U.S. stock futures slip lower; Cook’s firing increases Fed independence worries

Introduction & Market Context

Mirion Technologies Inc (NYSE:MIR) released its second quarter 2025 earnings presentation on July 31, highlighting solid performance across key segments and improved free cash flow generation. The nuclear measurement and detection technology provider saw its stock rise 1.25% in aftermarket trading to $22.70, approaching its 52-week high of $22.80.

The company continues to benefit from growing momentum in the nuclear power sector, where utility companies are increasing capital expenditures from 9% of revenue in 2021-2024 to a projected 11% for 2025-2028. This trend supports Mirion’s expanding portfolio of nuclear safety and measurement solutions.

Quarterly Performance Highlights

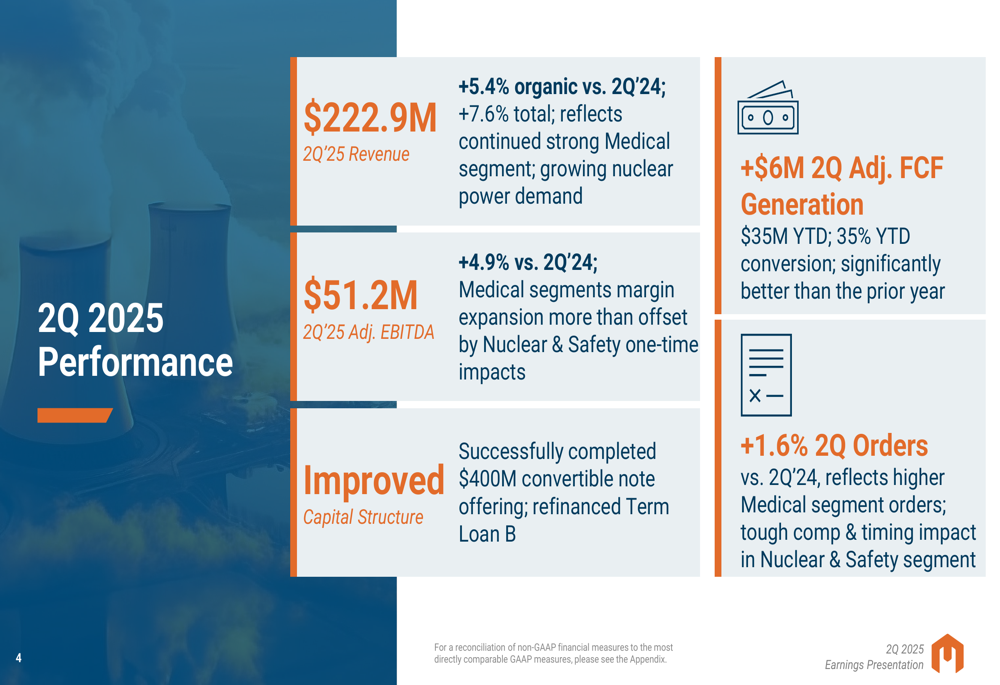

Mirion reported Q2 2025 revenue of $222.9 million, representing 7.6% total growth and 5.4% organic growth compared to the same period last year. Adjusted EBITDA reached $51.2 million, up 4.9% year-over-year, while adjusted diluted EPS came in at $0.13 per share.

As shown in the following financial performance summary:

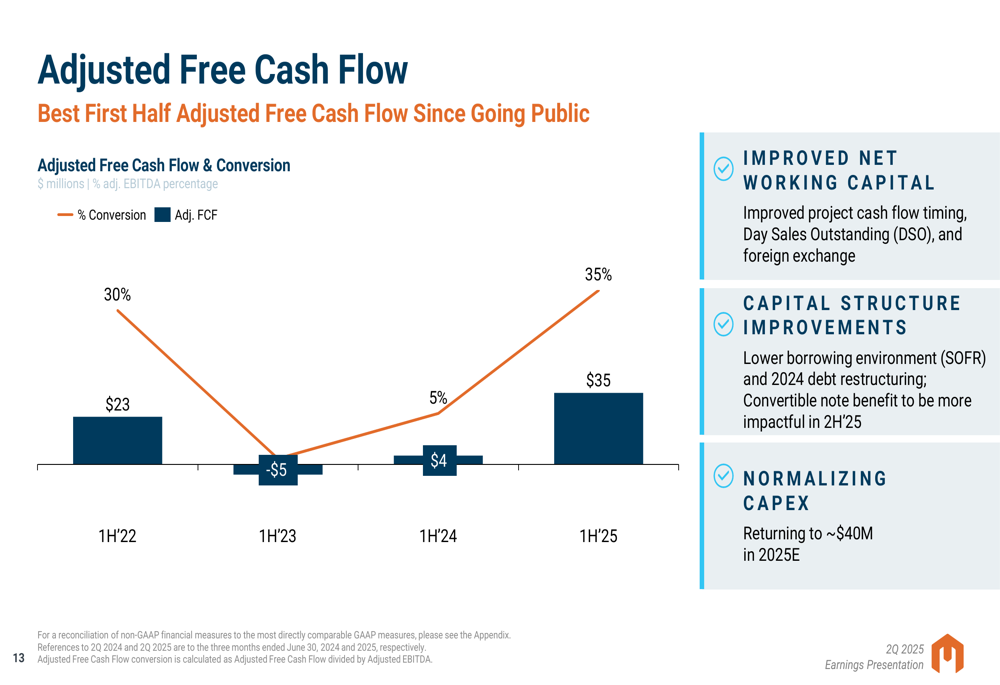

The company generated $6 million in adjusted free cash flow during the quarter, bringing the year-to-date total to $35 million with a 35% conversion rate. This marks the best first half adjusted free cash flow performance since Mirion went public, reflecting improved net working capital management and capital structure enhancements.

The free cash flow improvement trend is clearly illustrated in this chart:

Mirion also strengthened its financial position by successfully completing a $400 million convertible note offering and refinancing its Term Loan B, which should reduce interest expenses going forward.

Segment Performance

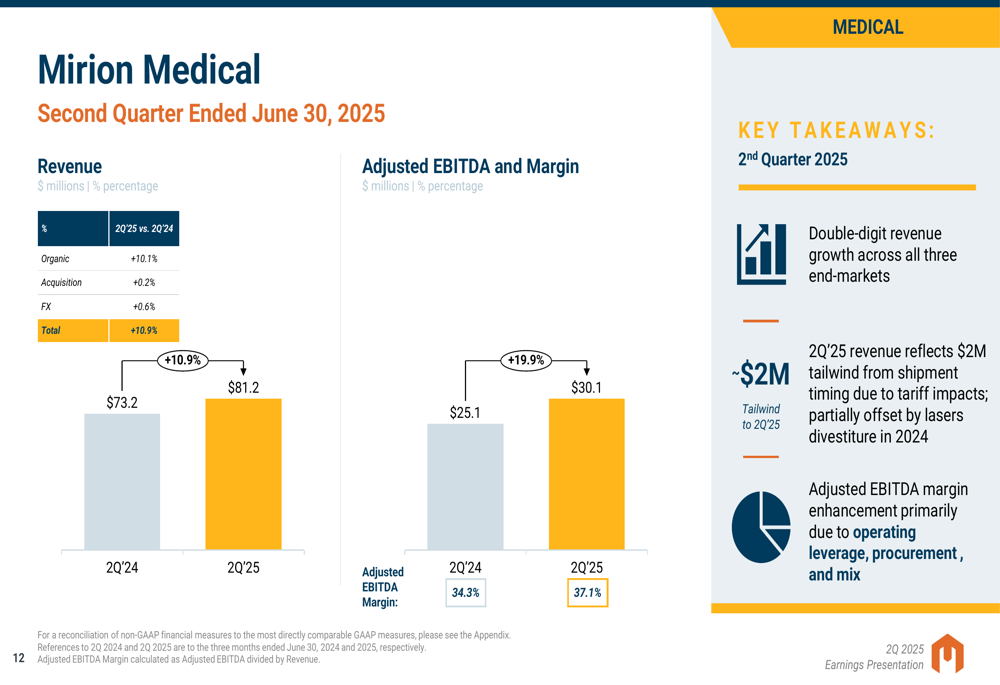

The Medical (TASE:BLWV) segment was a standout performer in Q2, with revenue increasing 10.9% to $81.2 million and organic growth of 10.1%. Adjusted EBITDA in this segment jumped 19.9% to $30.1 million, with margins expanding to 37.1%. Management attributed this strong performance to double-digit revenue growth across all three end-markets and improved operating leverage.

The Medical segment’s financial metrics show the impressive growth trajectory:

Meanwhile, the Nuclear & Safety segment reported revenue of $141.7 million, up 5.8% overall with 2.9% organic growth. However, adjusted EBITDA in this segment declined 2.6% to $37.9 million, with management citing negative impacts from product mix, a one-time cost true-up from a pre-public U.S. government contract, and project cost increases in France.

Despite these temporary headwinds, the Nuclear Power end market within this segment showed approximately 5% organic revenue growth in Q2 and 11% year-to-date growth, indicating strong underlying demand.

Strategic Initiatives

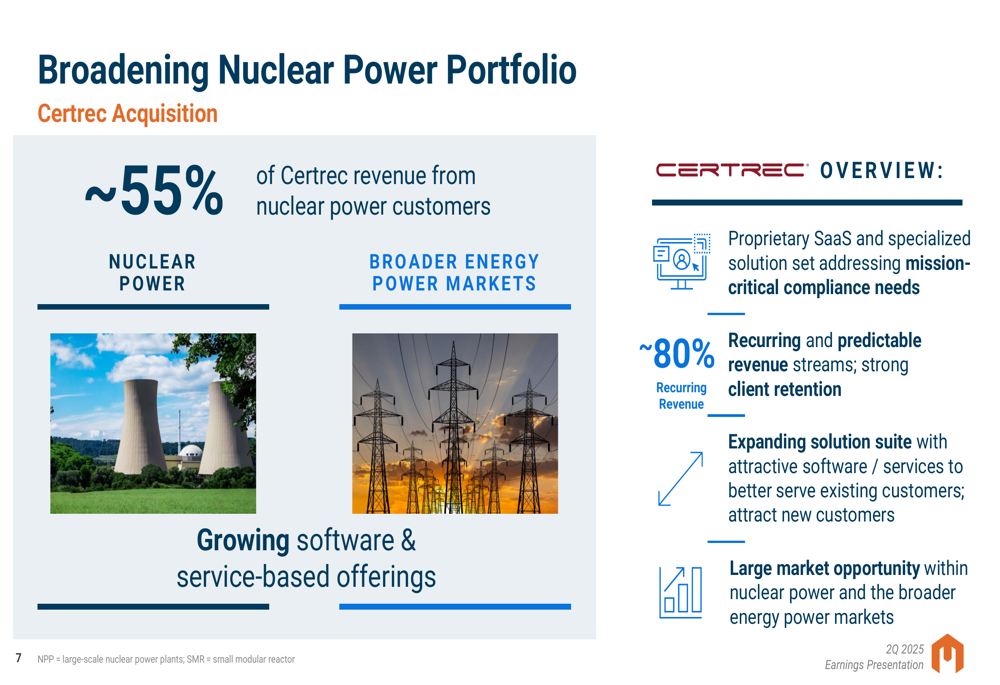

A key strategic development highlighted in the presentation was Mirion’s acquisition of Certrec, which expands the company’s nuclear software and services offerings. Approximately 55% of Certrec’s revenue comes from nuclear power customers, with the remainder from broader energy power markets.

The acquisition details reveal strong recurring revenue potential:

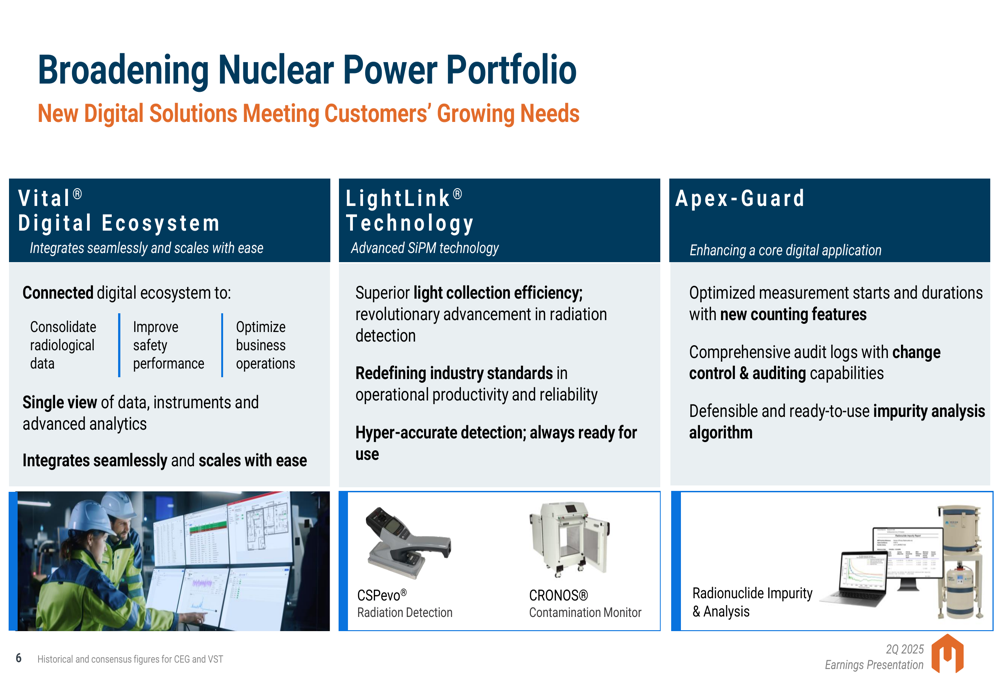

Mirion is also broadening its nuclear power portfolio with new digital solutions, including the Vital® Digital Ecosystem, LightLink® Technology, and Apex-Guard. These offerings enhance the company’s competitive position in the growing nuclear power market.

The expanded product portfolio is illustrated here:

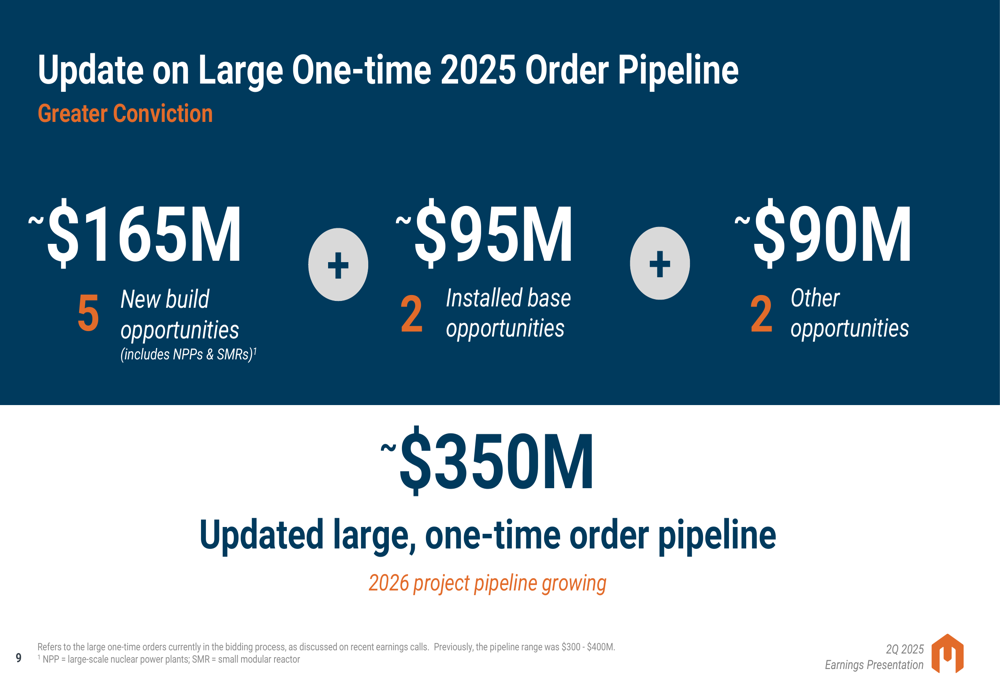

The company reported growing momentum in its large one-time order pipeline for 2025, with approximately $350 million in expected opportunities across new builds (including nuclear power plants and small modular reactors), installed base upgrades, and other projects.

The pipeline breakdown shows diversified growth opportunities:

Financial Outlook

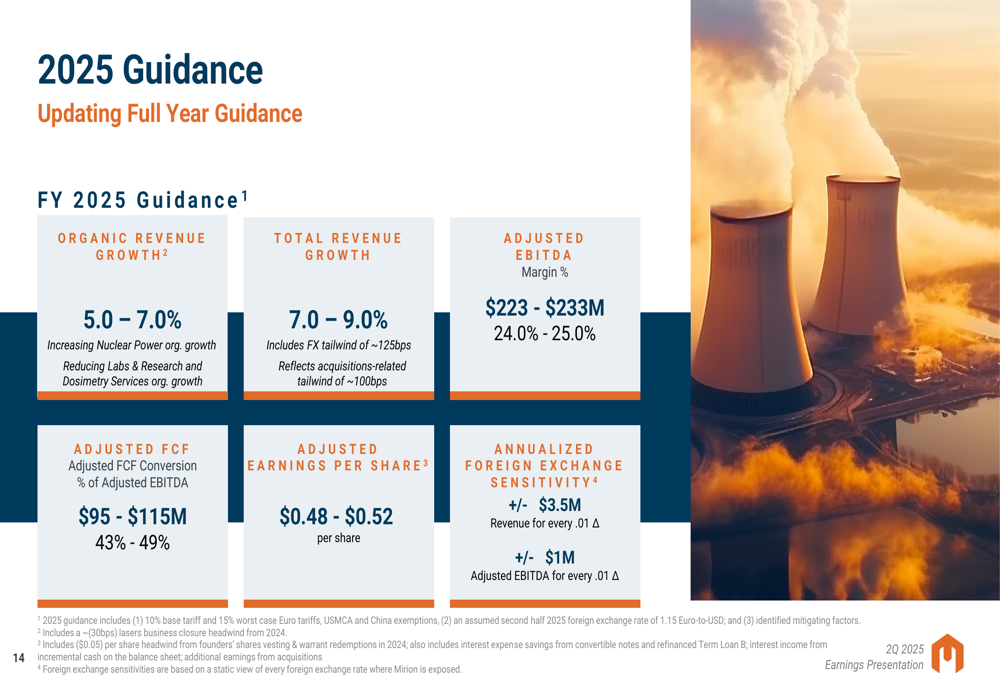

Mirion maintained its 2025 guidance, projecting organic revenue growth of 5.0-7.0% and total revenue growth of 7.0-9.0%. The company expects adjusted EBITDA between $223-$233 million and adjusted EPS of $0.48-$0.52.

The detailed guidance framework provides clear performance targets:

This outlook aligns with the company’s Q1 2025 performance, where Mirion exceeded analyst expectations with adjusted EPS of $0.10 against a forecast of $0.08, and revenue of $202 million versus the anticipated $199.34 million.

Management expressed confidence in accelerating order rates in the second half of 2025, noting approximately 10% year-to-date increase in Nuclear Power end-market orders and a growing small modular reactor (SMR) backlog. The company’s overall backlog stood at $819 million at the end of Q2 2025, providing visibility into future revenue streams.

With nuclear power gaining broader public support and utility companies increasing capital expenditures, Mirion appears well-positioned to capitalize on favorable industry trends while continuing to improve its operational efficiency and cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.