CVS Group shares surge over 10% after FY25 EBITDA beats estimates

Introduction & Market Context

Micron Technology (NASDAQ:MU) presented its fiscal fourth quarter 2025 results on September 23, 2025, showcasing record revenue and strong financial performance driven primarily by AI-related demand. The memory and storage solutions provider reported significant growth across its business segments, with particular strength in its data center and High Bandwidth Memory (HBM) products.

The company’s shares closed at $164.62 on the day of the presentation, up 1.13% from the previous close. In aftermarket trading, the stock gained an additional 0.6%, reflecting positive investor sentiment following the strong results and optimistic guidance.

Quarterly Performance Highlights

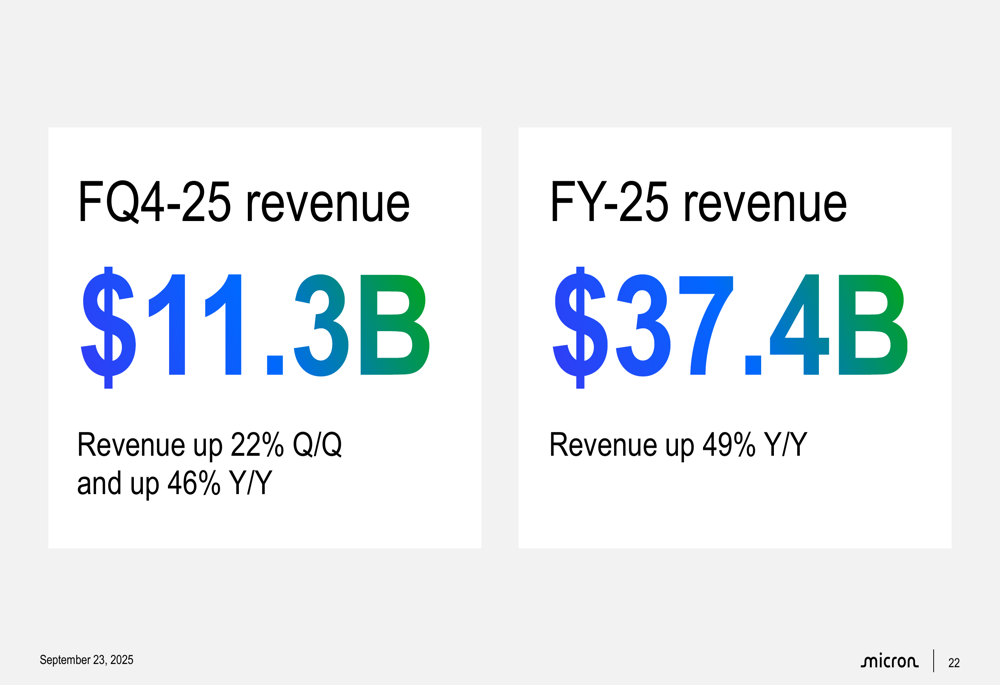

Micron delivered exceptional financial results for its fiscal fourth quarter of 2025, with revenue reaching $11.3 billion, representing a 22% increase quarter-over-quarter and a 46% jump year-over-year.

As shown in the following revenue breakdown:

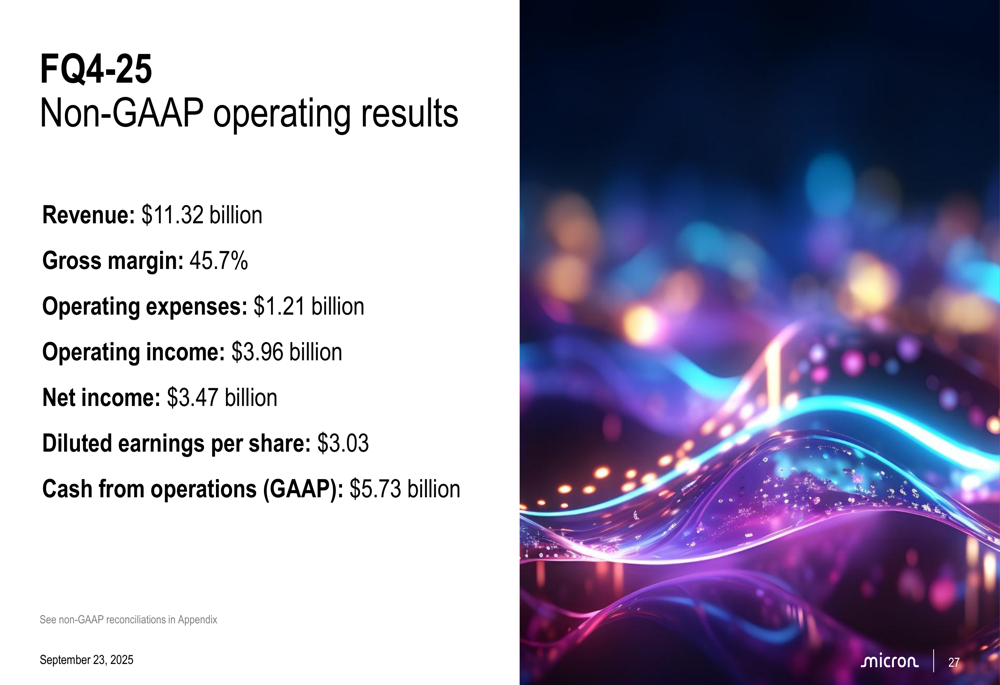

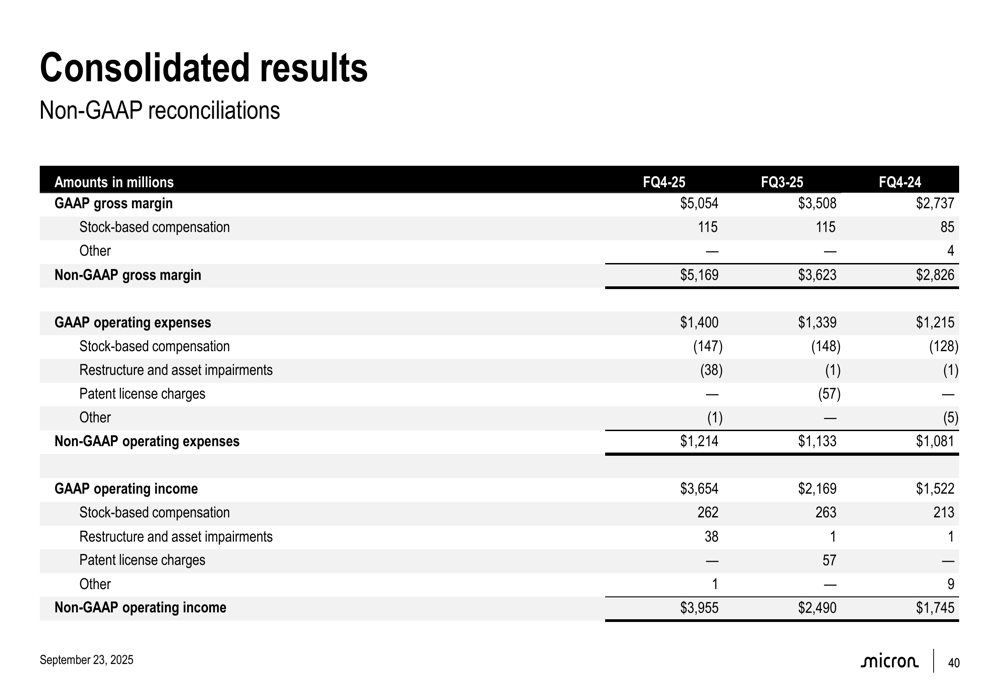

For the full fiscal year 2025, Micron achieved record revenue of $37.4 billion, up 49% compared to fiscal year 2024. The company’s non-GAAP operating results for FQ4-25 were equally impressive, with gross margin reaching 45.7%, operating income of $3.96 billion, and diluted earnings per share of $3.03.

The following chart illustrates Micron’s key non-GAAP operating metrics for the quarter:

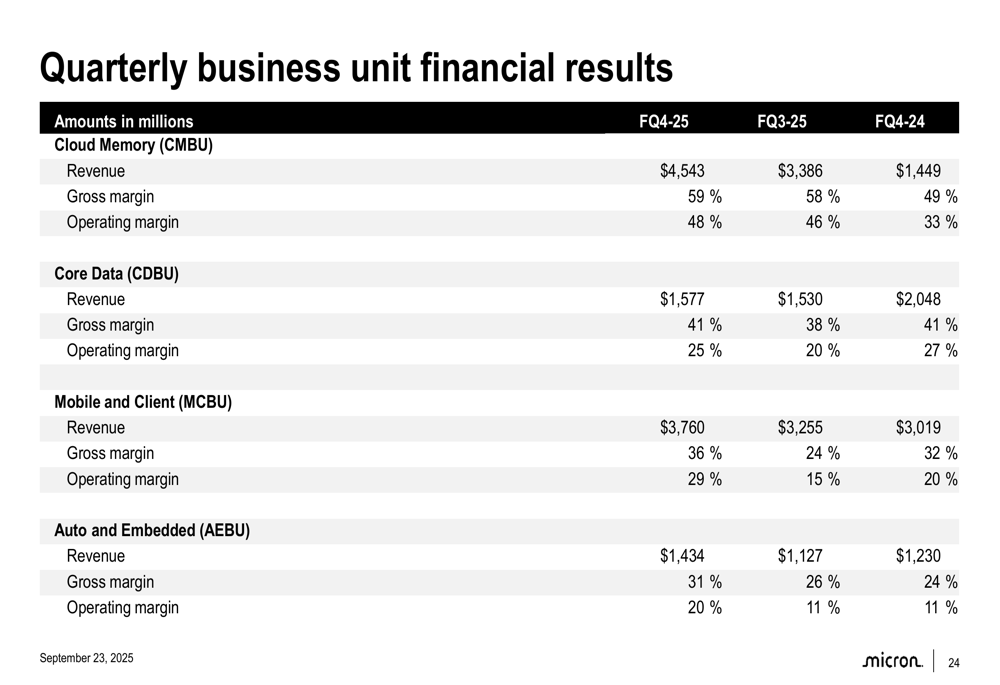

Micron’s performance was particularly strong in its Cloud Memory Business Unit (CMBU), which generated $4.5 billion in revenue (40% of total company revenue) with gross margins of 59%. This represented a 34% sequential increase, driven by robust bit shipment growth and record HBM revenues.

The company’s quarterly business unit results demonstrate the strength across its portfolio, with significant improvements in both revenue and profitability:

Detailed Financial Analysis

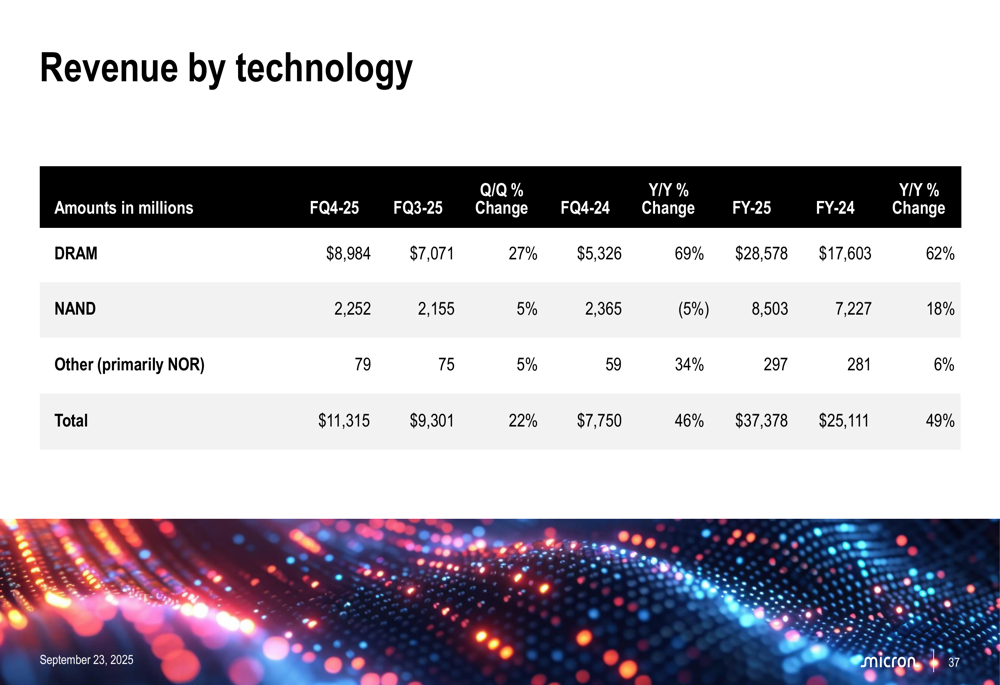

Breaking down Micron’s revenue by technology segments reveals the growing dominance of DRAM in the company’s portfolio. DRAM revenue reached $9.0 billion in FQ4-25, accounting for 79% of total revenue, and increased 27% quarter-over-quarter. NAND revenue was $2.3 billion (20% of total), up 5% quarter-over-quarter.

The following table provides a detailed breakdown of revenue by technology:

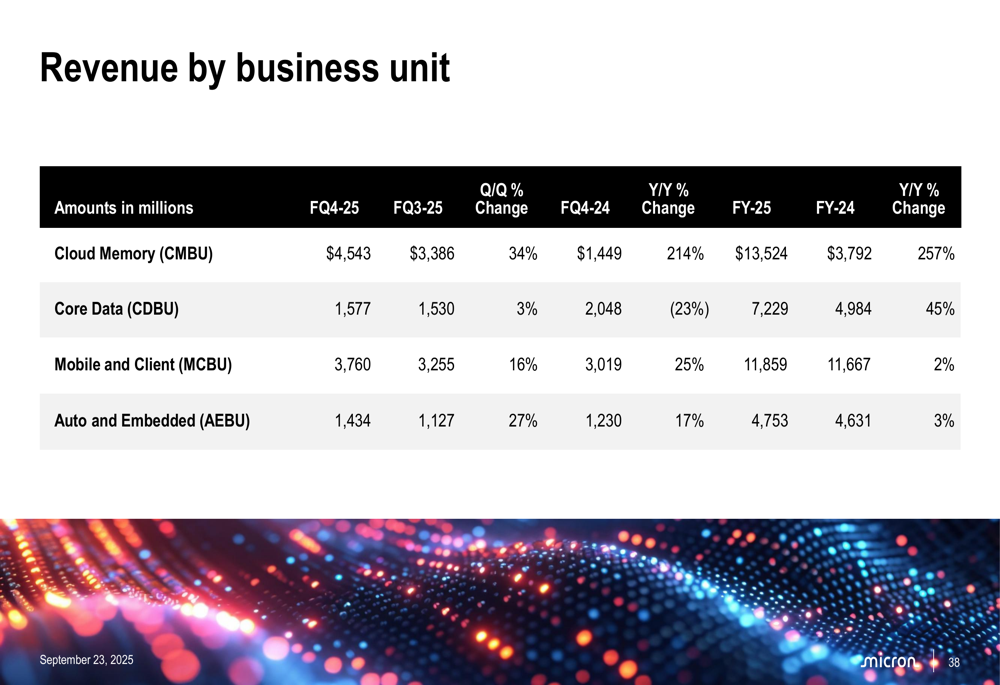

From a business unit perspective, Micron’s revenue distribution highlights the growing importance of its data center-focused segments. The Cloud Memory Business Unit led with $4.5 billion in revenue, followed by the Mobile and Client Business Unit at $3.8 billion, Core Data Business Unit at $1.6 billion, and Automotive and Embedded Business Unit at $1.4 billion.

The revenue breakdown by business unit shows strong sequential growth across all segments:

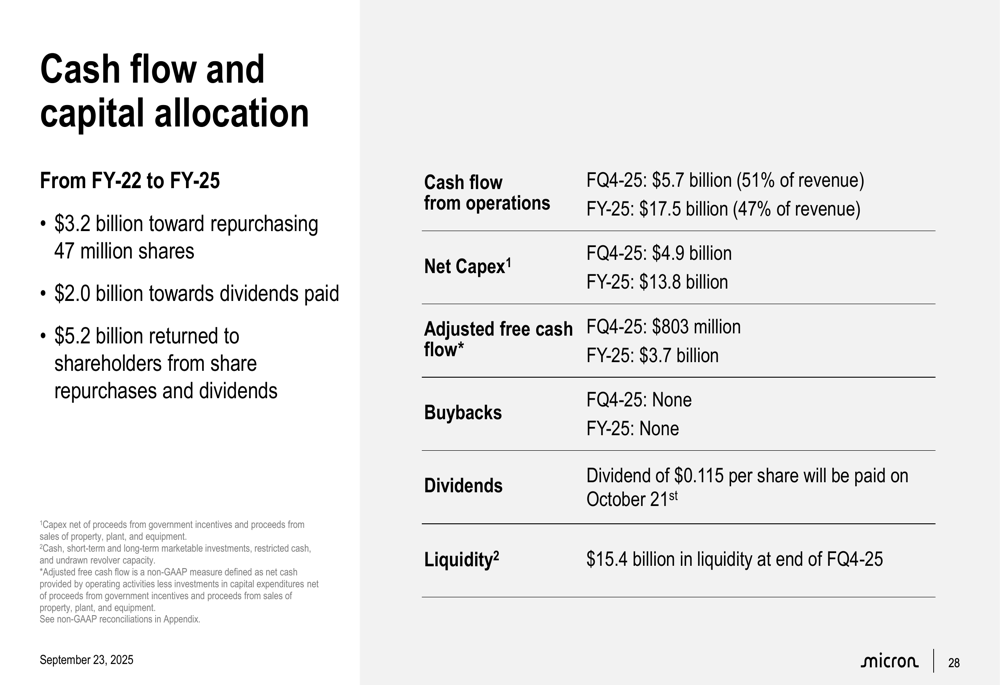

Cash flow generation was equally impressive, with cash flow from operations reaching $5.7 billion in FQ4-25 (51% of revenue) and $17.5 billion for the full fiscal year 2025 (47% of revenue). After accounting for capital expenditures of $4.9 billion in the quarter and $13.8 billion for the year, Micron generated adjusted free cash flow of $803 million and $3.7 billion, respectively.

The company’s cash flow and capital allocation strategy is outlined below:

Strategic Initiatives

Micron highlighted several strategic initiatives and technological advancements driving its strong performance. The company reported that its 1y DRAM node reached mature yields in record time, 50% faster than the prior generation, making Micron the first in the industry to ship 1y DRAM. This technological leadership is expected to provide significant competitive advantages across Micron’s DRAM portfolio.

In manufacturing, Micron received a CHIPS grant disbursement following the completion of a key construction milestone for its new high-volume manufacturing fab in Idaho (ID1), with the first wafer output expected to begin in the second half of calendar 2027. Design work has also begun for a second Idaho manufacturing fab (ID2), which will provide additional capacity beyond 2028.

The company’s HBM business has shown particularly strong growth, with HBM revenue growing to nearly $2 billion in FQ4-25, implying an annualized run rate of nearly $8 billion. This growth has been driven by the ramp of Micron’s industry-leading HBM3E products, with the company’s HBM share on track to grow again and be in line with its overall DRAM share.

Looking forward, Micron’s HBM4 development remains on track to support customer platform ramps, with the company recently shipping customer samples of HBM4 with industry-leading bandwidth exceeding 2.8 TBps and pin speeds over 11 Gbps. For HBM4E, Micron will offer both standard products and options for customization of the base logic die, partnering with TSMC for manufacturing.

Forward-Looking Statements

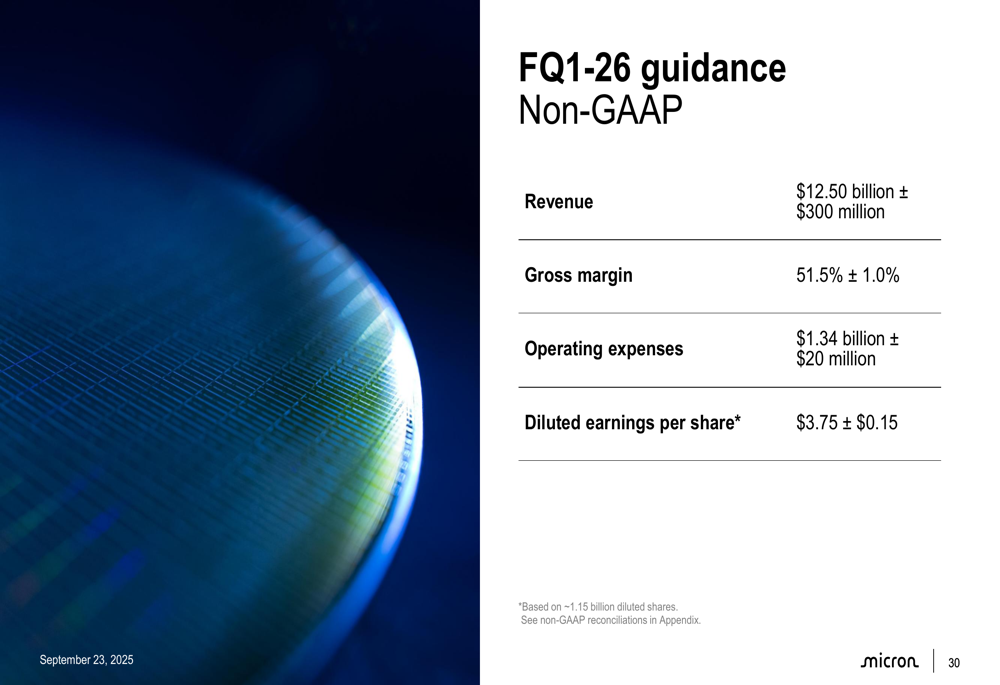

Micron provided an optimistic outlook for its fiscal first quarter of 2026, with guidance indicating continued strong performance. The company expects revenue of $12.5 billion (±$300 million), gross margin of 51.5% (±1.0%), and diluted earnings per share of $3.75 (±$0.15).

The following table details Micron’s FQ1-26 guidance:

The company’s market outlook suggests continued strong demand, particularly in the data center segment. Calendar 2025 industry DRAM bit demand growth is expected to be in the high-teens percentage range, while NAND bit demand growth is projected in the low-to-mid-teens percentage range. Micron anticipates further DRAM supply tightness and continued strengthening in NAND market conditions in calendar 2026.

In the data center, calendar 2025 total server units are expected to grow approximately 10%, with traditional server growth outlook strengthening significantly from flat to growth in the mid-single digit range. AI server growth continues to be robust, driving strong demand for DRAM products, particularly HBM.

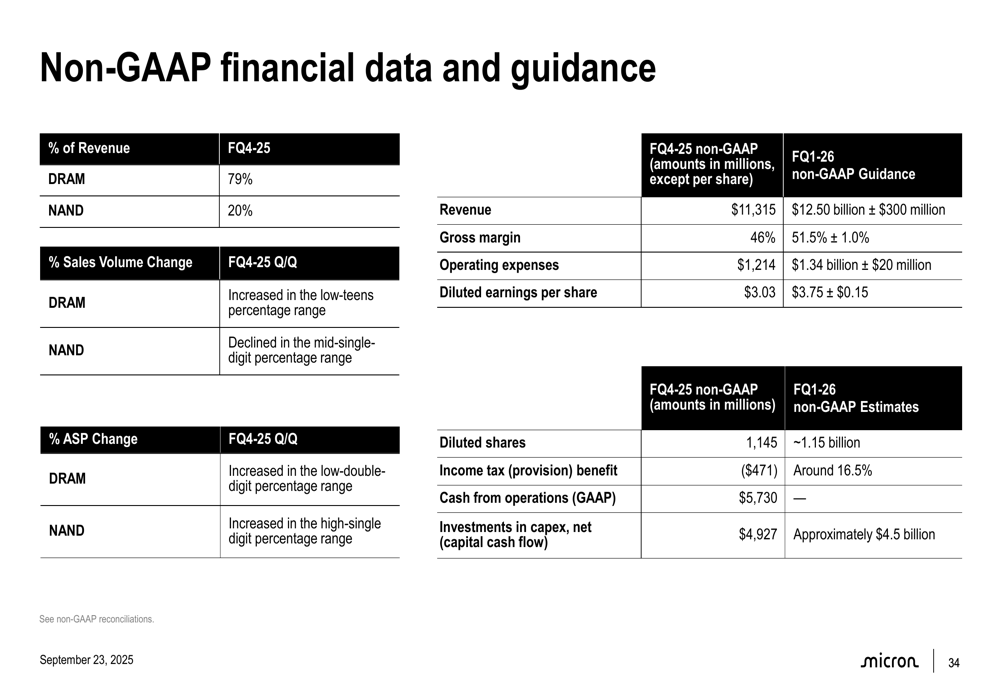

Micron’s comprehensive financial data and guidance provide a clear picture of the company’s expected trajectory:

The company’s consolidated results, reconciling GAAP to non-GAAP metrics, further underscore the strength of Micron’s financial position:

Overall, Micron’s FQ4 2025 presentation paints a picture of a company executing well in a favorable market environment, with AI-driven demand creating significant opportunities for growth in its high-value memory and storage products. The company’s strategic investments in advanced manufacturing capabilities and next-generation technologies position it well to capitalize on these trends in fiscal year 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.