Nvidia pushes back on AI bubble narrative as Blackwell drives Q3 beat

Introduction & Market Context

Logista (BME:LOG) released its full-year 2025 results on November 6, 2025, revealing a mixed performance with growing revenues but declining profits. The company's stock showed a modest reaction, rising 0.66% to €28.88 following the presentation, as investors weighed positive revenue growth against profit challenges.

The logistics and distribution company operates primarily across Iberia, Italy, and France, facing varying market conditions in each region. While tobacco volumes declined across all markets, the company benefited from price increases and tax changes that boosted inventory profits.

Executive Summary

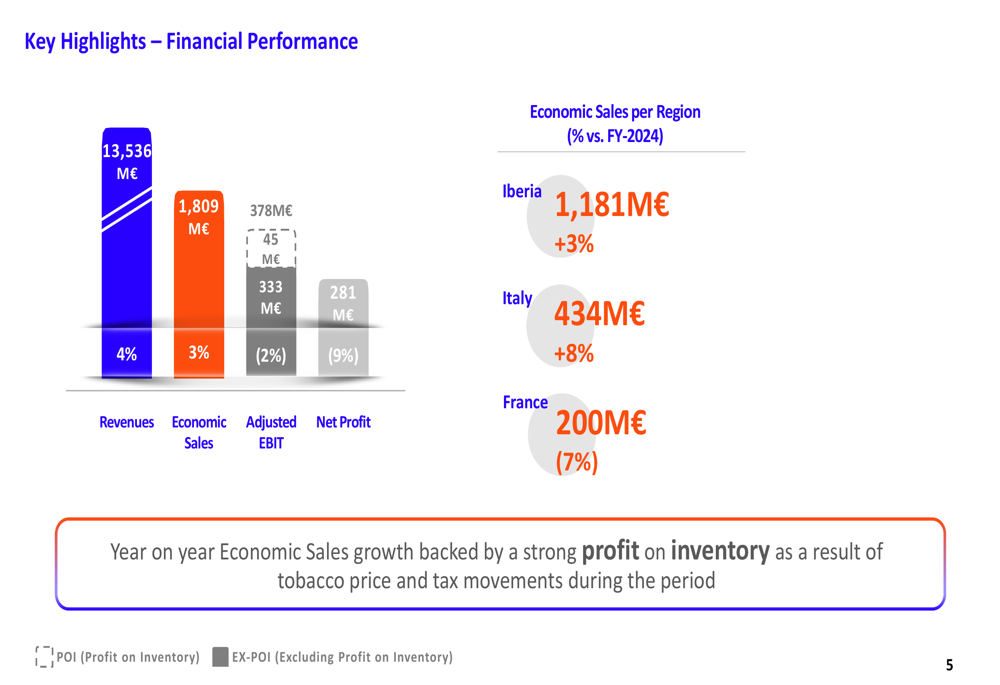

Logista reported a 4% increase in revenues to €13,536 million and a 3% rise in economic sales to €1,809 million for FY2025. However, adjusted EBIT declined by 2% to €378 million, and net profit fell more significantly by 9% to €281 million. Despite these profit challenges, the company achieved a substantial improvement in free cash flow, which more than doubled to €483 million from €225 million in the previous year.

As shown in the following financial performance highlights:

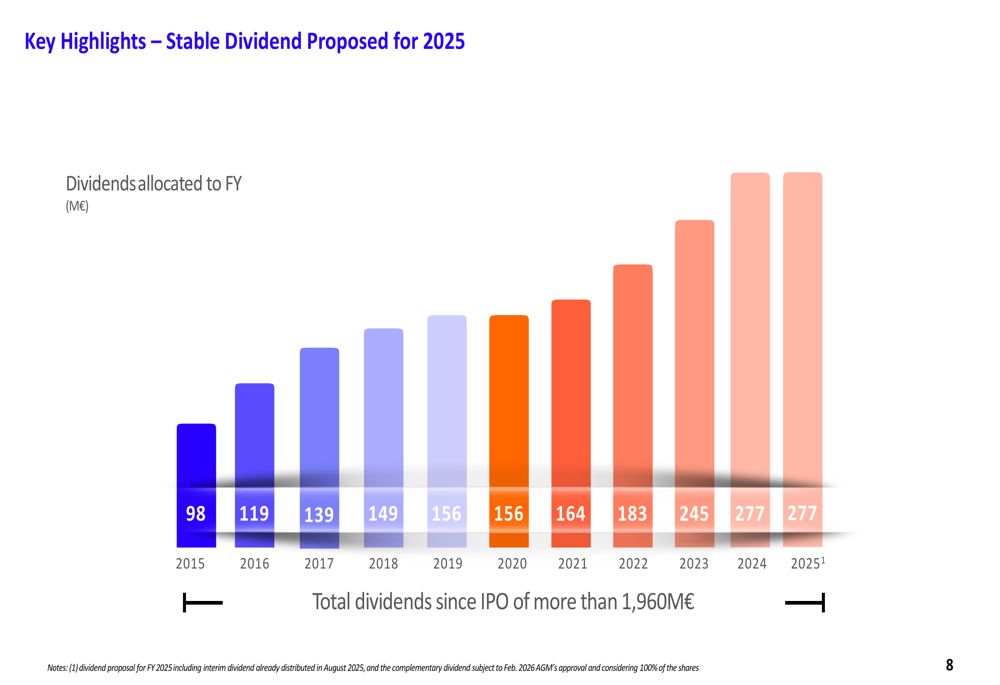

The company maintained its commitment to shareholder returns, proposing a stable dividend of €2.09 per share, representing a 99% payout ratio. This continues Logista's track record of consistent dividend growth since its IPO, with total dividends exceeding €1,960 million over that period.

Detailed Financial Analysis

Logista's financial performance showed contrasting trends across different metrics. While top-line growth remained solid, profitability measures declined due to increased costs and challenges in certain business segments.

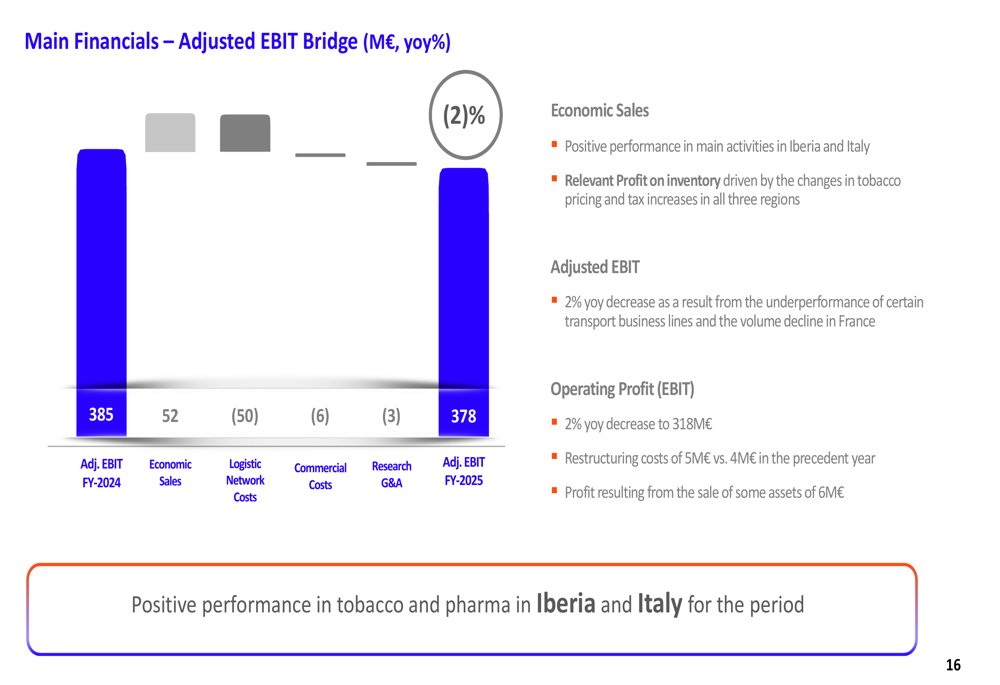

The company's adjusted EBIT bridge illustrates how positive economic sales growth of €52 million was offset by increased logistics network costs (€50 million), commercial costs (€6 million), and research and general administrative expenses (€3 million), resulting in the overall 2% decline:

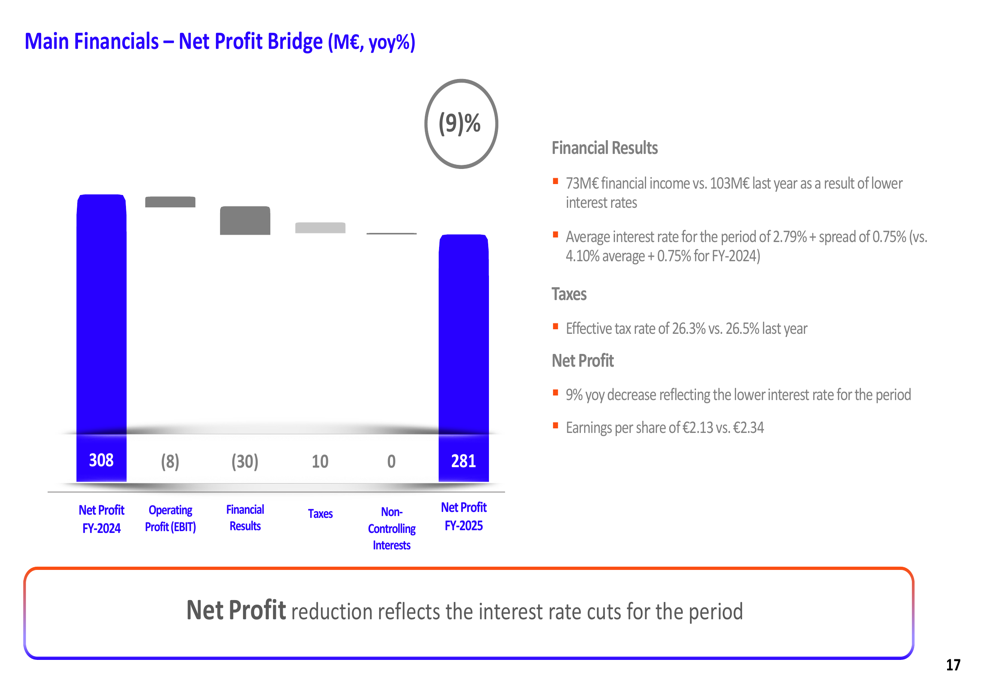

Similarly, the net profit bridge reveals how operating profit decline and significantly lower financial results contributed to the 9% decrease in net profit:

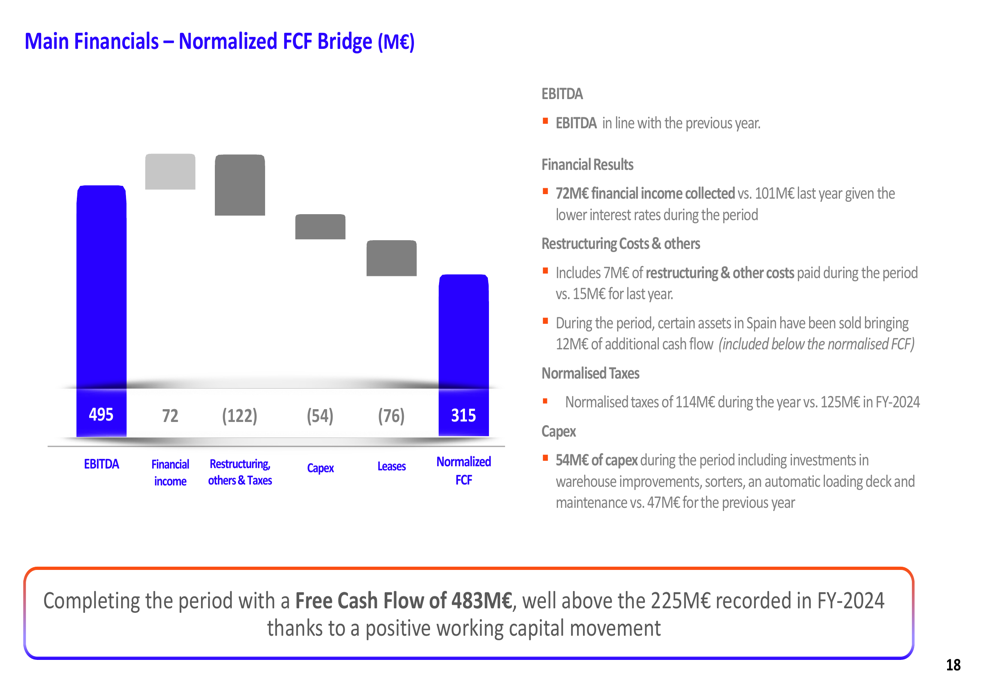

Despite these profit challenges, Logista's cash flow performance was a bright spot. The normalized free cash flow bridge shows how the company generated €315 million in normalized free cash flow, with the company ultimately achieving €483 million in free cash flow for the period:

Regional Performance

Logista's performance varied significantly across its three main regions, with Italy showing strong growth while France experienced substantial declines.

In Iberia, economic sales increased by 3% to €1,181 million, though adjusted EBIT declined by 5% to €191 million. The tobacco and related products segment saw minimal volume decline (-0.4%), while the transport segment faced challenges due to European demand slowdown. The pharmaceutical business was a bright spot, with 10% economic sales growth supported by new agreements.

Italy delivered the strongest performance, with economic sales growing 8% to €434 million and adjusted EBIT increasing 11% to €134 million. Despite a slight decline in tobacco volume (-0.9%), the region benefited from inventory value increases and growth in related products, including e-cigarettes and nicotine pouches. The pharmaceutical business in Italy also showed double-digit economic sales growth.

In contrast, France experienced significant challenges, with economic sales declining 7% to €200 million and adjusted EBIT falling 15% to €53 million. The region suffered from a substantial 9% drop in tobacco volume, though it saw some growth in electronic transactions and NGP (Next Generation Products) recycling.

Strategic Initiatives & Sustainability

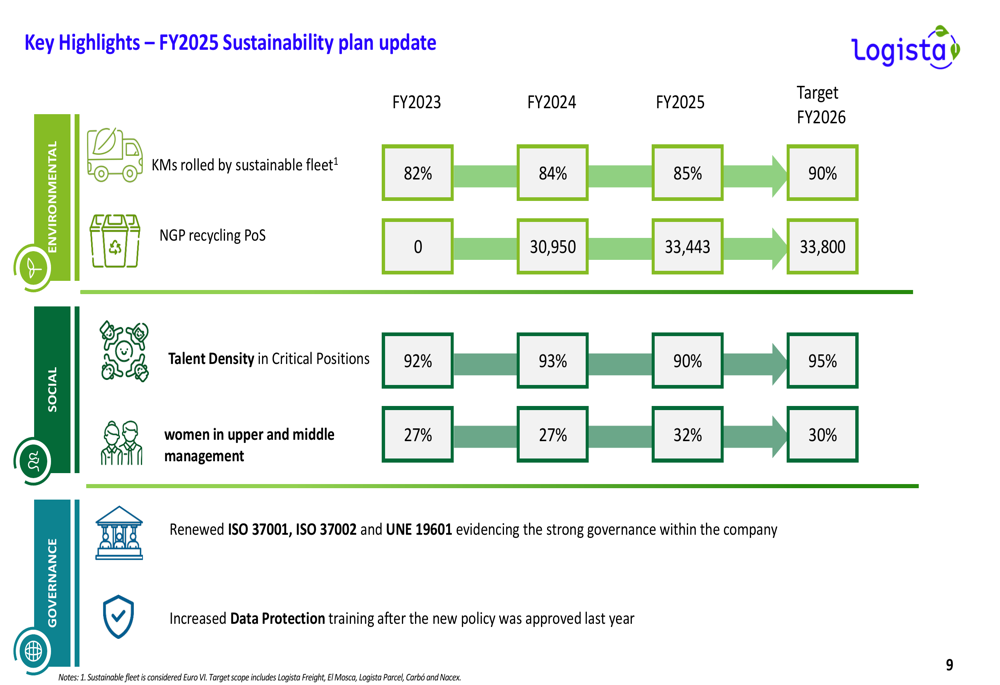

Logista continues to advance its sustainability agenda through its 2024-2026 plan. The company has made progress across environmental, social, and governance metrics, with particularly strong performance in increasing women in management positions.

As shown in the sustainability plan update:

The company is also addressing challenges in specific business segments. For Transportes El Mosca, which experienced a difficult year, Logista has implemented a turnaround strategy including new management, simplified company structure, and cost control measures.

Outlook & Dividend

Looking ahead to 2026, Logista expects to deliver mid-single-digit growth in adjusted EBIT, excluding profit on inventory. The company plans to continue its diversification strategy through small and mid-sized acquisitions while maintaining its dividend policy.

As illustrated in the 2026 outlook:

Logista's commitment to shareholder returns remains strong, with the company proposing a stable dividend of €2.09 per share for FY2025, totaling €277 million. This represents a 99% payout ratio and continues the company's history of consistent dividend payments.

The dividend proposal details:

The historical view of Logista's dividends shows the company's consistent focus on shareholder returns:

Forward-Looking Statements

Logista's management expressed confidence in the company's ability to improve operating results despite the challenges faced in FY2025. The focus on diversification through acquisitions and maintaining dividend stability suggests a balanced approach to growth and shareholder returns.

The company's ESG commitments remain a priority, with clear targets set for 2026 across environmental, social, and governance metrics. Logista's recycling initiatives and sustainable fleet expansion demonstrate its focus on reducing environmental impact while maintaining business growth.

While tobacco volumes continue to decline across all markets, Logista is adapting through expansion in related products and diversification into areas like pharmaceuticals. The company's ability to generate strong free cash flow despite profit challenges provides financial flexibility for future investments and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.