Nscale secures deal for 200,000 NVIDIA GB300 GPUs with Microsoft

Introduction & Market Context

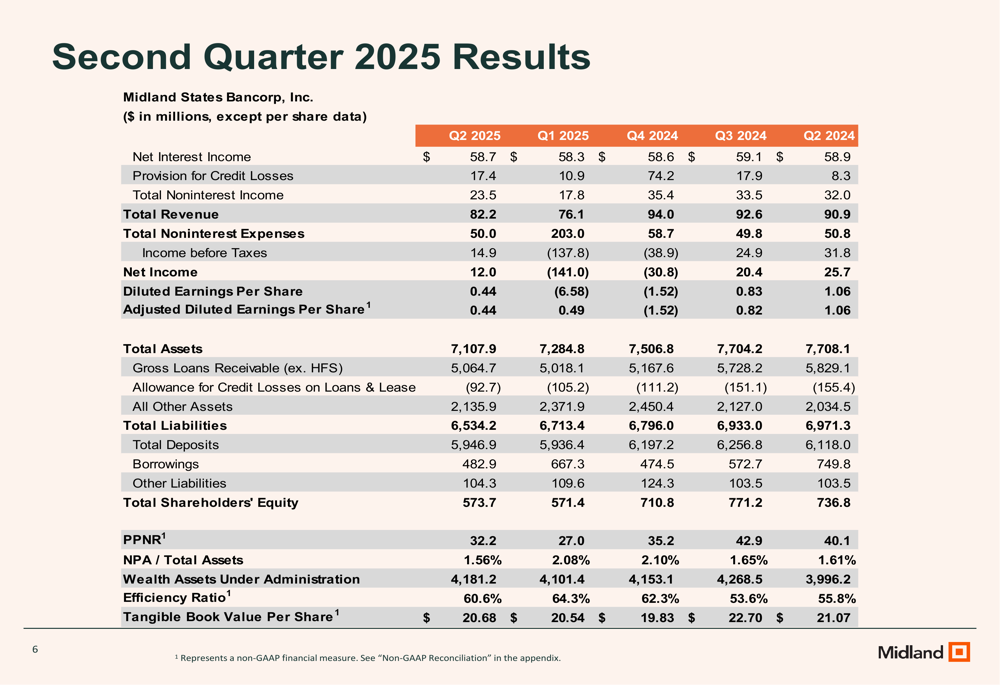

Midland States Bancorp, Inc. (NASDAQ:MSBI) presented its second quarter 2025 earnings on July 24, highlighting progress in credit remediation efforts and growth in its core community banking business. The Illinois and Missouri-based regional bank reported earnings per share of $0.44 amid an improving interest margin environment and strengthening capital ratios.

Despite the positive narrative in the presentation, MSBI stock has been under pressure, trading at $16.83 in after-hours on August 1, down 0.77% from the previous close. The stock remains significantly below its 52-week high of $28.08 and closer to its 52-week low of $14.79, suggesting investors may still harbor concerns about the bank’s overall trajectory.

Quarterly Performance Highlights

Midland States reported pre-provision net revenue (PPNR) of $32.2 million ($1.48 per share) for Q2 2025, representing a 19% increase from the previous quarter. The bank’s net interest margin expanded to 3.56%, up 7 basis points quarter-over-quarter, driven primarily by lower deposit costs.

As shown in the comprehensive financial results table below, the bank maintained total assets of $7.1 billion while improving several key metrics compared to previous quarters:

Net interest income reached $58.7 million, benefiting from a 10 basis point reduction in deposit costs quarter-over-quarter. Total (EPA:TTEF) noninterest income was $23.5 million, with a 7.3% increase excluding credit enhancement income. The efficiency ratio improved to 60.6%, reflecting the bank’s ongoing efforts to streamline operations.

Credit Quality Improvement

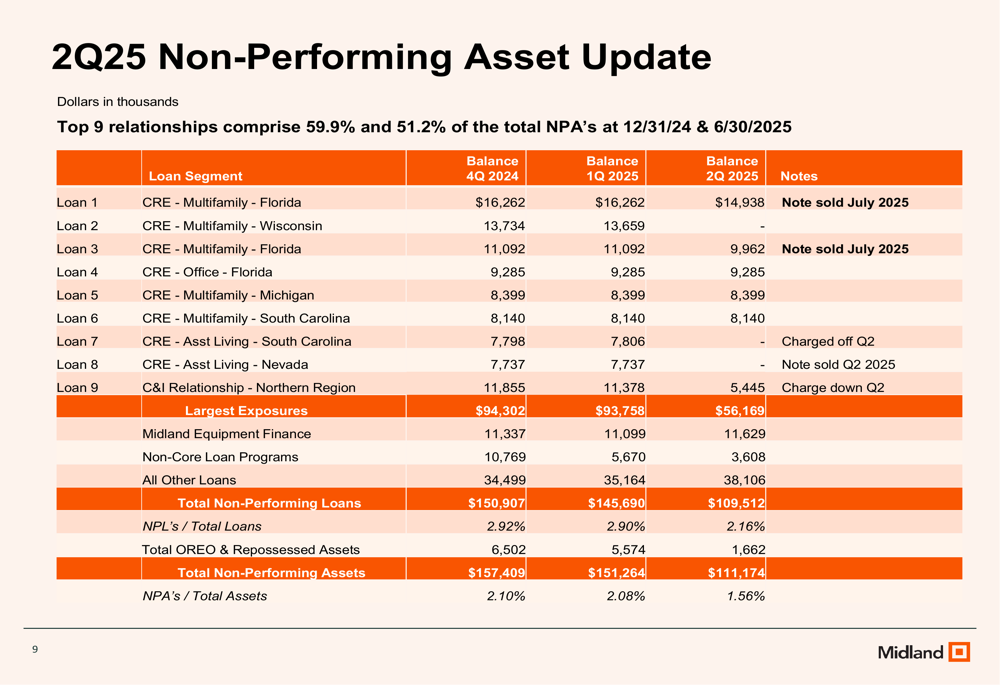

A central theme of Midland’s presentation was the accelerated credit remediation efforts, with $65 million of non-performing loans exited through July 2025. This strategic initiative has reduced the bank’s non-performing assets to total assets ratio to 1.56%, down 52 basis points from the previous quarter.

The bank provided a detailed breakdown of its non-performing asset resolution progress:

Midland has strategically exited non-core loan programs originated by FinTech partners LendingPoint and GreenSky, with the remaining Banking-as-a-Service portfolio at $54 million and retained GreenSky at $50 million. The Specialty Finance Group and Midland Equipment Finance segments, which had been sources of credit concerns, showed improvement with targeted management efforts.

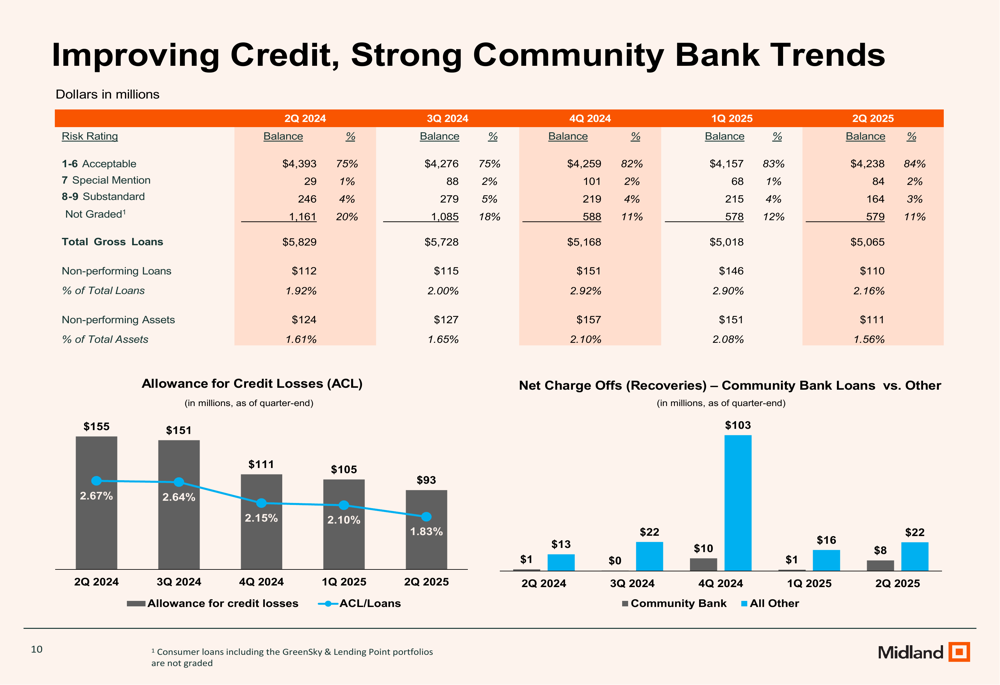

The bank’s credit quality trends demonstrate consistent improvement across risk ratings:

Core Business Growth

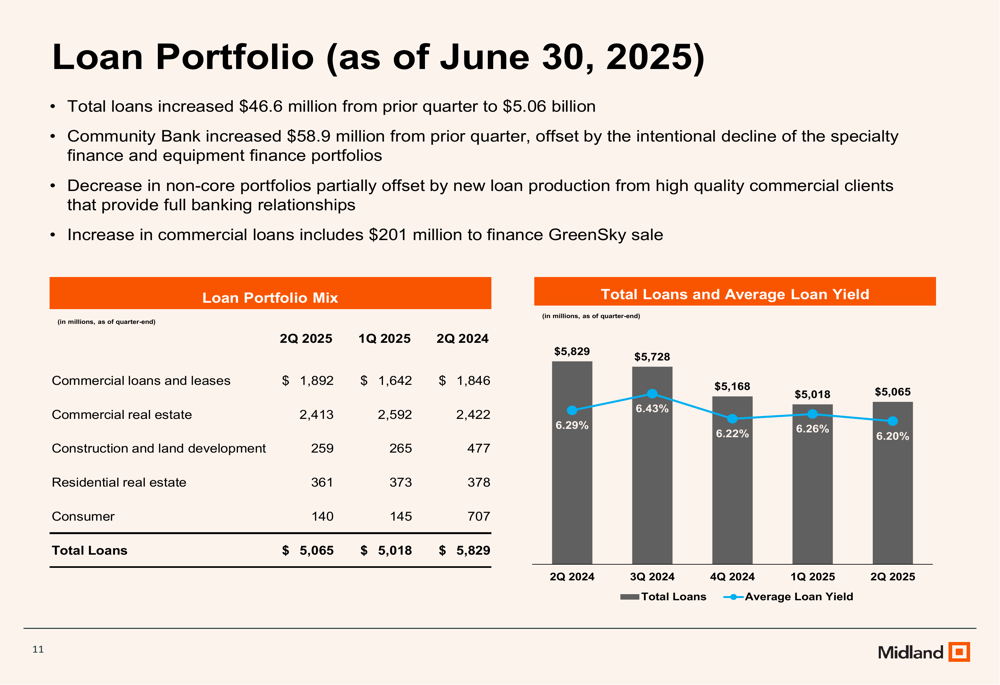

While addressing credit challenges, Midland States has maintained focus on growing its core community banking business. Loans increased by $46.6 million from the previous quarter to $5.06 billion, with community bank loans specifically growing by $58.9 million (1.8%).

The loan portfolio composition shows diversification across commercial, real estate, and consumer segments:

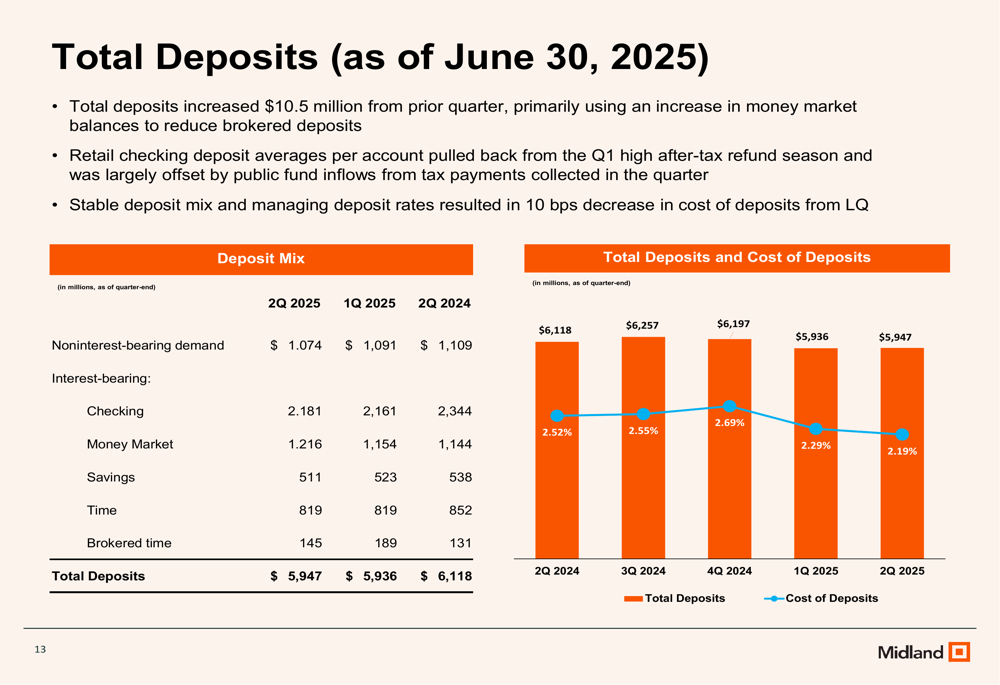

On the funding side, total deposits increased by $10.5 million to $5.95 billion, with stable deposit mix and improved cost management resulting in a 10 basis point decrease in deposit costs from the previous quarter:

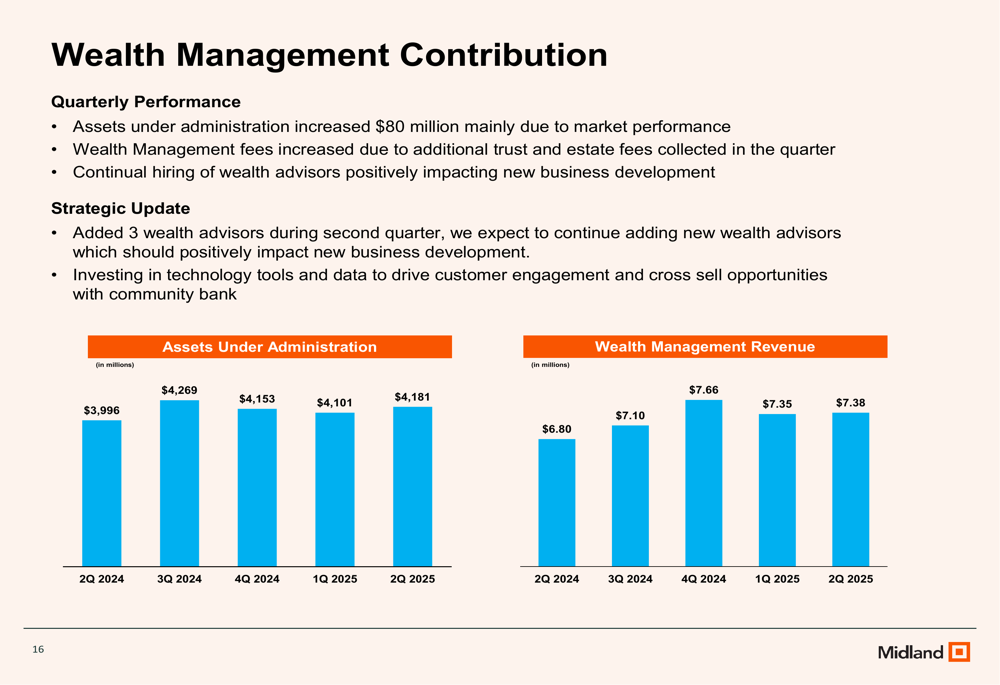

The bank’s wealth management business continues to be a bright spot, with assets under administration increasing by $80 million due to market performance. Wealth management fees increased due to trust and estate fees, and the bank added three wealth advisors while investing in technology tools:

Capital and Liquidity Position

Midland States emphasized its strong capital and liquidity position as a foundation for future growth. The bank reported a tangible book value of $20.68 per share, up $0.14 from the previous quarter and $0.85 from the prior year-end.

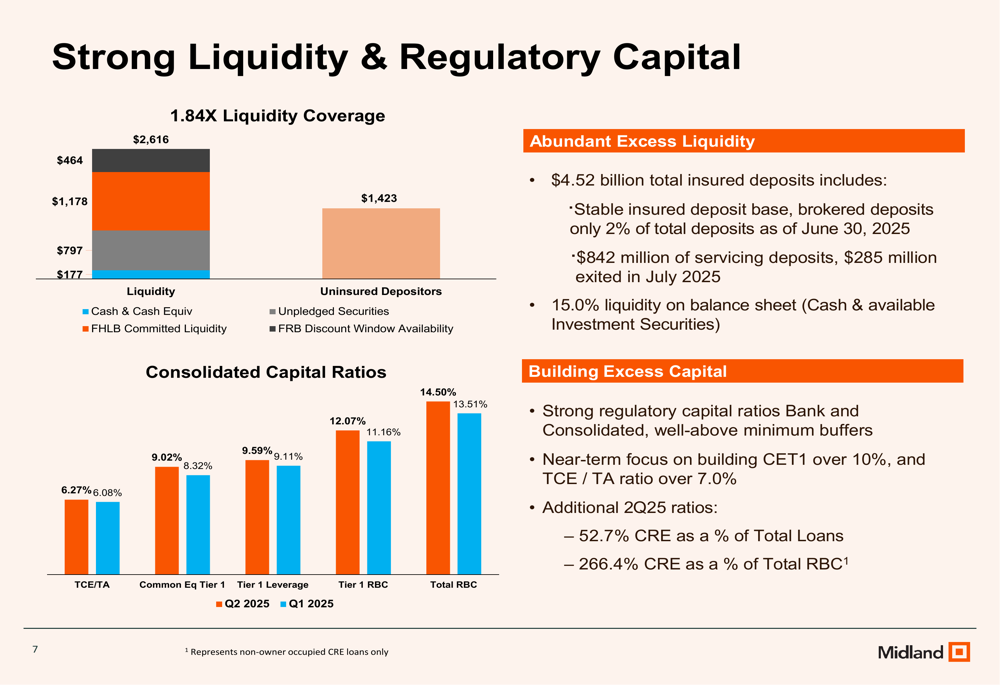

All capital ratios improved sequentially, with the TCE/TA ratio increasing 19 basis points to 6.3%. The consolidated Common Equity Tier 1 ratio stood at 9.02%, while the Total Capital ratio reached 14.50%.

The bank’s liquidity coverage and capital position are illustrated in the following slide:

Midland highlighted its 1.84x liquidity coverage, with insured deposits of $2,616 million and uninsured deposits at $1,423 million. The bank maintains a stable insured deposit base, with brokered deposits representing only 2% of total deposits as of June 30, 2025.

Strategic Initiatives and Outlook

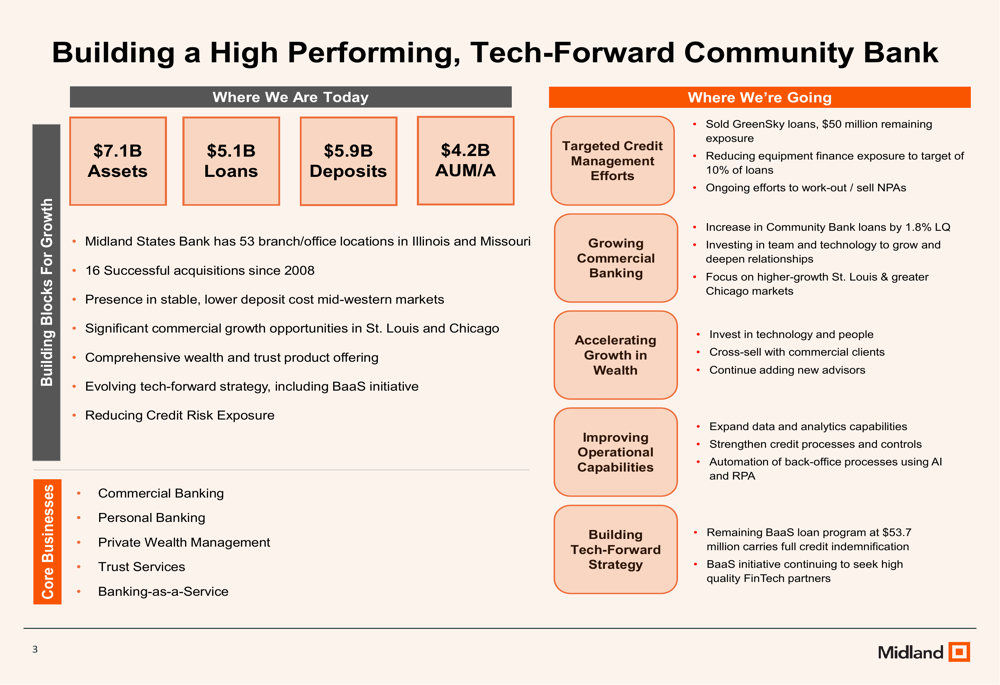

Looking ahead, Midland States outlined its strategy as a "high-performing, tech-forward community bank" with several key initiatives:

The bank’s financial outlook includes expectations for stable total assets in the near term, net interest margin expansion as short-term rates lower, reduced credit costs in 2026, continued community bank focus, growing regulatory capital, and unchanged focus on efficiency.

Management indicated a near-term focus on increasing the CET1 ratio to over 10% and the TCE/TA ratio to over 7.0%, signaling a commitment to further strengthening the bank’s capital position while pursuing growth in its core business segments.

As Midland States continues to navigate the challenging banking environment, its focus on credit remediation, core business growth, and capital strength positions it to potentially benefit from an improving interest rate environment while addressing legacy credit issues.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.