Gold prices edge lower; heading for weekly losses ahead of U.S.-Russia talks

MediaAlpha Inc (NYSE:MAX) released its Q2 2025 investor presentation on August 6, 2025, highlighting significant growth across key financial metrics. The company’s stock closed at $10.14, up 2.07% on the day, reflecting positive investor sentiment about the online insurance marketplace’s performance and outlook.

Introduction & Market Context

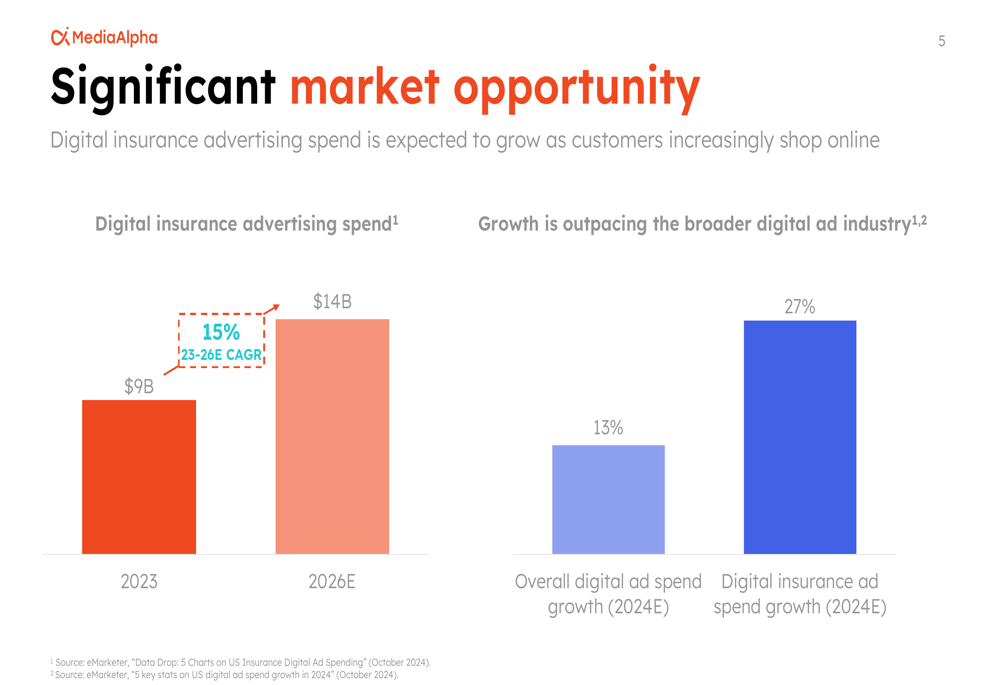

MediaAlpha positions itself as one of the largest online customer acquisition platforms for insurance, operating a proprietary two-sided marketplace that connects insurance carriers with online shoppers. The company benefits from a growing digital insurance advertising market, which is expected to reach $14 billion by 2026, representing a 15% CAGR from 2023 to 2026.

As shown in the following chart of digital insurance advertising growth, the sector is outpacing the broader digital advertising industry, with insurance ad spend projected to grow 27% in 2024 compared to 13% for overall digital ad spend:

This growth is supported by improving conditions in the property and casualty (P&C) insurance industry, with U.S. private auto combined ratios improving from a peak of 112% in 2022 to a projected 98% in 2024, indicating a return to profitability for carriers and potentially increased marketing spend.

Quarterly Performance Highlights

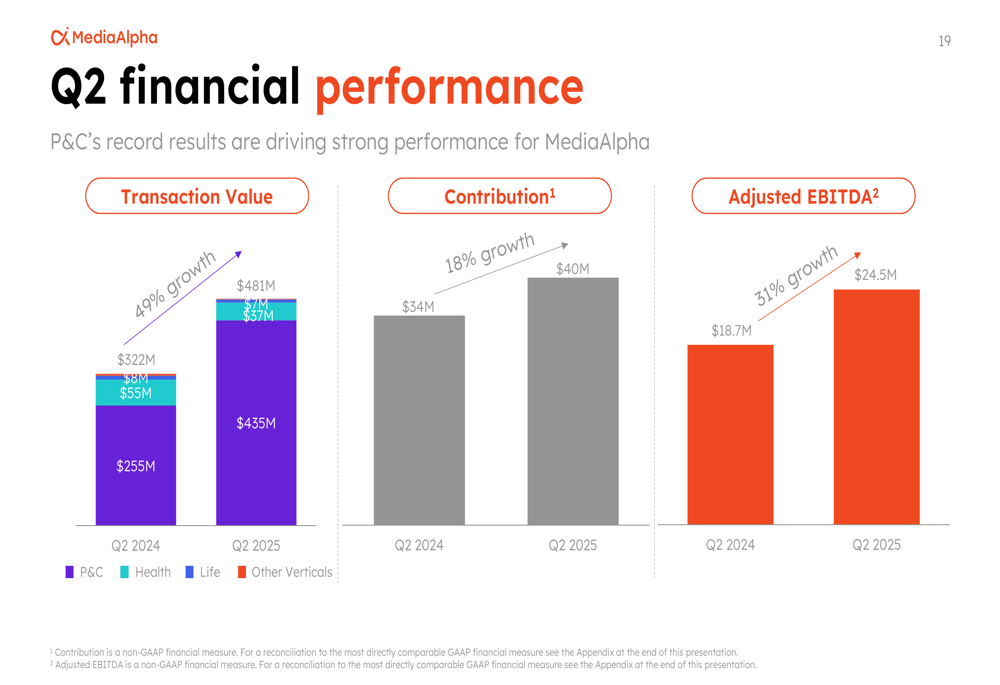

MediaAlpha delivered strong financial results in Q2 2025, with transaction value increasing 49% year-over-year, contribution growing 18%, and adjusted EBITDA rising 31% compared to Q2 2024.

The following chart breaks down the company’s Q2 financial performance across key metrics:

This quarterly performance continues a trend of substantial growth for the company. Over the last twelve months ending Q2 2025, MediaAlpha generated $1.9 billion in transaction value and $116.8 million in adjusted EBITDA, representing 136% year-over-year growth in adjusted EBITDA.

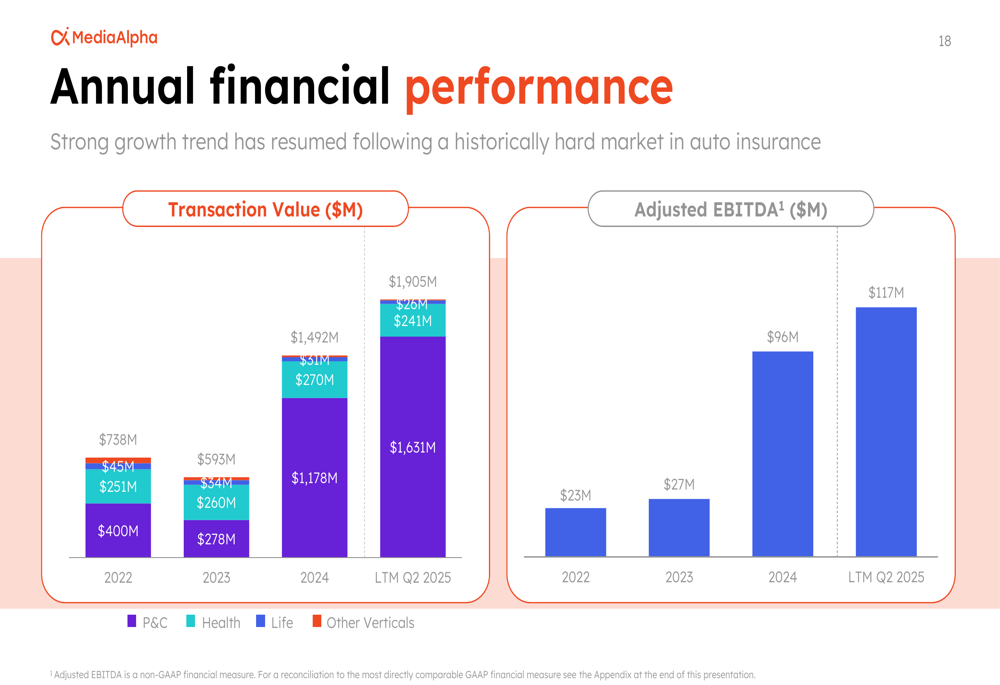

Looking at the company’s annual financial performance, both transaction value and adjusted EBITDA have shown consistent growth since 2022:

This performance aligns with the company’s Q1 2025 results, which showed a 116% year-over-year increase in transaction value to $473 million, with particularly strong growth in the P&C segment offsetting a 17% decline in health transaction value.

Business Model and Competitive Position

MediaAlpha’s business model centers on connecting insurance demand partners (carriers, brokers, and agents) with high-intent consumers through various supply partners (comparison sites, lead generators, and financial apps). The company has built a substantial network with over 400 supply partners and 700 demand partners.

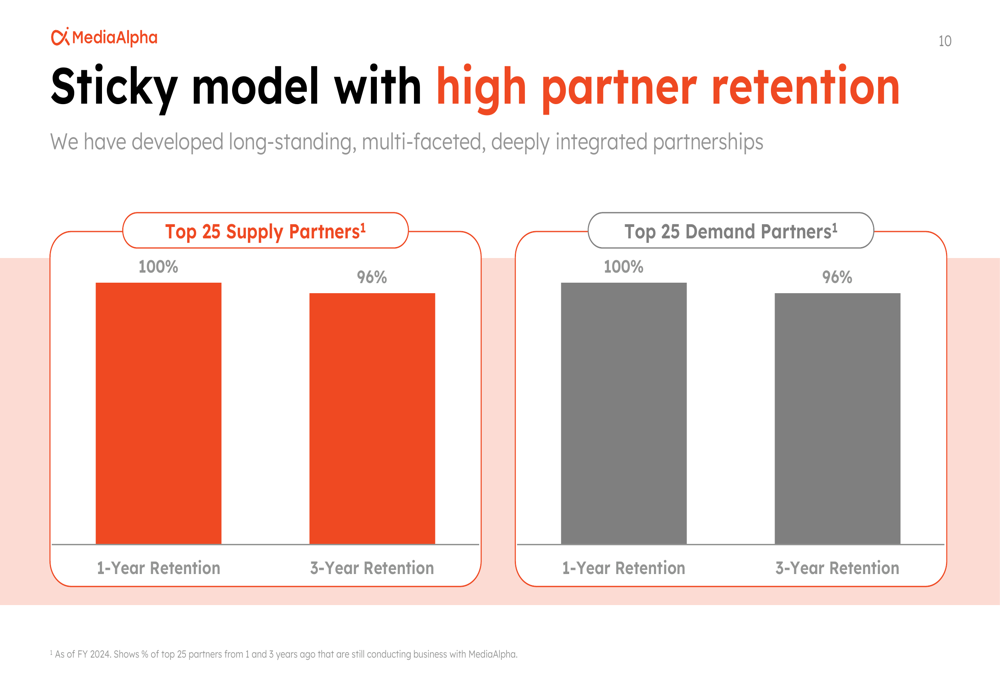

A key strength of MediaAlpha’s business model is its high partner retention rates, with both top supply and demand partners showing 100% one-year retention and 96% three-year retention:

The company generates revenue based on a percentage of transaction value, which is measured by partner spend and is not dependent on whether an insurance product is ultimately sold to a consumer. This model creates a virtuous cycle where more data leads to improved engagement, higher volumes, better yields, and ultimately more partners joining the platform.

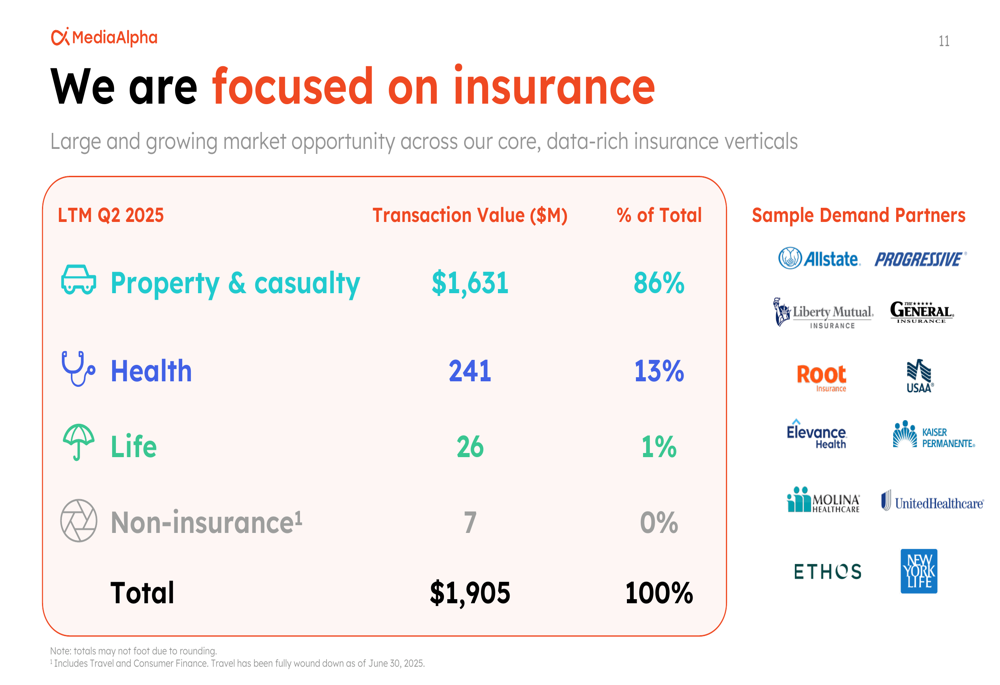

MediaAlpha’s business is heavily focused on the insurance market, with 86% of transaction value coming from property and casualty insurance, 13% from health insurance, and 1% from life insurance:

Growth Drivers and Market Opportunity (SO:FTCE11B)

MediaAlpha identifies several growth drivers for its business, including capitalizing on secular tailwinds in digital insurance advertising, extending market leadership through network effects, gaining wallet share with existing demand partners, bringing on new supply partners, and deepening data sharing with partners.

The company’s platform enables precise targeting and granular bidding based on numerous consumer attributes, allowing insurance carriers to automate and optimize their customer acquisition efforts. This capability is particularly valuable in the current insurance market environment, where carriers are increasingly focused on profitable growth.

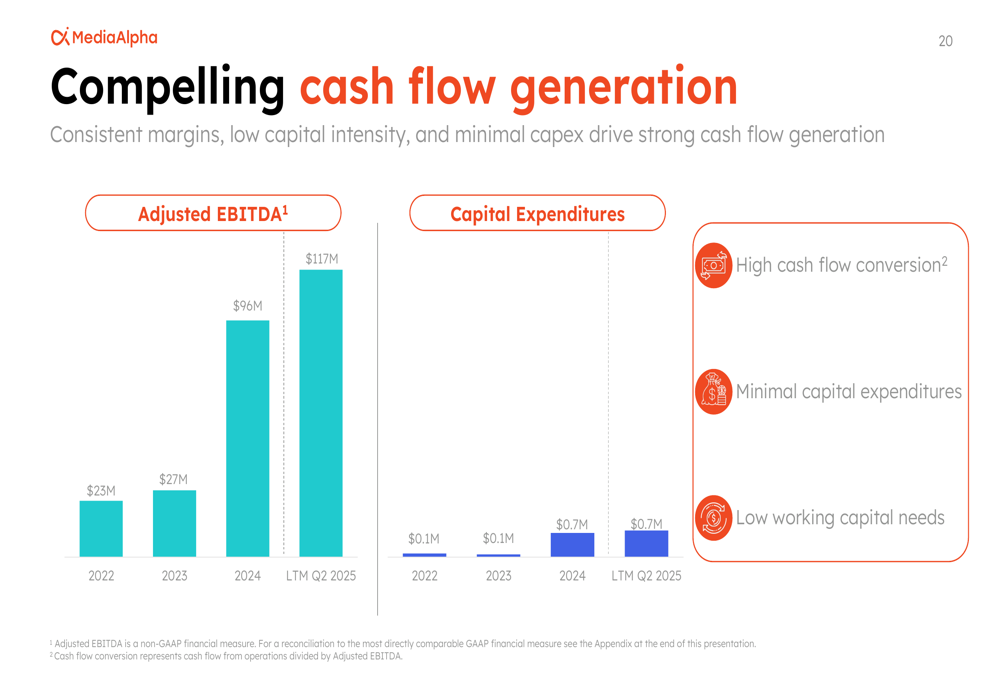

MediaAlpha also highlights its efficient operating model and strong cash flow generation with low capital intensity:

Forward-Looking Statements

Looking ahead, MediaAlpha is well-positioned to benefit from continued growth in digital insurance advertising, particularly in the P&C segment where market conditions are improving. The company also sees opportunity in the expanding Medicare Advantage market, which is projected to grow from 15 million enrollees in 2014 to 41 million by 2029, representing a 7% CAGR.

For Q2, MediaAlpha had forecasted transaction value between $470 million and $495 million, representing a 50% year-over-year increase at the midpoint. Based on the presentation, the company appears to have delivered results within this guidance range.

The company’s overall financial profile suggests continued strong performance, with MediaAlpha highlighting its "two-sided marketplace model with powerful network effects," "strong long-term growth potential benefitting from secular tailwinds," "efficient, highly profitable operating model," and "steady cash flow generation with low capital intensity" as key attributes of its business.

While the presentation focuses primarily on positive trends, investors should note that the company’s Q1 earnings call mentioned some challenges, including regulatory issues related to FTC matters and potential impacts from automotive tariffs expected in the second half of 2025. Additionally, the health insurance segment showed weakness in Q1, though this appears to be offset by strength in the larger P&C segment.

With a stock price of $10.14, MediaAlpha trades well below its 52-week high of $20.91, potentially indicating room for upside if the company continues to deliver strong financial results and execute on its growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.