Veeco launches Lumina+ MOCVD system, receives Rocket Lab order

Introduction & Market Context

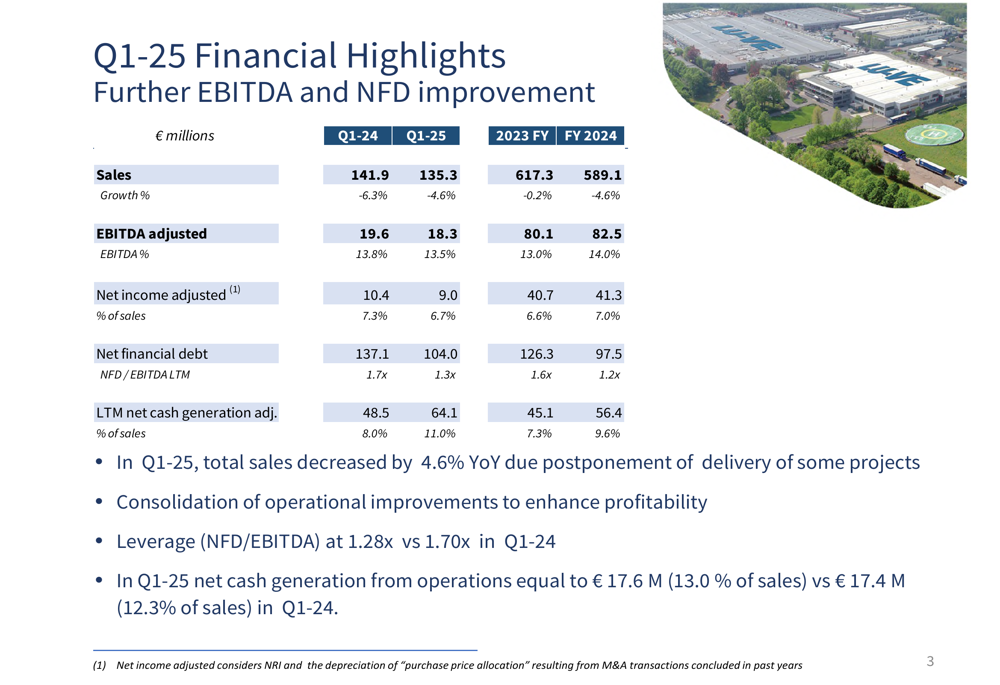

LU-VE SpA (BIT:LUVE) reported its Q1 2025 financial results on May 13, 2025, showing a 4.6% decline in sales while maintaining stable profitability margins. The company’s stock reacted negatively to the news, falling 4.27% to €30.30 on the day of the announcement, despite management’s optimistic outlook based on a record-high order book.

The Italian thermal equipment manufacturer faced headwinds from project postponements in several key segments, particularly in air conditioning and industrial cooling. However, the company highlighted its strong order book of €210.4 million, up 24.6% year-over-year, suggesting potential revenue recovery in upcoming quarters.

Quarterly Performance Highlights

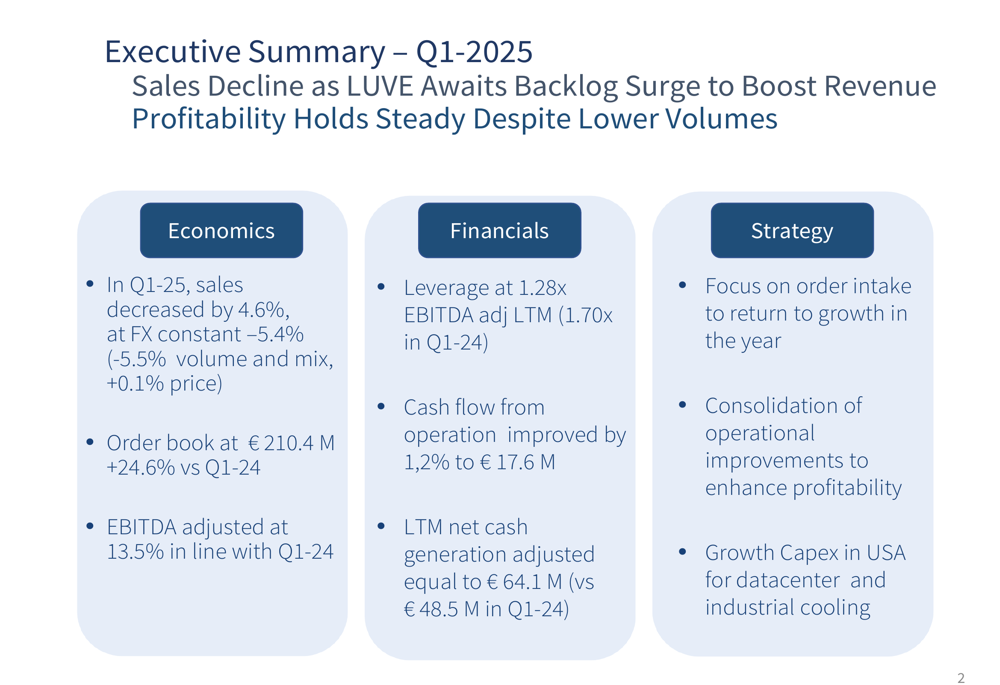

LU-VE reported Q1 2025 sales of €135.3 million, down 4.6% from €141.9 million in Q1 2024. Despite the revenue decline, the company maintained relatively stable profitability with adjusted EBITDA at 13.5% of sales, only slightly below the 13.8% recorded in the same period last year.

As shown in the comprehensive financial highlights table below, net income adjusted decreased to €9.0 million (6.7% of sales) compared to €10.4 million (7.3%) in Q1 2024, while the company significantly improved its financial position with net financial debt decreasing to €104.0 million from €137.1 million a year earlier.

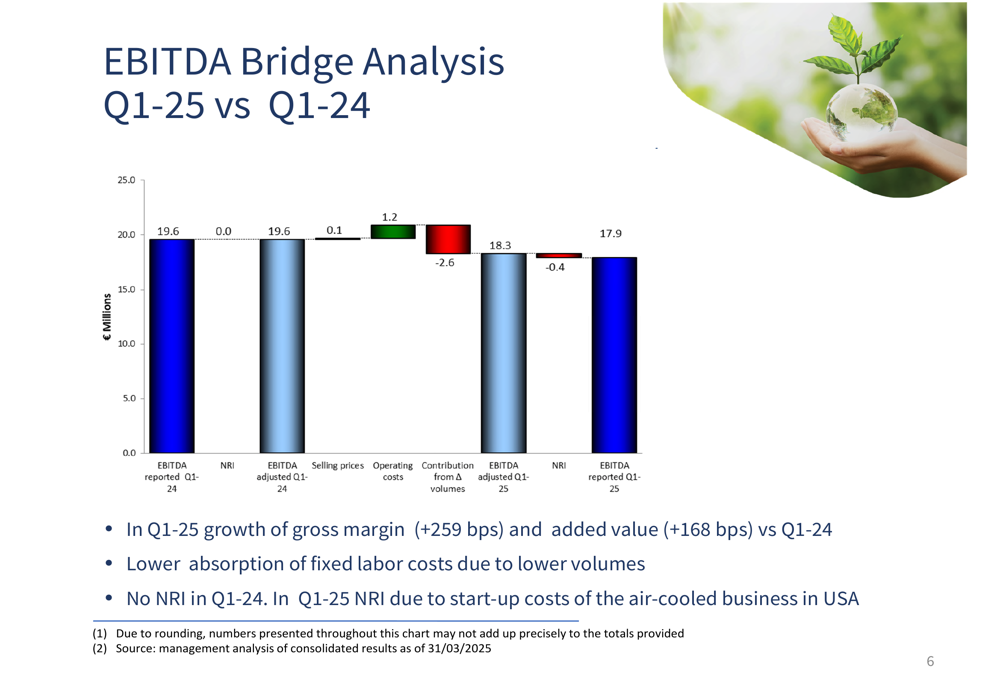

The company’s EBITDA bridge analysis reveals that while volume declines had a negative €2.6 million impact on profitability, this was partially offset by improvements in operating costs (+€1.2 million) and a slight positive contribution from selling prices (+€0.1 million).

Segment Performance

LU-VE’s performance varied significantly across product segments and applications. Heat Exchangers, representing 52.3% of Q1 2025 sales, showed modest growth of 0.7% year-over-year. In contrast, Air Cooled Equipment, which accounts for 43.8% of sales, declined by 11.5%, primarily due to project delays.

By application, Refrigeration (51.1% of sales) was the only segment showing growth, with a 1.5% increase compared to Q1 2024. Air Conditioning experienced the steepest decline at 17.6%, followed by Industrial Cooling at 15.7% and Special Applications at 2.1%.

The company maintains a diverse customer base, with its largest customer representing only 4.2% of total sales and the top 10 customers accounting for 30% of sales. Geographically, the European Union remains LU-VE’s primary market, representing 74.8% of sales, with Italy accounting for 20.3% and the rest of the world 25.2%.

Financial Position

LU-VE significantly strengthened its financial position in Q1 2025, with leverage (net financial debt to EBITDA) improving to 1.28x from 1.70x in Q1 2024. The company generated €17.6 million in cash flow from operations, representing 13.0% of sales, a slight improvement from 12.3% in the same period last year.

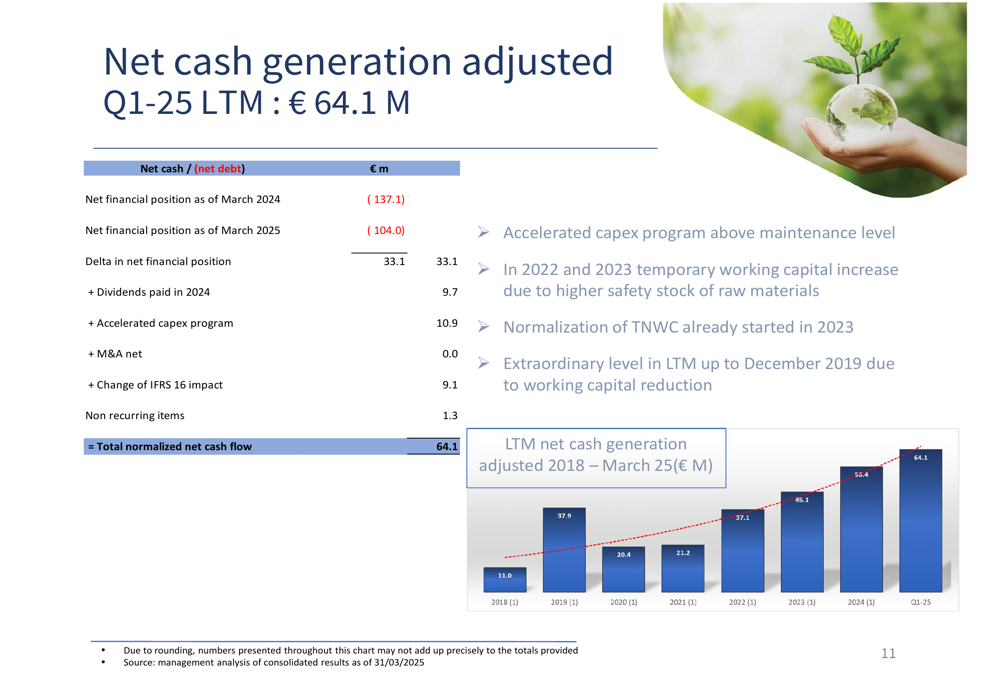

The following chart illustrates the company’s impressive trend in net cash generation, which reached €64.1 million on a last-twelve-months basis in Q1 2025, compared to €48.5 million in Q1 2024.

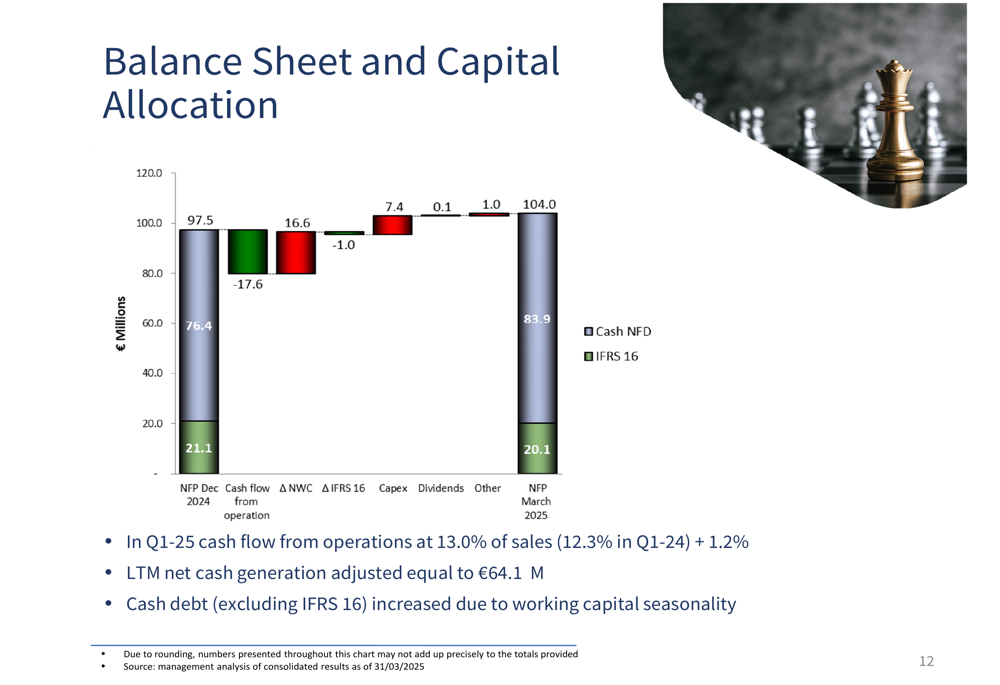

The company’s balance sheet and capital allocation strategy demonstrates a focus on debt reduction while maintaining strategic investments. As shown in the waterfall chart below, LU-VE’s net financial position improved despite seasonal working capital requirements.

Trade net working capital as a percentage of last-twelve-months sales stood at 19.3% in Q1 2025, slightly lower than the 19.8% recorded in Q1 2024 but higher than the 16.3% at year-end 2024, reflecting typical seasonal patterns.

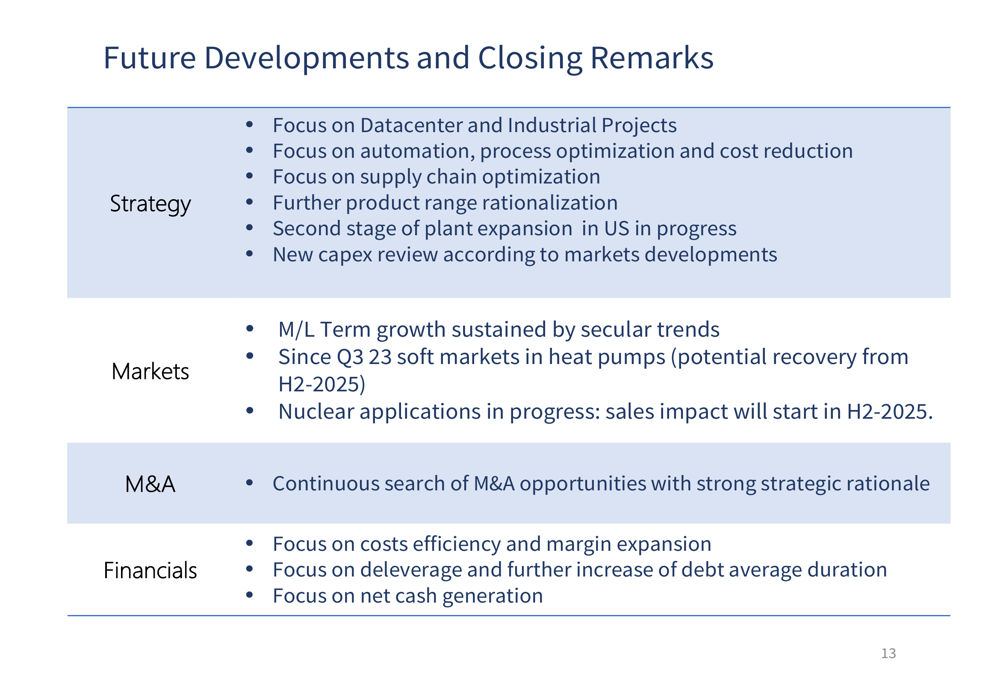

Strategic Initiatives

LU-VE outlined several strategic initiatives focused on long-term growth and operational improvements. The company is prioritizing datacenter and industrial cooling projects, areas expected to show strong demand in coming years. Additionally, the second stage of plant expansion in the United States is progressing, positioning the company to capture growth opportunities in the North American market.

Management emphasized ongoing efforts to enhance profitability through automation, process optimization, cost reduction, and supply chain improvements. The company is also undertaking product range rationalization to streamline operations and improve efficiency.

Forward-Looking Statements

Despite current challenges, LU-VE’s management expressed confidence in returning to growth later in the year, supported by the record-high order book. The company noted that the first signs of recovery are appearing in heat pump heat exchangers, with a broader market recovery expected in the second half of 2025.

Nuclear applications represent another growth opportunity, with sales impact expected to begin in H2 2025. The company also continues to search for M&A opportunities with strong strategic rationale, while maintaining focus on cost efficiency, margin expansion, and cash generation.

The executive summary slide below captures the company’s balanced assessment of current challenges and future opportunities:

While LU-VE faces near-term headwinds from project delays and market softness in certain segments, the company’s solid profitability, improved financial position, and strong order book suggest potential for improved performance in upcoming quarters. Investors will be watching closely to see if the anticipated conversion of the order book into revenue materializes as expected in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.