German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Metallus Inc (NYSE:MTUS), a specialty metals manufacturer formerly known as TimkenSteel, presented its Q2 2025 investor slides highlighting sequential improvement in financial performance while maintaining a cautious outlook for the coming quarter. The company, which produces high-quality specialty metals primarily from recycled scrap metal, reported modest gains amid challenging market conditions.

The presentation comes after Metallus reported disappointing Q1 2025 results in May, when the company missed EPS forecasts despite beating revenue expectations. The stock has struggled to regain momentum since then, trading at $15.08 as of August 7, 2025, well below its 52-week high of $18.72 but above its 52-week low of $10.78.

Established as a standalone public company in 2014 and renamed Metallus in February 2024, the company serves diverse end markets including automotive, industrial, aerospace & defense, and energy sectors. With annual melt capacity of approximately 1.2 million tons and ship capacity of about 0.9 million tons, Metallus positions itself as a key domestic producer of specialty steel products.

Quarterly Performance Highlights

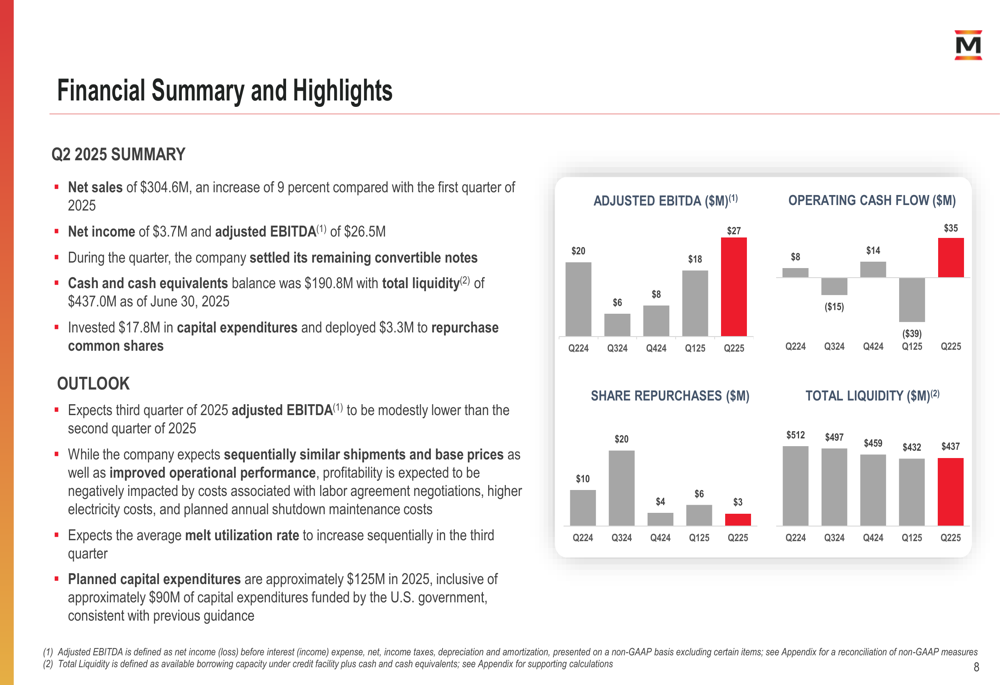

Metallus reported net sales of $304.6 million for Q2 2025, representing a 9% increase from Q1 2025. The company achieved net income of $3.7 million and adjusted EBITDA of $26.5 million, showing sequential improvement from the previous quarter when it reported EPS of $0.07 and adjusted EBITDA of $17.7 million.

As shown in the following chart of quarterly financial metrics, the company has demonstrated improving adjusted EBITDA and operating cash flow trends in recent quarters:

The company’s cash position strengthened to $190.8 million as of June 30, 2025, up from $180.3 million reported at the end of Q1. Total (EPA:TTEF) liquidity stood at $437.0 million, providing substantial financial flexibility. During the quarter, Metallus invested $17.8 million in capital expenditures and allocated $3.3 million to share repurchases.

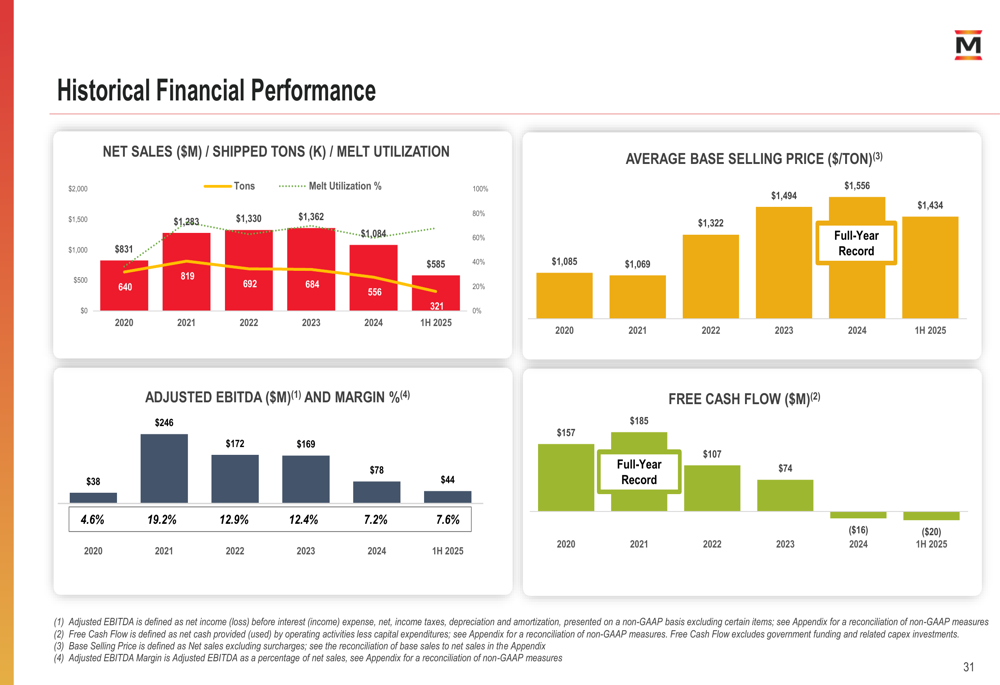

Looking at historical performance, Metallus has experienced significant volatility in financial results over recent years, with adjusted EBITDA ranging from $38 million in 2020 to a peak of $246 million in 2021, before moderating to $78 million in 2024:

Strategic Initiatives

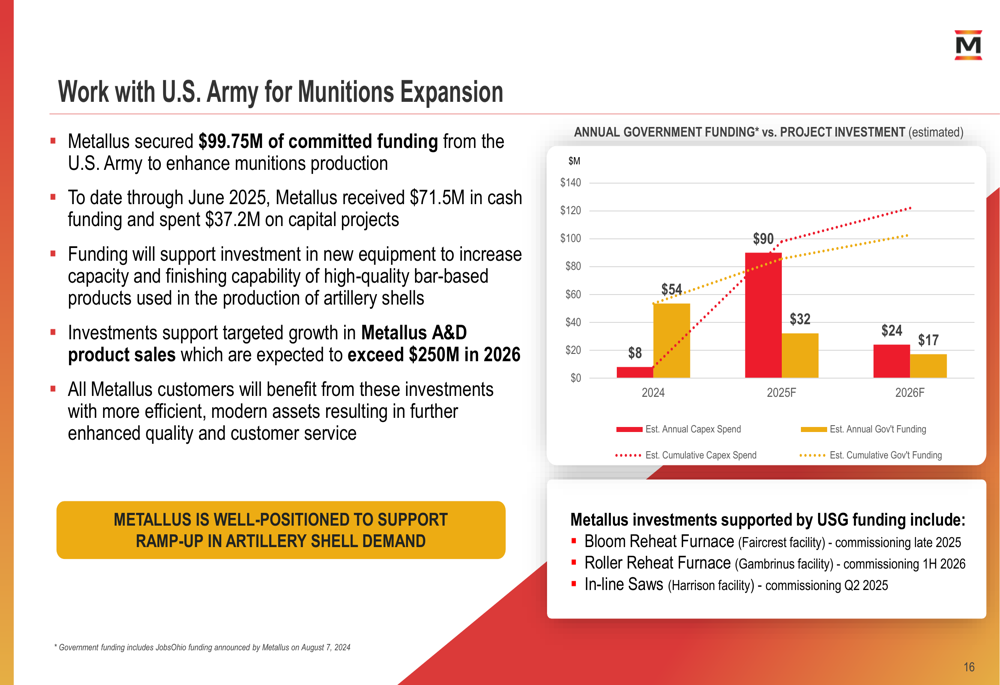

A cornerstone of Metallus’ growth strategy is its expanding presence in the aerospace and defense sector. The company has secured $99.75 million in committed funding from the U.S. Army to enhance munitions production capabilities, with $71.5 million received in cash funding through June 2025. This strategic partnership is expected to drive significant growth, with the company projecting A&D product sales to exceed $250 million in 2026, more than doubling the 2023 level.

The following chart illustrates the funding timeline and investment plans for the U.S. Army partnership:

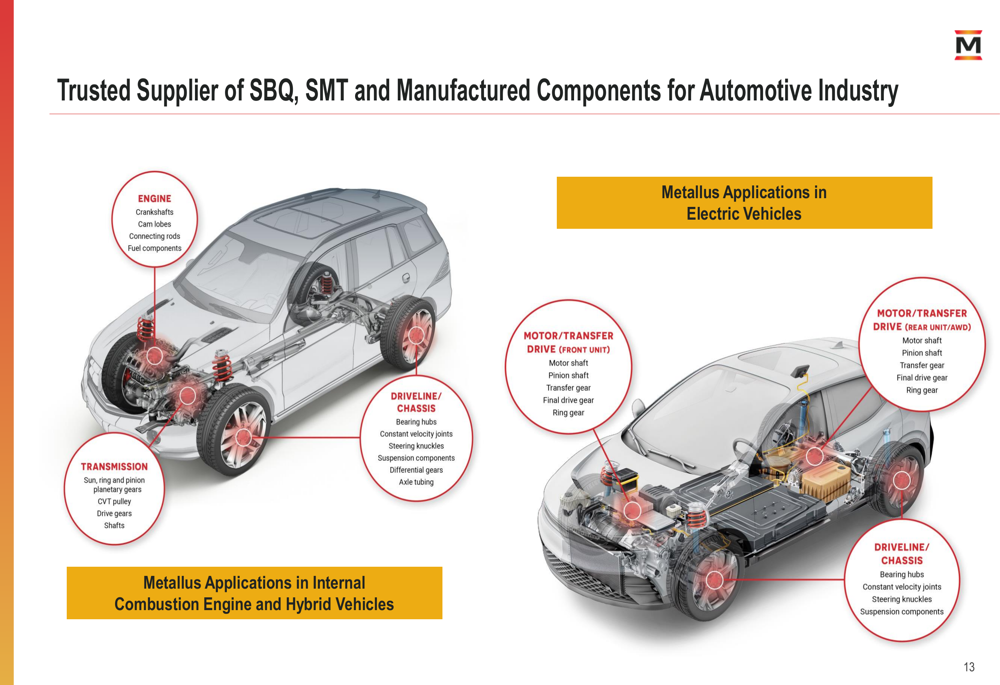

Metallus is also positioning itself to capitalize on the automotive industry’s transition to electric and hybrid vehicles. The company has secured long-term manufactured component agreements for its growing EV and hybrid portfolio, which currently consists of approximately 20 awarded component parts.

The company’s product applications span both traditional internal combustion engines and electric vehicles, as illustrated in this comprehensive overview:

Detailed Financial Analysis

Metallus serves a diverse range of end markets, with automotive representing 42% of net sales in 2024, followed by industrial at 40%, aerospace & defense at 12%, and energy at 8%. This diversification helps buffer against sector-specific downturns, though the company remains significantly exposed to automotive industry cycles.

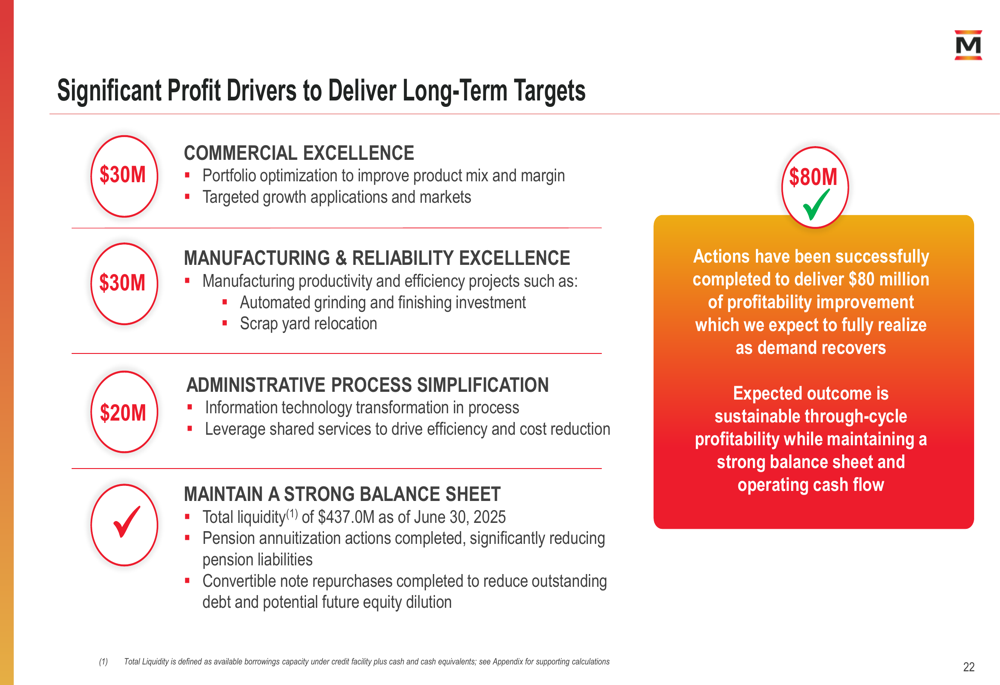

The company has outlined specific profit drivers to achieve its long-term financial targets, focusing on three key areas: Commercial Excellence ($30 million), Manufacturing & Reliability Excellence ($30 million), and Administrative Process Simplification ($20 million). These initiatives are designed to deliver $80 million in profitability improvements as demand recovers.

As shown in the following breakdown of profit drivers:

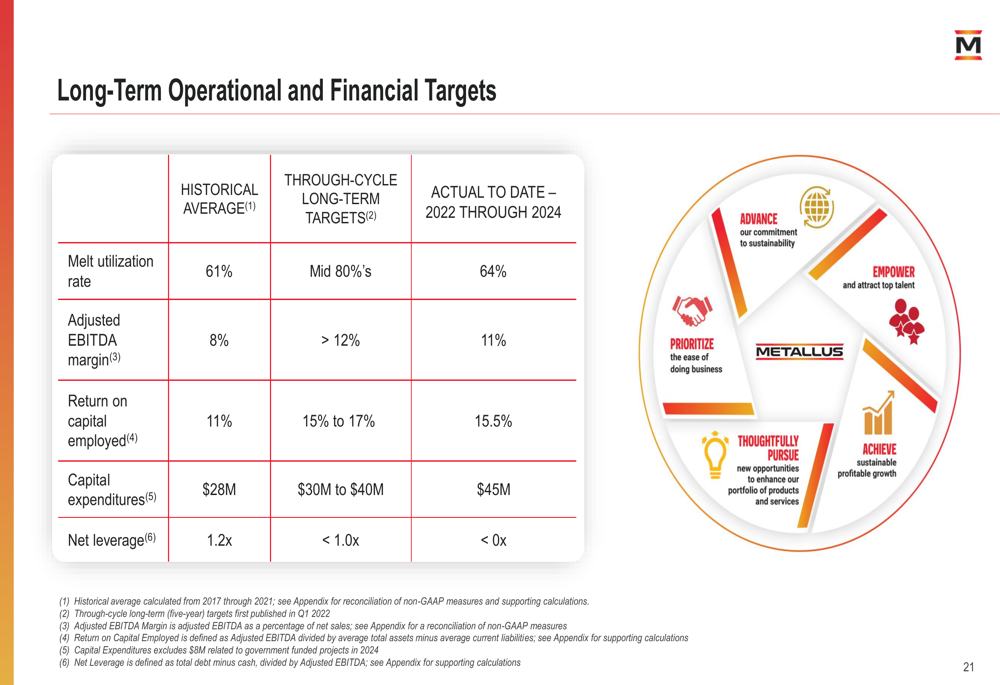

Metallus has established ambitious long-term operational and financial targets, including increasing its melt utilization rate from a historical average of 61% to the mid-80% range, improving adjusted EBITDA margin from 8% historically to above 12%, and maintaining return on capital employed between 15-17%:

Forward-Looking Statements

Despite the sequential improvement in Q2, Metallus provided a cautious outlook for Q3 2025, expecting adjusted EBITDA to be "modestly lower" than Q2 due to increased labor and electricity costs and planned shutdown maintenance. The company anticipates similar shipments and base prices in Q3 compared to Q2, with the melt utilization rate increasing.

For full-year 2025, Metallus plans capital expenditures of $125 million, including $90 million funded by the U.S. government. This significant investment underscores the company’s strategic focus on expanding its defense sector capabilities.

The company’s long-term strategy centers on delivering sustainable through-cycle profitability, growing A&D product sales to over $250 million by 2026, employing a balanced capital allocation approach, and progressing toward its 2030 environmental goals. These environmental targets include a 40% reduction in greenhouse gas emissions, 30% reduction in energy consumption, 35% reduction in fresh water withdrawn, and 10% reduction in waste-to-landfill intensity from a 2018 baseline.

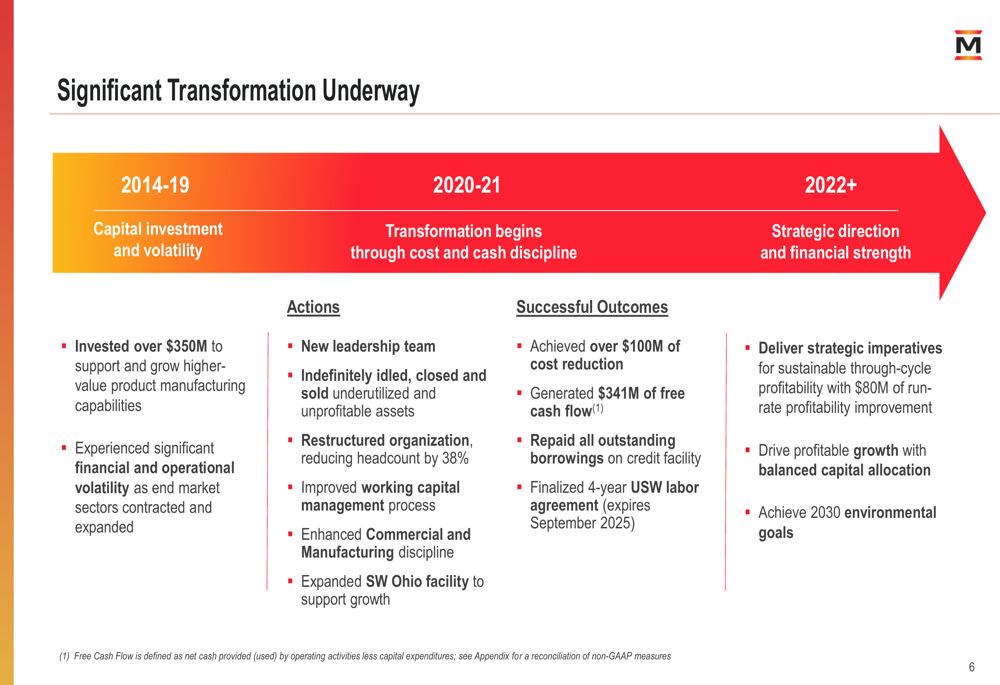

Metallus’ transformation journey, which began in 2020 with new leadership and significant cost-cutting measures, continues to evolve as the company positions itself for sustainable growth in demanding end markets:

While Metallus faces challenges including increased labor and energy costs, the company’s strong balance sheet with no outstanding borrowings and substantial liquidity provides a solid foundation for navigating market uncertainties while pursuing strategic growth initiatives, particularly in the promising aerospace and defense sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.