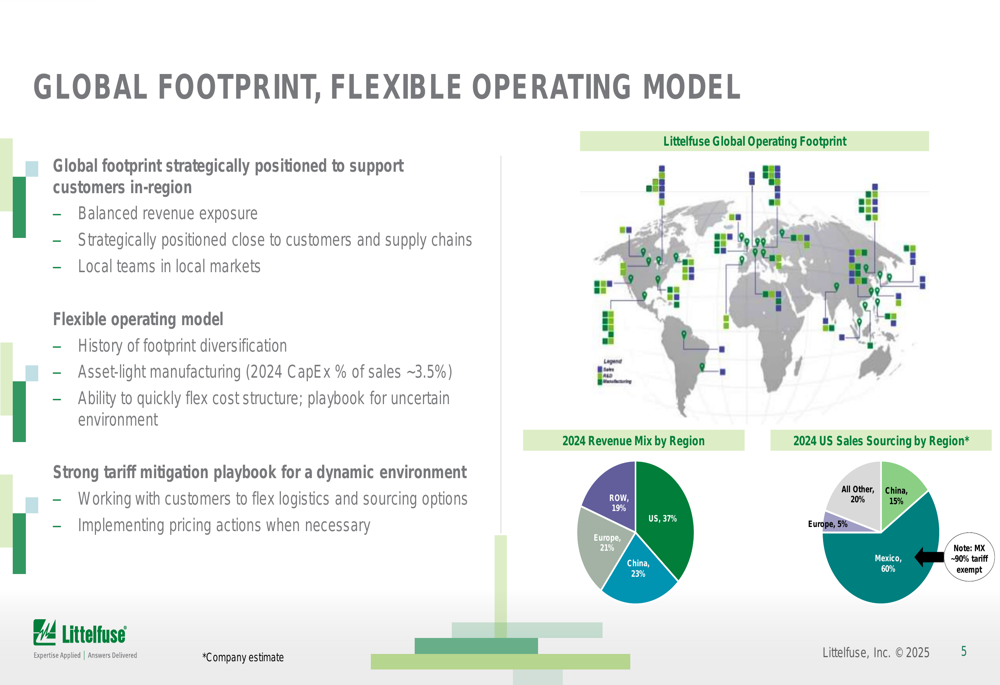

Global Operations

Littelfuse emphasized its strategically positioned global footprint and flexible operating model as key competitive advantages. The company’s revenue is geographically diverse, with 37% from the US, 23% from China, 21% from Europe, and 19% from the rest of the world.

Notably, the company has diversified its manufacturing footprint, with 60% of US sales sourced from Mexico, 15% from China, 15% from other regions, and 5% from Europe. This diversification provides resilience against trade tensions and supply chain disruptions.

The company’s global presence is illustrated in this breakdown:

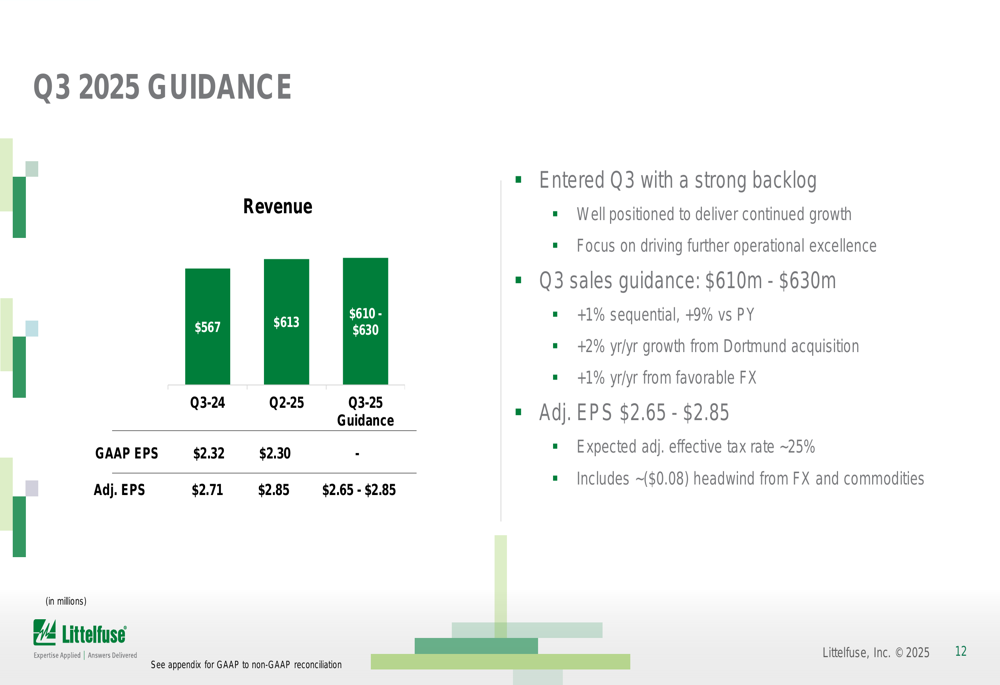

Forward-Looking Statements

Looking ahead to Q3 2025, Littelfuse provided guidance for sales between $610 million and $630 million, representing approximately 9% year-over-year growth. The company expects adjusted EPS between $2.65 and $2.85, with an anticipated adjusted effective tax rate of approximately 25%.

The Q3 guidance is visualized in the following chart:

For the full year 2025, Littelfuse expects the Dortmund acquisition to contribute approximately 2% to company sales growth, though with a neutral EPS impact. Foreign exchange and commodities are anticipated to provide a 1% tailwind to sales and approximately $0.14 benefit to EPS.

The company projects capital expenditures of $90-95 million for the year and expects approximately 100% free cash flow conversion.

"We entered Q3 with a strong backlog and are well positioned to deliver continued growth, focusing on driving further operational excellence," the company stated in its outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.