ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Deutsche Lufthansa AG (ETR:LHA) presented its third quarter 2025 results on October 30, highlighting a 4% revenue increase to €11.2 billion despite ongoing yield pressure in key markets. The company's stock responded positively to the results, surging 9.41% to close at €37.75, approaching its 52-week high of €39.

CEO Carsten Spohr emphasized the favorable market environment, noting that "global passenger numbers are expected to double by 2045 versus 2024," while acknowledging that European carriers face structural and regulatory disadvantages requiring enhanced efficiency measures.

Quarterly Performance Highlights

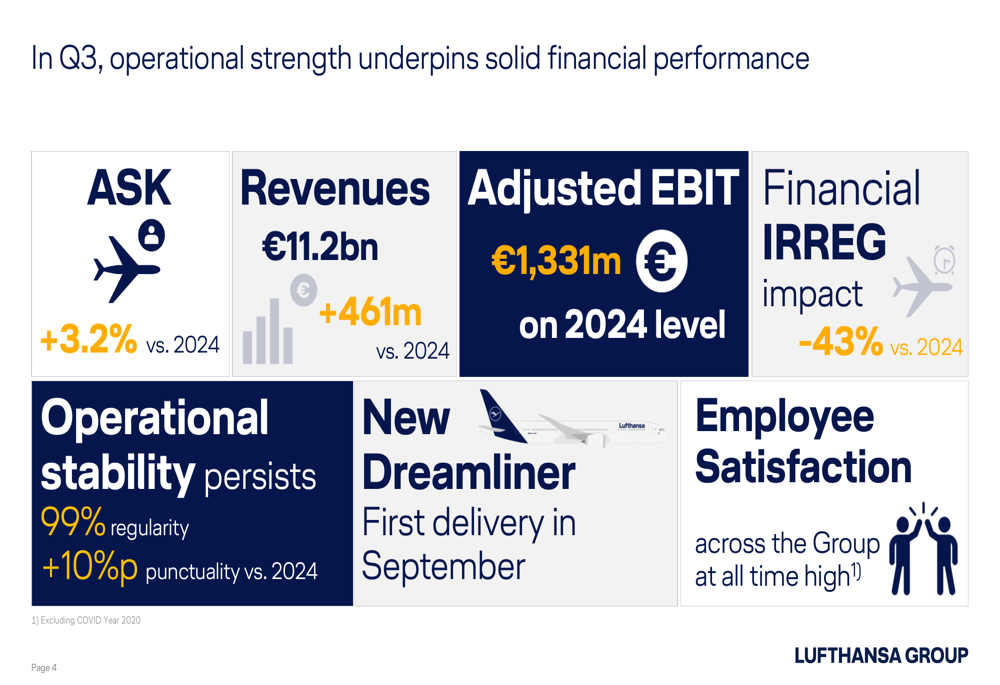

Lufthansa reported stable profitability with adjusted EBIT of €1,331 million, essentially flat compared to Q3 2024 (-1%), despite a 5.4% decline in yield. The company achieved this balance through operational improvements and cost control measures.

As shown in the following operational and financial highlights:

Revenue growth was supported by a 3.2% increase in available seat kilometers (ASK), while the company significantly improved operational stability with 99% regularity and a 10 percentage point improvement in punctuality compared to the previous year. This operational excellence contributed to a 43% reduction in irregular operations costs.

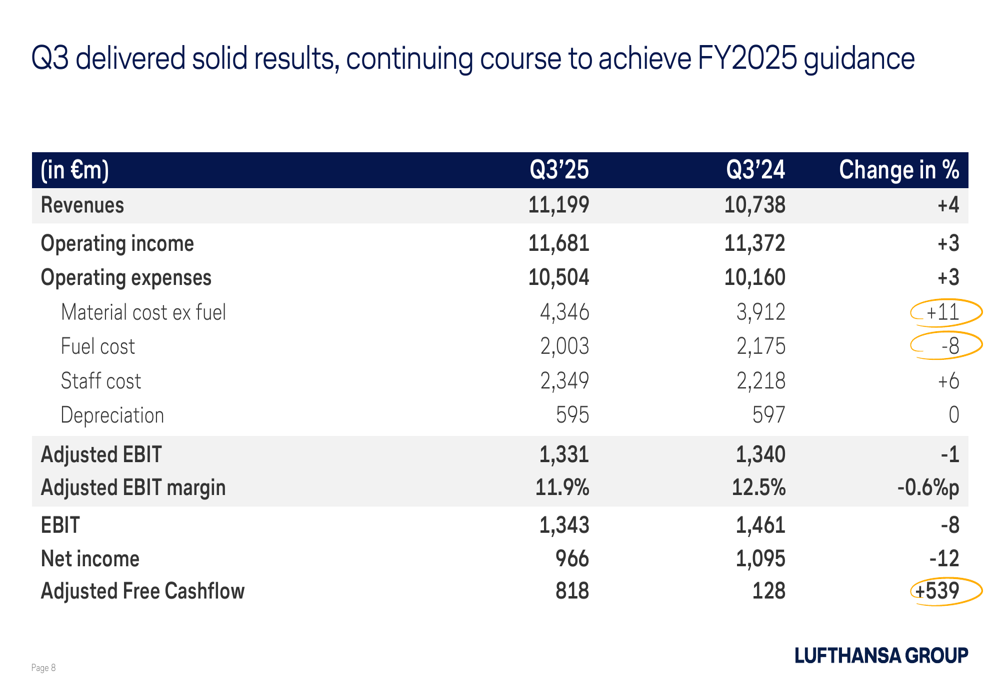

The detailed financial performance breakdown reveals pressure on net income, which declined 12% year-over-year to €966 million, while adjusted free cashflow surged 539% to €818 million:

Segment Performance Analysis

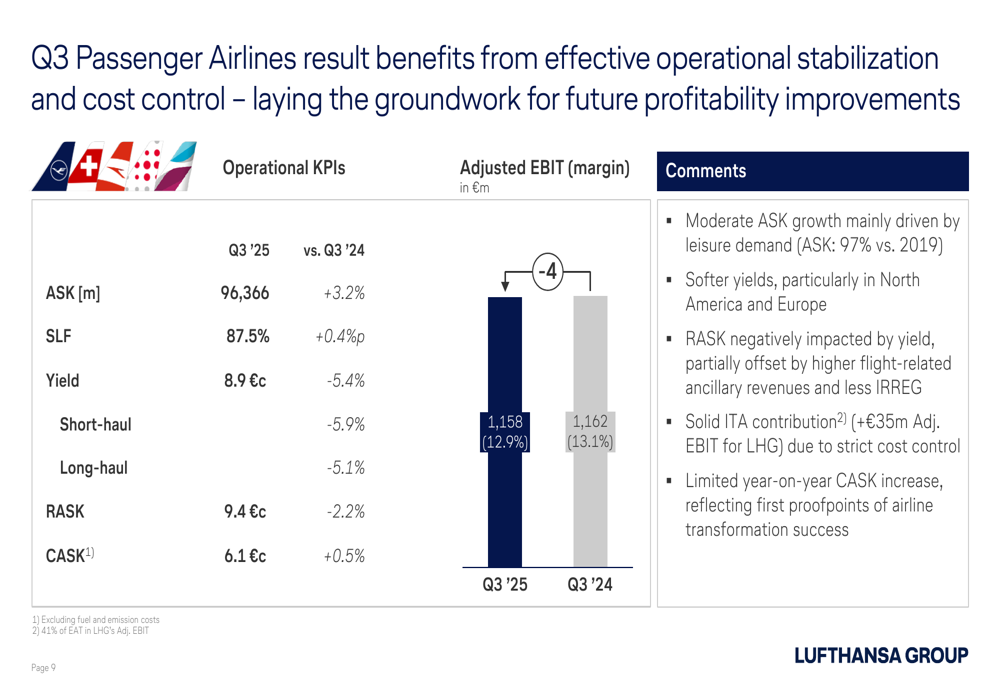

The Passenger Airlines segment, Lufthansa's core business, delivered an adjusted EBIT of €1,158 million with a 12.9% margin, nearly matching the previous year's €1,162 million (13.1% margin). This stability was achieved despite yield pressure, particularly in continental and North American markets.

The following chart illustrates the key performance indicators for the Passenger Airlines segment:

Lufthansa Cargo showed improvement with adjusted EBIT increasing to €49 million (6.0% margin) from €38 million (4.9%) in Q3 2024. The cargo business benefited from 11% volume growth and a 5% revenue increase to €824 million. Additionally, SWISS World Cargo joined the joint venture between Lufthansa Cargo and United, expanding the network to 200 destinations.

Meanwhile, Lufthansa Technik experienced declining profitability despite topline growth. Revenue increased 10% year-over-year to €1,942 million, driven by 28% growth in third-party customers, but adjusted EBIT fell 19% to €130 million (6.7% margin) from €161 million (9.1%) in Q3 2024. The company cited higher tariffs, a weaker USD, and temporary ramp-up costs related to production expansion as factors impacting profitability.

Strategic Initiatives

Lufthansa is advancing its premium strategy with the delivery of its first Boeing 787 Dreamliner in September 2025, featuring the new Allegris cabin. The company plans to rapidly expand its premium product offering across its long-haul fleet:

The airline is implementing a comprehensive turnaround program at Lufthansa Airlines with an expected EBIT impact of €0.5 billion in 2025, focusing on yield optimization, ancillary revenue growth, operational stability, and cost reduction. This program has already contributed to a 1.4 percentage point reduction in unit costs (CASK) at Lufthansa Airlines year-to-date.

Customer satisfaction metrics have improved significantly, with overall satisfaction increasing 8 percentage points year-over-year to 71% in Q3 2025, supported by enhanced network stability (99%, +2 percentage points) and service center accessibility (96%, +2 percentage points).

Financial Outlook and Guidance

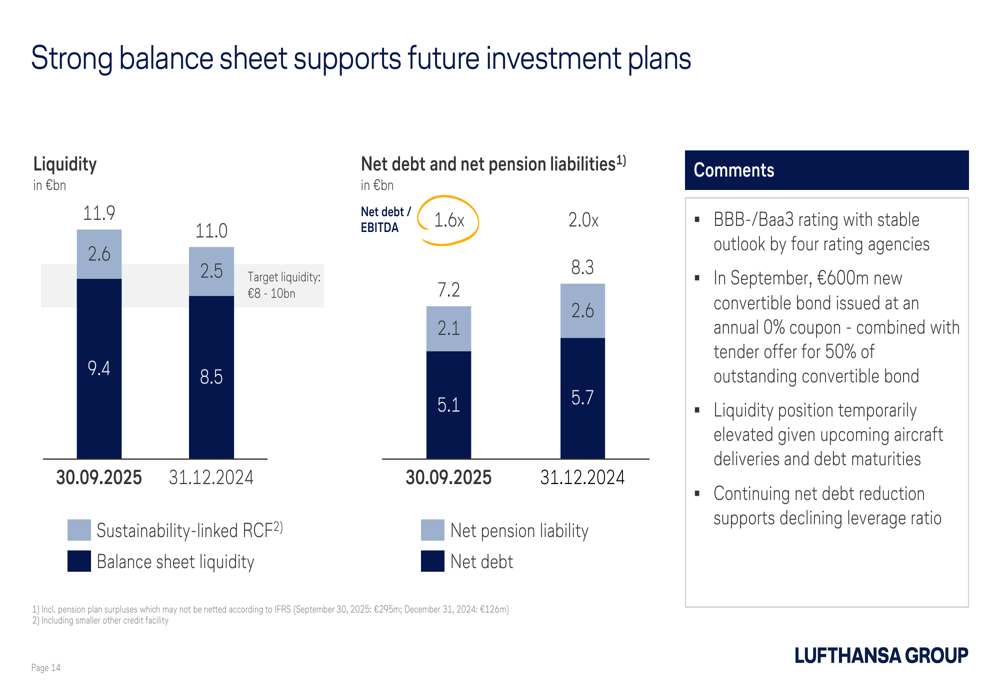

Lufthansa's balance sheet continues to strengthen with net debt and pension liabilities decreasing to €7.2 billion as of September 30, 2025, down from €8.3 billion at the end of 2024:

The company maintains a strong liquidity position of €11.9 billion, temporarily above its target range of €8-10 billion in anticipation of upcoming aircraft deliveries and debt maturities.

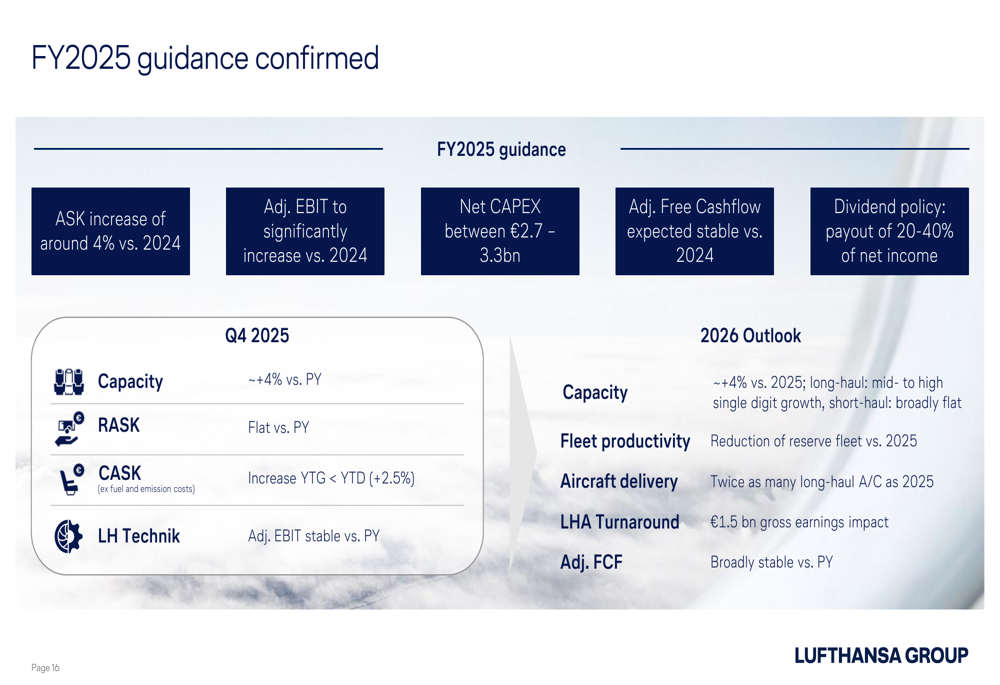

For the full year 2025, Lufthansa expects:

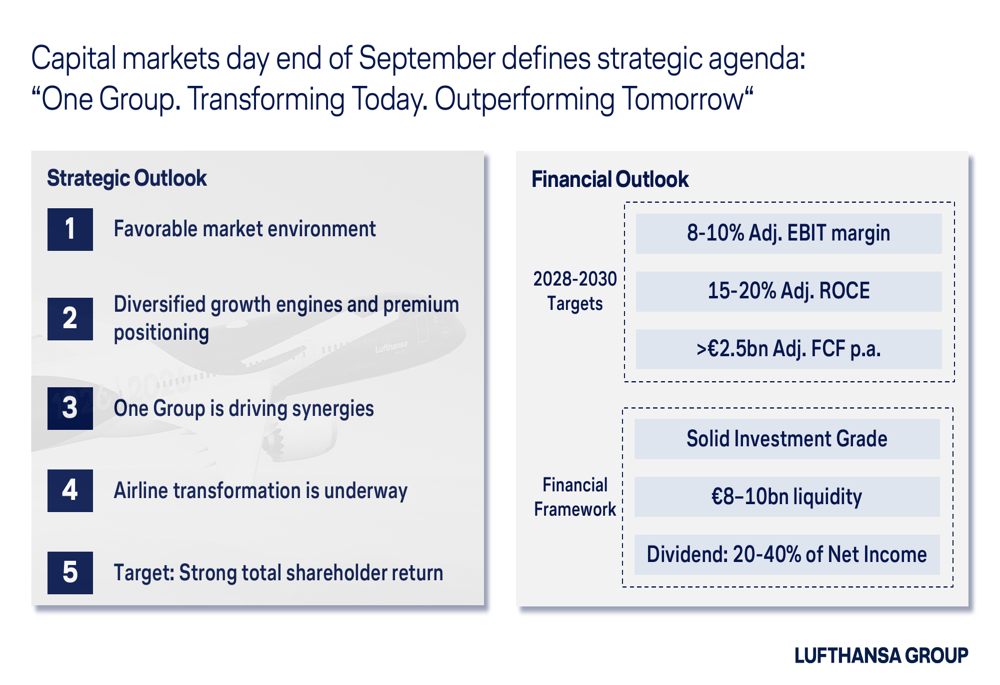

Looking further ahead, the company has established ambitious financial targets for 2028-2030, including an adjusted EBIT margin of 8-10%, adjusted ROCE of 15-20%, and annual adjusted free cashflow exceeding €2.5 billion:

For 2026, Lufthansa projects capacity growth of approximately 4% versus 2025, with mid- to high-single-digit growth in long-haul capacity while short-haul capacity remains broadly flat. The company expects twice as many long-haul aircraft deliveries in 2026 compared to 2025, supporting its fleet renewal and premium strategy.

Lufthansa's dividend policy remains unchanged, with a target payout of 20-40% of net income, underscoring the company's commitment to shareholder returns while investing in its premium strategy and fleet modernization.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.