Gold is 2025’s best performer. UBS sees more upside

Introduction & Market Context

Manitowoc Company Inc (NYSE:MTW) presented its second-quarter 2025 earnings results on August 8, 2025, revealing declining profitability despite modest order growth. The crane manufacturer’s stock plummeted 20.14% following the release, with premarket trading showing an additional 12.23% decline, reflecting investor concerns about deteriorating financial metrics and increasing leverage.

The company faces varied market conditions globally, with tariff-related uncertainty particularly affecting its North American operations. While overall customer sentiment remains positive, regional performance continues to diverge significantly across Manitowoc’s key markets.

Quarterly Performance Highlights

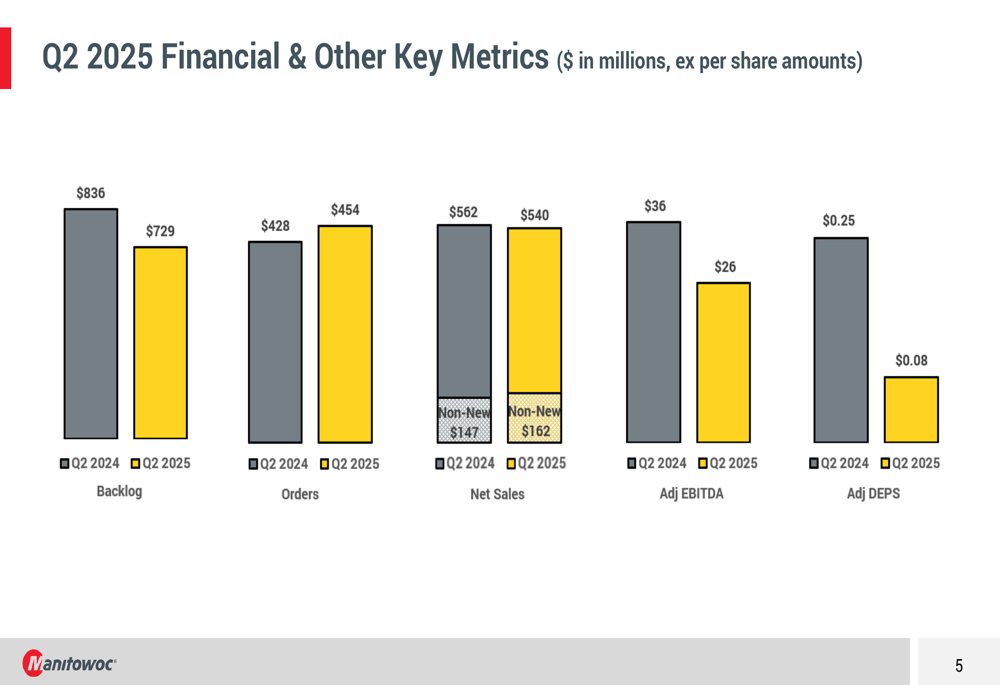

Manitowoc reported second-quarter net sales of $540 million, down 3.9% from $562 million in the same period last year. Despite this decline, orders increased by 6.1% to $454 million, up from $428 million in Q2 2024, suggesting some underlying demand resilience.

As shown in the following chart of key financial metrics, the company’s profitability measures declined significantly year-over-year:

Particularly concerning was the 27.8% drop in adjusted EBITDA to $26 million, compared to $36 million in Q2 2024. Adjusted diluted earnings per share fell to $0.08, a 68% decline from $0.25 in the prior-year period.

One bright spot was the company’s non-new machine sales, which increased 10% year-over-year to $162 million, continuing to provide a more stable revenue stream amid fluctuating new equipment demand. The company also highlighted improved safety performance, with the recordable injury rate decreasing from 1.26 in the first half of 2024 to 0.67 in the first half of 2025.

Detailed Financial Analysis

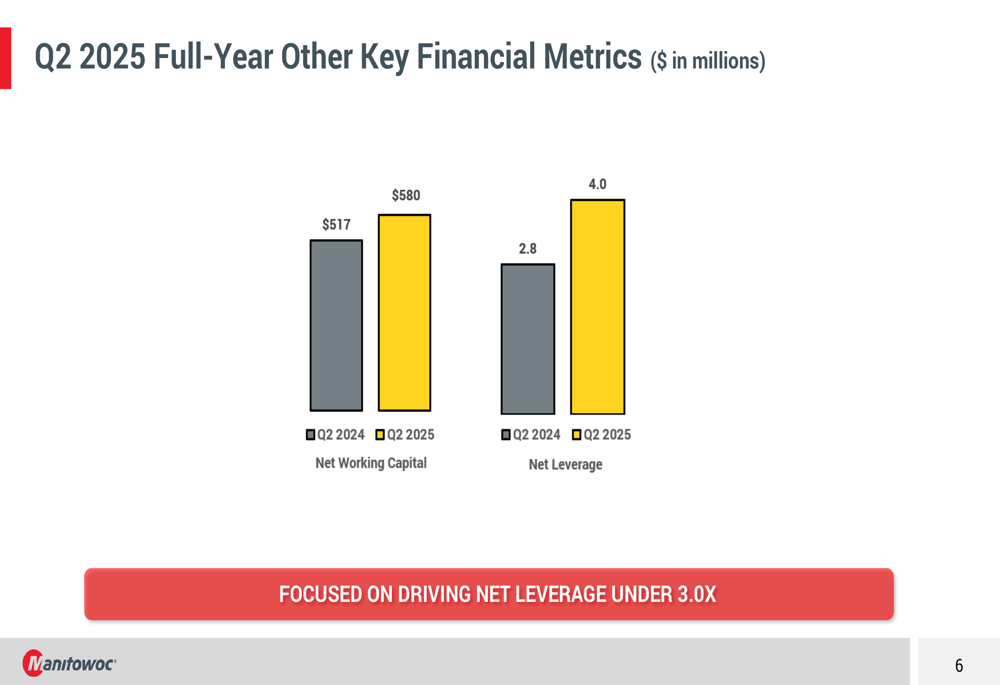

Manitowoc’s financial position showed signs of strain in the second quarter. Net working capital increased to $580 million from $517 million a year earlier, while net leverage rose significantly to 4.0x from 2.8x in Q2 2024, moving well above the company’s stated target of below 3.0x.

The following chart illustrates these concerning trends:

Free cash flow deteriorated substantially to negative $73.7 million for the quarter, compared to negative $1.9 million in Q2 2024. This significant cash burn represents a challenge for the company as it attempts to manage its increasing leverage.

The company’s backlog stood at $729 million at the end of Q2 2025, down 12.8% from $836 million at the same point last year, potentially signaling softer demand in coming quarters despite the recent uptick in orders.

Strategic Initiatives

Manitowoc continues to advance its CRANES+50 initiative, which focuses on expanding its service capabilities and non-new equipment revenue streams. The company highlighted new and expanded service locations in Poland, Sydney (Australia), Nantes (France), and Nashville (Tennessee).

A key component of this strategy is the implementation of SERVICEMAX, a platform designed to integrate various legacy systems to enhance technician productivity, improve service contract management, reduce administrative workload, and enable comprehensive asset management.

The following image illustrates the company’s service expansion strategy:

This focus on service expansion aligns with the company’s success in growing non-new machine sales, which have been a relative bright spot amid challenging market conditions for new equipment.

Market Conditions

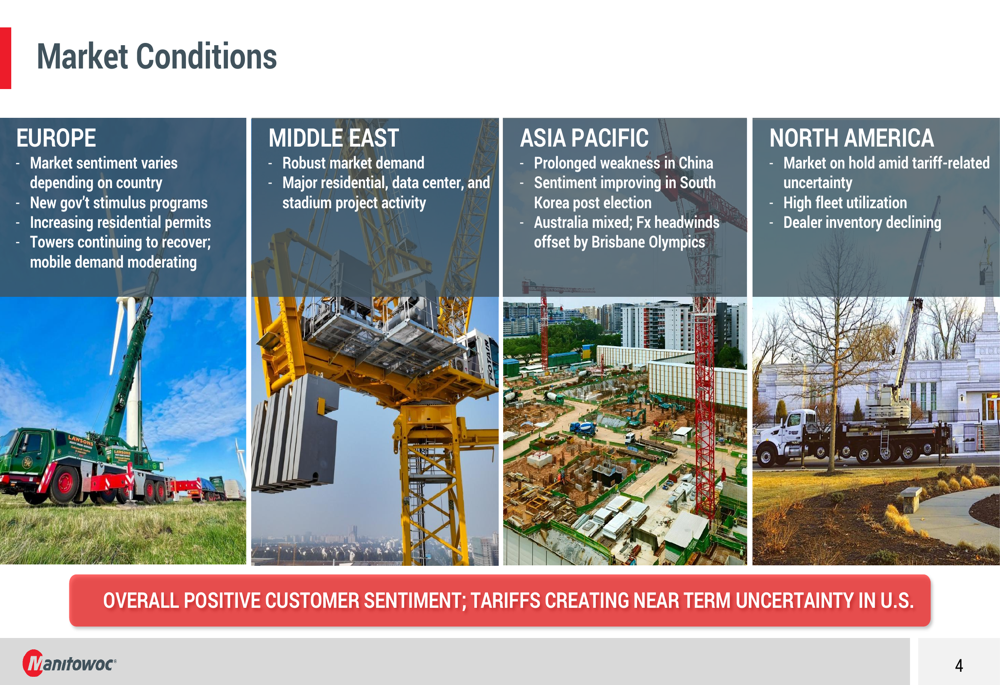

Manitowoc provided a detailed regional market outlook, highlighting significant variations across its global operations. The company noted that tariff-related uncertainty is creating near-term challenges in the U.S. market, despite high fleet utilization and declining dealer inventory.

The following regional breakdown illustrates the varied market conditions:

In Europe, market sentiment varies by country, with tower cranes continuing to recover while mobile demand is moderating. The Middle East shows robust market demand driven by major residential, data center, and stadium projects. Asia Pacific continues to experience prolonged weakness in China, though sentiment is improving in South Korea following recent elections. The Australian market remains mixed, with foreign exchange headwinds offset by activity related to the Brisbane Olympics.

Forward-Looking Statements

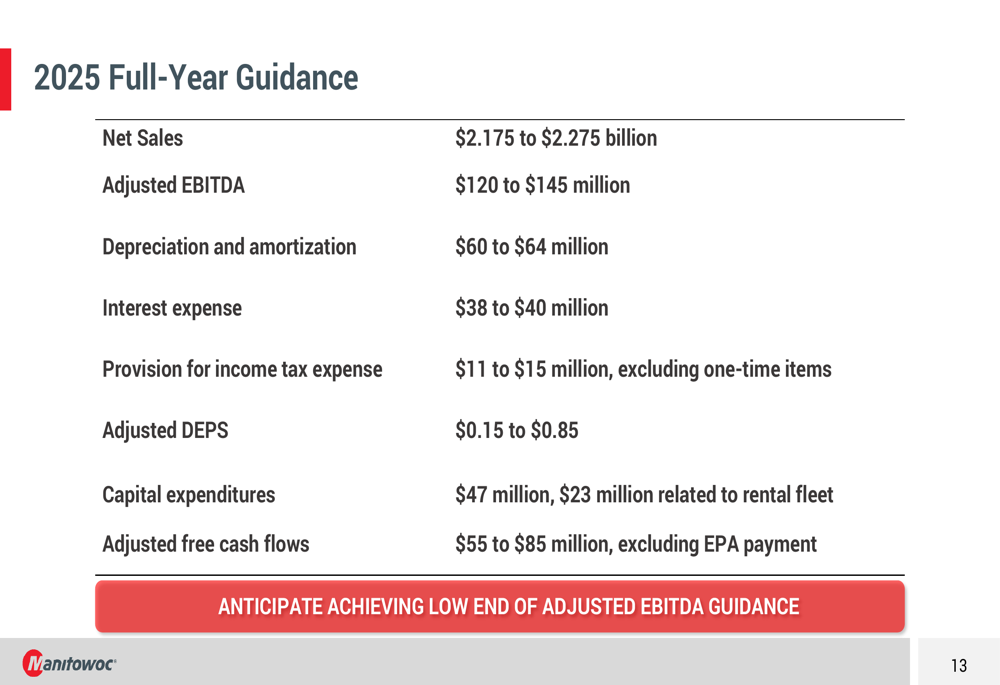

Manitowoc maintained its full-year 2025 guidance, projecting net sales between $2.175 billion and $2.275 billion and adjusted EBITDA between $120 million and $145 million. However, the company now anticipates achieving only the low end of its adjusted EBITDA guidance range, signaling continued profitability challenges.

The detailed guidance includes:

Additional guidance metrics include depreciation and amortization of $60-64 million, interest expense of $38-40 million, and adjusted diluted earnings per share of $0.15-$0.85. Capital expenditures are projected at $47 million, with $23 million related to rental fleet expansion.

The company expects adjusted free cash flows between $55-85 million, excluding an EPA payment. However, given the significant negative free cash flow in the first half of the year, achieving this target will require substantial improvement in the second half of 2025.

Conclusion

Manitowoc’s second-quarter results reveal a company facing significant challenges, with declining profitability, increasing leverage, and deteriorating cash flow. While order growth and the expansion of non-new machine sales provide some positive indicators, the sharp stock decline following the earnings release suggests investors remain concerned about the company’s financial trajectory.

The varied regional market conditions and ongoing tariff-related uncertainty in North America present additional headwinds as Manitowoc attempts to navigate an increasingly complex global market environment. The company’s ability to execute on its CRANES+50 initiative and manage its rising leverage will be critical factors to watch in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.