5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Matson Inc (NYSE:MATX) presented its second quarter 2025 earnings results on July 31, showing mixed performance across its shipping segments as tariff uncertainties impacted its China service while domestic routes demonstrated resilience. Despite quarterly declines in key financial metrics, the company raised its full-year outlook based on strong year-to-date performance and operational adaptability.

Introduction & Market Context

Matson’s stock closed at $90.11 on the day of the presentation, up 3.18% during regular trading hours, though it dipped 0.81% in aftermarket trading. The stock is trading near its 52-week low of $86.97, significantly below its 52-week high of $169.12, reflecting investor concerns about ongoing trade tensions between the U.S. and China.

The company’s presentation highlighted market uncertainty stemming from tariffs, global trade dynamics, regulatory measures, and U.S. economic conditions. Despite these challenges, Matson emphasized its ability to navigate the volatile environment through service differentiation and operational flexibility.

Quarterly Performance Highlights

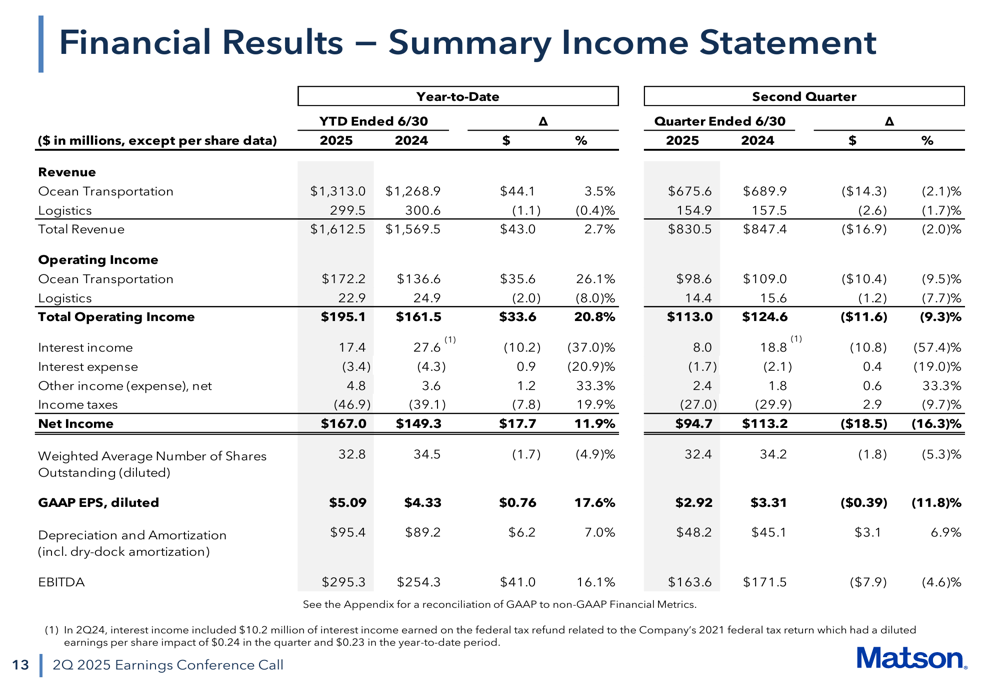

Matson reported declines across all major financial metrics for Q2 2025 compared to the same period in 2024. Total revenue decreased by 2.0% to $830.5 million, while operating income fell 9.3% to $113.0 million. Net income saw a more significant drop of 16.3% to $94.7 million, with diluted earnings per share decreasing 11.8% to $2.92.

As shown in the following comprehensive income statement summary:

Despite the quarterly decline, Matson’s year-to-date performance through June 30, 2025, remained positive compared to 2024, with total revenue up 2.7% to $1,612.5 million and operating income increasing 20.8% to $195.1 million. This stronger first-half performance contributed to the company’s decision to raise its full-year outlook.

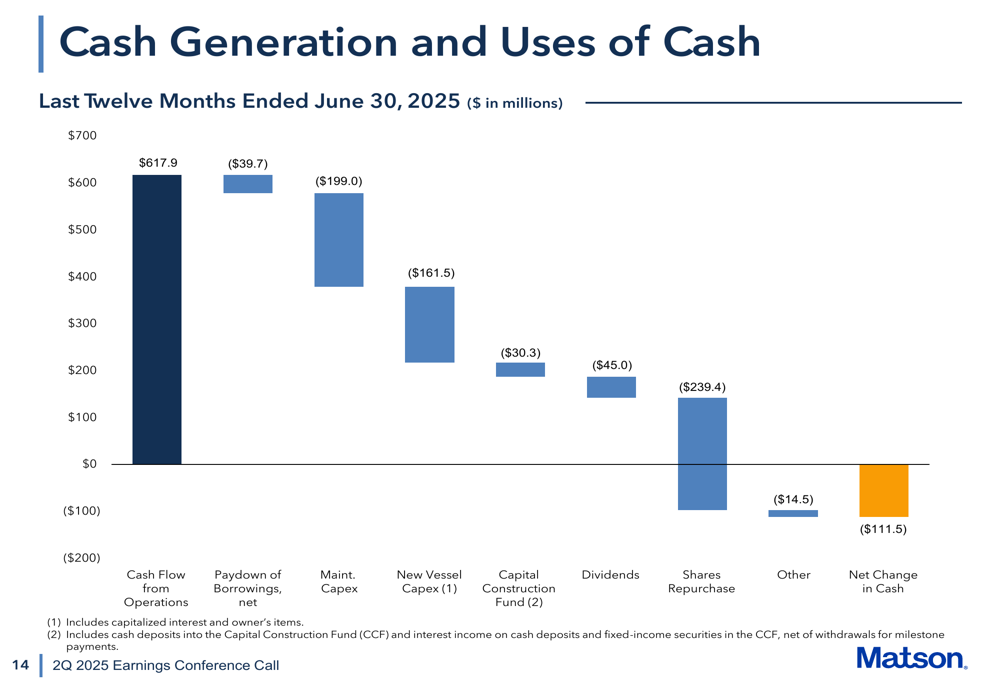

The company maintained robust cash generation, reporting $617.9 million in cash flow from operations for the twelve months ended June 30, 2025. This strong cash flow supported significant capital allocation activities, including share repurchases and debt reduction.

Segment Performance Analysis

Matson’s performance varied significantly across its different service segments, with domestic routes generally outperforming the China service.

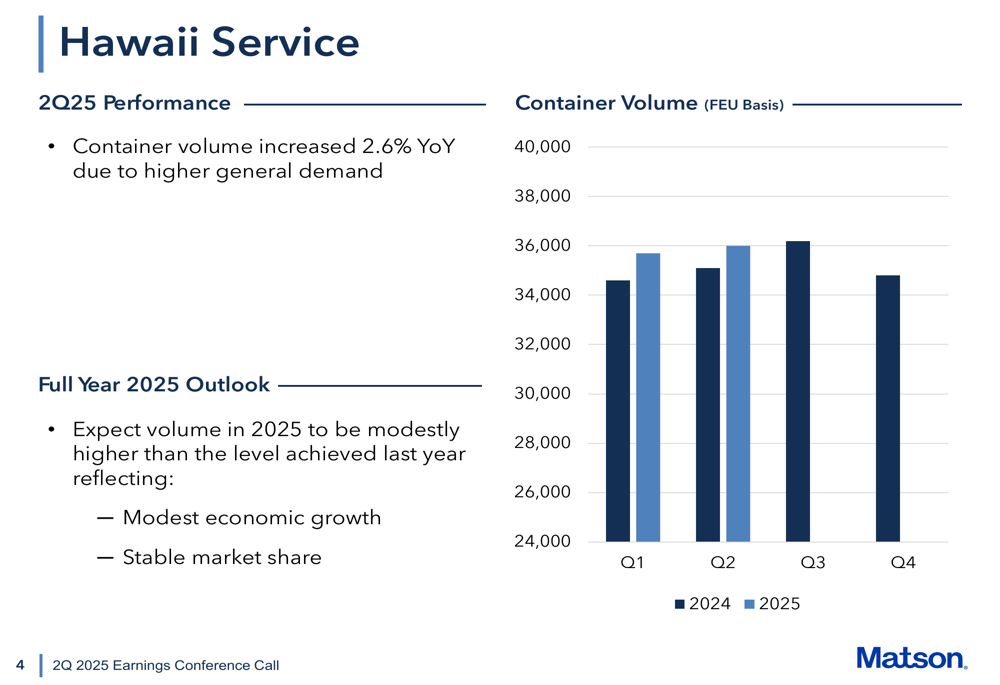

The Hawaii service showed positive momentum with container volume increasing 2.6% year-over-year due to higher general demand. Matson expects volume to remain modestly higher than last year, reflecting modest economic growth and stable market share in this important domestic market.

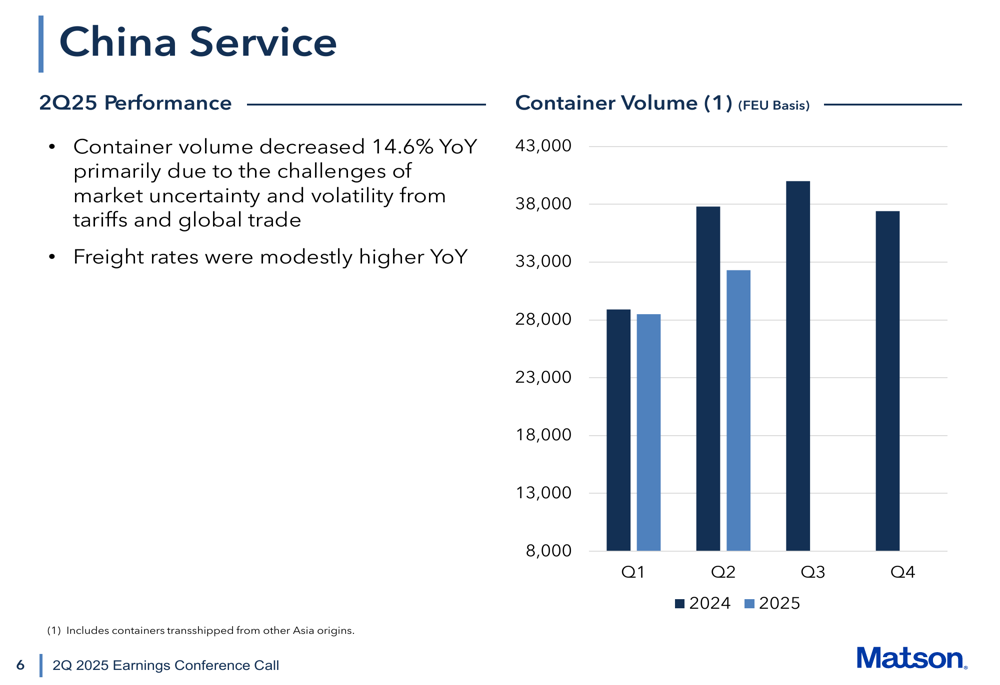

In contrast, the China service faced significant headwinds, with container volume decreasing 14.6% year-over-year primarily due to market uncertainty and volatility from tariffs and global trade tensions. The presentation detailed how customers were negotiating tariffs with trading partners and carriers were reducing capacity due to the volume downturn.

Matson noted that demand rebounded in mid-May after the U.S. and China agreed to a temporary reduced level of tariffs, but volume has stabilized modestly below prior year levels. The company also highlighted a shift in production throughout Asia as customers respond to tariff pressures, with higher container volume levels outside of China and the opening of a new expedited Ho Chi Minh service.

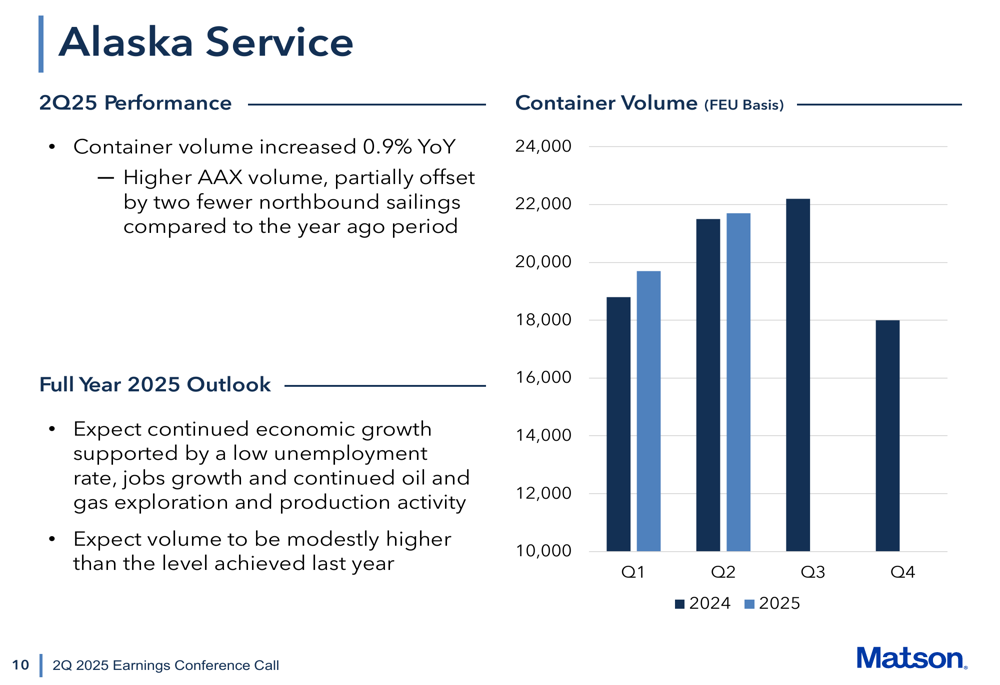

Alaska service showed modest growth with container volume increasing 0.9% year-over-year, driven by higher AAX volume despite two fewer northbound sailings compared to the prior year. The company expects continued economic growth in Alaska supported by low unemployment, jobs growth, and ongoing oil and gas activity.

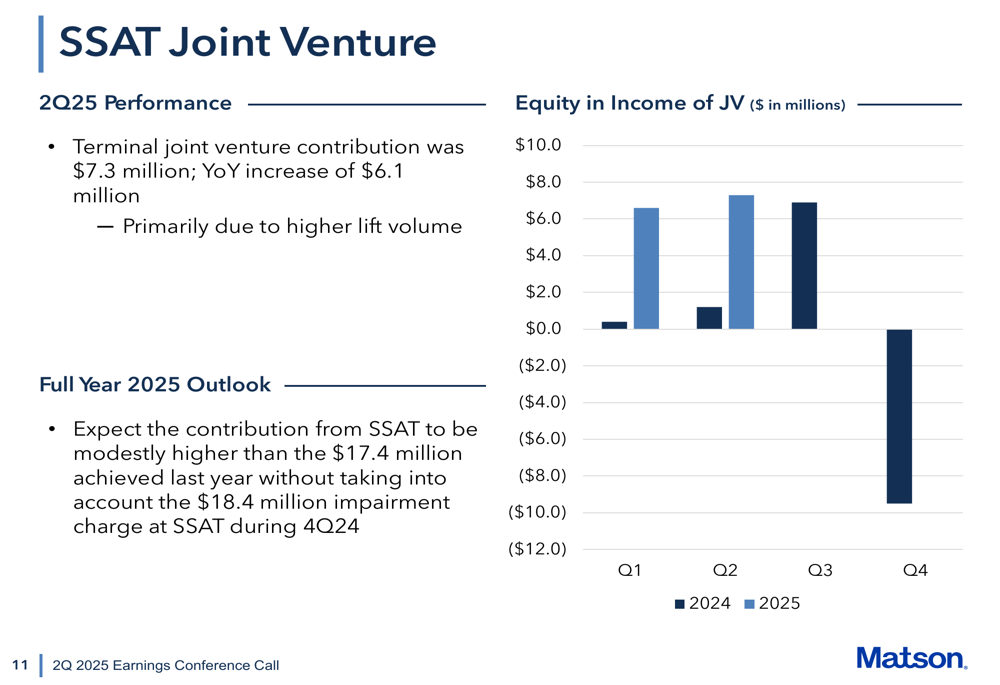

The SSAT terminal joint venture was a bright spot, contributing $7.3 million in the quarter, a year-over-year increase of $6.1 million primarily due to higher lift volume. For the full year 2025, Matson expects the contribution from SSAT to be modestly higher than the $17.4 million achieved in 2024, excluding the $18.4 million impairment charge recorded in Q4 2024.

Financial Position and Cash Allocation

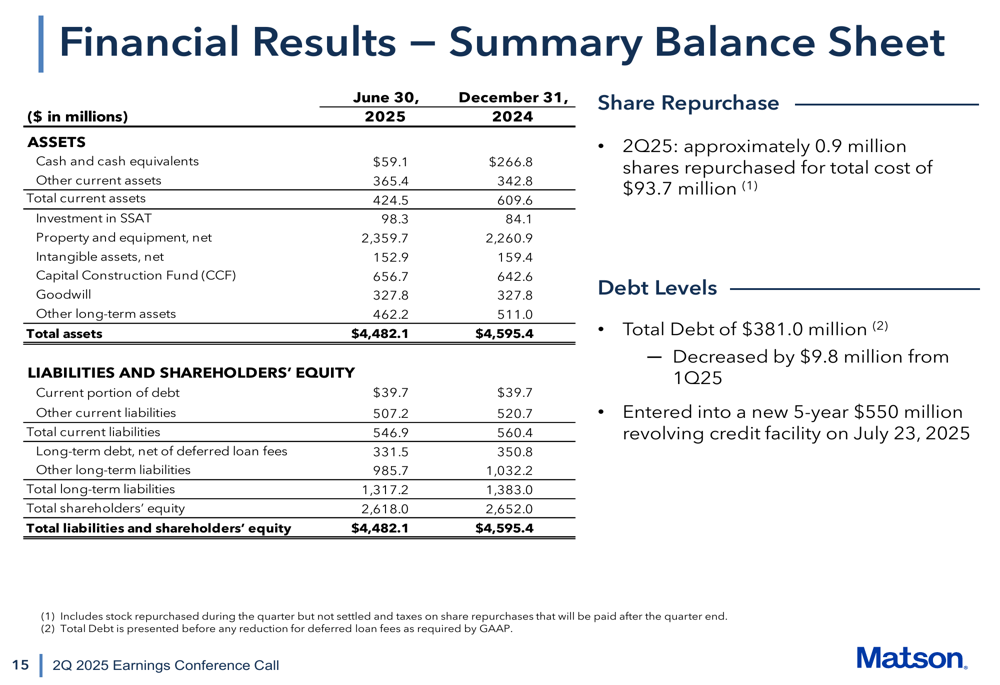

Matson’s balance sheet remained solid with total assets of $4,482.1 million as of June 30, 2025, compared to $4,595.4 million at the end of 2024. The company reduced its total debt to $381.0 million, a decrease of $9.8 million from Q1 2025, and entered into a new 5-year $550 million revolving credit facility on July 23, 2025.

The company continued its share repurchase program, buying back approximately 0.9 million shares for a total cost of $93.7 million during Q2 2025. This reflects management’s confidence in Matson’s long-term prospects despite near-term challenges.

Capital expenditures remain a significant focus, with expected new vessel construction milestone payments of $305 million in 2025, including owner’s items and capitalized interest expense. Maintenance and other capital expenditures are projected to be between $100-120 million. The company expects to make approximately $189 million in milestone payments in the second half of 2025 from the Capital Construction Fund (CCF).

Forward-Looking Statements

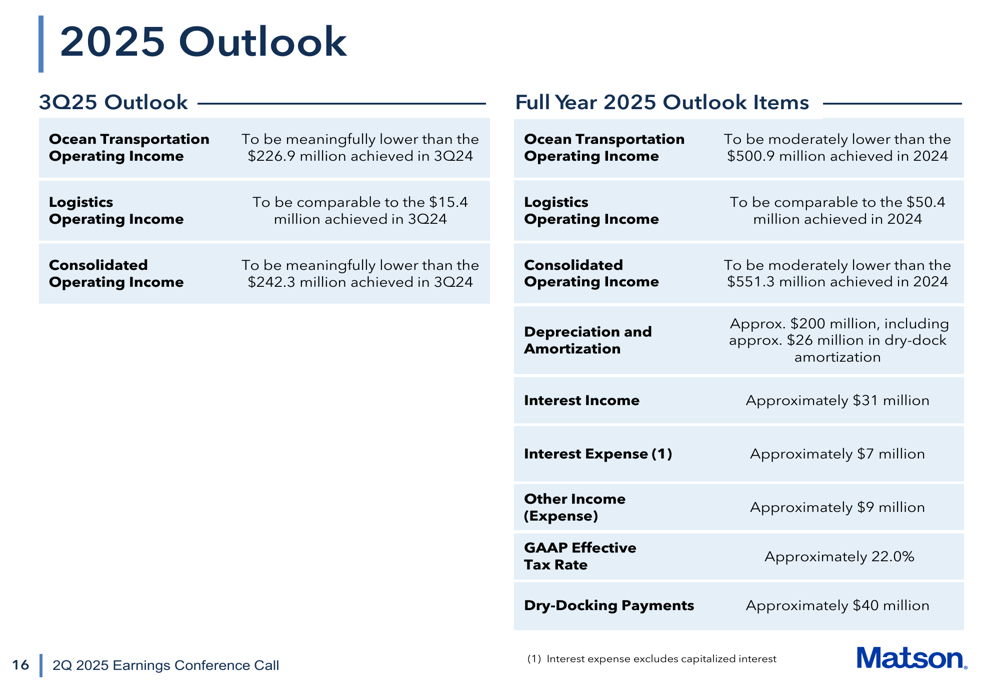

Despite the quarterly decline, Matson raised its full-year 2025 outlook based on strong first-half performance and operational adaptability. For the third quarter of 2025, the company expects ocean transportation operating income to be meaningfully lower than the $226.9 million achieved in Q3 2024, while logistics operating income is expected to be comparable to the $15.4 million achieved in the same period last year.

For the full year 2025, Matson projects ocean transportation operating income to be moderately lower than the $500.9 million achieved in 2024, while logistics operating income is expected to be comparable to the $50.4 million achieved last year. The company anticipates depreciation and amortization of approximately $200 million, including about $26 million in dry-dock amortization, and an effective tax rate of approximately 22.0%.

Management emphasized that Matson is well-positioned in its tradelanes and logistics operations to manage through the current period of market uncertainty and volatility. The company is focusing on maintaining its two fastest and most reliable transpacific services while supporting customers as they diversify their manufacturing base throughout Asia.

"It is during uncertain times like these that Matson demonstrates its unique capabilities and service qualities across our organization," the company stated in its closing remarks, highlighting its commitment to providing world-class services and customer support in an evolving marketplace.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.