ServiceNow nears deal to acquire Veza for at least $1 bln - The Information

Introduction & Market Context

Matthews International Corporation (NASDAQ:MATW) reported its fourth quarter and full-year fiscal 2025 results on November 21, 2025, revealing a significant strategic transformation through divestitures alongside mixed financial performance. The company’s shares closed at $24.65, down 1.44% following the earnings release, despite beating analyst expectations with an adjusted EPS of $0.50 compared to the forecasted $0.23.

The presentation, delivered by CEO Joseph Bartolacci and CFO Steven Nicola, highlighted the company’s ongoing portfolio reshaping efforts, debt reduction initiatives, and improved profitability metrics amid lower overall revenue due to strategic divestitures.

Strategic Portfolio Transformation

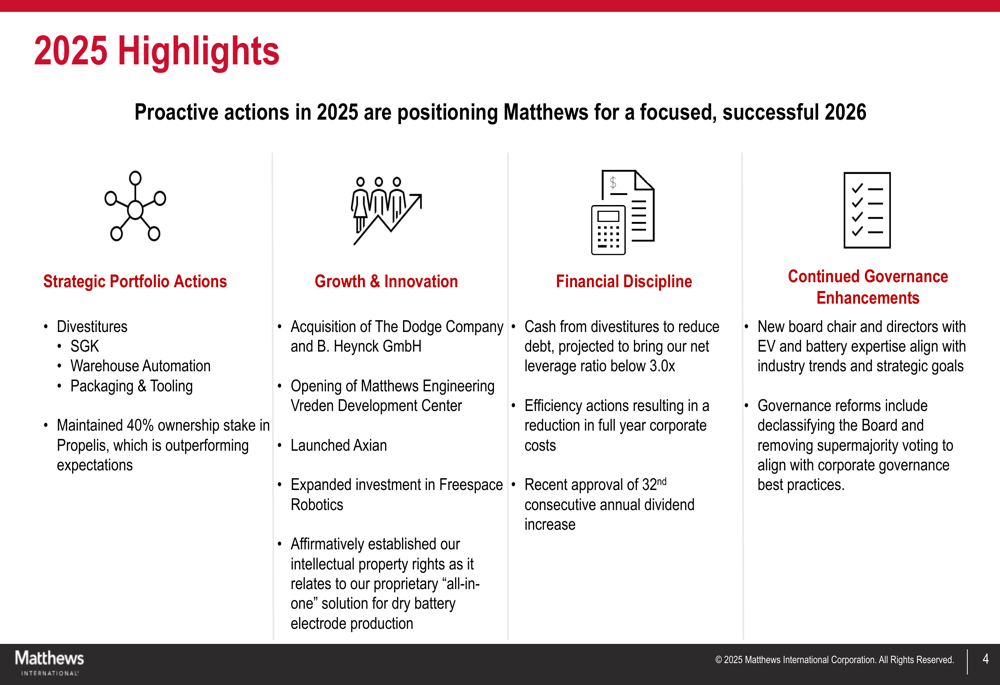

Matthews International undertook significant portfolio actions in fiscal 2025, positioning the company for a more focused future. The company completed several major divestitures, including its SGK business, warehouse automation, and packaging & tooling operations, while maintaining a 40% ownership stake in Propelis, which management noted is outperforming expectations.

As shown in the following strategic highlights:

Simultaneously, Matthews strengthened its core operations through strategic acquisitions, including The Dodge Company and B. Heynck GmbH. The company also expanded its technology capabilities by opening the Matthews Engineering Vreden Development Center and increasing investment in Freespace Robotics.

A key strategic achievement was establishing intellectual property rights for the company’s proprietary "all-in-one" solution for dry battery electrode production, positioning Matthews in the growing energy storage market. During the earnings call, CEO Bartolacci emphasized the value of this technology, stating, "We are seeing increased interest. The technology is highly valuable and focused on any type of energy storage."

Quarterly Performance Highlights

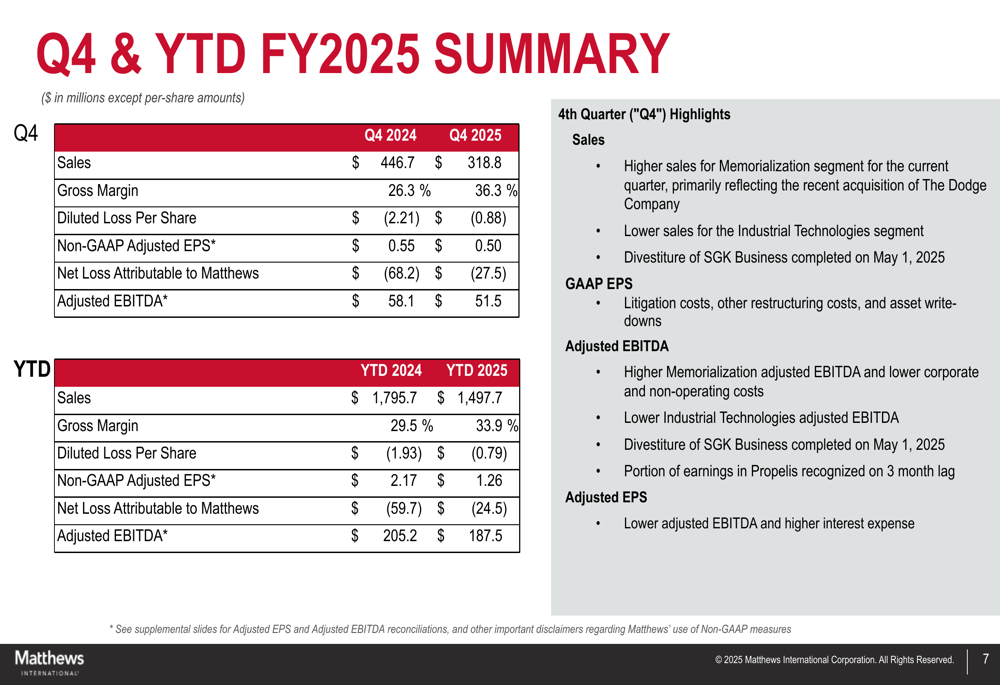

Matthews International’s fourth quarter results reflected both the impact of divestitures and underlying operational improvements. While headline numbers showed declines, the company achieved significant margin expansion and beat analyst expectations.

The following summary highlights key financial metrics for Q4 and the full fiscal year:

For Q4 FY2025, Matthews reported:

- Sales of $318.8 million, down from $446.7 million in Q4 FY2024

- Gross margin of 36.3%, up from 26.3% in the prior-year period

- Adjusted EBITDA of $51.5 million, compared to $58.1 million a year earlier

- Adjusted EPS of $0.50, exceeding analyst expectations of $0.23 but down from $0.55 in Q4 FY2024

For the full fiscal year 2025:

- Sales of $1,497.7 million, compared to $1,795.7 million in FY2024

- Gross margin improvement to 33.9% from 29.5%

- Adjusted EBITDA of $187.5 million, versus $205.2 million in the prior year

- Adjusted EPS of $1.26, down from $2.17 in FY2024

Segment Performance

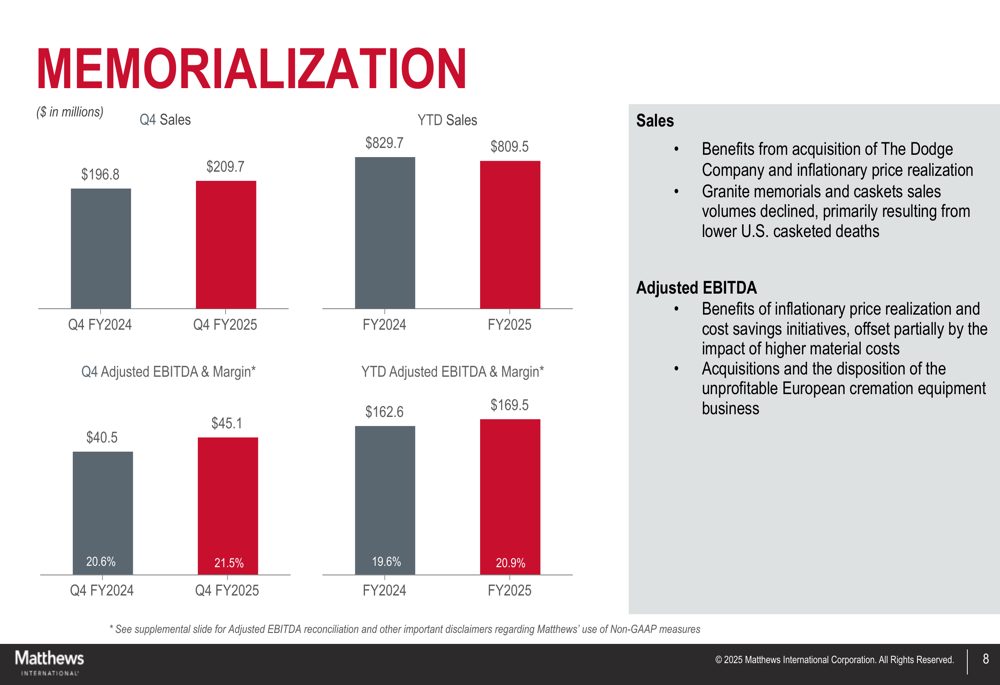

Matthews’ business segments showed divergent performance, with Memorialization emerging as a bright spot while Industrial Technologies faced challenges.

The Memorialization segment demonstrated solid growth, as shown in the following chart:

Memorialization sales increased to $209.7 million in Q4 FY2025 from $196.8 million in the prior year, with adjusted EBITDA rising to $45.1 million from $40.5 million. The segment’s margin expanded to 21.5% from 20.6%, benefiting from the acquisition of The Dodge Company, inflationary price realization, and cost-saving initiatives.

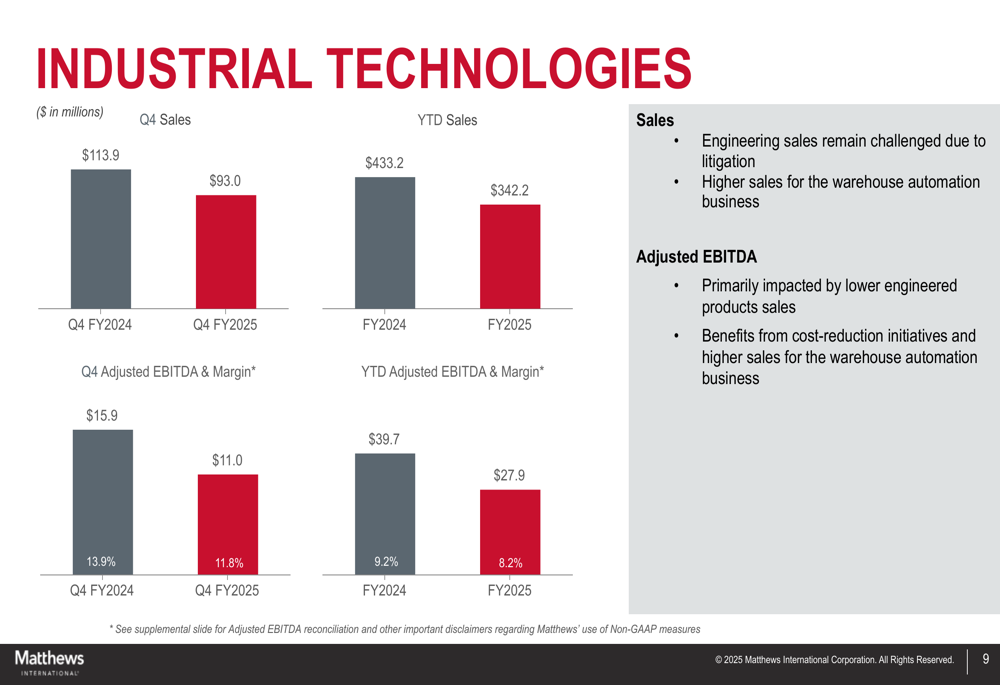

In contrast, the Industrial Technologies segment experienced declines:

Industrial Technologies sales fell to $93.0 million in Q4 FY2025 from $113.9 million in Q4 FY2024, while adjusted EBITDA decreased to $11.0 million from $15.9 million. The segment’s margin contracted to 11.8% from 13.9%, primarily due to lower engineered product sales, partially offset by cost-reduction initiatives.

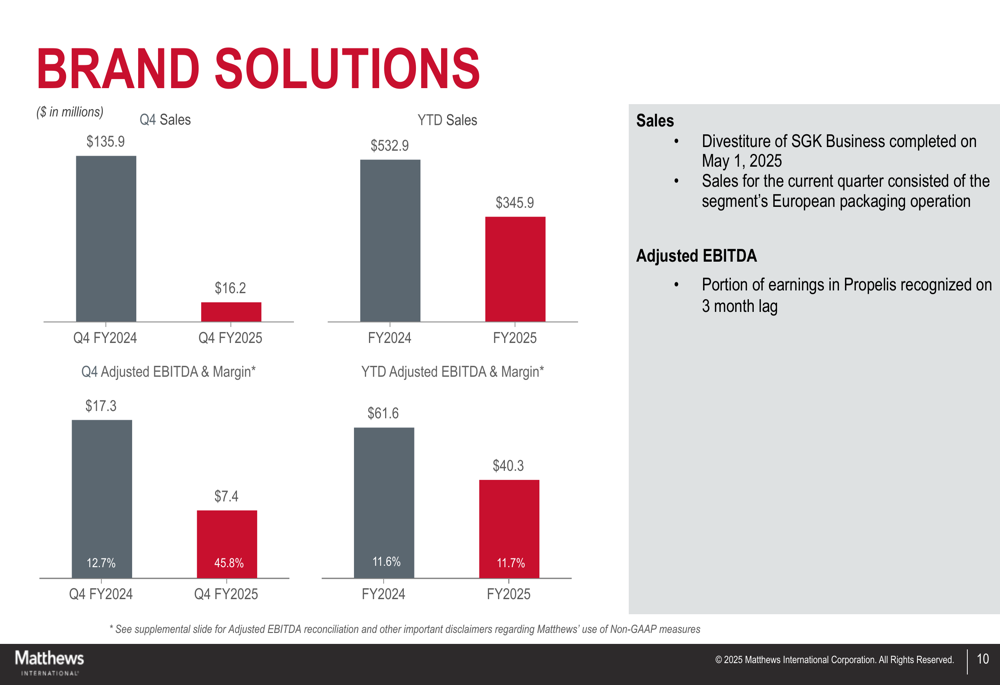

The Brand Solutions segment was dramatically reshaped by the divestiture of the SGK Business:

Following the May 1, 2025 divestiture of the SGK Business, Brand Solutions sales dropped to $16.2 million in Q4 FY2025 from $135.9 million in the prior-year period. Despite the revenue decline, adjusted EBITDA margin significantly improved to 45.8% from 12.7%, reflecting the company’s retention of a 40% stake in Propelis.

Financial Position

Matthews International made progress on debt reduction and capital allocation in fiscal 2025, though operating cash flow declined year-over-year.

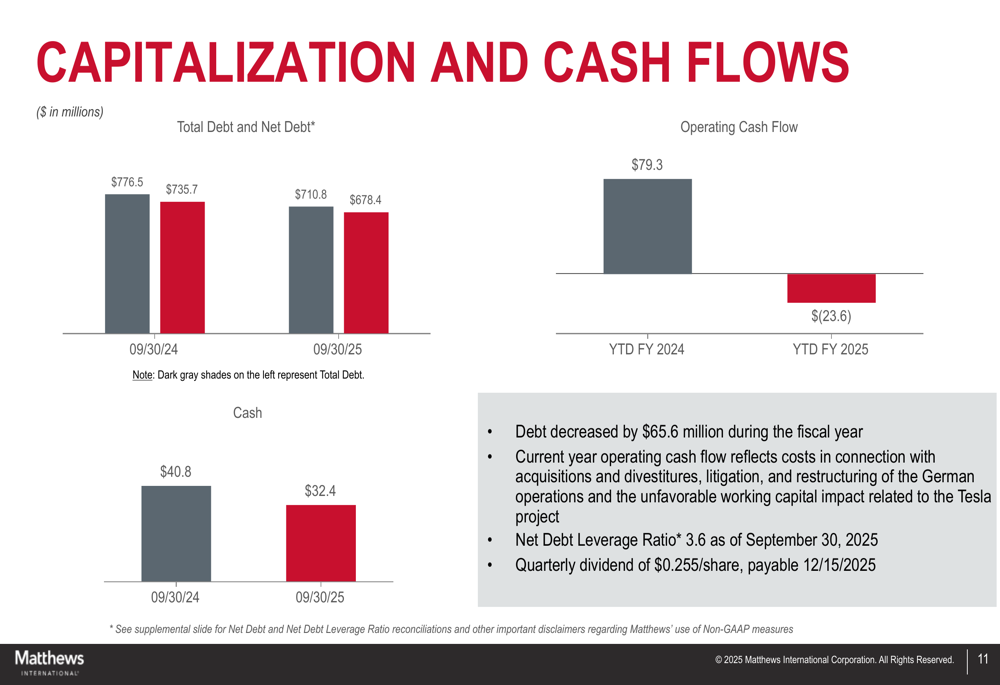

The following chart illustrates the company’s capitalization and cash flow position:

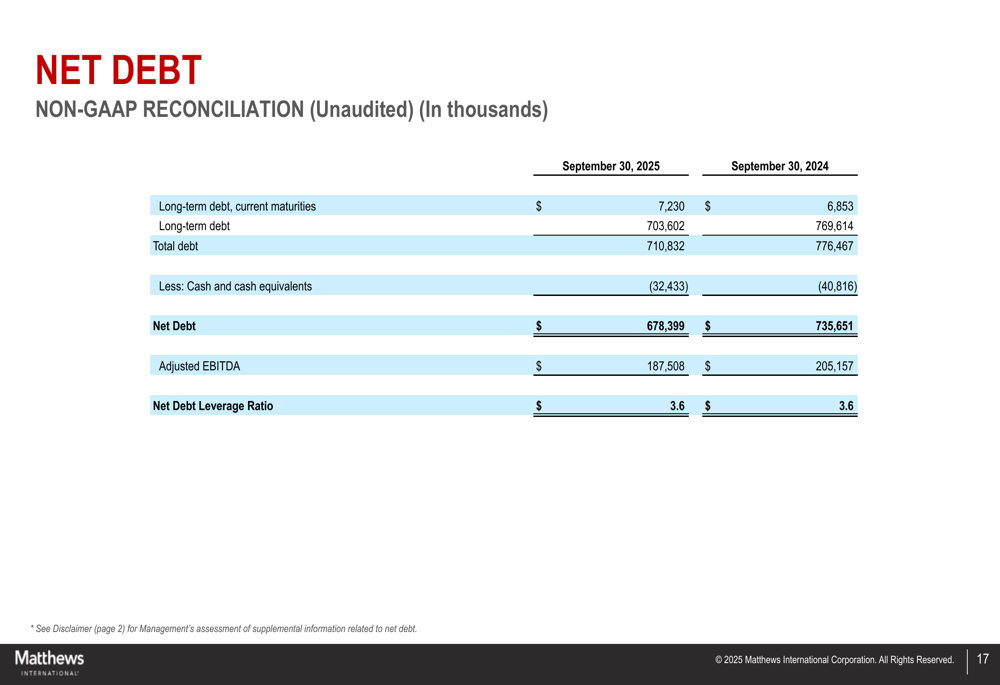

Total debt decreased by $65.6 million during the fiscal year to $710.8 million, while net debt fell to $678.4 million from $735.7 million. The company’s net debt leverage ratio remained unchanged at 3.6x, though management projects this will fall below 3.0x in the coming year as a result of divestiture proceeds.

Operating cash flow turned negative at ($23.6) million for FY2025, compared to a positive $79.3 million in FY2024. Despite this, Matthews maintained its commitment to shareholder returns, approving its 32nd consecutive annual dividend increase with a quarterly dividend of $0.255 per share, payable December 15, 2025.

The detailed reconciliation of net debt provides additional insight into the company’s financial position:

Outlook and Guidance

Looking ahead to fiscal 2026, Matthews International provided a cautiously optimistic outlook while acknowledging ongoing challenges in certain segments.

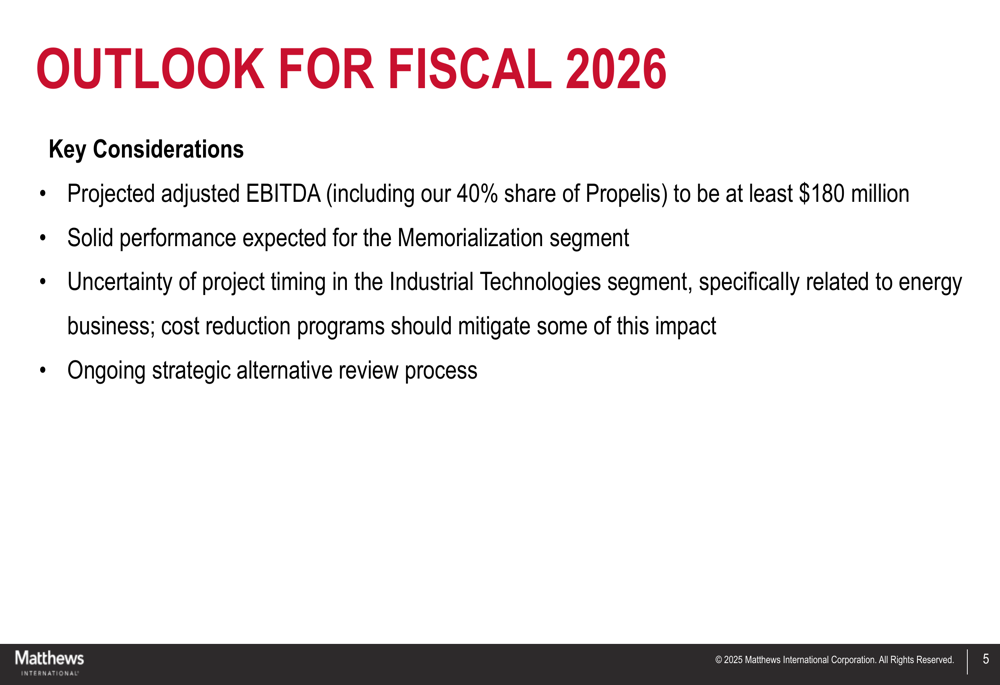

As outlined in the company’s forward-looking projections:

Management expects adjusted EBITDA (including the 40% share of Propelis) to be at least $180 million in fiscal 2026. The Memorialization segment is anticipated to deliver solid performance, while the Industrial Technologies segment faces uncertainty related to project timing in the energy business.

The company continues to pursue its strategic alternative review process, which could result in additional portfolio changes. Matthews also aims to further reduce its leverage ratio, targeting a level below 3.0x in the near term.

Conclusion

Matthews International’s Q4 and fiscal 2025 results reflect a company in transition, strategically reshaping its portfolio while working to improve profitability and reduce debt. The divestiture of non-core businesses has resulted in lower overall revenue but improved margins and a more focused operation.

The company’s strong performance in the Memorialization segment and strategic positioning in energy storage technology provide potential growth avenues, though challenges remain in the Industrial Technologies segment. With a projected adjusted EBITDA of at least $180 million for fiscal 2026 and ongoing strategic initiatives, Matthews appears focused on creating a more streamlined and profitable business model.

Investors will likely monitor the company’s progress in reducing its leverage ratio, the performance of its retained stake in Propelis, and the development of its energy storage technology as key indicators of future success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.