TSX up after index logs fresh record high close

Introduction & Market Context

ManpowerGroup (NYSE:MAN) released its second quarter 2025 results presentation on July 17, showing adjusted earnings that exceeded guidance despite significant impairment charges that pushed reported earnings into negative territory. The workforce solutions provider’s stock rose 4.99% in premarket trading to $45.25, suggesting investors were focusing on the adjusted figures rather than headline numbers.

The presentation revealed a company navigating a complex global employment landscape with varying regional performance. After disappointing first quarter results that saw the stock drop 11.2%, ManpowerGroup appears to be stabilizing in certain markets while continuing to face headwinds in others.

Quarterly Performance Highlights

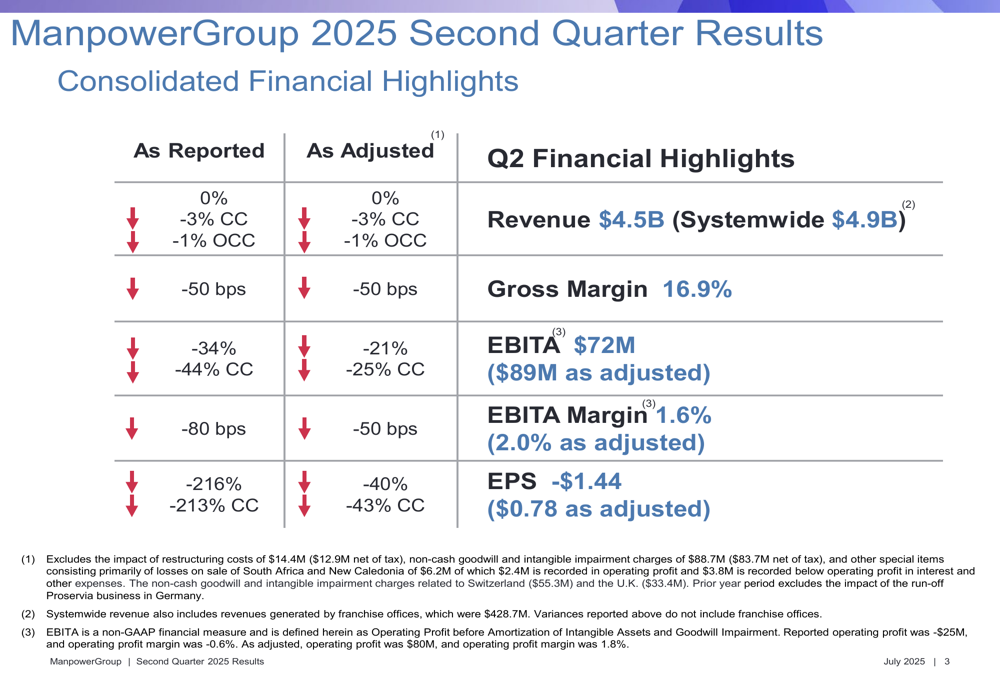

ManpowerGroup reported second quarter revenue of $4.5 billion, with systemwide revenue reaching $4.9 billion. While the company achieved an adjusted EBITA of $89 million (2.0% margin), reported figures were significantly impacted by restructuring costs and impairment charges.

As shown in the following consolidated financial highlights:

The most striking figure was the reported earnings per share of -$1.44, dramatically affected by non-cash goodwill and intangible impairment charges of $88.7 million ($83.7 million net of tax), restructuring costs of $14.4 million, and losses on the sale of operations in South Africa and New Caledonia totaling $6.2 million.

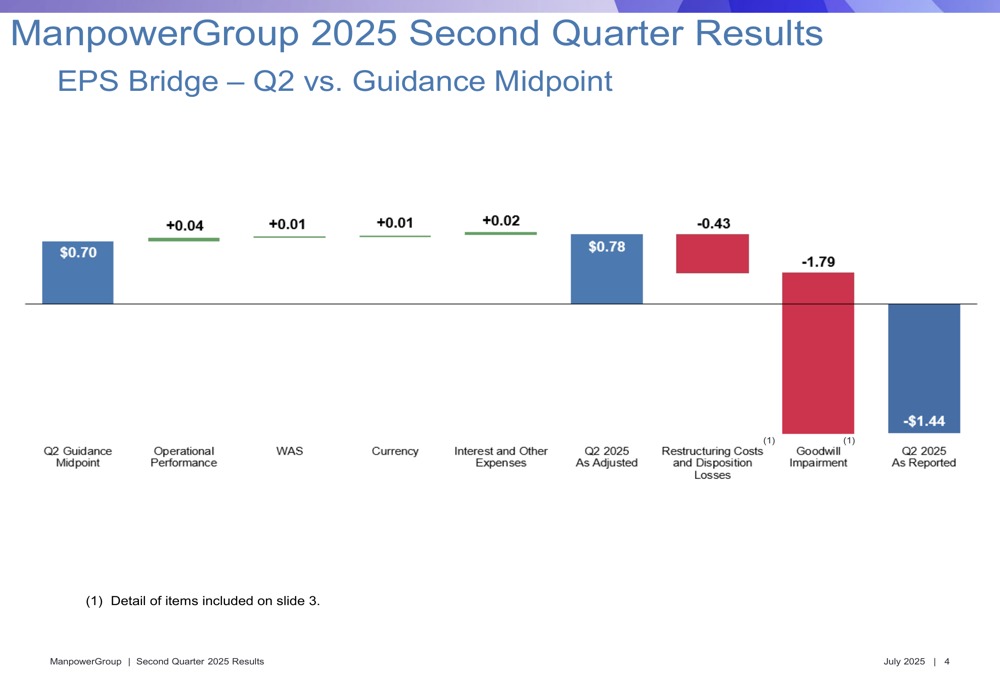

However, the adjusted EPS of $0.78 exceeded the guidance midpoint of $0.70, as illustrated in this EPS bridge:

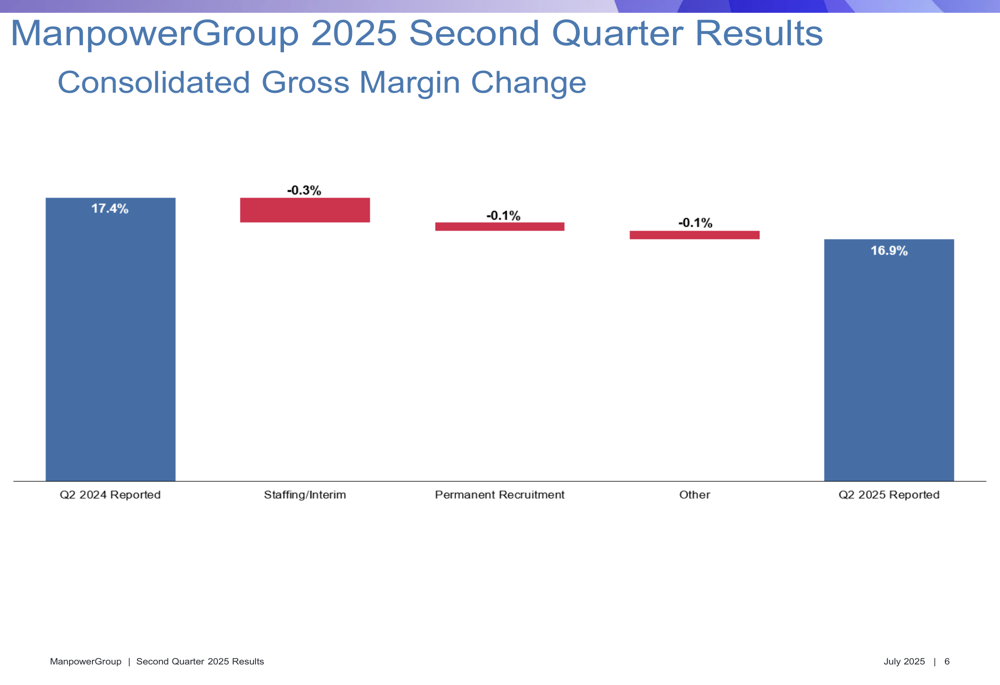

Gross margin declined to 16.9% from 17.4% in the same quarter last year, with negative contributions from staffing/interim (-0.3%), permanent recruitment (-0.1%), and other segments (-0.1%).

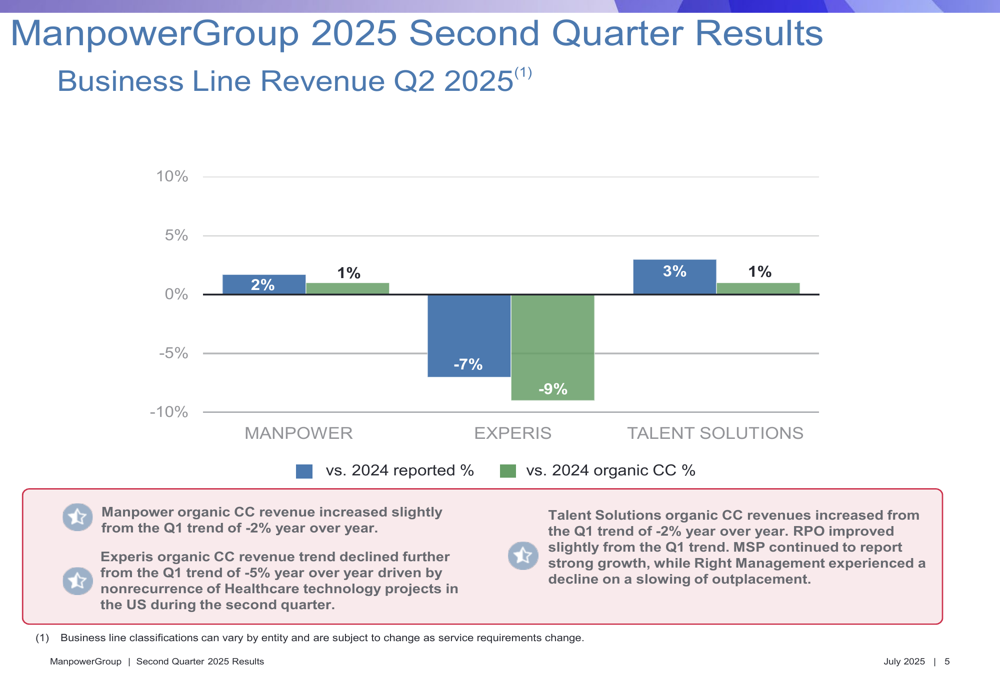

The company’s business lines showed divergent performance, with Manpower and Talent Solutions returning to growth while Experis experienced declines:

Regional Performance Analysis

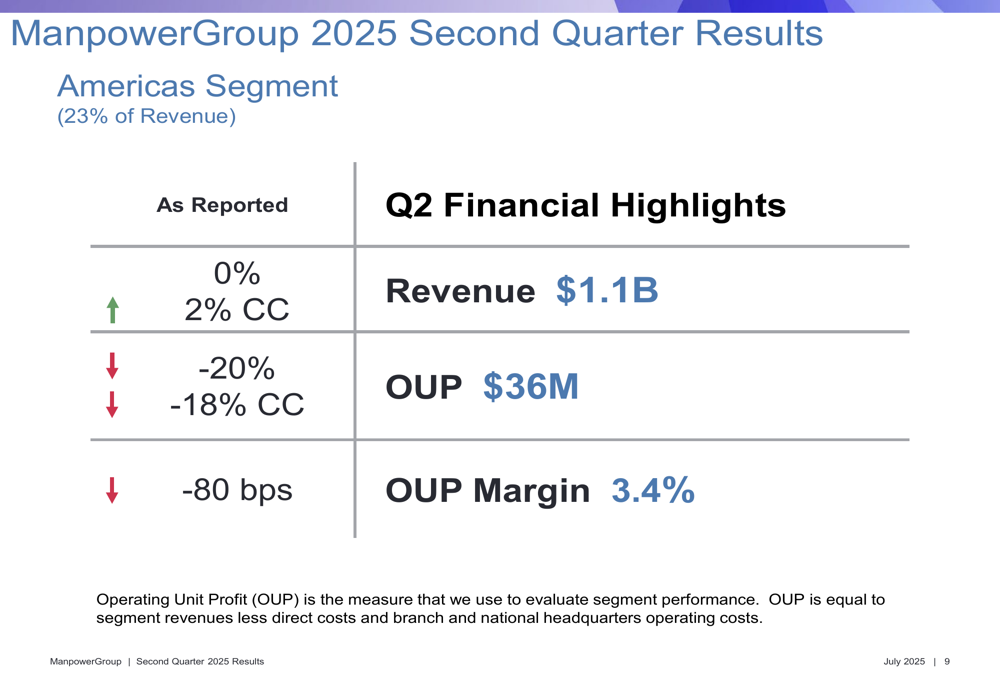

ManpowerGroup’s global footprint revealed significant regional disparities in performance. The Americas segment, representing 23% of total revenue, reported flat revenue growth but a 20% decline in operating unit profit:

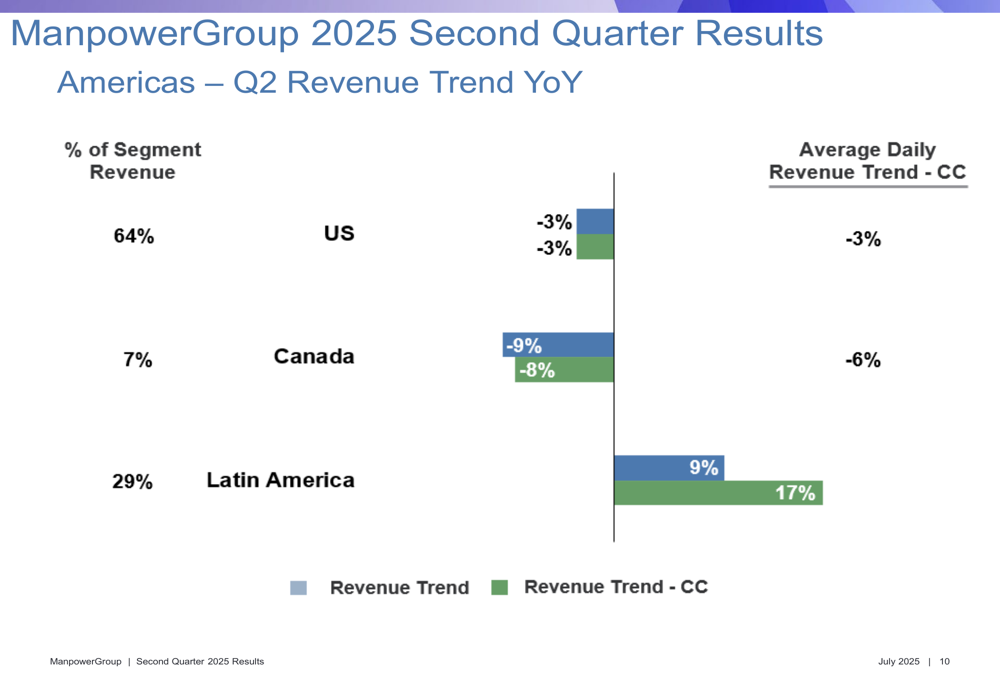

Within the Americas, Latin America emerged as a bright spot with 9% reported revenue growth (17% in constant currency), while the US (-3%) and Canada (-9%) continued to face challenges.

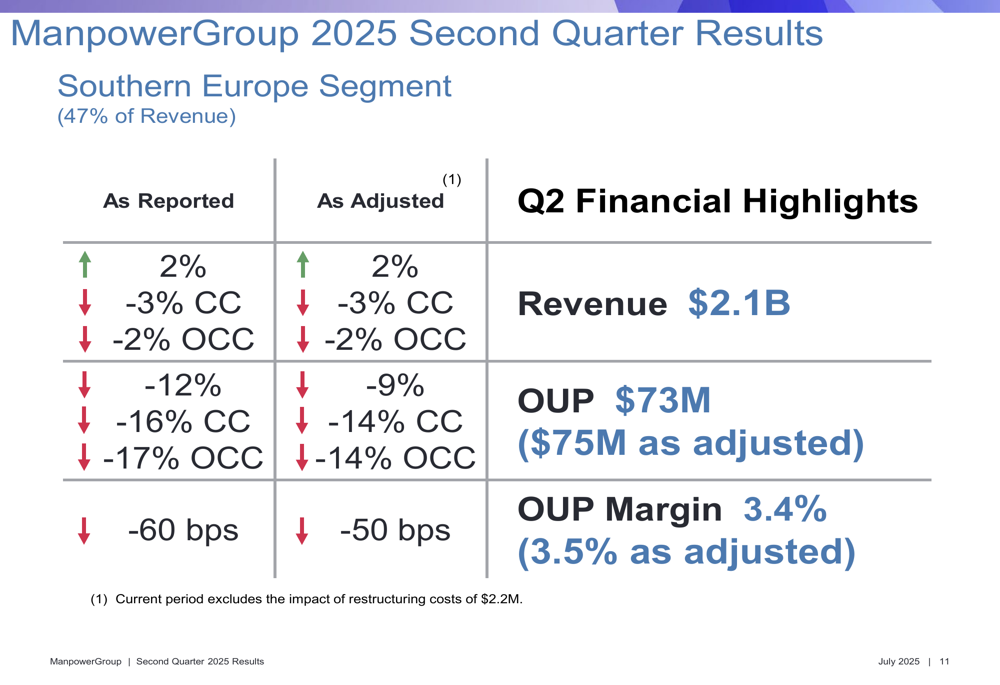

Southern Europe, the company’s largest segment at 47% of revenue, showed modest 2% reported revenue growth but a 12% decline in operating unit profit:

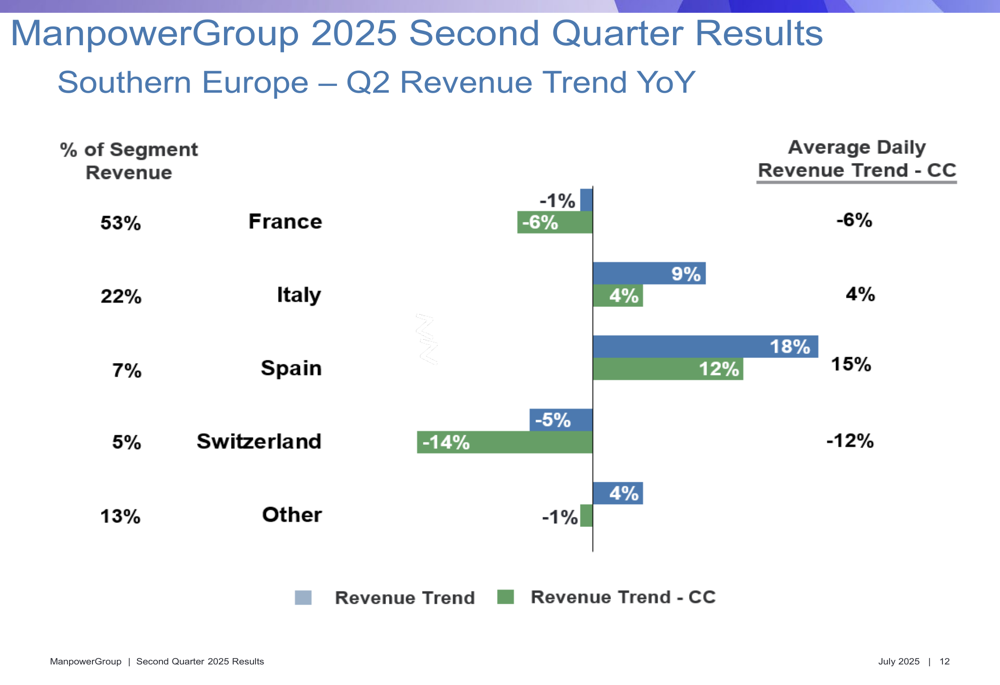

The region’s performance was mixed, with Italy (9% growth) and Spain (18% growth) showing strength, while France, representing over half of the segment’s revenue, declined 1% (-6% in constant currency).

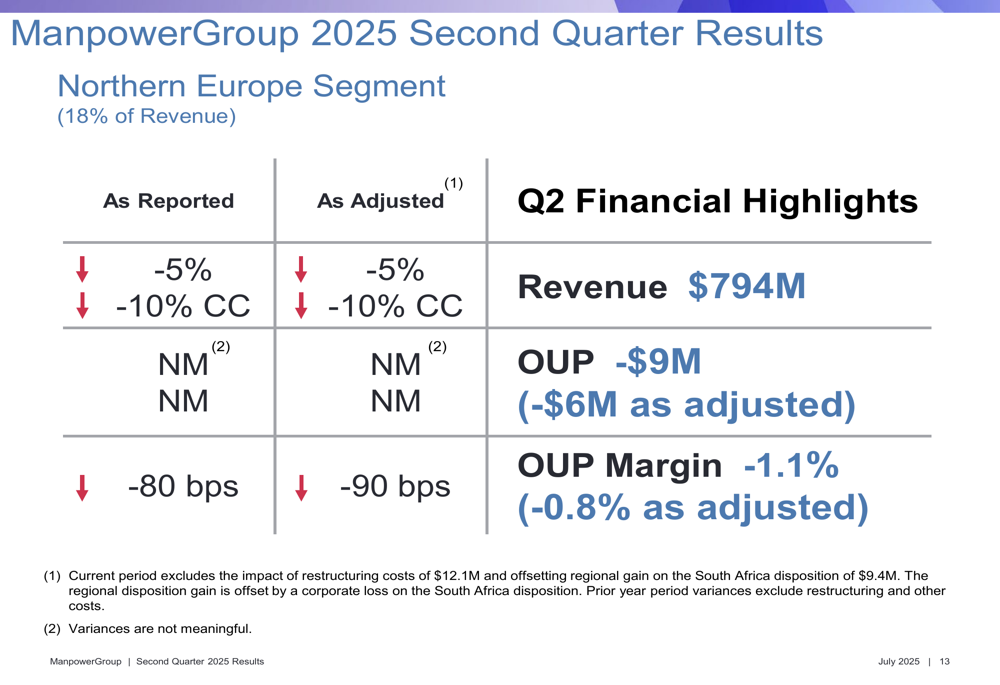

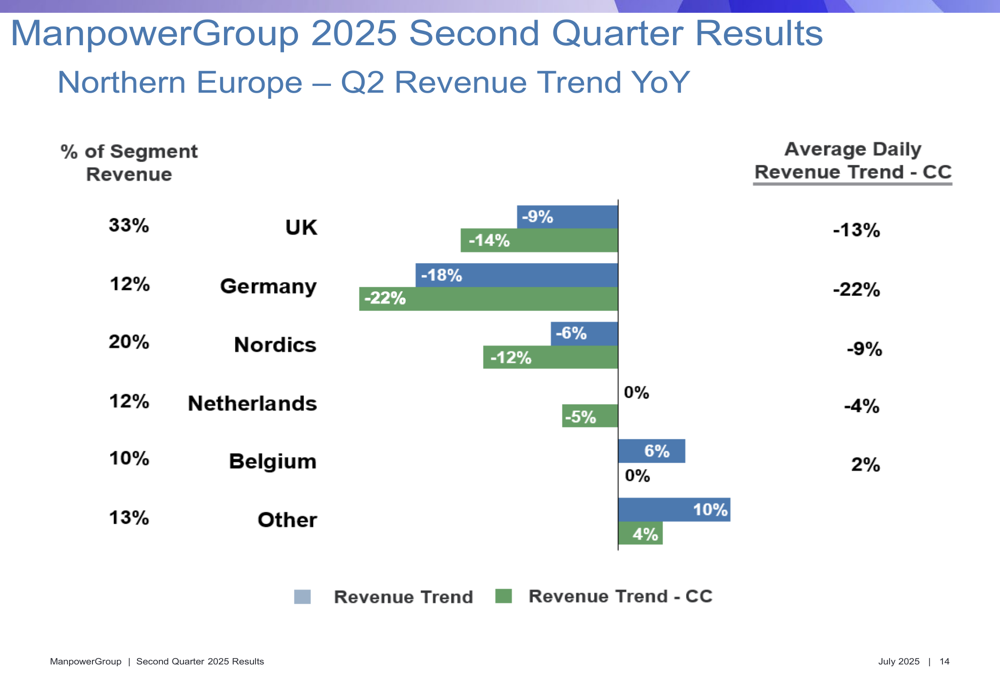

Northern Europe continued to struggle, with revenue declining 5% and operating unit profit turning negative at -$9 million:

The UK market, representing a third of the Northern Europe segment, declined 9% (-14% in constant currency), while Germany saw an 18% drop (-22% in constant currency). The Netherlands showed stability at 0% growth, while Belgium grew 6%.

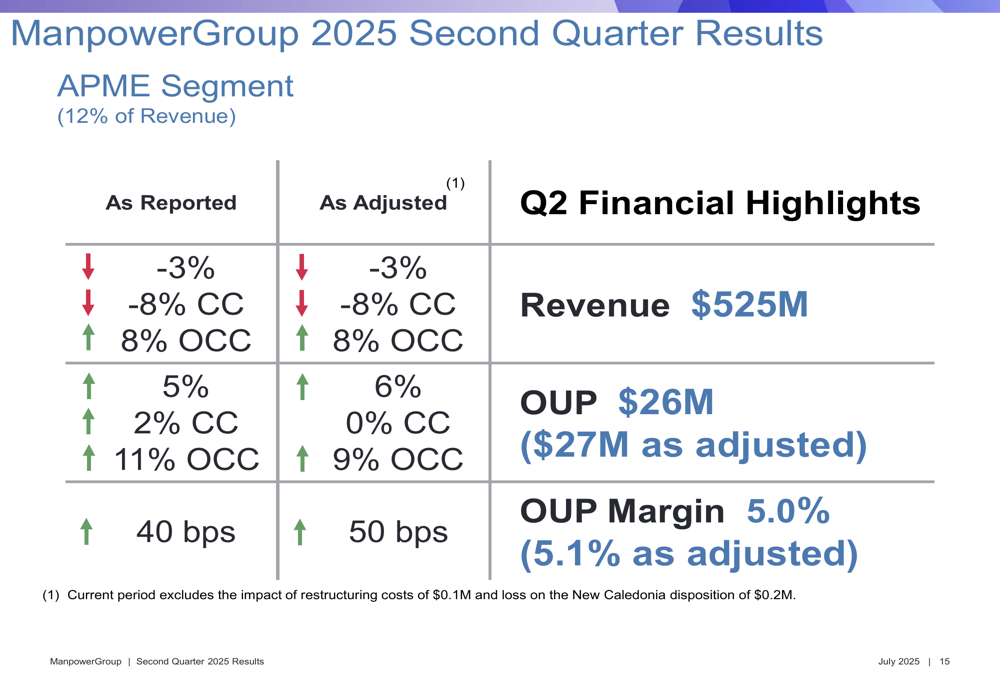

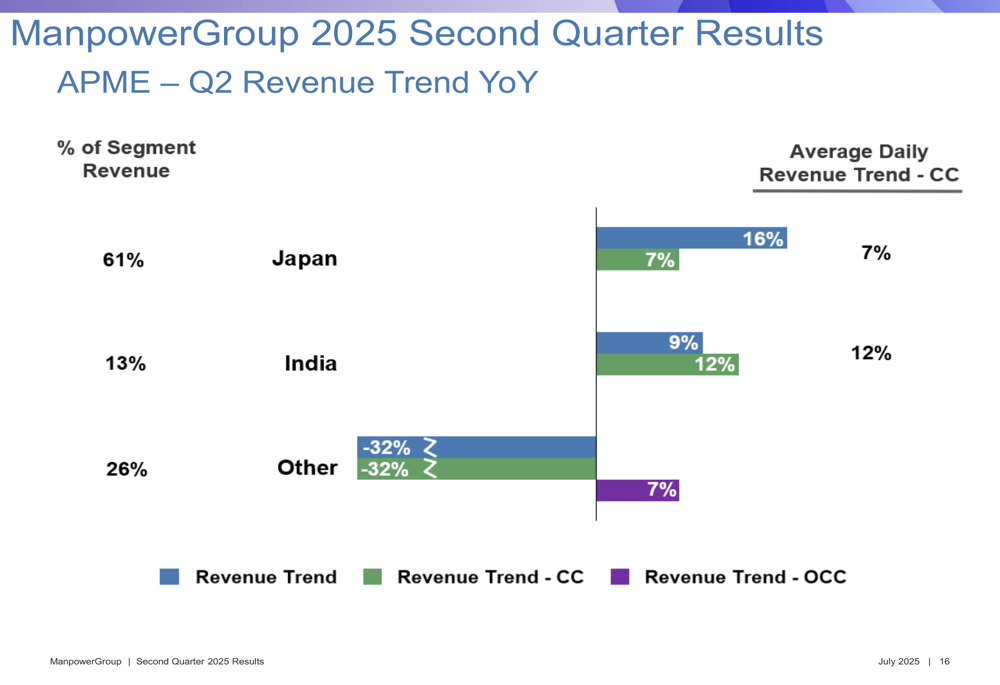

The Asia Pacific, Middle East, and Eastern Europe (APME) segment demonstrated resilience with operating unit profit growing 5% despite a 3% revenue decline:

Japan, which accounts for 61% of the segment’s revenue, grew 16% (7% in constant currency), while India increased 9% (12% in constant currency).

Strategic Initiatives & Financial Position

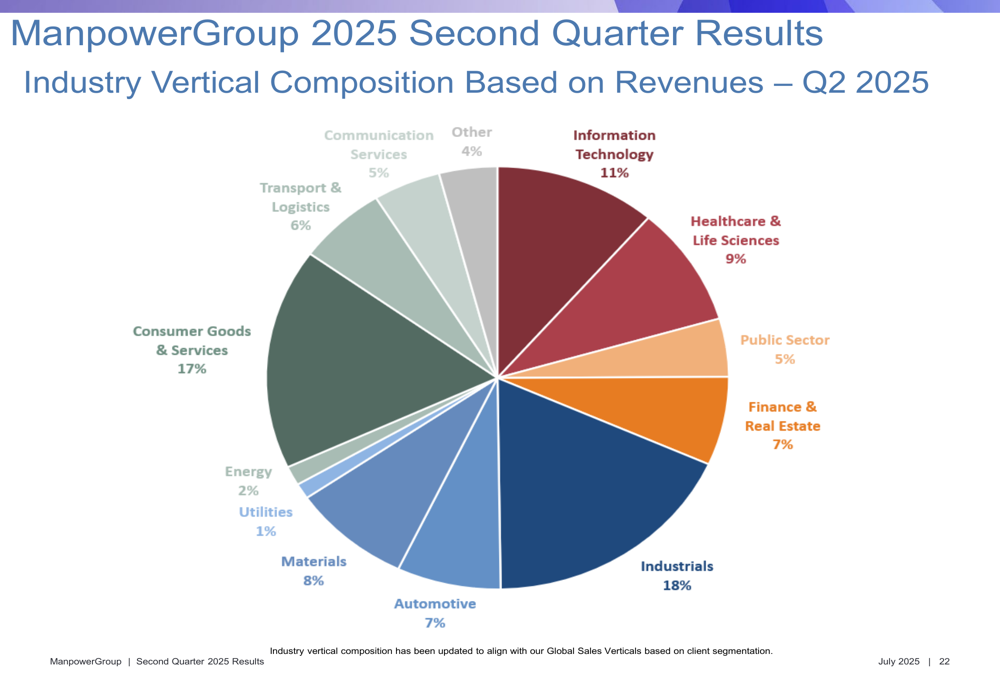

ManpowerGroup’s presentation highlighted ongoing restructuring efforts and strategic repositioning. The company’s industry vertical composition shows diversification across sectors, with the largest exposures to Industrials (18%), Consumer Goods & Services (17%), and Information Technology (11%):

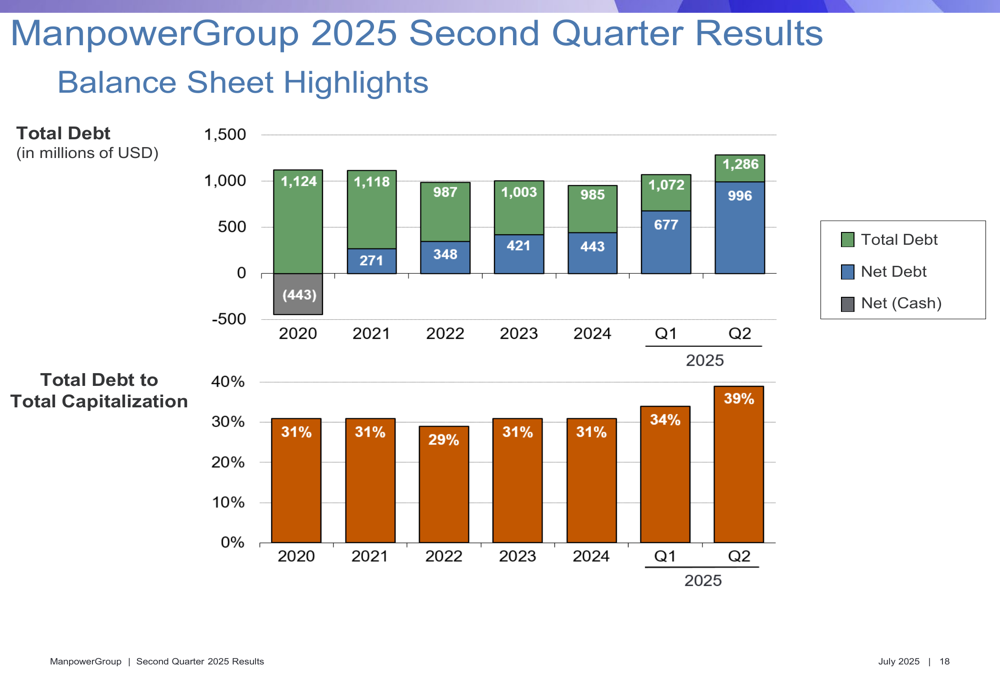

The company’s debt position has increased notably, with total debt rising to $1,286 million in Q2 2025 from $1,072 million in Q1 2025. The total debt to total capitalization ratio increased to 39% from 34% in the previous quarter:

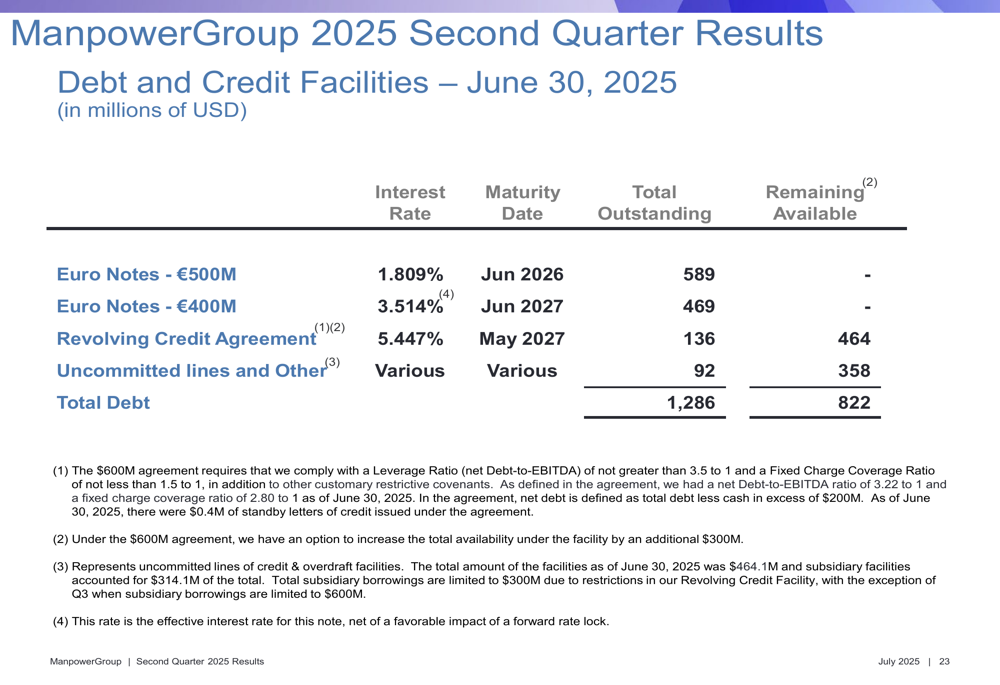

This debt increase comes amid ongoing restructuring efforts and strategic investments. The company’s debt structure includes €500 million in Euro Notes maturing in June 2026 and €400 million maturing in June 2027, along with revolving credit facilities:

Outlook & Forward Guidance

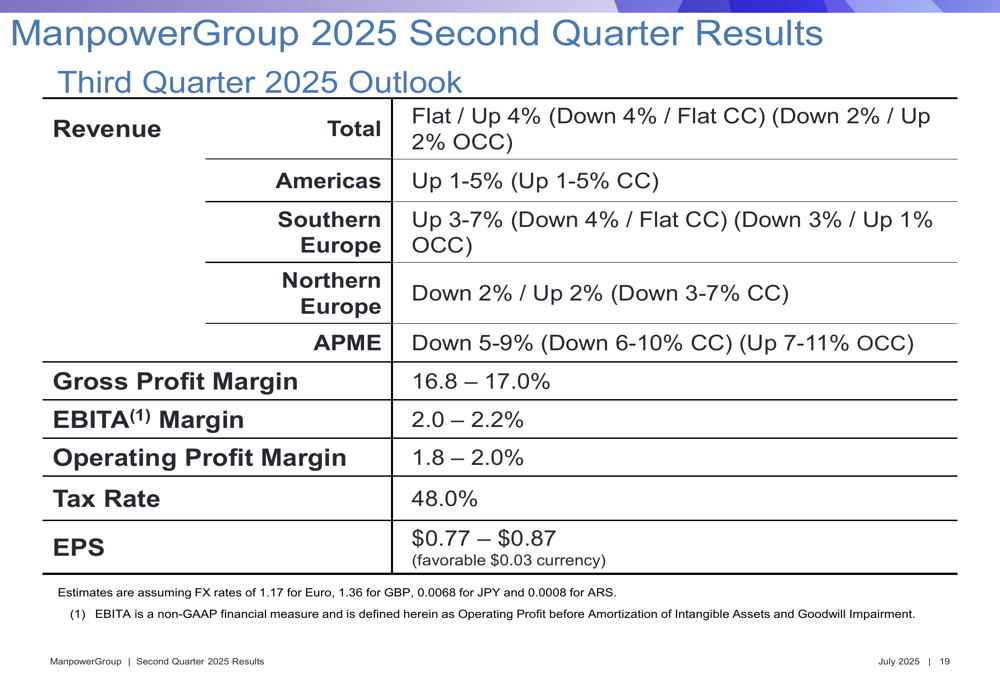

Looking ahead to the third quarter of 2025, ManpowerGroup provided guidance for revenue to be flat to up 4% on a reported basis, but down 4% to flat in constant currency. The company expects adjusted EPS of $0.77 to $0.87, which includes a favorable currency impact of $0.03.

The outlook varies significantly by region, with the Americas expected to grow 1-5%, Southern Europe projected at 3-7% growth, Northern Europe ranging from -2% to +2%, and APME forecasted to decline 5-9% on a reported basis but grow 7-11% on an organic constant currency basis.

Key Takeaways

ManpowerGroup emphasized several positive developments despite the mixed results. Latin America and Asia Pacific continued to experience good demand, while Europe and North America saw stabilizing trends in many markets. The Manpower and Talent Solutions brands returned to revenue growth, though Experis faced headwinds from sluggish professional staffing demand.

The company also highlighted its recognition by Forbes as America’s Best Temporary Staffing Firm, underscoring its market leadership position despite the challenging operating environment.

As ManpowerGroup navigates this complex global landscape, investors appear to be focusing on the company’s adjusted performance and signs of stabilization rather than the significant impairment charges that affected reported results. The premarket stock movement suggests cautious optimism about the company’s direction, though rising debt levels and ongoing restructuring point to continued transformation efforts ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.