Elastic launches GPU-accelerated inference service for AI workflows

Introduction & Market Context

Matthews International Corporation (NASDAQ:MATW) reported its third quarter fiscal 2025 results on August 6, 2025, showing significant improvement in net income despite lower sales following the divestiture of its SGK Business. The company’s shares, which have faced pressure in recent months, have shown signs of recovery with a 3.84% increase to $23.16 in the most recent trading session, though still well below the 52-week high of $32.24.

The quarter marks a substantial turnaround from Q2 2025, when Matthews reported disappointing results with a net loss of $8.9 million. This improvement comes as the company continues to execute on its strategic repositioning and cost reduction initiatives while maintaining its full-year adjusted EBITDA guidance.

Quarterly Performance Highlights

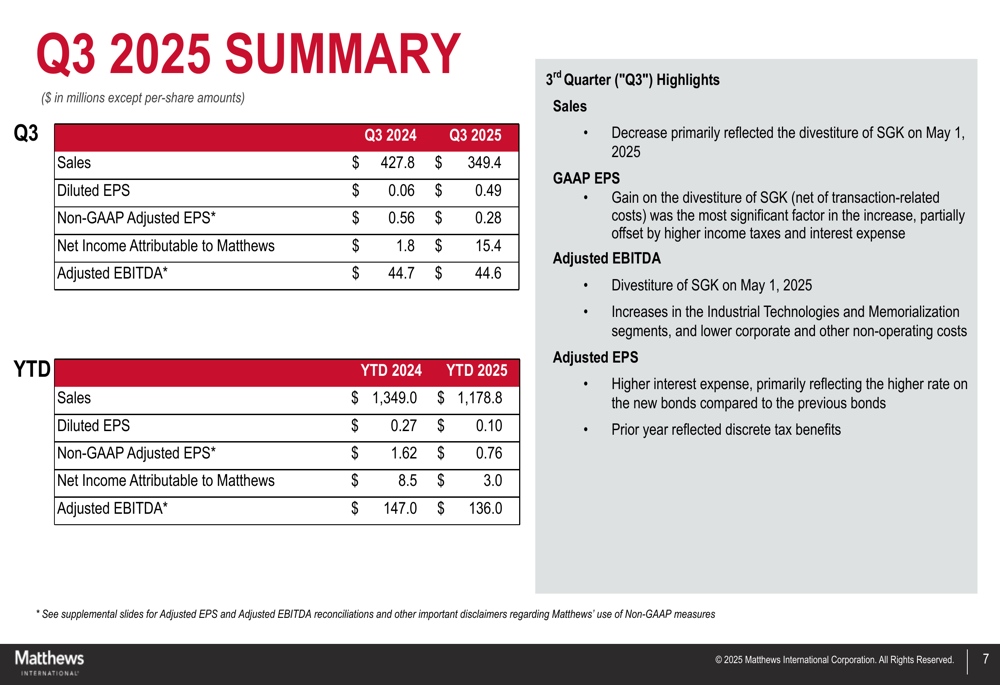

Matthews reported Q3 2025 sales of $349.4 million, down from $427.8 million in the same period last year, with the decrease primarily reflecting the May 1, 2025 divestiture of the SGK Business. Despite lower revenue, the company’s net income attributable to Matthews surged to $15.4 million ($0.49 per diluted share), compared to just $1.8 million ($0.06 per diluted share) in Q3 2024.

As shown in the following comprehensive financial summary:

The gain on the SGK divestiture (net of transaction-related costs) was the most significant factor in the net income increase, though this was partially offset by higher income taxes and interest expense. Adjusted EBITDA remained essentially flat at $44.6 million compared to $44.7 million in the prior year, despite the divestiture, reflecting improved performance in the remaining business segments.

Adjusted EPS, which excludes the impact of the divestiture and other one-time items, declined to $0.28 from $0.56 in the prior year, primarily due to higher interest expense reflecting the higher rate on new bonds compared to previous bonds, as well as the absence of discrete tax benefits that benefited the prior year’s results.

Segment Analysis

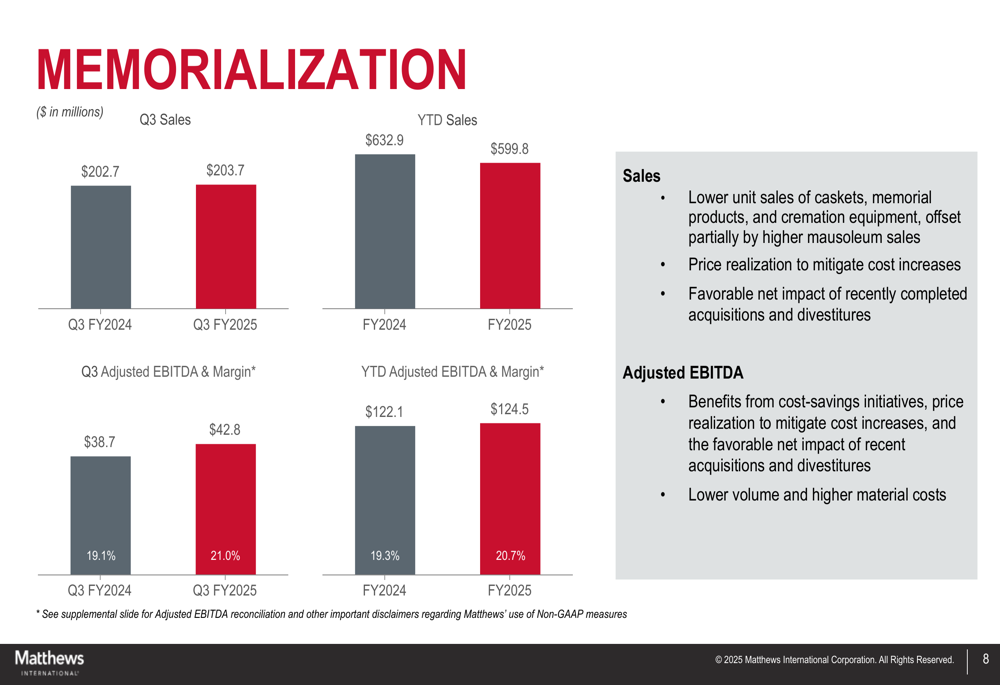

The Memorialization segment, which includes caskets, memorial products, and cremation equipment, showed improved profitability despite relatively flat sales. Q3 2025 sales were $203.7 million, compared to $202.7 million in Q3 2024, while adjusted EBITDA increased to $42.8 million (21.0% margin) from $38.7 million (19.1% margin).

The segment’s performance is illustrated in the following chart:

The improved profitability was driven by cost-savings initiatives and price realization, which more than offset lower unit sales of caskets, memorial products, and cremation equipment. The acquisition of The Dodge Company also contributed positively to the segment’s results.

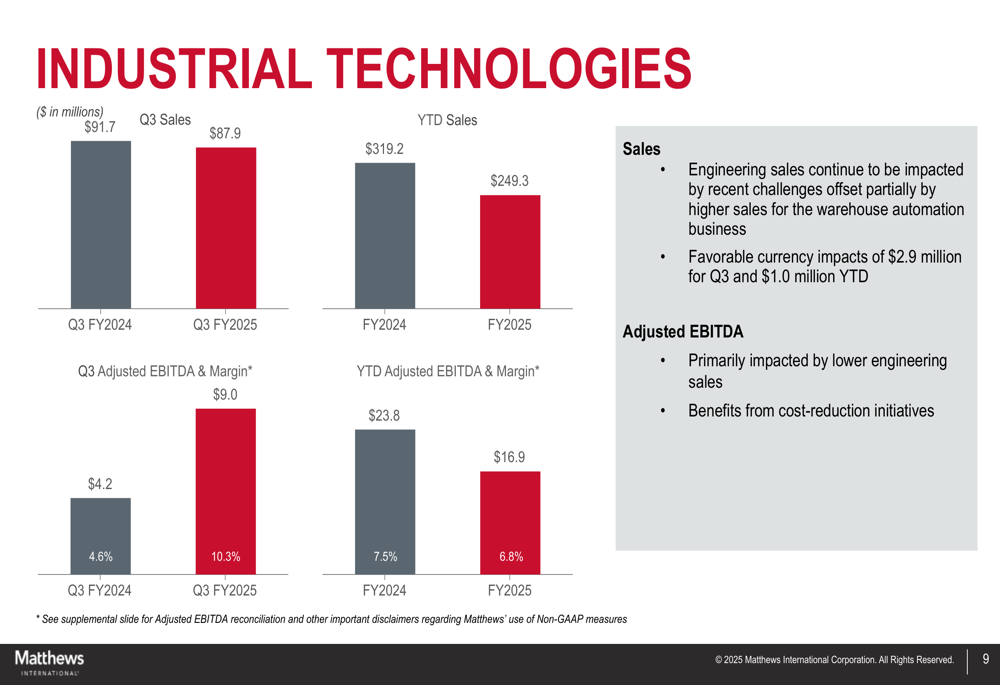

The Industrial Technologies segment showed signs of recovery with adjusted EBITDA more than doubling to $9.0 million (10.3% margin) from $4.2 million (4.6% margin) in the prior year, despite a slight sales decrease to $87.9 million from $91.7 million.

As shown in the segment performance breakdown:

While engineering sales continue to be impacted by challenges related to the Tesla (NASDAQ:TSLA) litigation, the warehouse automation business showed improvement. The company also noted significant customer interest in its energy storage solutions, with quotes exceeding $150 million since early February 2025.

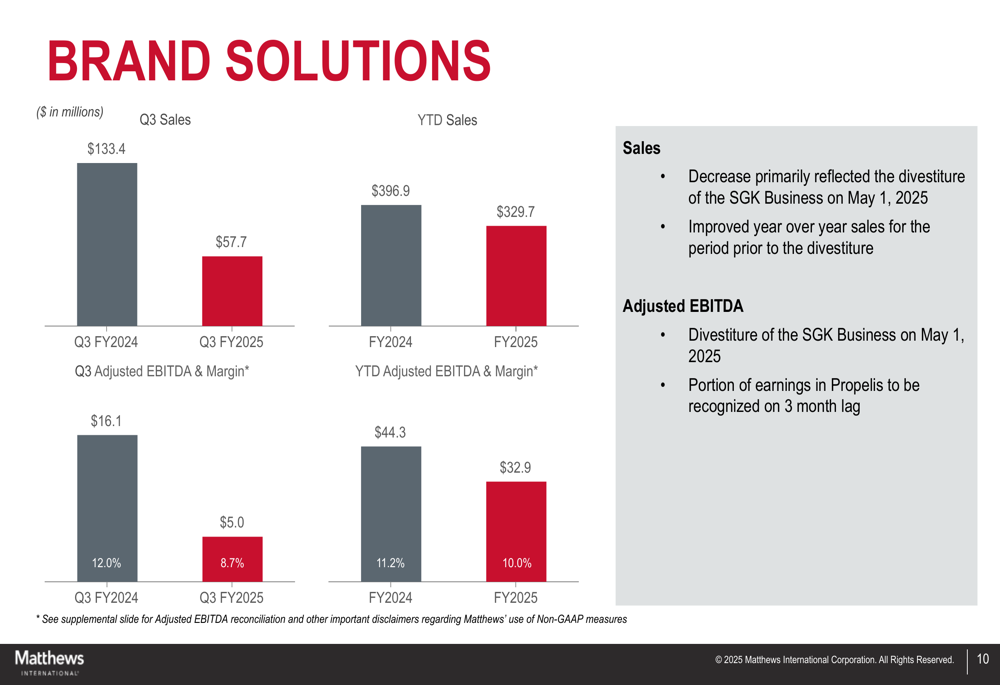

The Brand Solutions segment, significantly impacted by the SGK divestiture, reported Q3 2025 sales of $57.7 million, down from $133.4 million in Q3 2024. Adjusted EBITDA declined to $5.0 million from $16.1 million in the prior year.

The company noted that a portion of earnings from Propelis, related to the divested business, will be recognized on a three-month lag, which will impact future results.

Strategic Initiatives and Outlook

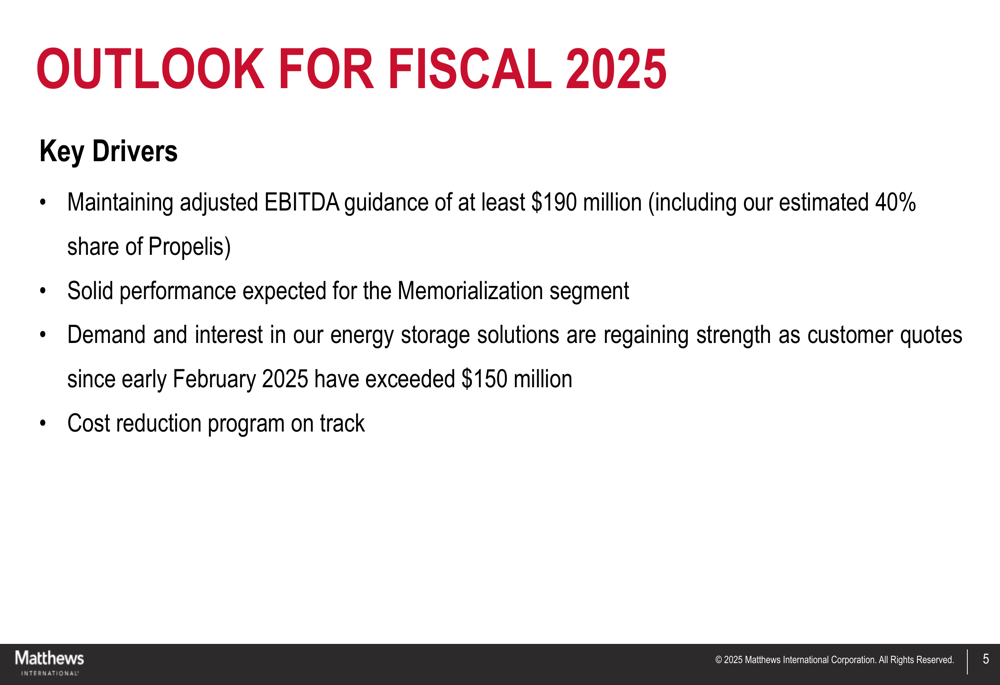

Matthews maintained its fiscal 2025 adjusted EBITDA guidance of at least $190 million, including the estimated 40% share of Propelis. This guidance reflects management’s confidence in the company’s strategic direction despite recent challenges.

The company’s cost reduction program remains on track, and management expressed optimism about the Memorialization segment’s expected solid performance. Additionally, demand and interest in Matthews’ energy storage solutions are regaining strength, as evidenced by the significant increase in customer quotes since early February 2025.

As outlined in the company’s outlook:

This outlook represents a stabilization from the challenging Q2 2025 results, when the company missed both EPS and revenue forecasts. The maintenance of the full-year guidance suggests that management believes the worst of the challenges may be behind them.

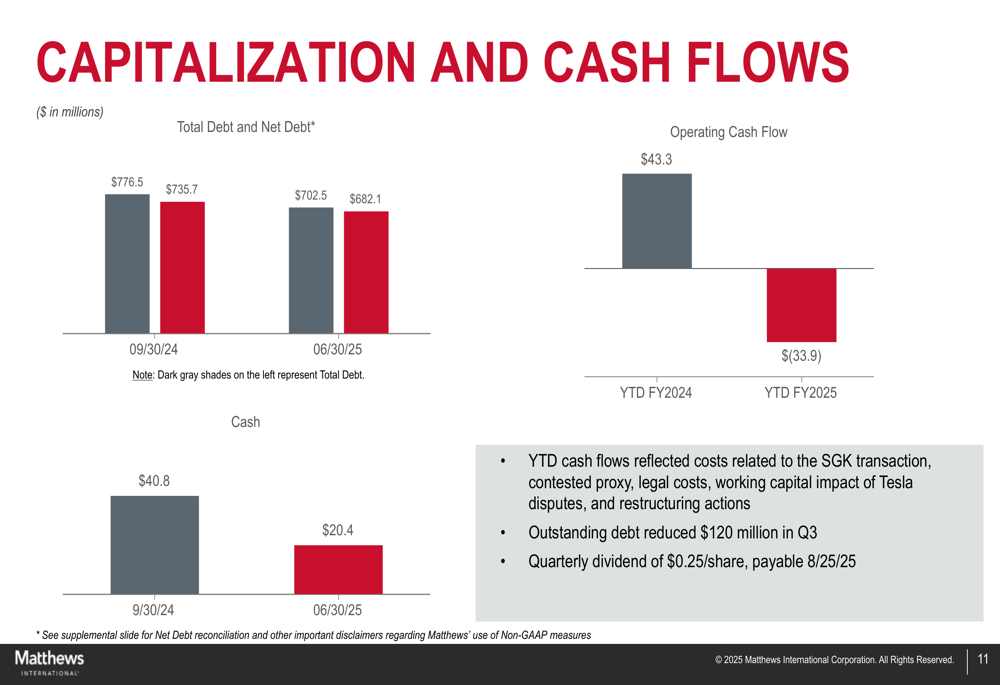

Financial Position and Capital Allocation

Matthews made significant progress in reducing its debt burden during the quarter, with outstanding debt reduced by $120 million in Q3 2025. As of June 30, 2025, total debt stood at $702.5 million, down from $776.5 million as of September 30, 2024, while net debt (total debt less cash) was $682.1 million.

The company’s capitalization and cash flow position is illustrated in the following chart:

Year-to-date operating cash flow remained negative at $(33.9) million, compared to positive $43.3 million in the prior year period. The company attributed this to costs related to the SGK transaction, contested proxy, legal costs, working capital impact of Tesla disputes, and restructuring actions.

Despite these cash flow challenges, Matthews maintained its quarterly dividend of $0.25 per share, payable on August 25, 2025, continuing its commitment to shareholder returns.

The company’s ability to maintain its dividend while reducing debt highlights management’s confidence in the underlying business despite recent challenges. However, the negative operating cash flow remains a concern that investors will likely monitor closely in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.