Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

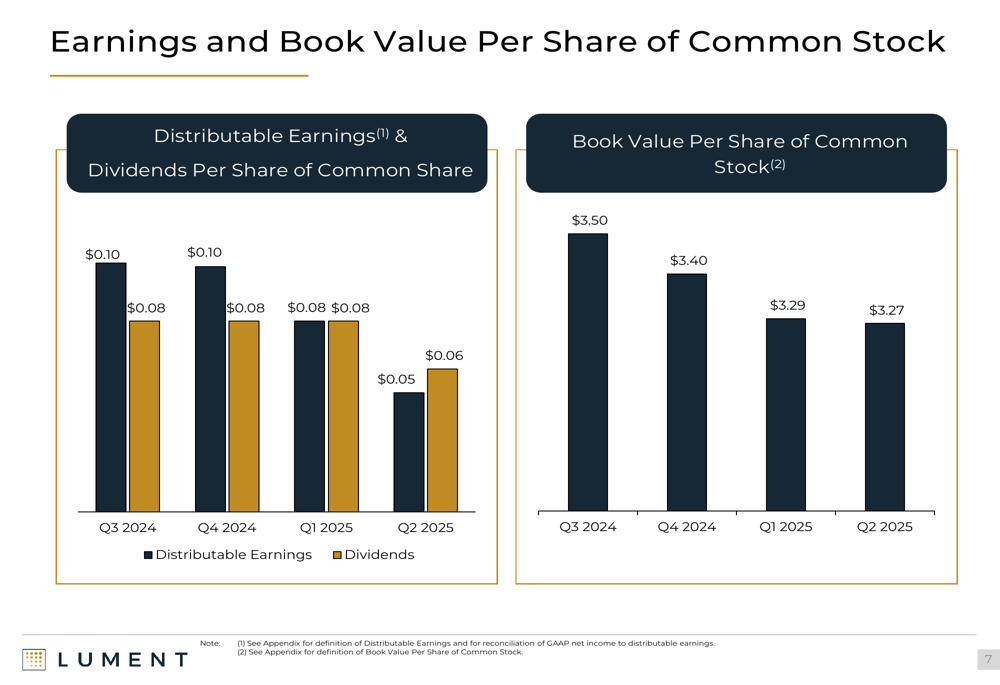

Lument Finance Trust (NYSE:LFT) released its Q2 2025 earnings presentation on August 8, showing continued pressure on earnings despite stable GAAP performance. The real estate investment trust, which focuses primarily on multifamily commercial real estate debt investments, reported distributable earnings matching its GAAP results at $0.05 per share, while announcing a reduced dividend of $0.06 per share.

The company’s stock closed at $2.27 on August 8, 2025, with a modest 1.76% gain during regular trading hours. In after-hours trading, the stock added another 1.32%, reaching $2.30. Despite these gains, LFT continues to trade significantly below its 52-week high of $2.84.

Quarterly Performance Highlights

Lument Finance Trust reported Q2 2025 GAAP net income attributable to common stockholders of $0.05 per share, a notable improvement from the GAAP net loss of $0.03 per share reported in Q1. However, distributable earnings declined to $0.05 per share from $0.08 in the previous quarter, continuing a downward trend observed over the past year.

As shown in the following chart of earnings and dividend trends, both metrics have been declining over recent quarters:

The company declared a cash dividend of $0.06 per share on June 20, 2025, representing a 25% reduction from the $0.08 per share paid in the previous three quarters. This reduction aligns with the company’s declining distributable earnings but maintains a dividend that slightly exceeds current earnings.

Book value per share continued its gradual decline, reaching $3.27 as of June 30, 2025, compared to $3.29 at the end of Q1 and $3.40 at year-end 2024.

Portfolio Composition and Credit Quality

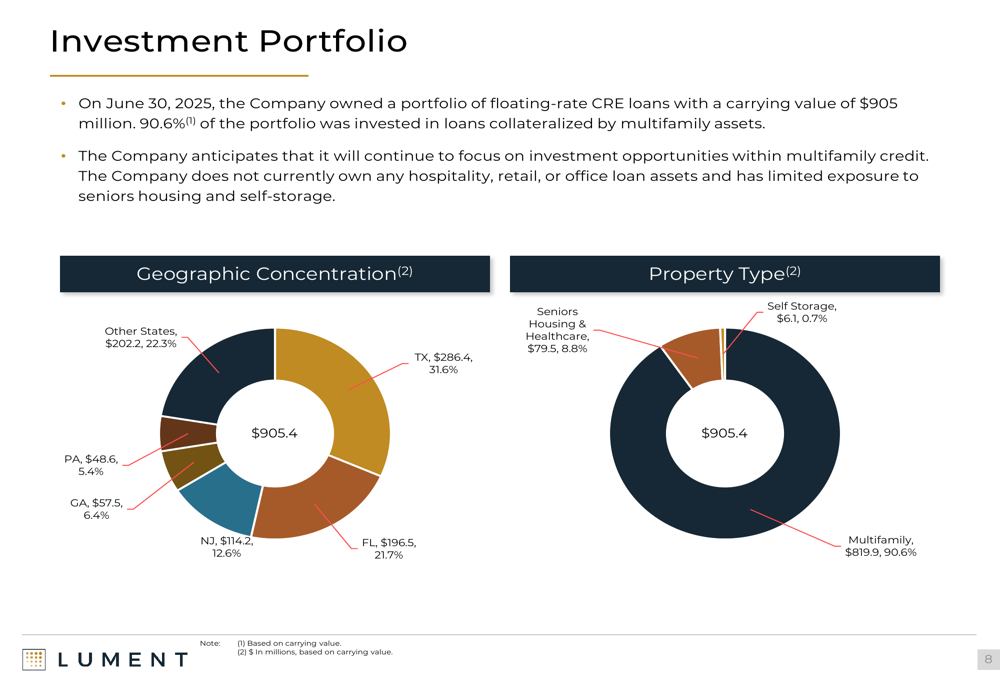

As of June 30, 2025, Lument Finance Trust’s investment portfolio consisted of floating-rate commercial real estate loans with a carrying value of $905.4 million, down from $988.8 million in the previous quarter. The portfolio remains heavily concentrated in multifamily assets, which represent 90.6% of the total, with the remainder in seniors housing & healthcare (8.8%) and self-storage (0.7%).

The following chart illustrates the portfolio’s property type and geographic concentration:

During the quarter, the company experienced $63.4 million in loan payoffs, all from multifamily properties, while funding only $3.6 million in new loans, exclusively in the healthcare sector. This net reduction in the loan portfolio contributed to the company’s improved leverage ratio, which declined from 3.6x to 3.3x quarter-over-quarter.

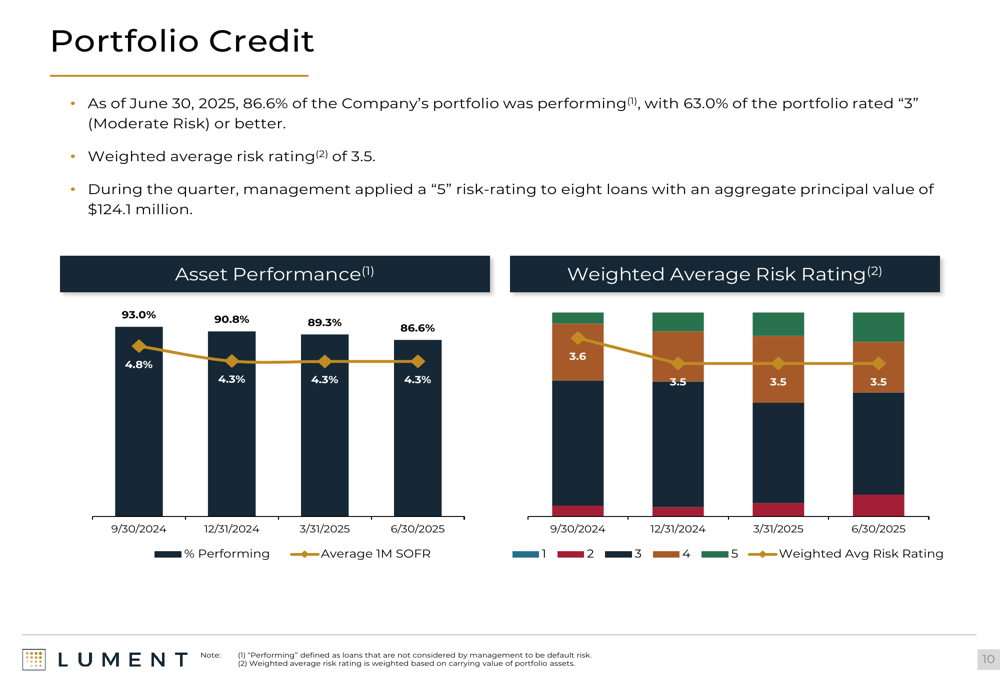

The portfolio’s credit quality showed concerning trends, with the percentage of performing loans declining to 86.6%, down from 93.0% in Q3 2024. The weighted average risk rating improved slightly to 3.5 from 3.6, but management applied a high-risk "5" rating to eight loans with an aggregate principal value of $124.1 million during the quarter.

The following chart demonstrates the deteriorating trend in asset performance:

Capital Structure and Financing

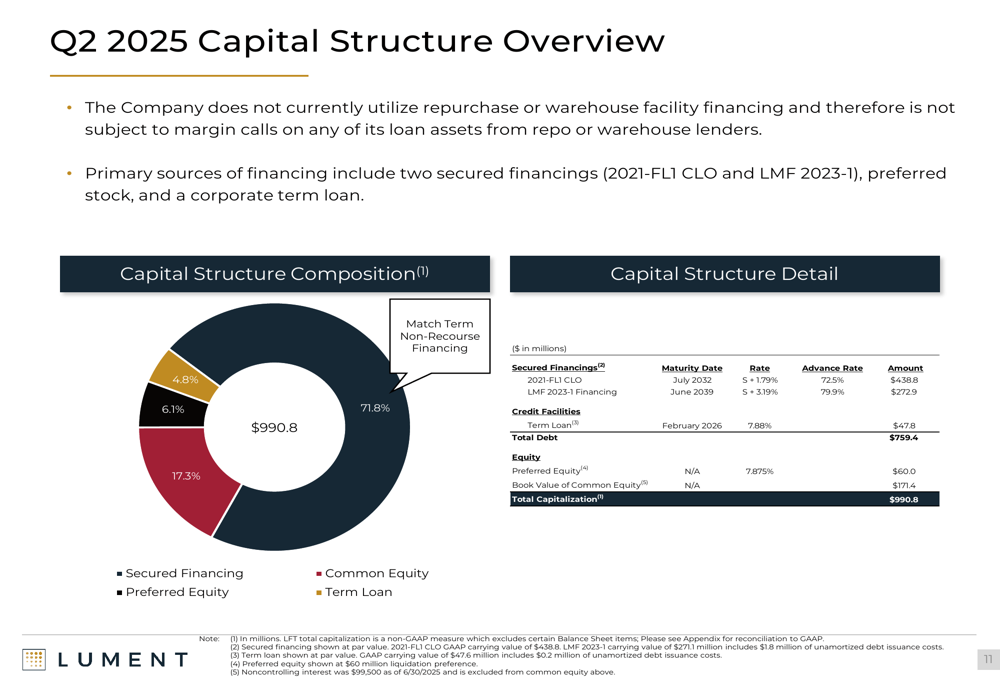

Lument Finance Trust maintains a diversified capital structure, primarily relying on secured financings through its CLO and other structured vehicles rather than repurchase or warehouse facility financing. As of June 30, 2025, the company reported cash and cash equivalents of $59.4 million, providing liquidity for operations and potential investment opportunities.

The company’s capital structure consists of secured financing (71.8%), common equity (17.3%), preferred equity (6.1%), and term loan (4.8%), as illustrated in the following chart:

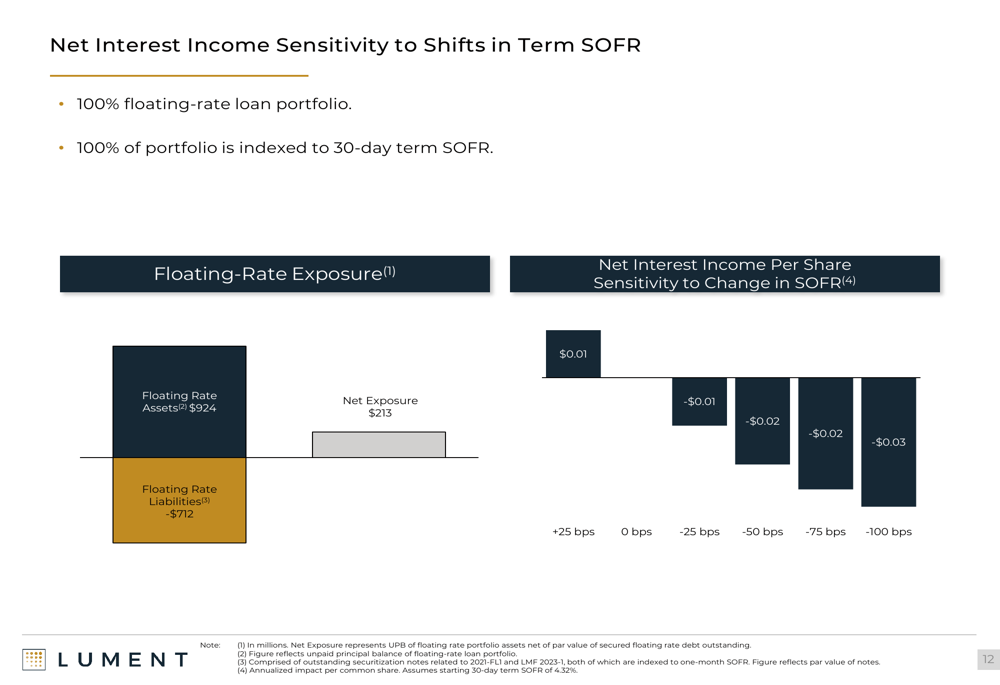

With 100% of its loan portfolio floating-rate and indexed to 30-day term SOFR, Lument’s net interest income remains sensitive to interest rate fluctuations. The company’s analysis suggests that a 25 basis point increase in SOFR would increase earnings per share by $0.01, while a 100 basis point decrease would reduce earnings per share by $0.03.

The following chart shows the company’s net interest income sensitivity to shifts in Term SOFR:

Forward-Looking Statements

Looking ahead, Lument Finance Trust faces both challenges and opportunities. The declining trend in distributable earnings and increasing proportion of non-performing loans suggest continued pressure on the company’s financial performance. However, the improved leverage ratio and substantial cash position provide flexibility to navigate market uncertainties.

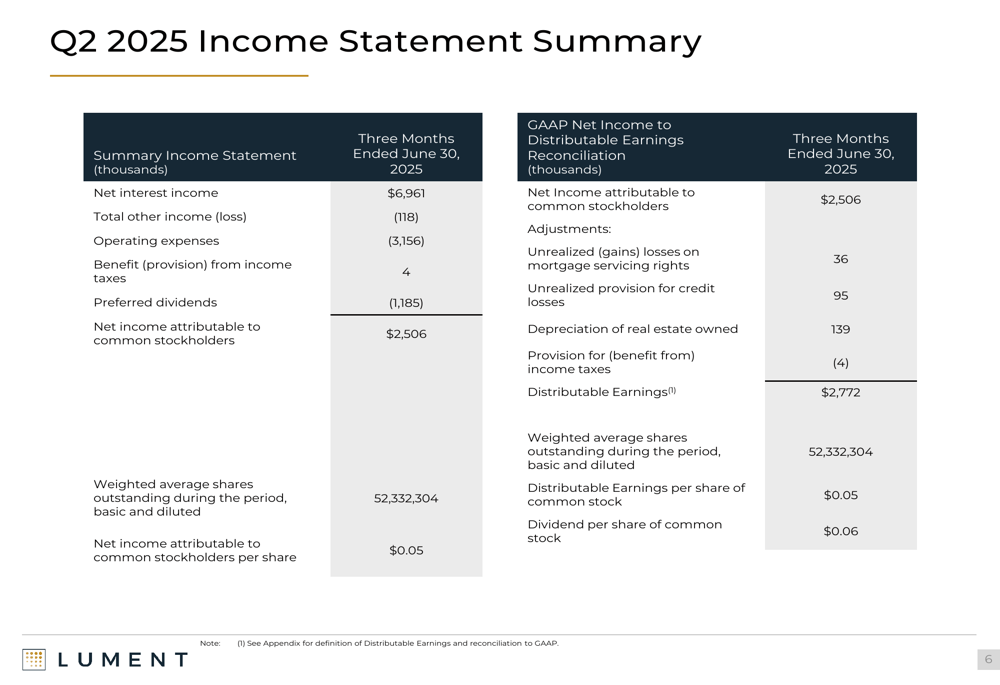

The company’s Q2 2025 income statement reveals the pressure on earnings, with net interest income of $6.96 million and operating expenses of $3.16 million:

The reduction in dividend payout suggests management is taking a more conservative approach to capital allocation amid the challenging environment. With 90.6% of its portfolio in multifamily assets and no exposure to more volatile sectors like hospitality, retail, or office properties, Lument maintains a relatively defensive positioning within the commercial real estate lending market.

However, investors should monitor the increasing proportion of loans receiving high-risk ratings, as further deterioration could lead to additional loan loss provisions and potential impacts on book value. The company’s ability to resolve problem loans and redeploy capital into new, high-quality investments will be crucial for reversing the current negative trends in earnings and portfolio performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.