ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Mo-BRUK SA, a leader in Poland’s circular economy waste management sector, presented its Q1 2025 financial results on May 22, 2025, showing solid revenue growth and improved EBITDA margins despite facing some profitability challenges. The company, which trades on the Warsaw Stock Exchange (WSE:MBR), continues to strengthen its position across its three core business segments while successfully integrating its El-Kajo acquisition.

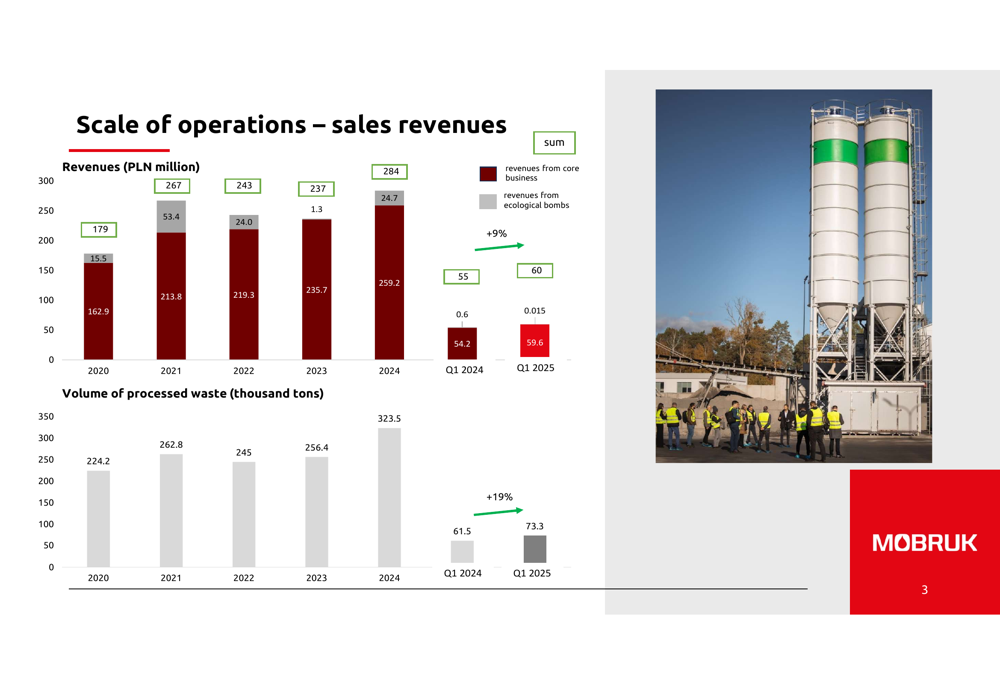

The waste management specialist reported a 10% year-over-year revenue increase for Q1 2025, reaching 59.6 million PLN, while processing volumes grew by 19.2% to 73.3 thousand tons. The company’s shares closed at 274 PLN following the presentation, up 0.18% for the day.

Quarterly Performance Highlights

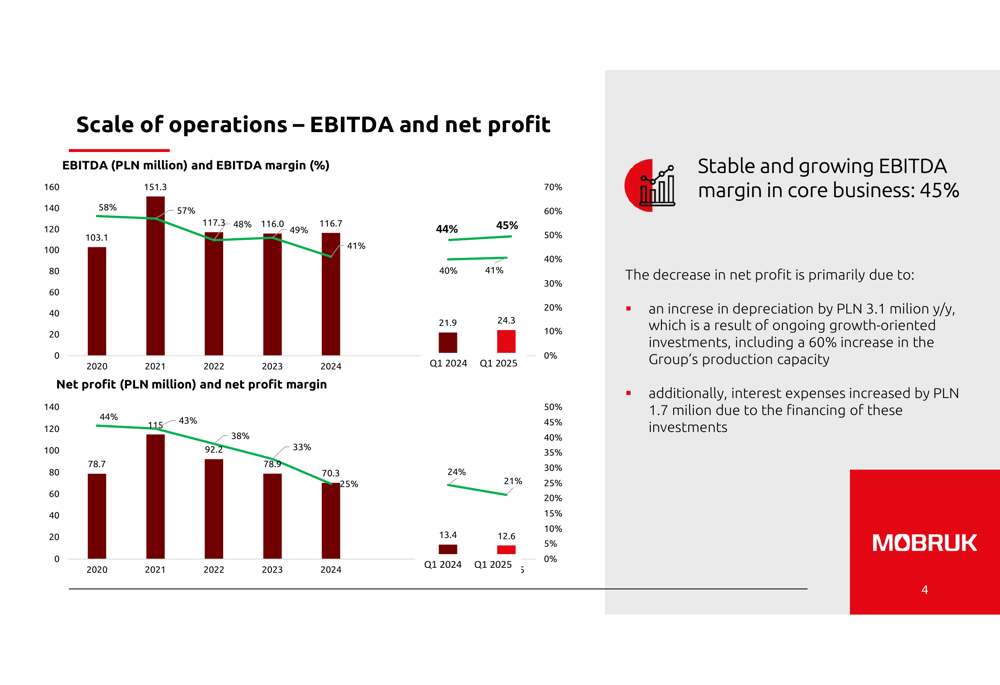

Mo-BRUK demonstrated strong operational performance in the first quarter of 2025, with revenue increasing to 59.6 million PLN from 54.2 million PLN in the same period last year. The company’s EBITDA grew to 24.3 million PLN, representing a 45% margin, up from 21.9 million PLN and a 40% margin in Q1 2024.

As shown in the following chart of EBITDA and net profit performance, the company has maintained strong profitability metrics over recent years:

Despite the improved EBITDA performance, net profit decreased slightly to 12.6 million PLN (21% margin) from 13.4 million PLN (24% margin) in Q1 2024. The company attributed this decline primarily to increased depreciation expenses and higher interest costs related to debt financing.

The company’s waste processing volumes showed significant growth, increasing from 61.5 thousand tons in Q1 2024 to 73.3 thousand tons in Q1 2025. This operational expansion is illustrated in the following chart:

Detailed Financial Analysis

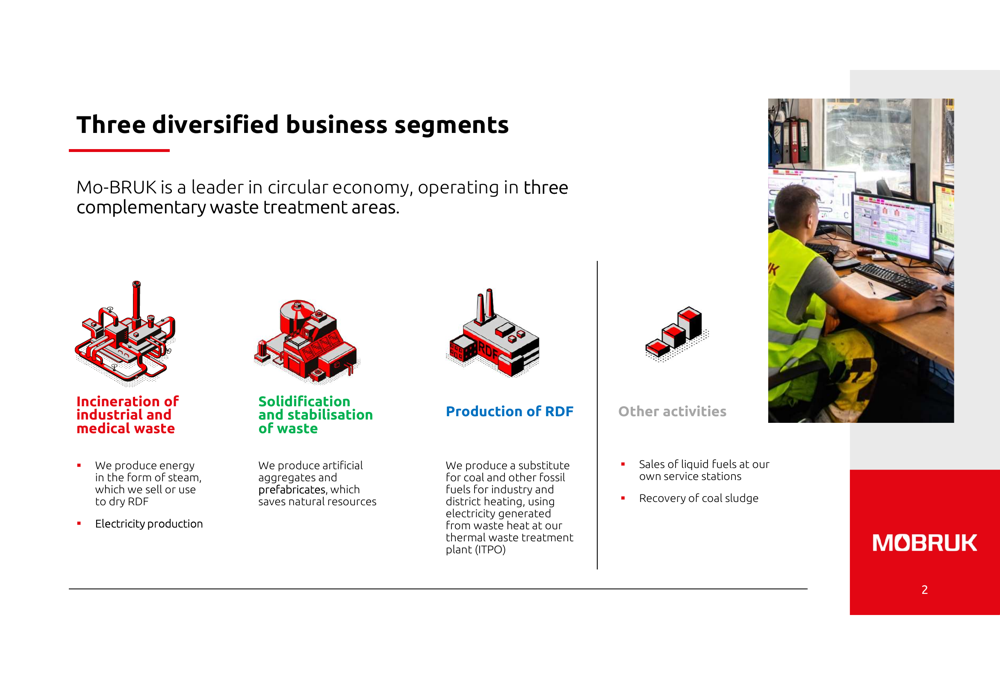

Mo-BRUK operates through three complementary business segments: incineration of industrial and medical waste, solidification and stabilization of waste, and production of RDF (Refuse Derived Fuel). The company’s diversified business model is illustrated below:

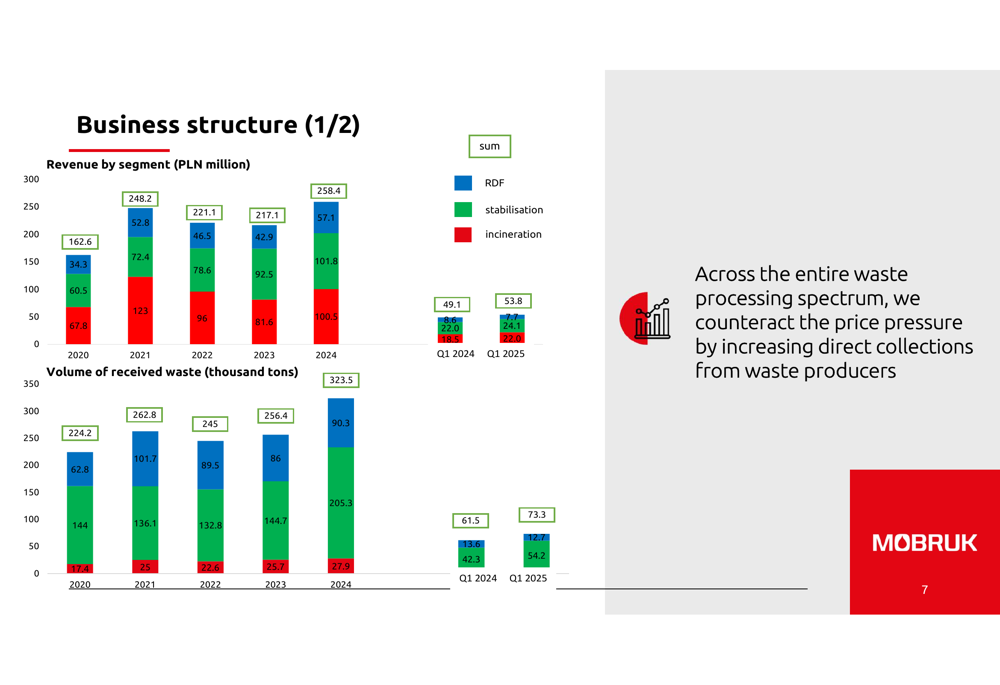

The segment performance shows varying results across the business units. The RDF segment demonstrated the strongest growth with revenue increasing by 30.3% to 24.1 million PLN in Q1 2025 compared to 18.5 million PLN in Q1 2024. The Stabilization segment grew by 11.7% to 8.6 million PLN, while the Incineration segment remained flat at 22 million PLN.

The following chart provides a detailed breakdown of revenue by segment and waste processing volumes:

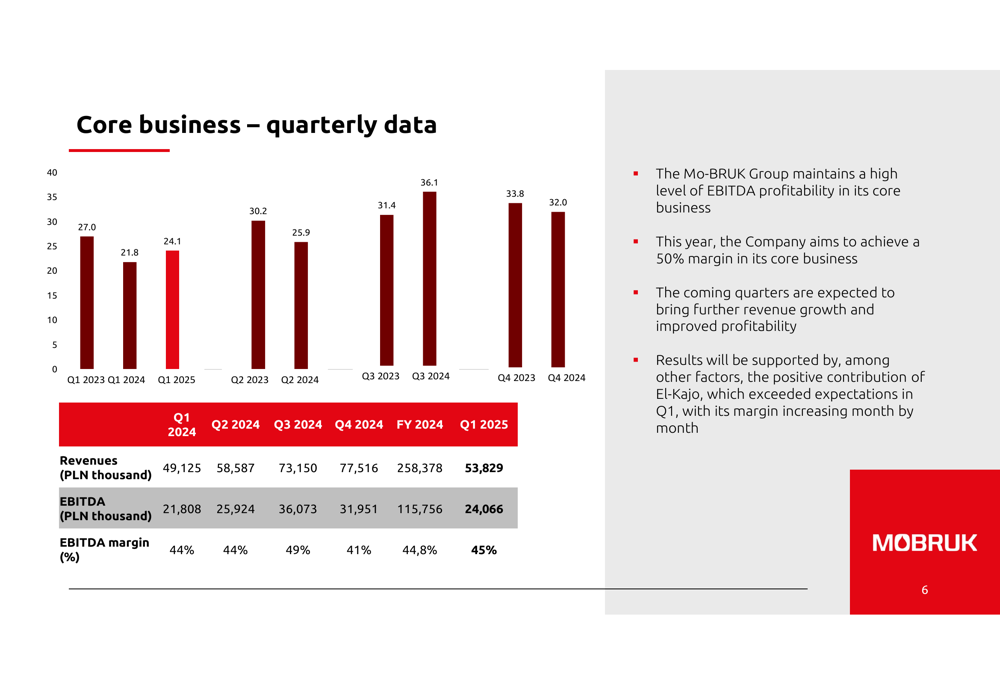

The company’s core business continues to maintain high profitability, with quarterly EBITDA margins consistently in the 40-49% range over the past year. Mo-BRUK has stated its aim to achieve a 50% EBITDA margin in its core business in 2025, as shown in the following quarterly performance data:

Strategic Initiatives

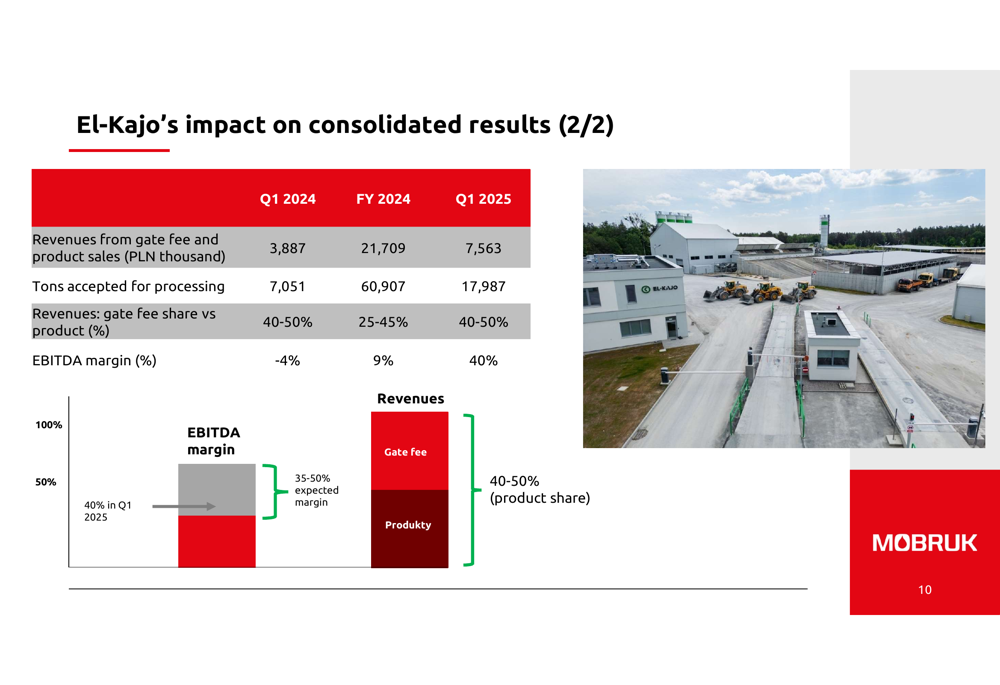

The integration of El-Kajo has proven to be a significant success story for Mo-BRUK. The acquisition has shown remarkable improvement in financial performance, with revenue nearly doubling from 3.89 million PLN in Q1 2024 to 7.56 million PLN in Q1 2025. More impressively, El-Kajo’s EBITDA margin jumped from -4% in Q1 2024 to 40% in Q1 2025, demonstrating successful operational integration.

The following chart illustrates El-Kajo’s financial transformation:

The company reported that El-Kajo has completed its investment process and achieved its target processing capacity of 220 thousand tons. The acquisition has expanded Mo-BRUK’s waste processing capabilities and customer portfolio, as detailed below:

Forward-Looking Statements

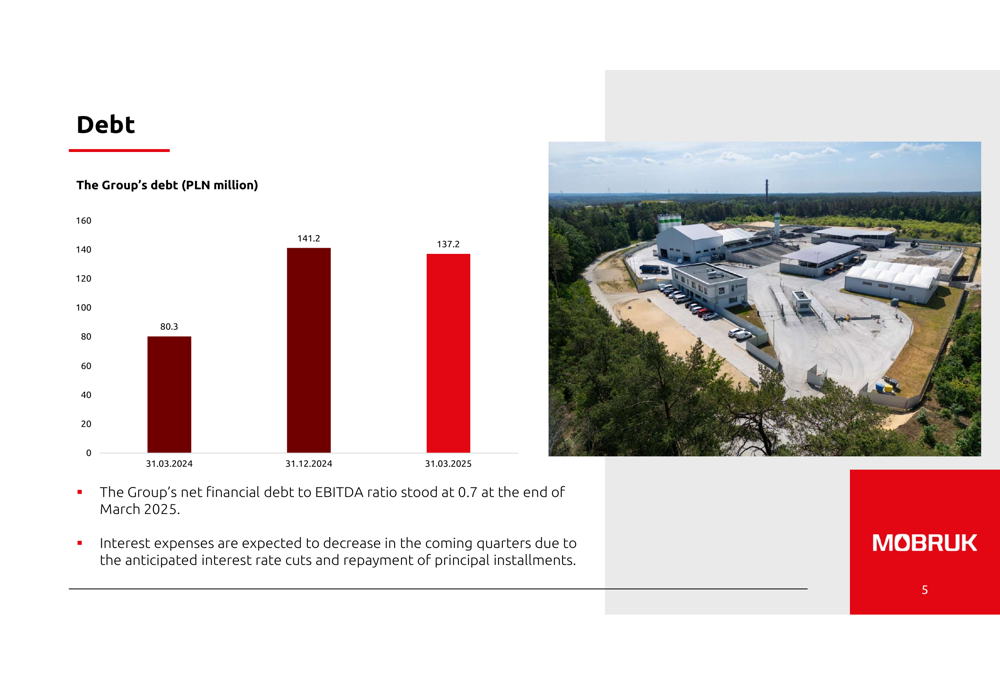

Mo-BRUK’s debt management shows a positive trend, with the company’s debt decreasing from 141.2 million PLN at the end of 2024 to 137.2 million PLN by March 31, 2025. The company’s net financial debt to EBITDA ratio stood at 0.7 at the end of Q1 2025, indicating a manageable leverage position.

The debt trends are illustrated in the following chart:

The company expects interest expenses to decrease in the coming quarters due to anticipated interest rate cuts in Poland and ongoing principal repayments. This should help improve net profit margins, which were pressured in Q1 2025 despite the strong operational performance.

Mo-BRUK is also making progress in energy efficiency and self-sufficiency. The company’s electricity production increased significantly, with the share of self-produced electricity rising from just 1% of consumption in Q1 2024 to 34% in Q1 2025. This improvement in energy management should help mitigate cost pressures and support margin expansion going forward.

With solid revenue growth, improving EBITDA margins, successful integration of El-Kajo, and prudent debt management, Mo-BRUK appears well-positioned to continue its growth trajectory through 2025 despite the challenges in net profit performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.